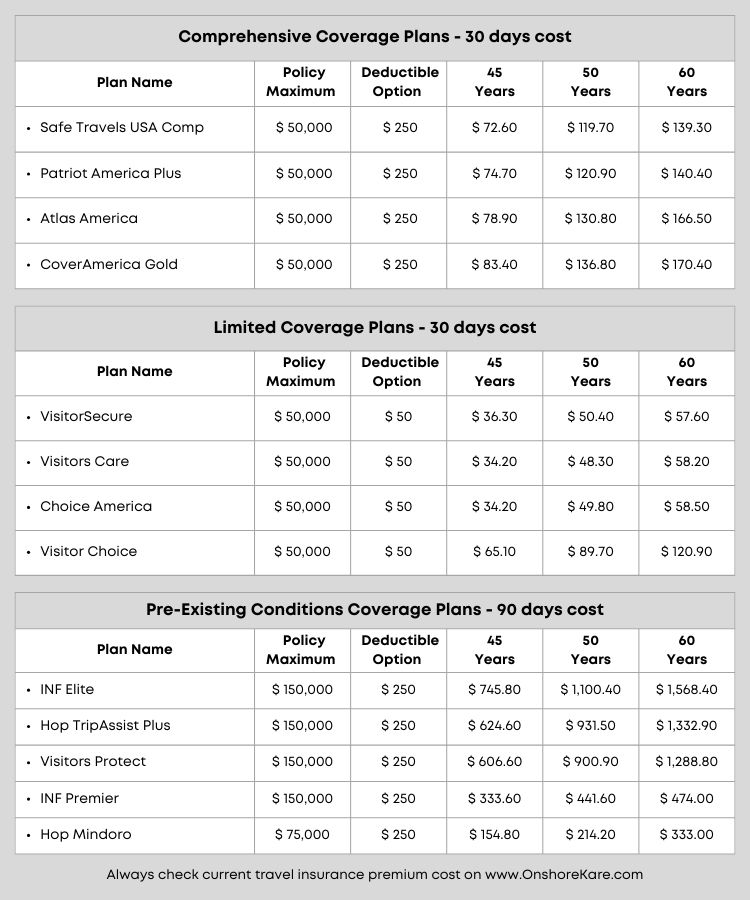

Travel Insurance Fees

Travel insurance fees can often catch travelers off guard, despite the growing awareness of the importance of coverage. While the cost of a policy may seem straightforward, various fees and hidden charges can significantly impact the final price.

These may include administrative fees, cancellation charges, or costs tied to pre-existing condition waivers. Understanding the fee structure is essential when comparing plans, as even similar policies can vary greatly in affordability and value. Consumers must scrutinize fine print, ask questions, and calculate total expenses before purchasing. A clear grasp of travel insurance fees ensures travelers are protected without paying more than necessary.

Understanding Travel Insurance Fees: What You Need to Know

Travel insurance is a crucial safeguard for travelers, offering financial protection against unexpected events such as trip cancellations, medical emergencies, lost baggage, and travel delays.

Difference Between Basic And Comprehensive Travel Insurance

Difference Between Basic And Comprehensive Travel InsuranceHowever, many travelers are unaware of the various fees associated with purchasing and using travel insurance. These fees can include policy premiums, administrative charges, claim processing fees, and costs tied to optional add-ons or upgrades. The total cost of travel insurance typically depends on factors like trip duration, destination, traveler age, coverage limits, and pre-existing medical conditions.

It's essential to read the fine print, as some policies may include hidden fees or apply charges for services such as emergency assistance or changes to the original plan. Comparing multiple policies and understanding the full fee structure ensures travelers get optimal coverage without unexpected expenses.

Types of Fees Included in Travel Insurance Plans

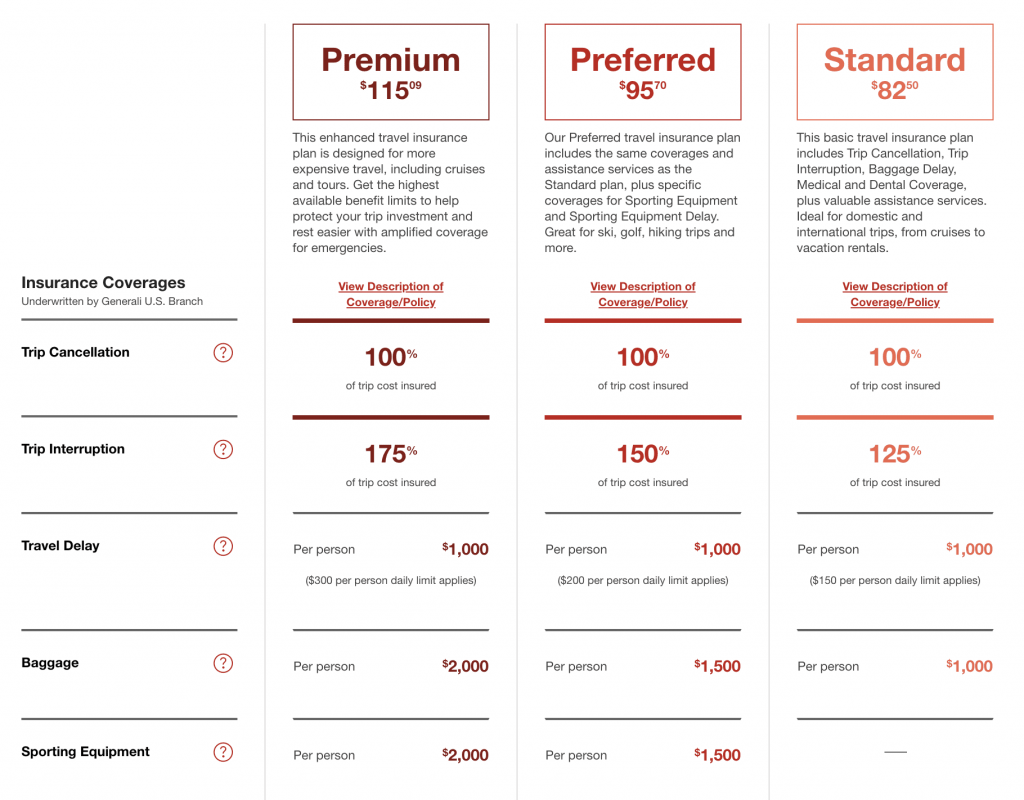

Travel insurance plans often include several types of fees beyond the base premium. The most obvious is the policy premium, which is the upfront cost of purchasing coverage and generally calculated as a percentage of the total trip cost. Additional fees may arise from optional coverages such as cancel-for-any-reason (CFAR) upgrades, premium medical coverage, or rental car protection.

Some insurers charge administrative or service fees for policy changes, customer support, or claim submission. Moreover, third-party providers involved in medical evacuations or concierge services might apply their own charges, which may not always be fully covered by the insurance. Understanding each fee component helps travelers avoid surprises and select a plan that offers transparency and value.

Expat Travel Insurance

Expat Travel InsuranceHow Age and Destination Impact Insurance Costs

Two of the most significant factors affecting travel insurance fees are the traveler's age and destination. Older travelers usually face higher premiums because insurers perceive them as having a greater risk of medical issues while abroad.

For instance, someone over 70 may pay significantly more than a traveler under 40 for the same coverage level. Destination also plays a critical role—trips to countries with high healthcare costs, such as the United States or Switzerland, typically trigger higher insurance premiums due to the potential for expensive medical claims.

Similarly, travel to regions with political instability or limited medical infrastructure may require more extensive (and costly) coverage. Assessing how these variables influence pricing helps travelers budget appropriately and choose suitable protection.

Comparing Insurance Providers and Fee Structures

When selecting travel insurance, comparing not only coverage limits but also fee structures across providers is essential. Some companies advertise low base premiums but include numerous附加 charges for services like 24/7 assistance, claim filing, or medical referrals. Others offer all-inclusive pricing, bundling most services without extra fees. Reputable insurers provide clear breakdowns of all potential costs in the policy documentation.

Expatriate Travel Insurance

Expatriate Travel InsuranceIndependent comparison websites and customer reviews can also shed light on which providers are transparent about fees and deliver reliable service. Travelers should pay attention to both the upfront cost and long-term value, considering how easily claims are processed and whether additional service charges could diminish the benefits of a seemingly low-priced plan.

| Insurance Provider | Base Premium (7-day trip) | Claim Processing Fee | CFAR Option Fee | Customer Support Fee |

|---|---|---|---|---|

| Allianz Travel | $65 | None | $35 | None |

| World Nomads | $78 | None | Included | None |

| TravelGuard | $58 | $25 | $40 | None |

| InsureMyTrip | $70 | None | $30 | None |

| Historic Average | $68 | $15 | $36 | $10 |

Understanding Travel Insurance Fees: A Comprehensive Guide

What are the typical fees for travel insurance coverage?

Factors That Influence Travel Insurance Costs

The cost of travel insurance can vary significantly depending on several key factors that insurers evaluate when calculating premiums. Understanding these elements helps travelers anticipate potential expenses and choose a plan that fits their budget and needs.

- Travelers' age plays a major role in determining insurance costs; older travelers often face higher premiums due to increased health risks, while younger individuals may benefit from lower rates.

- The total trip cost directly impacts the insurance price because most policies cover a percentage of the trip’s value, typically ranging from 4% to 10% of the total amount spent on non-refundable bookings.

- Destination influences pricing as well—trips to regions with high medical costs (like the United States) or areas with travel advisories usually result in higher premiums due to increased risk exposure.

Types of Travel Insurance and Associated Fees

Different types of travel insurance plans offer varying levels of protection, and each comes with its own pricing structure based on coverage depth and specific benefits included.

- Basic travel insurance plans, which usually cover trip cancellation, baggage loss, and emergency medical expenses, typically cost between $40 and $120 for a week-long domestic or international trip.

- Comprehensive plans, adding coverage for travel delays, rental car damage, and non-medical evacuations, generally range from $100 to $250, depending on trip length and destination.

- Specialty plans, such as those designed for adventure sports, cruises, or senior travelers, may cost 20% to 50% more than standard policies to account for higher-risk activities or age-related health concerns.

Average Percentage of Trip Cost Spent on Insurance

A common metric used to evaluate travel insurance expenses is the percentage of the total trip cost allocated toward the premium. This helps travelers assess the relative value of insurance compared to their overall investment.

- On average, travelers pay between 4% and 8% of their total trip cost for a standard travel insurance policy, meaning a $5,000 trip could incur insurance fees from $200 to $400.

- Premiums may exceed 10% for trips involving high-risk destinations, extended durations, or travelers with pre-existing medical conditions requiring additional coverage riders.

- Discounts and bundling options, such as purchasing insurance through a travel provider or credit card, can reduce the final cost by 10% to 25%, bringing the effective rate closer to 3% to 6% of the trip cost.

What are the typical travel insurance fees for a $5000 trip?

The typical cost of travel insurance for a $5000 trip generally ranges from $250 to $500, which is approximately 5% to 10% of the total trip cost. Several factors influence this price, including the traveler’s age, destination, length of the trip, level of coverage, and any pre-existing medical conditions.

For instance, older travelers or those visiting high-risk destinations may face higher premiums. Comprehensive plans that cover trip cancellation, medical emergencies, and baggage loss tend to fall on the higher end of the price range, while basic policies covering only essential elements may be more affordable.

Factors That Influence Travel Insurance Costs

- Traveler’s age: Older individuals typically pay more due to higher health risks, with insurers considering age a major pricing factor in underwriting policies.

- Destination: Trips to countries with expensive healthcare systems, such as the United States, or regions with political instability often result in higher insurance costs.

- Duration of the trip: Longer trips increase the likelihood of incidents occurring, leading to higher premiums to cover the extended period of coverage.

Different Types of Coverage and Their Impact on Price

- Basic plans: These often include minimal benefits like emergency medical coverage or simple trip interruption protection and can cost as low as $150 for a $5000 trip.

- Comprehensive plans: Including benefits such as trip cancellation, 24/7 assistance, baggage and rental car coverage, these typically range from $350 to $500, offering broader protection.

- Specialized add-ons: Optional upgrades—like cancel for any reason (CFAR) or adventure sports coverage—can increase the base price by 40% to 50%, depending on included benefits.

How to Get the Best Rate for a $5000 Trip

- Compare multiple providers: Using comparison tools allows consumers to evaluate coverage details and pricing from various insurers tailored to a $5000 trip budget.

- Purchase early: Buying insurance shortly after making the initial trip deposit may secure lower rates and qualify for time-sensitive benefits like CFAR.

- Assess actual needs: Avoid over-insuring by identifying necessary coverage—for example, skipping rental car insurance if already covered by a personal auto policy or credit card.

What is the average cost of $10,000 travel insurance coverage?

The average cost of $10,000 travel insurance coverage typically ranges from $40 to $90 for a week-long trip, depending on several factors such as the traveler’s age, destination, duration of travel, and the specific benefits included in the policy. Basic travel insurance plans offering $10,000 in medical coverage often cover emergency medical expenses, limited trip interruption, and minor baggage protection.

Budget-friendly plans from providers like SafetyWing or World Nomads may fall on the lower end, while comprehensive policies from larger insurers like Allianz or GeoBlue may cost more but offer additional services and broader networks. Cost also increases significantly for older travelers or for trips to high-cost medical destinations such as the United States.

Factors Influencing the Cost of $10,000 Travel Insurance Coverage

- Traveler’s age plays a major role—premiums generally increase with age due to higher health risks, making a 60-year-old’s plan notably more expensive than a 30-year-old’s for the same coverage amount.

- Destination matters greatly; medical care in countries like the U.S., Canada, or Western Europe is more costly, so insurers adjust premiums to reflect the potential expense of emergency treatment.

- The length of the trip impacts pricing as well—insurers assess risk over time, so a 10-day trip will cost more than a 3-day trip, even with the same $10,000 coverage limit.

Coverage Components Included in $10,000 Travel Insurance Policies

- Emergency medical expenses are the core component—this includes hospital stays, doctor visits, and emergency procedures up to the policy’s $10,000 limit.

- Medical evacuation is often included or available as an add-on, covering transportation to the nearest adequate medical facility or back home if needed after stabilization.

- Additional benefits such as trip interruption, accidental death & dismemberment, and limited personal belongings protection are sometimes bundled but vary widely by plan.

How to Find Affordable $10,000 Travel Insurance Coverage

- Compare multiple providers online using comparison tools from sites like InsureMyTrip or SquareMouth to evaluate plans offering $10,000 medical coverage at competitive rates.

- Consider membership-based or subscription-style travel medical insurance, such as SafetyWing or Atlas International, which offer flexible and cost-effective options for digital nomads or frequent travelers.

- Read the fine print carefully—cheaper plans may have lower reimbursement rates, exclusions for pre-existing conditions, or limited provider networks, so understanding the terms is essential before purchasing.

Frequently Asked Questions

What factors influence travel insurance fees?

Travel insurance fees are influenced by several factors, including trip cost, destination, length of travel, and the traveler’s age. Higher coverage limits and added benefits like adventure sports coverage or cancel-for-any-reason options also increase the cost. Pre-existing medical conditions may affect pricing, as can the level of medical and evacuation coverage selected. Comparing plans and understanding what each includes helps travelers find a suitable and fairly priced policy.

Are travel insurance fees refundable if I cancel my policy?

Yes, many travel insurance policies offer a money-back guarantee during a review period, typically 10 to 14 days after purchase, as long as you haven’t started your trip or filed a claim. After this window, refunds may not be available unless the policy specifically allows it. Always check the insurer's cancellation and refund policy before purchasing to understand your options and avoid unexpected fees.

How much should I expect to pay for travel insurance fees?

Travel insurance typically costs between 4% and 10% of your total trip cost. For a $5,000 trip, this means paying $200 to $500. Factors like destination, traveler age, coverage options, and trip length influence the final price. Comprehensive plans with higher medical coverage or cancellation benefits usually cost more. Getting multiple quotes helps compare fees and coverage to find the best value.

Do travel insurance fees cover medical emergencies abroad?

Yes, most travel insurance plans include coverage for unexpected medical emergencies abroad, but the extent of coverage depends on the policy. Fees paid contribute to benefits like emergency treatment, hospital stays, and medical evacuation. However, pre-existing conditions or high-risk activities may require additional coverage. Always review the policy details to ensure adequate medical protection based on your destination and health needs.

Leave a Reply