Auto Insurance For At Risk Drivers

Finding affordable auto insurance can be a significant challenge for high-risk drivers. Whether due to a history of traffic violations, past accidents, or DUI convictions, these individuals often face steep premiums or outright denials from standard insurers.

Yet, driving is essential for many, making coverage not just a legal requirement but a practical necessity. Specialized insurance providers and state-mandated programs have emerged to meet this demand, offering options tailored to elevated-risk profiles.

While coverage may cost more, understanding available alternatives, how insurers assess risk, and ways to improve one’s driving record can lead to more manageable solutions for those navigating the complexities of high-risk auto insurance.

Does diy electrical wiring void home insurance

Does diy electrical wiring void home insuranceAuto Insurance Options and Challenges for High-Risk Drivers

For individuals classified as high-risk drivers, securing affordable and reliable auto insurance can be a challenging and often frustrating task. Insurance companies determine risk based on numerous factors such as traffic violations, at-fault accidents, DUI convictions, lapses in coverage, and poor credit history.

These markers signal to insurers a higher probability of future claims, leading them to either deny coverage outright or offer policies at steep premiums. However, despite these hurdles, coverage is both available and legally required in most states.

Specialized insurers, assigned risk pools, and high-risk auto insurance programs exist specifically to serve this demographic. Understanding the landscape—knowing what impacts your risk profile, how to reduce premiums over time, and where to shop for coverage—is essential for high-risk drivers aiming to regain financial and driving stability.

What Makes a Driver Classified as High-Risk?

A driver is typically labeled as high-risk due to behaviors or circumstances that statistically increase the likelihood of filing an insurance claim.

Safeu home insurance review

Safeu home insurance reviewCommon factors include DUI or DWI convictions, multiple traffic violations (such as speeding or reckless driving), being involved in at-fault accidents, having uninsured motorist incidents, or maintaining a record with frequent insurance lapses. Additionally, insurers may consider low credit scores as an indicator of higher risk, even if unrelated to driving behavior. New drivers or those with limited driving experience may also be categorized as higher risk due to inexperience.

Each insurance company uses proprietary algorithms and underwriting guidelines to assess these factors, which means that one insurer might classify a driver as high-risk while another offers standard rates based on mitigating circumstances like completion of defensive driving courses.

How High-Risk Drivers Can Obtain Auto Insurance

Even with a tarnished driving record, high-risk drivers have several avenues to secure auto insurance. One common route is through non-standard insurance carriers, companies that specialize in covering individuals who don’t qualify for conventional policies.

Another option is state-run assigned risk plans or automobile insurance plans (AIPs), which distribute high-risk applicants among private insurers to ensure everyone can obtain mandatory coverage. Additionally, high-deductible policies, limited coverage plans, or franklin plans (state-specific programs) may be available depending on location.

Smart home devices lower insurance rates

Smart home devices lower insurance ratesIt's crucial to compare quotes from multiple insurers, including those that focus exclusively on high-risk clients, such as The General, Dairyland, or Progressive’s high-risk division. Over time, maintaining a clean driving record, enrolling in traffic school, and improving credit can open doors to more affordable options.

While initial premiums for high-risk drivers can be significantly higher than average, there are proven ways to reduce costs over time. The most effective strategy is to maintain a clean driving record—avoiding tickets, accidents, and violations demonstrates improved risk to insurers.

Completing an approved defensive driving course can lead to immediate discounts and sometimes court-dismissed infractions. Insurers may also offer safe driver discounts, pay-in-full incentives, or low-mileage reductions if the driver uses their vehicle infrequently.

Bundling auto insurance with other policies like renters or homeowners can yield multi-policy discounts. Usage-based insurance programs, which use telematics to monitor driving behavior, allow conscientious drivers to prove their safety and qualify for lower rates. Over 3 to 5 years of responsible driving, a high-risk driver can often transition back to a standard or even preferred risk category.

Storm damage coverage standard home insurance

Storm damage coverage standard home insurance| Risk Factor | Impact on Insurance | Potential Mitigation |

|---|---|---|

| DUI/DWI Conviction | Can increase premiums by 75–100% or lead to policy denial | Complete court-mandated programs, install ignition interlock device |

| Multiple Traffic Tickets | Each violation can raise rates; multiple lead to non-standard classification | Traffic school, consistent safe driving over time |

| At-Fault Accidents | Substantially increases premiums, especially if frequent | No additional incidents, usage-based insurance programs |

| Insurance Lapse | Signals financial instability; penalties vary by state | Maintain continuous coverage, set up automatic payments |

| Low Credit Score | Many insurers use credit-based insurance scores to assess risk | Improve credit through timely payments, reduce debt |

Comprehensive Guide to Auto Insurance for High-Risk Drivers

What are the top auto insurance options for at-risk drivers?

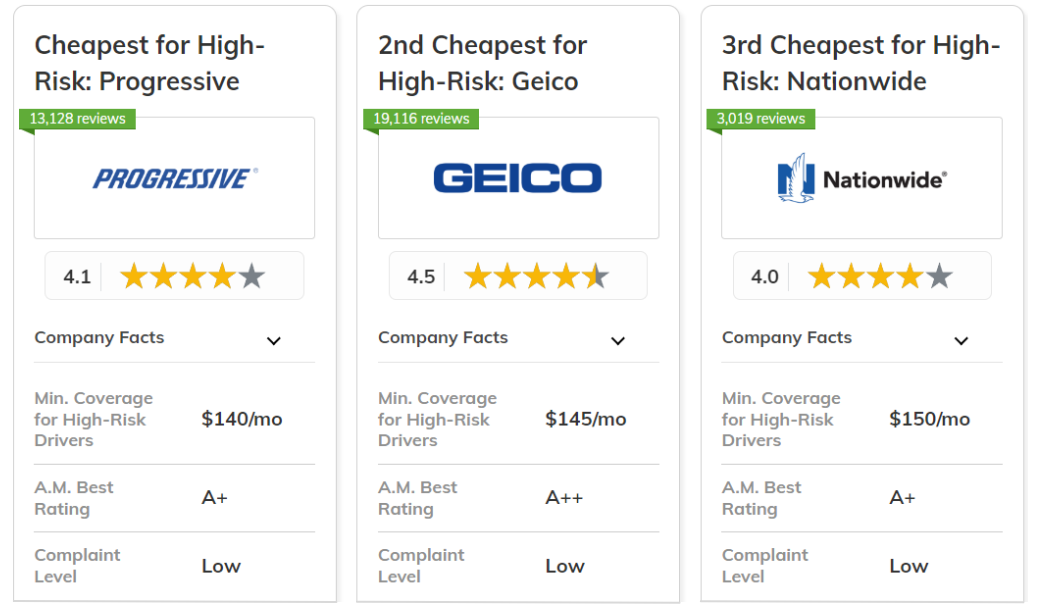

High-Risk Auto Insurance Providers Specializing in At-Risk Drivers

- State Farm offers tailored policies for high-risk drivers despite its mainstream reputation, using individualized risk assessments to provide coverage even after incidents like DUIs or multiple accidents. Their extensive agent network allows for personalized service and flexible payment plans.

- Geico is known for competitive rates among drivers with blemished records, including those with suspended licenses or poor credit. They use advanced algorithms to evaluate risk factors beyond traditional metrics, often resulting in more affordable premiums than expected.

- The Hartford partners with independent agents to offer high-risk coverage through their Passport program, focusing on mature drivers with past violations. This program emphasizes safety education and usage-based discounts, making it a reliable option for older at-risk individuals.

Non-Standard Insurance Companies Focused on High-Risk Coverage

- Progressive stands out with its unique pricing model that compares various risk tiers and offers specialized programs like Snapshot, a telematics-based system that rewards safe driving habits even for those with prior infractions. This flexibility makes Progressive a top contender for at-risk drivers seeking redemption through behavior tracking.

- Mercury Insurance operates in select states and provides non-standard policies tailored for drivers with recent at-fault accidents, DUI convictions, or lapses in coverage. Their underwriting process considers the context behind violations, which may lead to faster reinstatement of coverage.

- National General Insurance, now part of Progressive, specializes exclusively in high-risk and non-standard policies. They offer inclusive options for drivers with past license suspensions or multiple speeding tickets, and they provide tools such as online claims tracking and mobile policy management.

State-Sponsored and Assigned Risk Pool Options

- The California Automobile Assigned Risk Plan (CAARP) serves drivers who cannot obtain insurance in the voluntary market due to serious violations. Participating insurers are required to accept a portion of these high-risk applicants based on market share, ensuring universal access to minimum liability coverage.

- Other states operate similar mechanisms, such as the New York Automobile Insurance Plan (NYAIP) and the Florida Assigned Risk Plan (FARP), which distribute at-risk drivers among licensed companies. These pools maintain baseline coverage requirements and are regulated to prevent excessive pricing.

- While premiums through assigned risk plans tend to be higher and benefits more limited, they serve as a critical safety net. Drivers enrolled in these programs can transition back to standard insurers after maintaining clean records for designated periods, usually three years.

What are the best auto insurance options for high-risk drivers?

1. Specialized High-Risk Insurance Companies

- Some insurers specialize in providing coverage for high-risk drivers, such as those with DUI convictions, multiple accidents, or poor credit histories. Companies like The General, Dairyland Insurance, and Direct Auto are known for catering specifically to this demographic, offering policies that may not be available through standard carriers.

- These specialized providers often have more lenient underwriting criteria, allowing drivers who have been denied elsewhere to obtain mandatory liability coverage. They may also offer payment plans and discounts for completing defensive driving courses or maintaining continuous coverage.

- While premiums are typically higher than standard rates, these companies can be a reliable starting point for drivers rebuilding their insurance history. It's important to compare quotes from multiple high-risk insurers to find the most affordable option with acceptable coverage limits.

2. State-Sponsored Assigned Risk Plans

- When private insurers refuse coverage, most states offer assigned risk plans, also known as auto insurance plans or residual market programs. These state-managed pools ensure that all drivers can obtain minimum liability coverage, regardless of their driving record.

- Drivers apply through a central administrator, and the state assigns them to an insurance company that participates in the pool. Each insurer is required to accept a portion of the risk based on their market share, spreading the financial burden across the industry.

- Although premiums in these plans are generally higher and customer service may be limited, they provide a legal pathway to insurance for those who cannot secure it otherwise. Examples include the California Automobile Assigned Risk Plan (CAARP) and the New York Automobile Insurance Plan (NYAIP).

3. Non-Standard Insurance from Major Providers

- Some large insurance companies, such as Progressive and State Farm, offer non-standard insurance policies designed for high-risk drivers through separate divisions or subsidiaries. These policies allow major carriers to serve drivers who wouldn't qualify for their standard or preferred tiers.

- Non-standard policies often include coverage options like liability, collision, and comprehensive, but with higher deductibles and premiums. They may also provide tools for improving driving records over time, such as usage-based insurance programs like Snapshot.

- By maintaining a clean driving record, paying premiums on time, and taking advantage of available discounts, drivers can eventually transition from non-standard to standard policies, often with the same insurer. This continuity can help improve long-term rates and reliability of coverage.

Does GEICO Provide Auto Insurance for High-Risk Drivers?

Yes, GEICO does provide auto insurance for high-risk drivers, though availability and eligibility can vary based on individual circumstances and state regulations. High-risk drivers typically include those with recent traffic violations, multiple accidents, DUI convictions, or a lapse in insurance coverage.

Usaa home insurance eligibility

Usaa home insurance eligibilityWhile GEICO considers these factors during underwriting, they use a range of variables to assess risk, including driving history, age, location, and vehicle type. Drivers classified as high-risk may face higher premiums, but GEICO aims to offer competitive rates by leveraging its underwriting algorithms and customer service strengths.

What Qualifies a Driver as High-Risk?

- One of the primary factors that categorizes a driver as high-risk is a history of traffic violations such as speeding tickets, reckless driving, or at-fault accidents. Insurers like GEICO review motor vehicle records to evaluate past incidents and determine future risk.

- Drivers with serious offenses like driving under the influence (DUI) or driving while intoxicated (DWI) are almost always considered high-risk. These convictions significantly impact insurance eligibility and rates due to the heightened statistical likelihood of future claims.

- Another common qualifier is a lapse in auto insurance coverage. Going uninsured for a period, even if brief, signals instability to insurers and can result in being classified as high-risk, leading to higher premiums or more limited coverage options.

How Does GEICO Evaluate High-Risk Applications?

- GEICO evaluates high-risk applications by analyzing the applicant’s Motor Vehicle Record (MVR), which details past traffic infractions, accidents, and license status. This report helps GEICO understand driving behavior and potential risk exposure over time.

- The company uses an automated underwriting system that weighs various risk factors, including the number and severity of violations, time elapsed since infractions, and the driver’s age and experience. This allows GEICO to assign risk tiers and price policies accordingly.

- GEICO may require additional documentation or impose conditions, such as completing a defensive driving course, especially for drivers with recent DUIs or repeated violations. Meeting these conditions can sometimes improve eligibility or reduce premiums over time.

Are There Alternatives If GEICO Doesn’t Offer Coverage?

- If GEICO declines coverage for a high-risk driver, one alternative is to explore policies through assigned risk plans or state-sponsored auto insurance programs, such as the California Automobile Assigned Risk Plan (CAARP). These programs ensure that all drivers can obtain minimum required coverage, even with poor records.

- Specialty insurance companies that focus exclusively on high-risk drivers may offer more flexible underwriting standards. Examples include companies like The General, Dairyland, or State Auto, which are known for serving drivers who struggle to find coverage in the standard market.

- Another option is to reassess eligibility after improving driving behavior. Maintaining a clean record, taking approved traffic safety courses, and keeping continuous insurance coverage can make a driver eligible for GEICO or other insurers in the future.

Does State Farm offer auto insurance for high-risk drivers?

Does State Farm Provide Coverage for High-Risk Drivers?

State Farm does offer auto insurance for individuals considered high-risk drivers, although eligibility depends on several factors. High-risk status can result from multiple traffic violations, at-fault accidents, license suspensions, or driving under the influence.

While State Farm may not directly market a specific “high-risk” policy, many drivers with less-than-perfect records can still obtain coverage through its standard insurance options. Underwriters at State Farm evaluate applications based on individual circumstances, including driving history, location, vehicle type, and prior insurance gaps. Drivers seeking coverage should work directly with a State Farm agent to discuss their record and available options.

- State Farm assesses each application on a case-by-case basis rather than applying a universal denial policy for high-risk profiles.

- Certain severe infractions, such as multiple DUIs, may limit eligibility or result in non-renewal of existing policies.

- Working with a licensed agent allows high-risk drivers to explore possible discounts and safer driving programs that may improve their eligibility.

How Does State Farm Classify a High-Risk Driver?

State Farm uses a combination of internal underwriting guidelines and historical claims data to classify drivers as high-risk. Common determining factors include recent traffic violations such as speeding tickets, reckless driving charges, or multiple at-fault accidents within a few years.

Additionally, license suspensions, driving without insurance, or incidents involving DUI/DWI significantly increase the likelihood of being categorized as high-risk. The company may also consider the driver's age, credit history (where permitted by law), and total years of driving experience. These factors help State Farm assess the statistical probability of future claims and determine appropriate premiums.

- Drivers with three or more moving violations in a three-year period are often viewed as higher risk during underwriting.

- Young or inexperienced drivers with a single serious violation may face higher scrutiny due to their limited driving history.

- State Farm may reevaluate risk classification over time if the driver maintains a clean record and completes approved driver education courses.

What Alternatives Exist If State Farm Doesn't Offer a Policy?

If State Farm determines that it cannot provide coverage due to an individual's driving record, there are still several alternatives available to high-risk drivers. Many states operate assigned risk programs or high-risk auto insurance pools designed to ensure that all drivers can obtain mandatory liability coverage.

Private insurers specializing in non-standard insurance, such as The General, Dairyland, or National General, often accept applicants whom standard carriers decline. Additionally, drivers can take steps to improve their profile, such as enrolling in defensive driving courses, which may open doors to future coverage with major providers like State Farm.

- State-specific assigned risk plans, such as the California FAIR Plan or New York's Motor Vehicle Assignment System, guarantee minimum coverage regardless of driving history.

- Non-standard insurance companies typically charge higher premiums but offer payment plans and options tailored to high-risk individuals.

- Improving one's driving record over time and maintaining continuous insurance can eventually make drivers eligible for policies from standard insurers again.

Frequently Asked Questions

What is auto insurance for high-risk drivers?

Auto insurance for high-risk drivers is a specialized policy designed for individuals more likely to file claims due to factors like DUIs, multiple accidents, or poor credit.

Standard insurers may deny coverage, so high-risk drivers often turn to non-standard insurance companies. These policies typically have higher premiums but provide necessary legal coverage. State-assigned risk pools may also help drivers obtain mandatory insurance when private options are unavailable.

Why do high-risk drivers pay more for insurance?

High-risk drivers pay higher premiums because insurers view them as more likely to file costly claims. Factors such as traffic violations, accidents, or driving without insurance increase perceived risk.

Insurance companies use statistical data showing these drivers have a higher accident rate. To offset potential losses, they charge more for coverage. While expensive, this insurance ensures financial protection and meets legal driving requirements, making it essential despite the increased cost.

Yes, high-risk drivers can reduce premiums by improving their driving record, completing a defensive driving course, or maintaining continuous coverage. Insurers may offer discounts for safety features or bundling policies.

Over time, responsible driving helps reclassify you as standard-risk. Avoiding violations and parking tickets also helps. While rates start high, consistent positive behavior leads to lower premiums, making it worthwhile to adopt safer driving habits and maintain a clean record.

How long am I considered a high-risk driver?

You're typically considered a high-risk driver for 3 to 5 years, depending on the offense and insurer. For example, a DUI may affect your status for 5 years, while a speeding ticket may only impact it for 3.

Over time, safe driving and no new violations help restore your standing. Insurers periodically review your history, so maintaining a clean record is key. Eventually, you may qualify for standard or even preferred rates with improved behavior.

Leave a Reply