Best home owners insurance florida

Choosing the best homeowners insurance in Florida requires careful consideration of coverage options, pricing, and provider reliability.

With the state’s high risk of hurricanes, flooding, and tropical storms, adequate protection is essential for every homeowner. A strong policy should cover dwelling damage, personal property, liability, and additional living expenses. Many standard policies exclude flood damage, making supplemental coverage crucial in vulnerable areas.

Top insurers offer competitive rates, excellent customer service, and optional upgrades like roof protection or hurricane deductibles. Comparing quotes, understanding local regulations, and evaluating financial strength ratings help homeowners make informed decisions for long-term security.

Risks of bundling home insurance with other products

Risks of bundling home insurance with other productsBest Homeowners Insurance in Florida: What You Need to Know

Florida homeowners face some of the most challenging insurance conditions in the United States due to frequent hurricanes, tropical storms, flooding, and high property values along the coastlines.

As a result, finding the best homeowners insurance in Florida requires a deep understanding of available coverage options, pricing trends, and the financial stability of insurance providers. The goal is to secure comprehensive protection that balances affordability with reliable claims support when disaster strikes.

With rising premiums and insurer withdrawals from the state, it’s more important than ever for Florida residents to compare policies carefully, understand policy limitations, and consider additional protections such as flood or windstorm insurance, which are typically not included in standard policies.

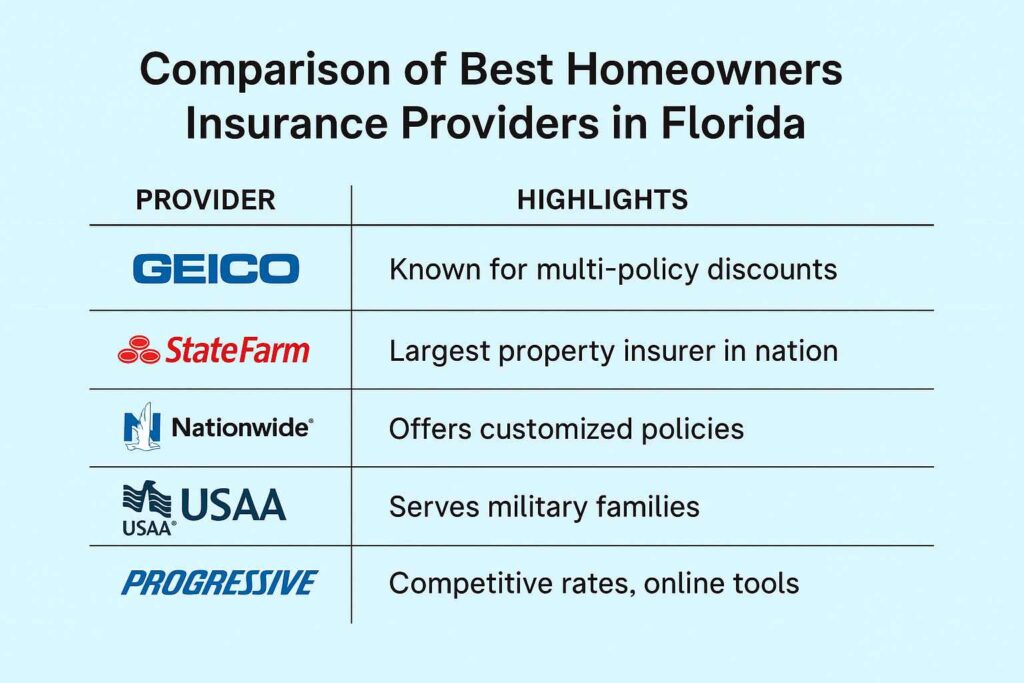

Top-Rated Homeowners Insurance Companies in Florida

Several insurance providers earn high marks for customer satisfaction, financial strength, and competitive pricing in the Florida market.

Rock hill second home insurance

Rock hill second home insuranceCompanies like Allstate, State Farm, and Liberty Mutual consistently rank among the top choices thanks to their robust coverage options and strong claims handling. Additionally, Florida Peninsula Insurance Company and Citizens Property Insurance Corporation — the state-run insurer of last resort — play crucial roles, especially in high-risk zones where private insurers may be reluctant to operate.

When evaluating top-rated providers, pay close attention to AM Best financial ratings, customer reviews on platforms like J.D. Power, and the availability of discounts such as bundling with auto insurance or installing storm-resistant features.

Factors That Impact Homeowners Insurance Rates in Florida

Insurance premiums in Florida are influenced by a combination of location-specific and property-related factors. Proximity to the coast dramatically increases risk exposure to hurricanes and wind damage, leading to higher premium costs.

Other key elements include the home’s construction type, age, roof condition, and whether it has been reinforced with impact-resistant windows or storm shutters. Insurers also examine credit-based insurance scores, claims history, and deductibles selected by the homeowner.

Role of home safety measures in insurance

Role of home safety measures in insuranceNotably, properties located within a designated windpool zone or those previously insured by carrier groups that have collapsed may face increased scrutiny and pricing. Understanding these variables allows homeowners to make informed adjustments to potentially reduce their rates.

Coverage Options and Endorsements to Consider

Standard homeowners insurance policies in Florida typically cover dwelling damage, personal property, and liability protection, but they often exclude coverage for flood damage and hurricane wind damage.

Homeowners in hurricane-prone areas should consider purchasing separate windstorm insurance through private carriers or the Florida Hurricane Catastrophe Fund (FHCF), while flood insurance is available via the National Flood Insurance Program (NFIP) or private insurers.

Additional endorsements such as code upgrade coverage, personal property replacement cost, and higher liability limits can significantly enhance protection. Ensuring your policy reflects the true cost of rebuilding — not just the market value — is essential in a state with volatile construction costs and strict building codes.

State farm home insurance rate increase 2025

State farm home insurance rate increase 2025| Insurance Company | Avg. Annual Premium (Estimate) | Key Features | Best For |

|---|---|---|---|

| State Farm | $2,100 | Strong local agent network, bundling discounts, reliable claims service | Suburban homeowners with multiple policies |

| Allstate | $2,400 | Flexible coverage options, digital tools, storm preparedness programs | Homeowners seeking customization |

| Citizens Property Insurance | $3,100 | Insurer of last resort, state-backed financial stability | Homeowners unable to secure private coverage |

| Florida Peninsula | $2,800 | Specializes in high-risk coastal properties | Coastal property owners in high-exposure zones |

| Liberty Mutual | $2,300 | Discounts for smart home devices and home safety features | Tech-savvy or newly renovated homes |

Best Homeowners Insurance in Florida: A Comprehensive Guide to Coverage and Providers

Which home insurance provider offers the best coverage and value for homeowners in Florida?

Top Home Insurance Providers for Florida Homeowners

- State Farm is frequently recognized as one of the most reliable home insurance providers in Florida, offering comprehensive coverage options and a strong local agent network. Their policies often include protection against wind damage and liability, which are crucial in a hurricane-prone state.

- Liberty Mutual stands out for its customizable policies and strong financial stability, ensuring prompt claims handling after severe weather events. They offer specialized endorsements for high-value homes and often provide discounts for storm-proofing improvements like impact-resistant windows.

- Florida Peninsula Insurance, now part of Assurant, is specifically designed for the Florida market and is a leading provider in high-risk coastal regions. The company specializes in wind-only coverage and partners with homeowners’ associations and property managers across the state.

Factors That Influence Coverage and Value in Florida

- Geographic location plays a major role in determining both premium costs and available coverage. Homes near the coast face higher wind and flood risks, leading to more expensive policies and mandatory windstorm coverage in many cases.

- Construction type and age of the home significantly impact insurance value. Newer homes built to modern hurricane codes typically receive better rates, while older structures may require costly upgrades to qualify for competitive coverage.

- The claims process and customer service responsiveness are critical, especially after widespread storm damage. Providers with local adjusters and 24/7 support help homeowners navigate repairs and rebuilding efficiently, which enhances the overall value of the policy.

Balancing Affordability and Comprehensive Protection

- To find the best value, homeowners should compare policies that include dwelling coverage, personal property protection, and loss of use, not just the lowest premium. Some budget insurers may exclude wind or water damage, which can lead to large out-of-pocket expenses after a storm.

- Discounts and bundling options, such as combining home and auto insurance, can improve value without sacrificing coverage. Many insurers offer reductions for installing security systems, storm shutters, or maintaining a claims-free history.

- It’s important to review policy exclusions carefully, particularly regarding hurricanes, mold, and flooding. While standard home insurance rarely covers floods, purchasing a separate policy through the National Flood Insurance Program (NFIP) or a private insurer can fill critical gaps in protection.

Frequently Asked Questions

What does home owners insurance in Florida typically cover?

Homeowners insurance in Florida typically covers the dwelling, other structures, personal property, liability, and additional living expenses. It protects against common perils like fire, storms, and theft. However, it usually excludes flood and hurricane wind damage, which require separate policies. Always review your policy details to understand specific coverages, limits, and exclusions based on your home’s location and construction.

Why is home insurance more expensive in Florida?

Home insurance is more expensive in Florida due to high risks from hurricanes, flooding, and coastal storms. The state's vulnerability to extreme weather increases the likelihood of claims, driving up premiums. Additionally, litigation rates and reinsurance costs contribute to higher prices. Insurers also account for construction costs and proximity to the coast when calculating rates, making coverage more costly than in many other states.

Do I need separate flood insurance in Florida?

Yes, you need separate flood insurance in Florida because standard homeowners policies do not cover flood damage. Florida’s low elevation and frequent storms make it highly susceptible to flooding. The National Flood Insurance Program (NFIP) offers flood coverage, and private options are also available. Even if you’re not in a high-risk zone, purchasing flood insurance is advisable due to the state’s unpredictable weather patterns.

Home insurance climate-related risks coverage

Home insurance climate-related risks coverageHow can I save on homeowners insurance in Florida?

You can save on homeowners insurance in Florida by installing storm-resistant features like impact windows, reinforced roofs, and shutters, which may qualify you for discounts. Raising your deductible, bundling policies, and maintaining a good credit score also help lower premiums. Shop around annually, compare quotes, and ask insurers about available discounts, including those for security systems, new homes, or being claims-free.

Leave a Reply