Wichita home insurance cost

The cost of home insurance in Wichita, Kansas, varies based on several factors, including location, home age, coverage needs, and local risk factors.

On average, homeowners in Wichita pay less than the national average, making it an affordable market for property insurance. Tornadoes, storms, and wind damage—common in the region—influence premiums, as insurers account for severe weather risks. Additionally, local crime rates, proximity to fire services, and home value play key roles in pricing.

Shopping around, bundling policies, and improving home safety can help reduce costs significantly. Understanding these variables is essential for Wichita homeowners seeking optimal coverage at competitive rates.

New York Life Insurance Company Bga Imo

New York Life Insurance Company Bga ImoUnderstanding Wichita Home Insurance Costs in 2024

Home insurance costs in Wichita, Kansas, are influenced by a combination of local risk factors, property characteristics, and market trends. As of 2024, the average annual premium for homeowners insurance in Wichita ranges between $1,200 and $1,600, which is slightly above the national average.

This cost reflects protection for dwelling, personal property, liability, and additional living expenses. Various elements contribute to these rates, including the age and construction type of the home, its location within Wichita, local crime rates, and exposure to natural hazards such as tornadoes, hailstorms, and wind damage—common risks in the region.

Insurance providers also consider a homeowner’s credit score, claims history, and chosen deductible levels when calculating premiums. Shopping around and bundling policies can help Wichita homeowners secure more competitive rates.

Factors That Influence Home Insurance Rates in Wichita

Insurance providers determine premiums based on multiple risk-related variables specific to the Wichita area. One of the most significant factors is the region’s severe weather exposure, especially during tornado season, which increases the likelihood of structural damage claims.

Buy Life Insurance For Seniors

Buy Life Insurance For SeniorsHomes constructed with storm-resistant materials or equipped with reinforced roofs, impact-resistant windows, and storm shelters may qualify for discounts. The age and condition of a home also play crucial roles—older homes may have outdated electrical or plumbing systems, increasing the risk of fire or water damage.

Additionally, neighborhood crime rates and proximity to fire stations or hydrants affect pricing, with safer, more accessible areas typically seeing lower premiums. Personal history, such as previous claims or credit-based insurance scores, further shapes the final cost.

How Wichita Compares to Kansas and National Averages

When compared to both state and national figures, Wichita’s home insurance costs are moderately higher.

The average cost in Kansas is approximately $1,400 per year, while the national average sits around $1,300, making Wichita’s range of $1,200–$1,600 competitive yet reflective of local risk. Areas in south and central Kansas, including Wichita, face elevated premiums due to their location in Tornado Alley, where insurers account for frequent wind and hail claims.

What Is The Most Reputable Life Insurance Company

What Is The Most Reputable Life Insurance CompanyRural areas outside Wichita may have lower property values but higher premiums due to limited emergency response access, whereas urban neighborhoods benefit from proximity to fire protection services. Homeowners in Wichita often pay more than those in western Kansas but less than storm-prone areas in neighboring states like Oklahoma.

Cost-Saving Tips for Wichita Homeowners

Wichita residents can reduce their home insurance expenses through several proactive strategies. One of the most effective methods is bundling home and auto insurance with the same provider, which typically yields a multi-policy discount of 10% to 25%.

Installing security systems, smoke detectors, and deadbolt locks can also lower premiums by reducing the risk of theft and fire. Raising the deductible can significantly decrease the annual premium, although it increases out-of-pocket costs in the event of a claim.

Homeowners should also regularly shop around and compare quotes from multiple insurers, as rates can vary widely. Maintaining a strong credit score and avoiding frequent claims can lead to eligibility for preferred pricing tiers and loyalty rewards.

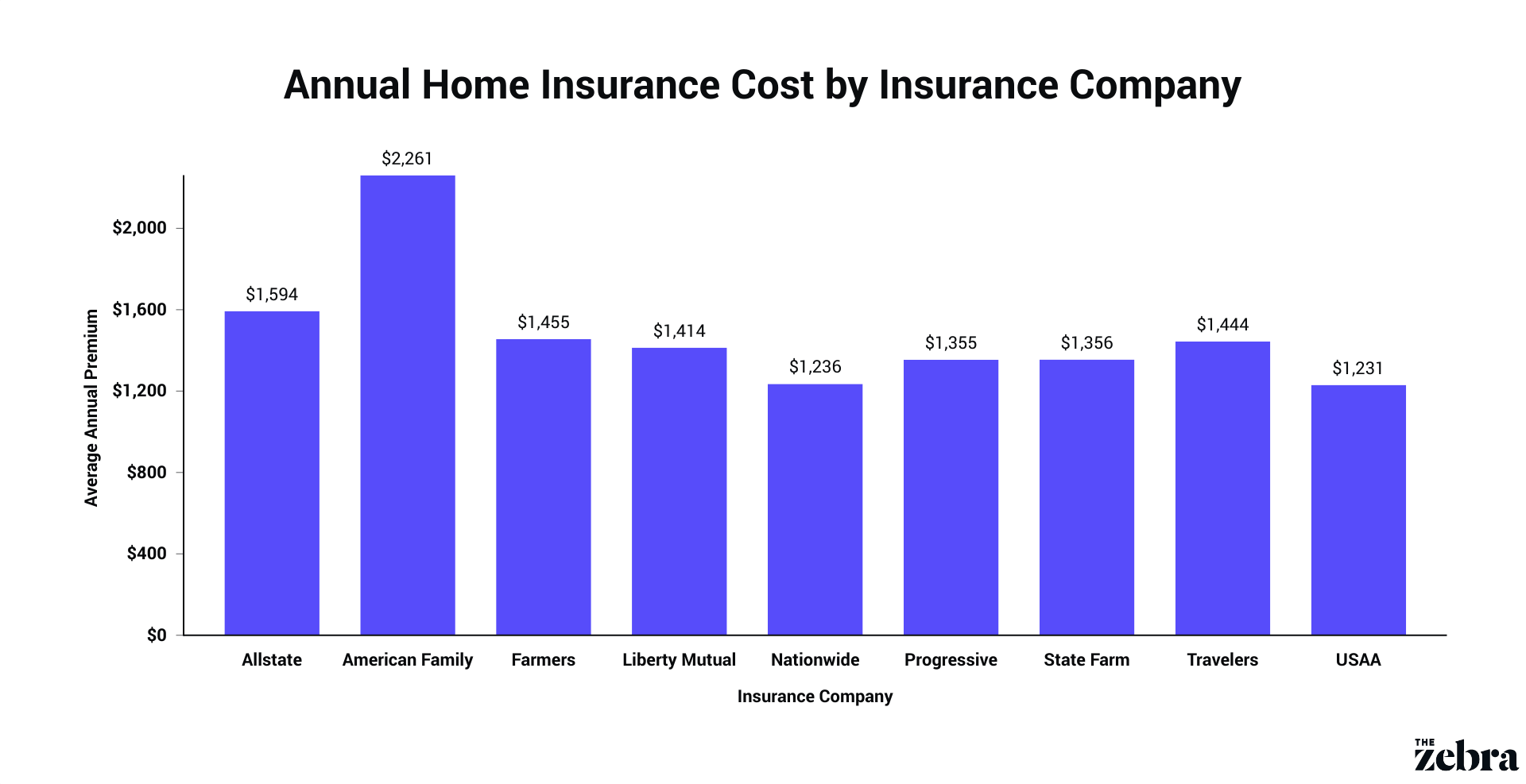

Aaa Life Insurance Sign In

Aaa Life Insurance Sign In| Insurance Provider | Average Annual Premium (Wichita) | Notable Discounts |

|---|---|---|

| State Farm | $1,250 | Bundling, claims-free, home safety devices |

| Allstate | $1,480 | Protective devices, loyalty, early signing |

| USAA | $1,100 | Military affiliation, bundling, home monitoring |

| Farmers Insurance | $1,550 | Roof type, claims-free, multi-home |

Available to military members, veterans, and their families.

Wichita Home Insurance Costs: A Comprehensive Guide to Rates and Coverage Options

What factors influence home insurance costs in Wichita, KS?

Location and Local Risk Factors in Wichita, KS

The geographic location of a home within Wichita, KS, significantly affects insurance premiums. Insurers evaluate proximity to fire stations, quality of local fire protection services, and crime rates in the neighborhood.

Areas with higher incidents of theft, vandalism, or fire risk typically see higher premiums. Additionally, homes located near flood-prone zones or in regions with limited access to emergency services may face increased costs due to perceived risk. Severe weather patterns common in south-central Kansas, including thunderstorms and hail, also contribute to risk assessments.

- Homes closer to fire stations often have lower premiums because of quicker emergency response times.

- Neighborhoods with higher crime rates may result in increased home insurance costs due to property and theft-related claims.

- Areas prone to severe weather such as hailstorms, which are frequent in Wichita, face higher premiums because of the increased likelihood of roof and property damage.

Home Characteristics and Construction Type

The physical attributes of a house play a crucial role in determining insurance costs. The age of the home, type of construction materials, roof condition, and square footage all influence the risk level assessed by insurers.

Newer homes built with modern, impact-resistant materials may cost less to insure, whereas older homes with outdated electrical or plumbing systems may be deemed higher risk. The design and foundation type can also affect resistance to weather damage, especially against common regional threats like high winds or tornadoes.

- Homes constructed with sturdy materials like brick or reinforced concrete may receive lower rates due to better durability during storms.

- Older homes not updated with modern wiring or plumbing may be charged higher premiums due to increased risk of fire or water damage.

- The roof’s age and material affect pricing, as newer, storm-resistant roofs are less likely to sustain damage during Wichita’s frequent hail events.

Insurance Coverage Options and Policy Features

The specific coverage choices made by the homeowner directly influence the cost of an insurance policy. The amount of coverage selected, deductible levels, and any added endorsements or riders will change the premium.

Opting for higher liability limits or including optional protections such as water backup or extended replacement cost will increase the overall cost. Conversely, choosing a higher deductible can lower the monthly premium, though it means greater out-of-pocket expenses if a claim occurs.

- Higher coverage limits increase premiums but provide more financial protection in the event of major damage or loss.

- Selecting a higher deductible generally reduces the monthly premium but increases the amount the homeowner must pay during a claim.

- Adding optional coverage for perils common in Kansas, such as hail damage or windstorms, will raise the policy cost but enhance protection.

What factors influence the cost of insuring a $400,000 home in Wichita?

Location and Local Risk Factors

Insurance providers consider the specific location within Wichita when determining premiums for a $400,000 home. Even within the same city, risk levels can vary by neighborhood due to factors like crime rates, proximity to fire stations, and flood zones.

- Areas with higher crime rates may lead to increased premiums due to the elevated risk of theft or vandalism.

- Homes located farther from fire hydrants or fire departments often incur higher costs because of the increased response time in emergencies.

- If the property lies in a flood-prone zone, even if not directly in a high-risk FEMA floodplain, insurers may require or recommend additional flood coverage, influencing the overall cost.

Home Construction and Age

The structural characteristics of the home significantly impact insurance pricing. Insurers evaluate building materials, the home’s age, and the condition of major systems when calculating risk.

- Older homes, especially those with outdated electrical, plumbing, or roofing systems, may be considered higher risk and lead to increased premiums.

- Homes built with fire-resistant materials like brick or concrete typically cost less to insure compared to wood-frame structures.

- Features such as a recently updated roof, reinforced garage doors, or storm-resistant windows can reduce risk and, in turn, lower insurance costs.

Policy Coverage and Deductibles

The scope of coverage selected and the deductible amount directly affect the premium for insuring a $400,000 home. Policyholders have flexibility in choosing how much protection they need based on their financial priorities.

- A policy that includes coverage for replacement cost (rebuilding the home at current prices) will generally have higher premiums than one covering only the market value.

- Opting for higher deductibles—such as $2,500 instead of $1,000—can reduce the monthly or annual premium, though it increases out-of-pocket expenses in the event of a claim.

- Additional endorsements, such as coverage for personal property, liability protection, or identity theft services, add to the overall cost but provide greater financial security.

Why are home insurance rates in Wichita, KS, higher than average?

)

Frequent Severe Weather Events

Wichita, Kansas, is located in the heart of Tornado Alley, making it especially vulnerable to extreme weather conditions. This geographic positioning exposes homes to frequent threats such as tornadoes, hailstorms, and high winds, which result in increased claims for roof damage, broken windows, and structural destruction.

Insurance companies determine premiums based on risk probability, so areas with historically high claims due to weather naturally face higher rates. Wichita’s consistent exposure to volatile spring and summer storm seasons further amplifies this risk.

- Hailstorms are particularly destructive in Wichita, often causing extensive damage to roofs, siding, and vehicles, leading to a high volume of property damage claims.

- Tornadoes, though not constant, pose a significant threat due to their potential to destroy entire neighborhoods, increasing insurers' liability exposure.

- Severe thunderstorms with high winds regularly contribute to siding, window, and tree damage, prompting homeowners to file frequent repair or replacement claims.

Building Costs and Material Inflation

The cost to rebuild or repair homes after a loss has risen substantially in recent years, affecting insurance premiums in Wichita. Factors such as increased prices for construction materials, labor shortages, and supply chain delays have driven up rebuild costs across Kansas.

Since home insurance rates are partly based on the estimated cost of reconstruction, these rising expenses directly impact premiums. Insurers must factor in the current economic environment when underwriting policies, leading to higher rates even in the absence of claims.

- Lumber prices and other key building materials have experienced significant volatility, raising the overall cost of home repairs and reconstruction projects.

- Skilled labor in the construction industry is limited, leading to longer repair times and higher labor costs, which insurers account for in policy pricing.

- Insurance companies use replacement cost estimates to set premiums, and with the cost of rebuilding rising, policies in Wichita reflect these updated figures.

Historical Claims Data and Risk Assessment

Insurance providers rely heavily on historical claims data to assess regional risk levels and set premium rates. Wichita has a documented history of costly property claims due to natural disasters, especially during peak storm seasons.

Areas with consistently high claim frequencies are deemed higher risk, leading insurers to charge more to offset potential future payouts. Additionally, insurers use predictive modeling based on past events, meaning regions like Wichita are often priced with anticipated risks in mind, regardless of year-to-year variations in storm activity.

- Insurance companies analyze data from past tornado outbreaks and hailstorm seasons to predict potential future losses, impacting current premium calculations.

- Neighborhoods in Wichita with densely packed housing are more susceptible to widespread damage, increasing collective claim amounts after a single event.

- Insurers also consider a property’s proximity to emergency services, flood zones, and local infrastructure quality—all factors that can influence individual and area-wide risk profiles.

What Is the Average Home Insurance Cost for a $100,000 House in Wichita?

Factors Influencing Home Insurance Costs for a $100,000 House in Wichita

- Several variables affect the cost of insuring a home valued at $100,000 in Wichita, Kansas. One of the primary factors is the home’s age and construction type. Older homes with outdated electrical or plumbing systems may cost more to insure due to an increased risk of fire or water damage.

- Location-specific risks, such as the likelihood of tornadoes and severe storms in the Wichita area, also impact premiums. Homes in regions with higher natural disaster exposure typically face increased insurance rates to account for potential claims.

- Additionally, the homeowner’s insurance history, credit score, and chosen deductible play significant roles. A clean claims history and higher credit score can lead to lower premiums, while opting for a higher deductible often reduces monthly or annual costs.

Estimated Average Annual Cost for $100,000 Home Insurance in Wichita

- The average home insurance premium in Kansas is approximately $1,500 to $1,800 per year, but for a home valued at $100,000 in Wichita, costs may be on the lower end of this range, typically between $1,200 and $1,500 annually.

- These estimates are based on standard coverage limits, including dwelling coverage, personal property, liability, and additional living expenses. A lower home value generally results in less dwelling coverage needed, which reduces premium costs.

- It is also important to note that exact prices vary by insurance provider. Companies like State Farm, Allstate, and USAA often offer competitive rates in Wichita, and obtaining multiple quotes can help homeowners find the most affordable option.

How to Lower Home Insurance Costs on a $100,000 House in Wichita

- One effective way to reduce home insurance premiums is by bundling policies. Many insurers offer discounts when homeowners combine their home and auto insurance under the same provider, potentially saving up to 20% on total costs.

- Installing safety and security upgrades such as smoke detectors, deadbolt locks, and monitored security systems can lead to measurable discounts. Some insurers also offer reduced rates for hurricane shutters or impact-resistant roofing, although these are less common in Kansas.

- Maintaining a high credit score and a record free of insurance claims can qualify homeowners for loyalty and responsible payer discounts. Additionally, periodically reassessing coverage needs and shopping around every few years ensures that policyholders are not overpaying for their protection.

Frequently Asked Questions

What factors influence the cost of home insurance in Wichita?

The cost of home insurance in Wichita is affected by several factors including the home's age, size, and location. Construction materials, security features, and claims history also play a role. Proximity to fire stations and local crime rates impact premiums. Additionally, the amount of coverage, deductible chosen, and whether the home is in a flood-prone area affect pricing. Insurance providers assess these elements to determine your final rate.

How much does home insurance typically cost in Wichita, Kansas?

On average, home insurance in Wichita costs between $1,200 and $1,600 annually. This varies based on coverage limits, home value, and individual risk factors. Policies usually include dwelling, liability, and personal property protection. Location within the city, home age, and credit score can further influence the price. Bundling with auto insurance or installing safety features may help lower the overall cost.

Does filing a claim increase home insurance costs in Wichita?

Filing a claim can increase your home insurance premiums in Wichita, especially if it’s a liability or weather-related claim. One claim might not drastically raise rates, but multiple claims over time often lead to higher costs. Insurers view frequent claims as a sign of increased risk. However, not all claims impact rates equally—smaller, non-recurring incidents may have minimal effect depending on your insurer's policies.

Yes, you can reduce your home insurance premium in Wichita by installing security systems, smoke detectors, or storm shelters. Raising your deductible can also lower monthly costs. Bundling home and auto insurance with the same provider often leads to discounts. Maintaining a good credit score and staying with the same insurer for multiple years may qualify you for reduced rates. Ask your provider about available discounts.

Leave a Reply