Unitedhealthcare Individual Health Insurance Plans

UnitedHealthcare offers a range of individual health insurance plans designed to meet diverse healthcare needs across the United States. These plans provide access to a broad network of physicians, specialists, and hospitals, ensuring members can receive quality care when and where they need it.

With options including Health Maintenance Organization (HMO), Preferred Provider Organization (PPO), and High-Deductible Health Plans (HDHPs) paired with Health Savings Accounts (HSAs), UnitedHealthcare allows individuals to select coverage based on their budget, preferred providers, and medical requirements.

Plans often include preventive services, prescription drug coverage, telehealth options, and wellness programs. This flexibility makes UnitedHealthcare a competitive choice for those seeking reliable, customizable individual health insurance.

Auto Insurance West Jordan Utah

Auto Insurance West Jordan UtahUnderstanding UnitedHealthcare Individual Health Insurance Plans

UnitedHealthcare offers a comprehensive range of individual health insurance plans designed to meet the diverse needs of people seeking coverage outside employer-sponsored programs. These plans are ideal for self-employed individuals, early retirees, and anyone without access to group health benefits.

UnitedHealthcare provides multiple plan options, including Health Maintenance Organization (HMO), Preferred Provider Organization (PPO), and High Deductible Health Plans (HDHPs) paired with Health Savings Accounts (HSAs), giving enrollees flexibility in choosing their level of coverage and cost-sharing. Each plan is structured with varying deductibles, copayments, and out-of-pocket maximums, enabling consumers to balance monthly premiums with potential medical expenses.

Coverage typically includes essential health benefits such as hospitalization, emergency services, prescription drugs, maternity care, and preventive services, all in compliance with the Affordable Care Act (ACA). UnitedHealthcare also supports members through digital tools like the myUHC portal, mobile app access, and 24/7 nurse advice lines, enhancing the user experience and overall care coordination.

Types of UnitedHealthcare Individual Health Plans

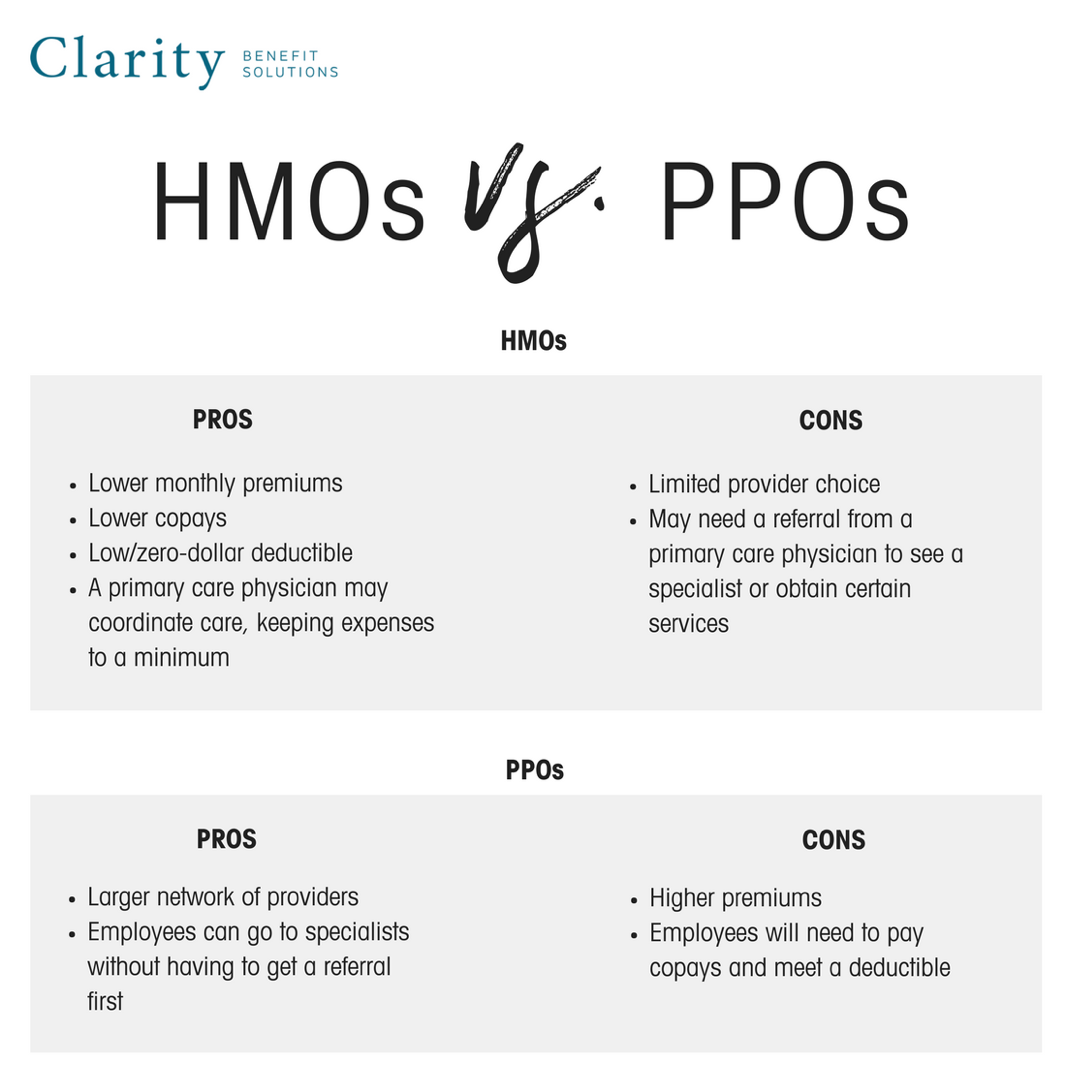

UnitedHealthcare offers several types of individual health insurance plans to suit different healthcare needs and financial situations. The HMO plans require members to use a defined network of doctors and hospitals and generally require referrals to see specialists, making them a cost-effective option with lower premiums.

Auto Insurance Westfield

Auto Insurance WestfieldIn contrast, PPO plans offer more flexibility by allowing access to both in-network and out-of-network providers without a referral, though services outside the network often cost more. HDHPs are ideal for healthy individuals who want lower monthly premiums and are comfortable paying higher deductibles; these plans are HSA-eligible, offering valuable tax advantages for saving or paying medical expenses.

Additionally, UnitedHealthcare provides catastrophic plans for eligible individuals under 30 or those who qualify for a hardship exemption, offering low premiums and high out-of-pocket costs as protection against worst-case medical scenarios. Each plan type balances cost and access, enabling consumers to choose based on personal preferences and medical needs.

Benefits and Coverage Included in UnitedHealthcare Plans

UnitedHealthcare individual plans cover all ten essential health benefits mandated by the ACA, ensuring comprehensive protection for policyholders. These include ambulatory patient services, mental health and substance use disorder treatment, prescription medications, rehabilitative services, and pediatric services, including dental and vision care for children.

Preventive care, such as vaccinations, cancer screenings, and wellness visits, is typically covered at 100% with no cost-sharing when delivered by in-network providers. Members also gain access to UnitedHealthcare’s extensive provider network, one of the largest in the U.S., which includes millions of doctors, clinics, and hospitals.

Auto Manufacturer Insurance

Auto Manufacturer InsuranceAdditional perks may include telehealth services for non-emergency consultations, fitness programs like SilverSneakers® (for eligible members), and tools for managing prescriptions through the OptumRx® platform. This broad coverage supports holistic health management and reduces long-term healthcare costs through early detection and preventive care.

How to Enroll in a UnitedHealthcare Individual Plan

Enrollment in a UnitedHealthcare individual health insurance plan can be done during the Annual Open Enrollment Period (OEP), which typically runs from November 1 to January 15, or through a Special Enrollment Period (SEP) if you experience a qualifying life event such as marriage, birth of a child, loss of other coverage, or relocation.

Individuals can apply directly through the UnitedHealthcare website, via healthcare.gov or a state-based exchange, or with the help of a licensed insurance agent. During the application process, applicants must provide personal information, household income details, and residency status to determine eligibility for premium tax credits or cost-sharing reductions under the ACA.

Once enrolled, members receive an insurance ID card and gain immediate access to benefits, provider networks, and customer support tools. It's crucial to compare plan details carefully—such as the provider network, formulary, and total out-of-pocket costs—to ensure the selected plan aligns with your healthcare usage and financial goals.

Auto Owners Insurance Phone Number Claims

Auto Owners Insurance Phone Number Claims| Plan Type | Key Features | Ideal For |

|---|---|---|

| HMO | Requires primary care physician (PCP) and referrals; lower costs; in-network only (except emergencies) | Individuals who prefer lower premiums and consistent care within a local network |

| PPO | No referrals needed; coverage for in-network and out-of-network care; higher premiums | Those who value provider flexibility and are willing to pay more for broader access |

| HDHP with HSA | High deductible; eligible for HSA with triple tax advantages; lower monthly premiums | Healthy individuals seeking long-term savings and tax benefits |

Comprehensive Guide to UnitedHealthcare Individual Health Insurance Plans

What is the cost of a UnitedHealthcare individual health insurance plan?

The cost of a UnitedHealthcare individual health insurance plan varies significantly depending on multiple factors such as geographic location, age, plan type, coverage level, and personal health status.

UnitedHealthcare offers a range of plans through the Health Insurance Marketplace (under the Affordable Care Act) and directly through their website, with monthly premiums typically ranging from around $200 to over $600 for individuals.

However, those who qualify for government subsidies may pay substantially less. In addition to premiums, individuals must also consider out-of-pocket costs such as deductibles, copayments, and coinsurance, which can greatly influence the total annual cost of a plan.

Auto Quotes Insurance New Jersey

Auto Quotes Insurance New JerseyFactors That Influence UnitedHealthcare Individual Plan Costs

- Location: Insurance premiums vary by state and even by ZIP code due to differences in healthcare provider costs, state regulations, and regional health risks. For example, a 30-year-old in rural Iowa may pay less than someone of the same age in New York City for the same coverage tier.

- Age and Health Status: Federal law allows insurers to vary premiums based on age, with older adults typically paying more. While pre-existing conditions cannot be used to deny coverage or increase costs, overall health can impact utilization of services, indirectly affecting total costs.

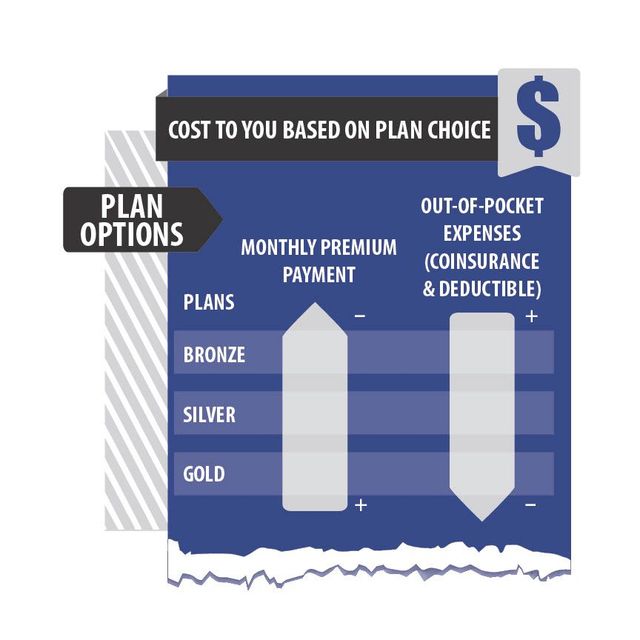

- Plan Tier and Network: UnitedHealthcare offers Bronze, Silver, Gold, and Platinum plans. Bronze plans have the lowest monthly premiums but higher out-of-pocket costs when care is needed, while Platinum plans reverse this balance. Additionally, choosing a plan with a narrow provider network (such as an EPO or HMO) often reduces premium costs compared to PPO plans with wider access.

- Monthly premiums for UnitedHealthcare individual plans depend heavily on the level of coverage and whether the plan is purchased through the Marketplace. On average, unsubsidized premiums start around $200 per month for basic Bronze-tier plans and can exceed $800 for comprehensive Platinum plans in high-cost areas.

- Individuals with household incomes between 100% and 400% of the federal poverty level may qualify for premium tax credits through the Health Insurance Marketplace. These subsidies reduce monthly payments significantly. For example, someone earning $45,000 per year may see their premium reduced by 50% or more, depending on location and family size.

- It is essential to renew coverage annually during open enrollment and reassess subsidy eligibility, as changes in income or household size can alter the amount of financial assistance available. UnitedHealthcare does not administer subsidies directly, but it partners with the Marketplace to help applicants identify the best-cost plan for their budget.

- Deductibles vary widely across UnitedHealthcare plans, ranging from a few hundred dollars in Platinum plans to thousands of dollars in high-deductible health plans (HDHPs), especially Bronze-tier options. A deductible is the amount you must pay for covered services before the insurance begins to pay.

- Copayments and coinsurance are additional cost-sharing elements. A typical doctor’s visit may have a $30–$50 copay, while coinsurance (e.g., 20% of the cost) applies after the deductible is met for services like hospital stays or specialist care. Knowing these amounts helps predict true annual healthcare spending.

- Maximum out-of-pocket limits protect consumers from catastrophic expenses. In 2024, the ACA sets this limit at $9,450 for an individual on most plans. Once this threshold is reached, UnitedHealthcare covers 100% of covered in-network services for the rest of the year, regardless of the initial deductible or coinsurance structure.

Which private health insurance provider offers the best individual plans compared to Unitedhealthcare?

Top Competitors to UnitedHealthcare for Individual Health Insurance Plans

- Blue Cross Blue Shield (BCBS) is one of the most extensive health insurance networks in the United States, offering individual plans through its network of independent state-based companies. Their broad provider network gives members access to care in nearly every county, making it a strong alternative to UnitedHealthcare, especially for those who travel frequently or live in rural areas. BCBS plans often include comprehensive coverage options with flexibility in selecting deductibles and out-of-pocket maximums.

- With a deep focus on Medicare and individual marketplace plans, Aetna, a CVS Health company, offers competitive individual health insurance options across many states. Aetna stands out for its integration with retail health clinics at CVS, providing convenient access to care and prescription benefits. Their networks are robust in urban and suburban regions, and they often include digital tools for health management that appeal to tech-savvy consumers.

- Kaiser Permanente is another major provider that differentiates itself through an integrated care model, combining insurance and health care delivery under one system. This approach improves care coordination and can reduce costs for members, particularly in states like California, Oregon, and Washington where Kaiser has a strong presence. However, its coverage is limited to specific regions, which makes it less accessible than UnitedHealthcare nationwide.

Key Factors to Compare When Evaluating Individual Plans

- When comparing UnitedHealthcare to other providers, network size and access to providers are essential. UnitedHealthcare boasts one of the largest networks in the country, but BCBS may surpass it in certain regions due to its local affiliate structure. It’s important to verify whether your preferred doctors, hospitals, and specialists are in-network with each provider, as out-of-network care can lead to significantly higher out-of-pocket costs.

- Premiums, deductibles, and out-of-pocket maximums vary widely across insurers and plans. While UnitedHealthcare offers a range of tiered plans (bronze, silver, gold, platinum), so do competitors like Aetna and BCBS. Shoppers should evaluate the full cost structure rather than focusing solely on monthly premiums. For instance, a plan with a lower premium but a high deductible may result in greater expenses during medical events.

- Additional benefits such as wellness programs, telehealth services, prescription drug coverage, and mental health support also influence the value of a plan. UnitedHealthcare’s Optum subsidiary provides robust telehealth and pharmacy services, but Aetna’s partnership with CVS enhances prescription affordability and convenience. Kaiser members benefit from seamless access to virtual visits and preventive care within their closed system, improving long-term health outcomes.

Regional Availability and Plan Customization Options

- UnitedHealthcare operates in most states and offers individual plans both on and off the Health Insurance Marketplace, providing flexibility for diverse needs. However, regional providers often outperform national insurers in localized areas. For example, Kaiser Permanente offers highly coordinated, high-quality care in the West Coast and Mid-Atlantic but is not available in many Southern or Midwestern states, limiting its appeal for national coverage.

- BCBS plans are customized by local affiliates, meaning benefits, pricing, and networks differ from state to state. This allows for greater alignment with regional health care markets but requires careful comparison across locations. In some areas, BCBS may have stronger hospital partnerships than UnitedHealthcare, particularly with community-based or nonprofit hospitals.

- Aetna has streamlined its individual offerings in recent years, focusing on key states with high demand for Affordable Care Act (ACA) plans. Their digital platform allows users to compare plans based on cost, coverage, and provider access, making customization easier. While not as widely available as UnitedHealthcare, Aetna remains a top-tier option in metropolitan areas where its network is well-developed and highly rated for customer satisfaction.

What are the drawbacks of UnitedHealthcare individual health insurance plans for seniors?

Limited Provider Networks and Access to Care

- UnitedHealthcare individual health insurance plans often operate with restricted provider networks, which can limit seniors' choices when selecting doctors, hospitals, and specialists. This is especially problematic for older adults who may already have established relationships with certain healthcare providers.

- If a senior requires care while traveling or relocating, they may find that out-of-network services are either not covered or come with significantly higher out-of-pocket costs, reducing the plan's flexibility.

- Specialists, particularly in rural or underserved areas, may not be part of UnitedHealthcare's network, making it difficult for seniors with chronic conditions or complex health needs to access necessary treatments.

Out-of-Pocket Costs and Financial Burden

- While monthly premiums for UnitedHealthcare individual plans may appear affordable, seniors often face high deductibles, copayments, and coinsurance that can add up quickly, especially with frequent medical visits or hospitalizations.

- Some plans may lack comprehensive coverage for critical senior-related services such as long-term care, routine vision, or hearing aids, forcing beneficiaries to pay for these expenses entirely out of pocket.

- Unexpected medical events can lead to substantial financial strain, particularly for fixed-income seniors who may not be able to anticipate or absorb sudden healthcare costs without careful planning.

Limited Plan Options and Coverage Gaps

- UnitedHealthcare offers fewer individual health insurance plans tailored specifically to seniors compared to its Medicare Advantage and Medicare Supplement options, reducing the availability of suitable coverage for those not yet eligible for Medicare.

- Many individual plans do not include prescription drug coverage as a standard feature, requiring seniors to purchase separate plans or rely on employer-sponsored benefits, which increases complexity and cost.

- Coverage for preventive services, while present, may not be as expansive as in group or government-sponsored programs, potentially leaving gaps in essential screenings and vaccinations important for aging populations.

What are the key differences between UnitedHealthcare PPO and HMO plans for individual health insurance?

Provider Network Flexibility

- UnitedHealthcare PPO plans offer greater flexibility when choosing healthcare providers. Members can visit any doctor or specialist without needing a referral, whether the provider is in-network or out-of-network.

- With HMO plans, members must select a primary care physician (PCP) and receive most of their care through in-network providers. Visiting a specialist typically requires a referral from the PCP, and out-of-network care is usually not covered unless in an emergency.

- This difference means PPO enrollees have more autonomy in managing their healthcare, while HMO plans require more structured access to services through a coordinated network.

- PPO plans generally come with higher monthly premiums compared to HMO plans. This is due to the broader provider access and reduced restrictions on care.

- While HMO plans feature lower premiums, they require members to stay within the designated network to receive coverage. Going out-of-network—except in emergencies—usually results in no cost-sharing, making unexpected bills more likely if guidelines aren't followed.

- PPO members benefit from some coverage even when using out-of-network providers, though their out-of-pocket costs such as deductibles, coinsurance, and copayments will be higher in those cases.

Geographic Coverage and Service Accessibility

- UnitedHealthcare PPO plans are better suited for individuals who travel frequently or live in multiple locations throughout the year, as they offer broader geographic coverage and access to out-of-network care with partial reimbursement.

- HMO plans are typically more limited in geographic scope and may not provide coverage outside certain service areas, which can be a challenge for those who relocate often or spend significant time away from their home region.

- Access to urgent or routine care under an HMO is generally efficient within the network, but PPOs provide an added layer of accessibility for individuals who need care outside their local area without sacrificing all benefits.

Frequently Asked Questions

What types of individual health insurance plans does UnitedHealthcare offer?

UnitedHealthcare offers several individual health insurance plans, including Health Maintenance Organization (HMO), Preferred Provider Organization (PPO), Exclusive Provider Organization (EPO), and High-Deductible Health Plans (HDHPs) with Health Savings Account (HSA) options. These plans vary in network flexibility, out-of-pocket costs, and coverage levels. You can choose a plan based on your healthcare needs, preferred doctors, and budget, with options available during open enrollment or qualifying life events.

How do I enroll in a UnitedHealthcare individual health plan?

You can enroll in a UnitedHealthcare individual health plan through the Health Insurance Marketplace during the annual Open Enrollment Period or after a qualifying life event, such as losing job-based coverage or moving. Visit Healthcare.gov, select a plan, and UnitedHealthcare will confirm your enrollment. You may also apply directly through UnitedHealthcare’s website or with help from a licensed agent to ensure the best plan choice.

Does UnitedHealthcare cover pre-existing conditions in its individual plans?

Yes, UnitedHealthcare covers pre-existing conditions in its individual health insurance plans as required by the Affordable Care Act. Insurers cannot deny coverage or charge higher premiums based on health history. Once enrolled, all medically necessary services related to pre-existing conditions are covered without waiting periods. This ensures access to essential treatments and promotes equitable healthcare for individuals regardless of prior diagnoses.

Can I keep my current doctor with a UnitedHealthcare individual plan?

Whether you can keep your current doctor depends on whether they are in UnitedHealthcare’s provider network. PPO plans offer more flexibility to see out-of-network providers, while HMO and EPO plans typically require in-network care except in emergencies. Before enrolling, verify your doctor’s participation in the specific plan’s network by using UnitedHealthcare’s online provider directory or contacting customer service for accurate, up-to-date information.

Leave a Reply