Auto Insurance In Mo

Driving in Missouri requires more than just a valid license—it demands reliable auto insurance coverage. With state-mandated liability requirements, drivers must carry minimum coverage to protect against financial responsibility in accidents. However, understanding what those requirements mean and how they apply can be confusing.

From urban areas like St. Louis and Kansas City to rural regions, insurance rates vary based on driving history, location, and vehicle type. Many drivers seek affordable options without sacrificing protection. This guide explores auto insurance in Missouri, helping residents make informed decisions about coverage, providers, and cost-saving strategies suited to their individual needs.

Understanding Auto Insurance Requirements in Missouri

Auto insurance in Missouri is governed by the state's financial responsibility laws, which mandate that all drivers maintain a minimum level of coverage to operate a vehicle legally. Missouri follows an at-fault system, meaning that the driver responsible for causing an accident is financially liable for damages.

When should adult child at home get own car insurance

When should adult child at home get own car insuranceTo ensure drivers can cover these liabilities, Missouri requires a minimum level of auto insurance: $25,000 in bodily injury coverage per person, $50,000 in bodily injury coverage per accident, and $25,000 in property damage coverage (commonly referred to as 25/50/25). Additionally, drivers must carry $25,000 in uninsured motorist coverage per person and $50,000 per accident to protect themselves in collisions with underinsured or uninsured drivers.

Failure to meet these requirements can result in fines, license suspension, or even vehicle impoundment. It’s also important to note that while the state allows drivers to post a cash bond or use a surety bond to satisfy financial responsibility, most opt for traditional insurance due to its convenience and broader protection.

Minimum Coverage Requirements and Legal Implications

In Missouri, the law requires drivers to carry at least 25/50/25 liability insurance to cover bodily injury and property damage they may cause to others in an accident. This means your insurance will pay up to $25,000 for injuries sustained by one person, up to a total of $50,000 per accident, and up to $25,000 for any property damage.

Missouri is one of the few states that permit drivers to demonstrate financial responsibility through alternatives such as a $50,000 cash deposit with the state or a surety bond, but these are rarely used.

Who offers the best unoccupied home insurance in the uk

Who offers the best unoccupied home insurance in the ukNot having proper coverage can lead to serious consequences, including fines of up to $500, suspension of your driver's license, and reinstatement fees. Additionally, if you're involved in an accident without insurance, the state may require you to file an SR-22 form with your insurance provider to prove financial responsibility for up to three years.

Uninsured Motorist Coverage and Why It Matters

Missouri law mandates that insurance companies offer uninsured/underinsured motorist coverage in the same minimum limits as liability coverage: $25,000 per person and $50,000 per accident.

While drivers have the legal right to reject this coverage in writing, it is strongly advised to keep it due to the high number of uninsured drivers on Missouri roads. According to recent data, over 13% of motorists in Missouri are uninsured, which increases the risk of being involved in an accident with someone who cannot pay for damages.

This coverage helps pay for your medical bills, lost wages, and other expenses if you're hit by a driver with no insurance or insufficient coverage. Opting out may save a few dollars on premiums, but it exposes you to significant financial risk in the event of a collision with an at-fault driver who lacks adequate coverage.

Wichita home insurance cost

Wichita home insurance costFactors That Influence Auto Insurance Rates in Missouri

Several factors determine how much you’ll pay for auto insurance in Missouri, including your driving record, age, location, vehicle type, and credit history. Drivers with a history of accidents or traffic violations typically face higher premiums due to their increased risk profile.

Urban areas such as St. Louis and Kansas City generally have higher insurance costs due to increased traffic density, higher rates of theft, and more frequent claims. Insurance companies also consider the make and model of your vehicle—high-performance or luxury cars cost more to insure because of higher repair costs and theft rates.

Additionally, insurers in Missouri use credit-based insurance scores to help predict risk, meaning a poor credit score can lead to higher premiums. Shopping around and comparing quotes from multiple providers can help drivers find more affordable rates tailored to their individual circumstances.

| Coverage Type | Missouri Minimum Limit | Purpose |

|---|---|---|

| Bodily Injury (per person) | $25,000 | Covers medical expenses for one person injured in an accident you cause. |

| Bodily Injury (per accident) | $50,000 | Covers total medical expenses for all persons injured in an accident you cause. |

| Property Damage | $25,000 | Pays for damage you cause to another person's property, such as their vehicle. |

| Uninsured Motorist (per person) | $25,000 | Protects you if injured by a driver with no or inadequate insurance. |

| Uninsured Motorist (per accident) | $50,000 | Covers total costs for you and passengers injured by an uninsured driver. |

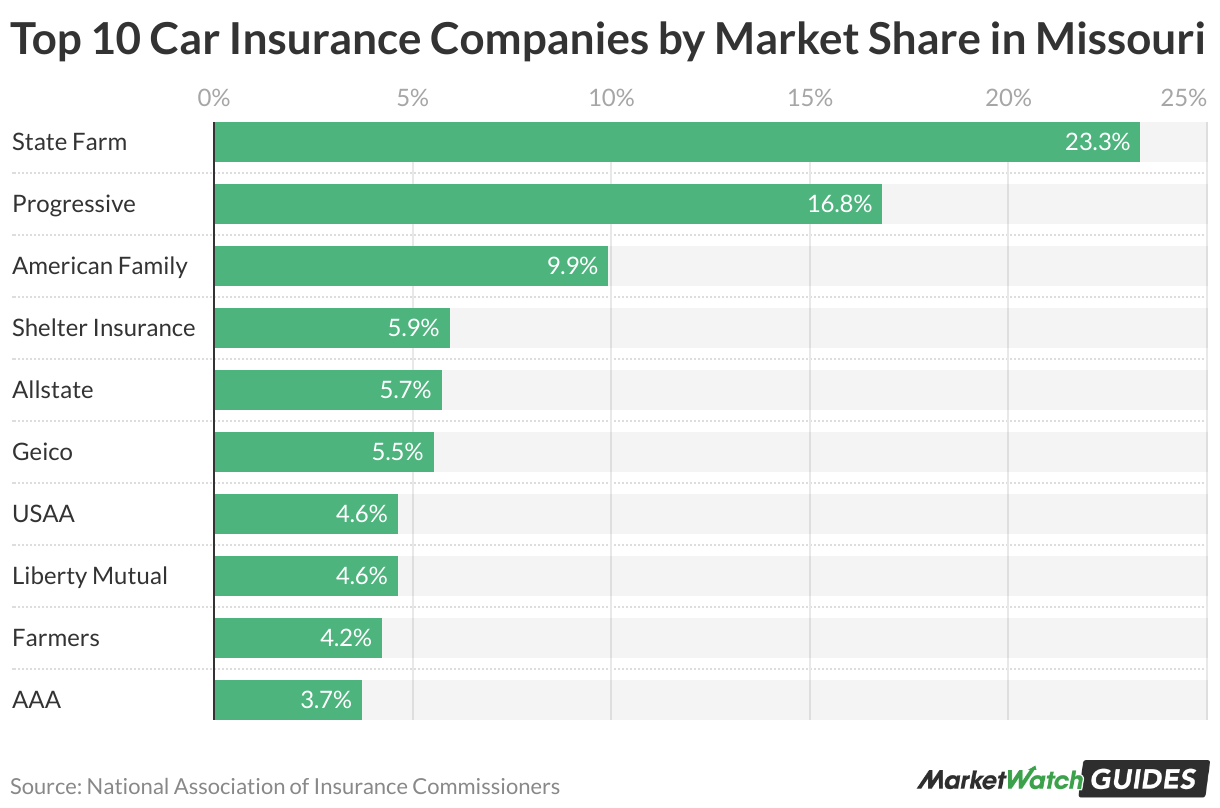

Comprehensive Guide to Auto Insurance in Missouri: Coverage Options and Requirements

What is the most affordable auto insurance provider in Missouri?

Affordable home insurance for older homes tips

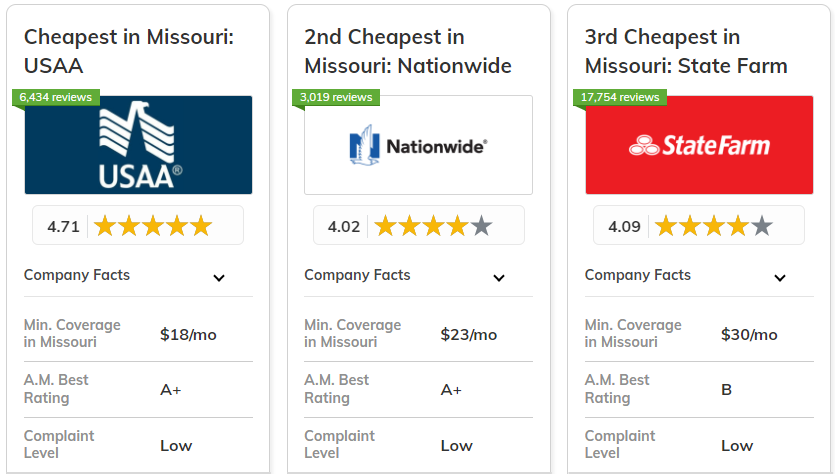

Affordable home insurance for older homes tipsThe most affordable auto insurance provider in Missouri varies based on individual factors such as driving history, age, credit score, and coverage needs. However, according to recent comparisons and data from sources like NerdWallet, Bankrate, and the Missouri Department of Insurance, USAA consistently offers the lowest average rates for eligible drivers.

USAA is available only to military members, veterans, and their immediate families. For civilians, companies like State Farm and Geico are frequently among the most budget-friendly options in the state, often providing competitive base premiums and multiple discount opportunities.

Top Low-Cost Auto Insurance Providers in Missouri

- USAA stands out as the most affordable option in Missouri, with average annual premiums significantly below the state average, but access is limited to military-affiliated individuals and their families.

- State Farm follows closely for non-military drivers, offering personalized rate plans and widespread agent availability across Missouri cities like St. Louis and Kansas City.

- Geico is another highly competitive provider, known for its online tools and fast quote process, making it easy for Missouri residents to secure low rates based on driving behavior and vehicle type.

Factors That Influence Auto Insurance Affordability in Missouri

- Driving record plays a major role; drivers with clean records typically qualify for the lowest rates from top insurers like Progressive and Farmers.

- Location within Missouri affects pricing—urban drivers in Springfield or Columbia may pay higher premiums due to traffic density and accident rates compared to rural areas.

- Credit history is legally considered in Missouri, so individuals with higher credit scores often receive better rates from companies such as Allstate and Nationwide.

Discounts That Can Lower Auto Insurance Costs in Missouri

- Many insurers offer multi-policy discounts (bundling auto with home or renters insurance), which can reduce premiums by 15% or more through providers like Travelers and Erie Insurance.

- Safe driver programs and usage-based insurance, such as Geico’s DriveEasy or Progressive’s Snapshot, allow Missouri drivers to lower their costs by demonstrating responsible driving habits.

- Good student discounts and defensive driving course completions are widely available across providers including State Farm and Farmers, offering measurable savings especially for younger drivers.

Why is auto insurance in Missouri more expensive compared to other states?

High Rate of Uninsured Drivers

One of the primary reasons auto insurance in Missouri is more expensive than in many other states is the high percentage of uninsured motorists on the roads. Missouri consistently ranks among the states with the highest numbers of drivers who operate vehicles without insurance. This widespread lack of coverage increases financial risk for insurance companies, which in turn leads to higher premiums for insured drivers.

Insurers must account for the likelihood of having to cover damages caused by uninsured drivers, especially in collision and medical payments claims. As a result, responsible policyholders end up subsidizing the risks posed by those who do not carry insurance, which directly contributes to increased costs across the board.

- Missouri has one of the highest rates of uninsured drivers in the U.S., often exceeding 20%, significantly above the national average.

- Insurance companies are required to offer uninsured/underinsured motorist coverage, which raises base policy costs.

- When accidents involve uninsured drivers, claims often fall on the insured driver’s policy, increasing loss exposure for insurers.

Missouri experiences a combination of harsh weather conditions and dense urban traffic, both of which contribute to a higher frequency of auto accidents.

Cities such as St. Louis and Kansas City have high traffic congestion, increasing the likelihood of collisions, especially rear-end and intersection-related crashes. Additionally, the state endures extreme weather, including ice storms, heavy rain, and snow, which reduce road visibility and traction, further elevating the risk of accidents.

These environmental and infrastructural factors result in a higher volume of insurance claims, which drives up the overall cost of coverage. Insurers factor in regional claim frequency and severity when setting premiums, and Missouri's risk profile is considered elevated compared to states with milder climates and less congested roadways.

- Winter weather in Missouri contributes to seasonal spikes in accident claims, particularly from slippery road conditions.

- Urban areas experience high claim volumes due to stop-and-go traffic and distracted driving.

- More frequent claims result in higher average payouts for insurers, which are passed on to consumers through increased premiums.

High Rate of Lawsuits and Legal Costs

Missouri is considered a tort state, meaning accident victims can sue for damages, including medical expenses, lost wages, and pain and suffering. The state also has relatively low thresholds for filing lawsuits after an accident, which leads to a higher number of legal claims and more litigation overall.

This legal environment increases the cost of claims for insurance companies, especially when cases go to court or are settled for large amounts. Higher legal and medical costs, particularly in metropolitan areas, are major factors in the overall expense of claims.

Insurers must maintain higher liability reserves in such environments, which translates directly into higher premiums for all policyholders. The presence of expensive medical treatments and an active personal injury legal market further inflates claim costs.

- Missouri's tort system allows extensive recovery for non-economic damages, increasing the value of many claims.

- Frequent litigation leads to higher legal defense and administrative costs for insurance companies.

- Urban centers see higher medical treatment costs, which are reflected in bodily injury claim payouts.

Who offers the lowest car insurance rates in Missouri?

Top Insurance Providers with the Lowest Rates in Missouri

- Geico consistently ranks among the most affordable car insurance providers in Missouri, offering competitive rates especially for drivers with clean records. Their cost-effective policies are supported by a broad range of discounts, including those for safe driving, military affiliation, and bundling with other insurance products.

- State Farm is another leading insurer known for low average premiums across the state. As the largest auto insurer in the U.S., State Farm benefits from local agent support and personalized service, along with discounts for loyalty, multi-car policies, and usage-based programs like Drive Safe & Save.

- USAA, available exclusively to military members and their families, often provides the lowest rates in Missouri. While access is limited, those eligible frequently report substantial savings combined with high customer satisfaction due to responsive service and comprehensive coverage options.

Factors That Influence Car Insurance Rates in Missouri

- Driving history plays a major role in determining insurance costs. Missouri drivers with accidents, speeding tickets, or DUIs typically face significantly higher premiums as insurers consider them high-risk.

- The type of vehicle insured affects pricing as well. Cars with high repair costs, poor safety ratings, or greater theft rates generally result in increased premiums, while fuel-efficient or safer models may qualify for lower rates.

- Location within Missouri also impacts pricing due to variations in traffic density, accident frequency, and crime rates. Urban areas like St. Louis and Kansas City tend to have higher insurance costs compared to rural regions with less congestion and fewer claims.

Ways to Save on Car Insurance in Missouri

- Take advantage of available discounts such as safe driver rewards, good student discounts, and low-mileage programs. Many insurers in Missouri offer savings for completing defensive driving courses or maintaining a claims-free history.

- Adjust your coverage levels strategically. While Missouri requires minimum liability coverage (25/50/25), increasing deductibles or dropping unnecessary coverages like rental reimbursement can reduce monthly premiums—though this should be weighed against personal risk tolerance.

- Compare quotes regularly using online tools or independent agents. Rates can vary widely between companies, and switching insurers every few years—especially when renewals come up—can lead to substantial savings without sacrificing coverage quality.

Frequently Asked Questions

What are the minimum auto insurance requirements in Missouri?

Missouri requires drivers to carry liability insurance with minimum coverage of $25,000 for bodily injury per person, $50,000 for bodily injury per accident, and $25,000 for property damage. This is known as 25/50/25 coverage. Uninsured motorist coverage with the same limits is also required unless explicitly rejected in writing.

Can I drive without auto insurance in Missouri?

No, you cannot legally drive without auto insurance in Missouri. The state mandates proof of financial responsibility, typically through auto insurance. Driving uninsured can result in fines, license suspension, vehicle impoundment, and personal liability for damages in case of an accident. While insurance is required, Missouri is not a no-fault state.

How does Missouri’s modified comparative fault law affect my auto insurance claim?

Missouri follows a modified comparative fault rule, meaning you can recover damages only if you are less than 50% at fault. Your compensation will be reduced by your percentage of fault. For example, with 30% fault, you recover 70% of damages. Your insurer uses this rule when settling claims involving shared responsibility.

What discounts are available on auto insurance in Missouri?

Many insurers in Missouri offer discounts for safe driving, bundling policies, having anti-theft devices, and completing defensive driving courses. You may also save with good student, multi-vehicle, or loyalty discounts. It's wise to ask your provider about available options, as rates and discounts vary between companies based on eligibility and driving history.

Leave a Reply