Auto Shop Liability Insurance

Auto shop liability insurance is a crucial safeguard for automotive repair businesses, protecting against financial losses resulting from property damage, bodily injury, or other accidents that may occur on the premises.

With vehicles, heavy machinery, and flammable materials present in most workshops, the risk of incidents is significant. This type of insurance covers legal fees, medical expenses, and repair costs that could otherwise cripple a business.

In addition to general liability, many auto shops also benefit from garagekeepers and environmental liability coverage. As regulations tighten and customer expectations rise, having comprehensive protection ensures operational continuity and builds trust with clients.

Can you keep home insurance claim money

Can you keep home insurance claim moneyUnderstanding Auto Shop Liability Insurance: Protecting Your Automotive Business

Auto shop liability insurance is a crucial safeguard for businesses involved in vehicle repair, maintenance, and customization. This specialized form of commercial insurance is designed to protect auto repair shops from financial losses stemming from third-party claims of bodily injury, property damage, or advertising injuries that occur during business operations.

For instance, if a customer slips and falls in your shop or a technician accidentally damages a client's vehicle during repairs, liability insurance can help cover legal fees, medical expenses, and repair costs. Without adequate coverage, these incidents could result in significant out-of-pocket expenses or even lead to business closure.

Furthermore, many landlords, clients, and contracting agencies require proof of liability insurance before engaging with a repair shop, making it not only a financial safeguard but also a professional necessity. Selecting the right policy involves evaluating the scope of services offered, the size of the facility, and the number of employees, ensuring that the coverage aligns with the unique risks associated with running an automotive repair business.

What Does Auto Shop Liability Insurance Cover?

Auto shop liability insurance typically includes protection against several types of claims arising from day-to-day operations. Bodily injury coverage applies when a customer or visitor suffers a physical injury on your premises—such as slipping on an oil spill in the garage—and requires medical treatment.

Chase home mortgage insurance

Chase home mortgage insuranceProperty damage coverage pays for repairs or replacement if your work accidentally damages a client's vehicle or other property; for example, if a technician drops a tool onto a car’s hood, causing a dent. Additionally, personal and advertising injury protection shields your business from claims related to libel, slander, or copyright infringement in promotional materials.

Most policies also cover legal defense costs, regardless of whether the claim is valid, which can help alleviate the burden of lawsuits. It’s important to note that general liability insurance does not cover damage to property in your care, custody, or control—this requires a separate garagekeepers policy.

Why Is Liability Insurance Essential for Auto Repair Shops?

Liability insurance is not optional for responsible auto repair businesses—it's a fundamental component of risk management. The automotive environment involves numerous hazards, from tools and heavy machinery to flammable materials and moving vehicles, all of which increase the likelihood of accidents.

A single incident, such as a fire caused by welding sparks or a dropped engine damaging a customer’s car, can lead to expensive litigation. With liability insurance, shop owners gain peace of mind knowing that their business assets are protected against unforeseen events.

Cheap home insurance in michigan

Cheap home insurance in michiganMoreover, carrying insurance enhances credibility with customers who are more likely to trust a professional establishment that is properly insured. It can also fulfill contractual obligations with landlords, fleet operators, or government agencies that require proof of coverage before doing business. Ultimately, the relatively low cost of premiums pales in comparison to the high financial risks of operating without protection.

Factors That Influence Auto Shop Liability Insurance Costs

Several key factors determine the premium costs for auto shop liability insurance, allowing owners to better understand and potentially reduce their expenses.

The size and location of the shop play a significant role—larger facilities or those in urban areas with higher litigation rates typically face increased premiums. The range of services offered also affects pricing; shops performing high-risk activities like welding, frame repairs, or engine rebuilding are considered higher exposure.

Claims history is another critical factor; a business with multiple past claims will likely pay more due to perceived higher risk. Additionally, the number of employees and their level of training can influence rates, as properly trained technicians reduce the likelihood of accidents.

Cheap home insurance los angeles ca

Cheap home insurance los angeles caChoosing higher deductibles may lower monthly premiums, though it means paying more out of pocket if a claim occurs. Comparing quotes from multiple insurers and bundling with other policies, such as commercial property or garagekeepers insurance, can also help optimize coverage and cost.

| Factor | Impact on Premium | How to Mitigate Cost |

|---|---|---|

| Shop Size and Location | Larger or urban shops cost more to insure | Implement strict safety protocols and crime prevention measures |

| Types of Services Offered | High-risk services increase premiums | Provide ongoing employee training and use safety equipment |

| Claims History | More claims result in higher rates | Maintain a clean record with proper incident documentation |

| Employee Count | More employees can raise risk exposure | Invest in comprehensive training programs |

| Deductible Level | Higher deductibles lower premiums | Select a deductible your business can afford if a claim arises |

Comprehensive Guide to Auto Shop Liability Insurance Coverage and Protection

What is the average cost of liability insurance for auto repair shops?

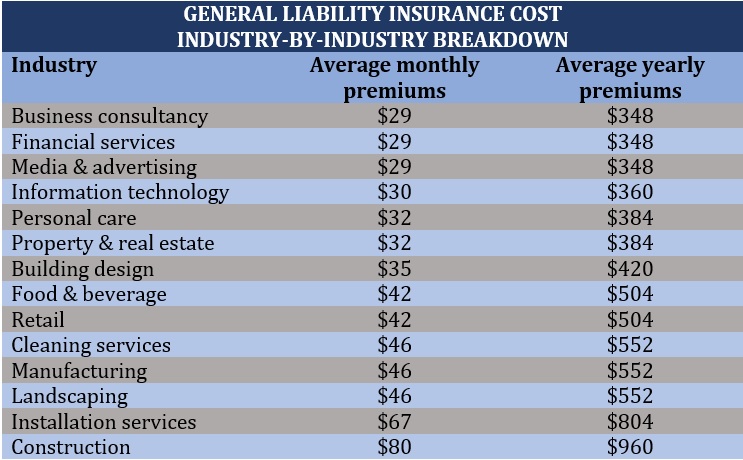

The average cost of liability insurance for auto repair shops typically ranges from $500 to $2,000 per year for general liability coverage. However, this amount can vary significantly based on several factors, including the size of the business, location, number of employees, services offered (such as engine repair, painting, or transmission work), and claims history.

Additional coverages like garage keepers liability, workers' compensation, and commercial property insurance are often bundled into a Business Owner's Policy (BOP), which can increase the total premium to between $2,000 and $5,000 annually. High-risk operations or shops in urban areas with higher litigation rates may face even steeper premiums.

Factors That Influence Liability Insurance Costs for Auto Repair Shops

- The geographical location of the auto repair shop plays a major role, as insurance rates in densely populated or high-crime areas tend to be higher due to increased risk of theft, vandalism, and liability claims.

- The size of the shop and the number of employees impact premiums because more workers increase the likelihood of workplace injuries, which can trigger higher workers' compensation costs—a component often tied to overall liability insurance pricing.

- The range of services offered is another key factor; shops performing high-risk work like welding, frame repair, or paint spraying are considered more hazardous and therefore face higher premiums than those offering basic oil changes or tire rotations.

Types of Liability Insurance Commonly Held by Auto Repair Shops

- General liability insurance covers third-party injuries and property damage, such as a customer slipping in the waiting area or a technician accidentally damaging a client’s vehicle during repairs.

- Garage keepers liability insurance is crucial for repair shops since it protects against damage to vehicles in their care, custody, or control, covering scenarios like fire, theft, or accidental damage while being serviced.

- Professional liability or mechanic's errors and omissions insurance helps cover claims related to faulty repairs, such as a brake job failure leading to a customer’s accident, which might result in a costly lawsuit.

How Auto Repair Shops Can Reduce Insurance Premiums

- Implementing comprehensive employee training programs can lower the risk of accidents and errors, showing insurers that the shop operates safely and responsibly, which may qualify the business for lower rates.

- Installing security systems like surveillance cameras, alarm systems, and secured storage areas can reduce the risk of theft and vandalism, leading to potential discounts on property and liability coverage.

- Choosing higher deductibles and bundling multiple policies (e.g., general liability, property, and workers' compensation) through a Business Owner's Policy can significantly reduce annual premiums while maintaining adequate protection.

What type of liability insurance is required to operate an auto repair shop?

General Liability Insurance

- General liability insurance is one of the most essential coverages for an auto repair shop, as it protects the business from third-party claims involving bodily injury, property damage, and personal injury that may occur on the premises or as a result of business operations.

- For example, if a customer slips and falls in the waiting area or a tool damages a client’s vehicle during repair, general liability insurance can help cover medical expenses, legal fees, and settlement costs.

- This policy typically includes coverage for advertising injuries, such as defamation or copyright infringement, which might arise from promotional materials used by the shop.

Garage Liability Insurance

- Garage liability insurance is specifically designed for auto service and repair businesses and covers damages to customers' vehicles while they are in the shop’s care, custody, or control.

- Unlike general liability, this policy addresses incidents such as fire, theft, accidental damage during repairs, or misplacement of a vehicle, which standard commercial policies may exclude.

- Many auto repair businesses are required by state regulations or lease agreements to carry garage liability insurance, especially if they handle vehicles regularly for servicing or storage.

Workers' Compensation Insurance

- Workers' compensation insurance is mandatory in most states for businesses with employees and is critical for auto repair shops due to the physically demanding and hazardous nature of the work environment.

- This insurance covers medical expenses, rehabilitation costs, and lost wages for employees who suffer work-related injuries or illnesses, such as burns, back injuries from lifting, or exposure to hazardous chemicals.

- In addition to providing employee benefits, workers' compensation helps protect the business from lawsuits filed by employees seeking damages for on-the-job injuries.

What does a $1,000,000 general liability insurance policy cost for an auto repair shop?

Factors That Influence the Cost of a $1,000,000 General Liability Policy for Auto Repair Shops

- The size and location of the auto repair shop significantly impact insurance premiums. Urban shops in high-traffic or high-crime areas often face higher rates due to increased risk exposure, including greater foot traffic and higher chances of accidents or property damage.

- The annual revenue and number of employees are key metrics insurers evaluate. Shops with higher revenue or more staff are typically seen as having greater operational risks, which can lead to higher premiums even for the same $1,000,000 coverage limit.

- The shop’s claims history plays a major role. A business with multiple prior liability claims is considered riskier, resulting in increased premiums. Conversely, a clean claims record over several years can lead to lower costs and possible discounts.

- Most auto repair shops can expect to pay between $1,000 and $3,500 annually for a $1,000,000 general liability policy. This range depends heavily on the shop’s operations, such as whether they perform high-risk services like welding or engine overhauls.

- Smaller garages with limited services and fewer customers often pay on the lower end of the spectrum, usually around $1,000 to $2,000 per year. These businesses present less exposure to third-party injury or property damage claims.

- Larger repair centers that handle commercial vehicles or offer comprehensive mechanical services may pay $2,500 to $3,500 or more annually. Additional risk factors such as handling hazardous materials or hosting numerous customer vehicles also contribute to higher pricing.

How Deductibles and Policy Add-Ons Affect Total Cost

- Choosing a higher deductible—such as $2,500 instead of $500—can reduce the annual premium. However, the business must be prepared to cover that amount out of pocket if a claim occurs, which affects cash flow during incidents.

- Common add-ons like garagekeepers legal liability, tools and equipment coverage, or umbrella policies will increase the total insurance cost. These endorsements are often essential for comprehensive protection but add to the base price of general liability insurance.

- Some insurers bundle general liability with property insurance or workers’ compensation, offering multi-policy discounts. While these packages increase the overall premium, the cost per coverage type may be lower compared to purchasing policies separately.

What is the average cost of auto shop liability insurance?

The average cost of auto shop liability insurance typically ranges from $500 to $2,000 per year for basic coverage, though it can exceed $5,000 annually depending on several variables.

Factors such as the size of the shop, number of employees, services offered, geographic location, and claims history all influence pricing. Collision repair shops, tire centers, and specialty garages may face higher premiums due to increased risk exposure.

Additionally, urban locations with higher accident or crime rates often see elevated insurance costs compared to rural areas. Business owners should obtain customized quotes from commercial insurance providers to get an accurate estimate based on their specific operations.

Factors That Influence Auto Shop Liability Insurance Costs

- The size and scope of operations play a significant role in determining premiums. Larger facilities with more bays, equipment, and employees typically face higher liability exposure, which insurers account for by increasing policy costs.

- Geographic location is another critical factor. Auto shops in densely populated cities or areas with high litigation rates tend to pay more for liability coverage due to increased risk of accidents and lawsuits.

- The types of services offered influence risk assessment. Shops performing high-risk tasks such as frame straightening, welding, or brake repairs may be charged higher premiums compared to those offering basic maintenance like oil changes or tire rotations.

Different Types of Coverage and Their Impact on Pricing

- Garage liability insurance is the core coverage for auto repair businesses and typically covers third-party bodily injury and property damage that occurs on the premises or due to operations. This coverage alone can range from $700 to $1,500 annually for small to mid-sized shops.

- Garagekeepers legal liability coverage protects customer vehicles in the shop’s care, custody, or control and can add $300 to $1,000 or more per year depending on the value of vehicles serviced.

- Workers’ compensation insurance, while not liability insurance per se, is often bundled or required alongside it. Premiums depend on payroll and job risk classification, and costs can range from $1,000 to $5,000+ annually, affecting overall insurance spending.

- Larger auto shops with multiple technicians and higher customer throughput are seen as having greater exposure to accidents and customer claims, leading to higher liability insurance premiums. Insurers assess annual revenue and employee count when calculating risk.

- A history of prior claims, especially those involving property damage or customer injury, can significantly increase premiums. Insurance companies view frequent claims as indicators of ongoing risk, which may lead to non-renewal or increased deductibles.

- Implementing safety protocols, employee training, and risk management practices can help reduce claims and, in turn, lower insurance costs over time. Some insurers offer discounts for shops that maintain clean claims histories or install security systems like surveillance cameras.

Frequently Asked Questions

What does auto shop liability insurance cover?

Auto shop liability insurance covers bodily injury and property damage that occurs on your premises or results from your operations. This includes customer injuries, damage to client vehicles, and third-party property damage.

It also helps pay for legal fees, settlements, or judgments. The policy typically covers accidents during repairs, test drives, or vehicle storage. It does not cover damage to your own tools or equipment, which requires separate coverage.

Is auto shop liability insurance required by law?

Auto shop liability insurance is not always legally required, but it is highly recommended and often required by landlords, lenders, or clients. While some states may not mandate it directly, operating without it exposes your business to significant financial risk.

Customer injuries or vehicle damage can lead to expensive lawsuits. Most auto repair shops need this coverage to operate safely and professionally. It also enhances credibility with customers and business partners.

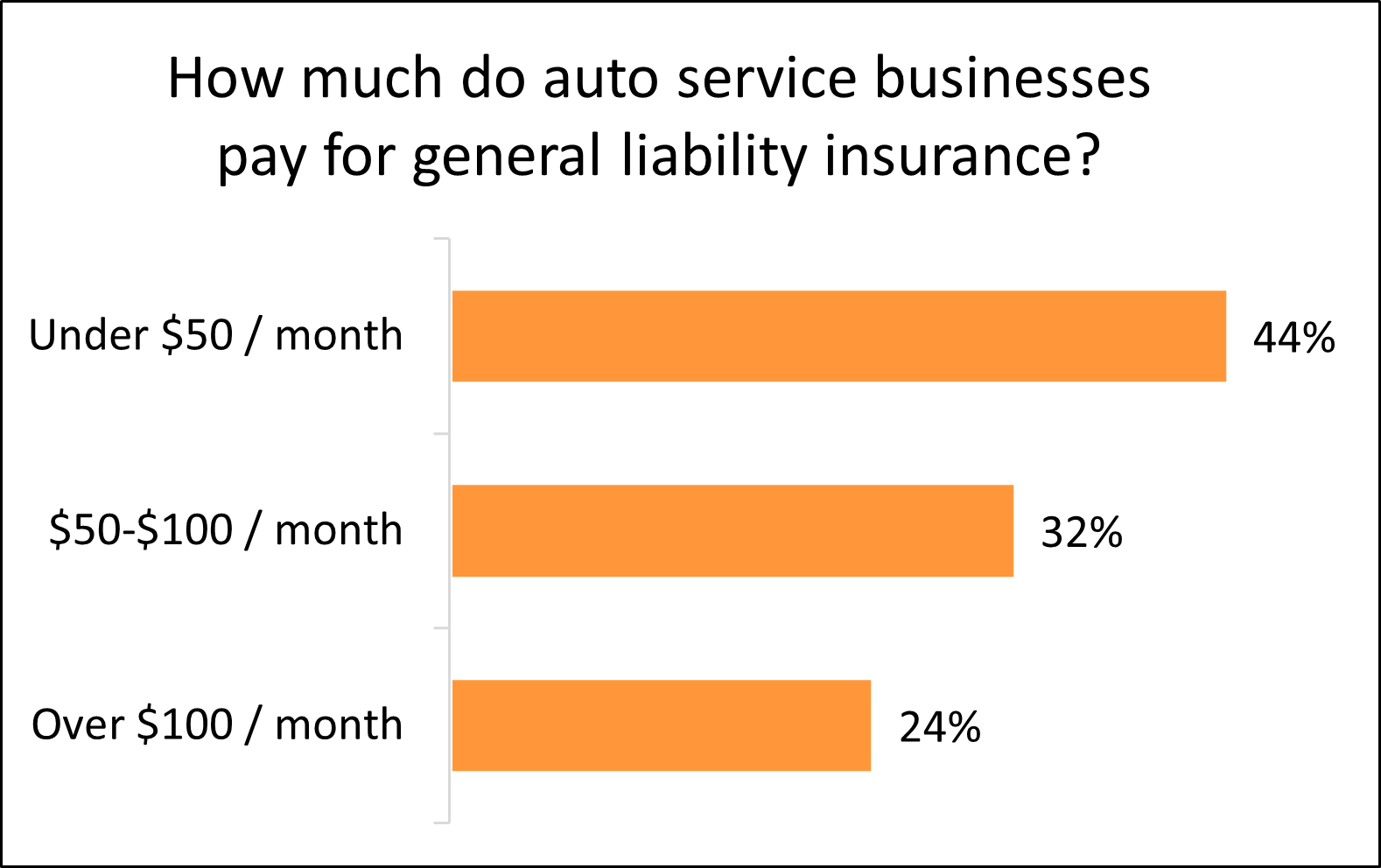

How much does auto shop liability insurance cost?

The cost of auto shop liability insurance typically ranges from $500 to $2,000 annually, depending on factors like shop size, location, services offered, and claims history.

High-risk operations, such as frame or engine repair, may increase premiums. Employers with more employees or higher sales volume may also face higher rates. Bundling with other policies like garage keepers or property insurance can reduce costs. Get quotes from multiple providers for the best rate.

What’s the difference between general liability and garage liability insurance?

General liability insurance covers third-party injuries and property damage not directly related to vehicle services, like a customer slipping in the waiting area. Garage liability insurance specifically covers accidents involving customer vehicles during repairs, test drives, or storage.

It includes bodily injury and property damage arising from garage operations. Many auto shops carry both policies to ensure comprehensive protection. Garage liability is essential for repair shops handling customer vehicles regularly.

Leave a Reply