Can You Rent A Car Without Auto Insurance

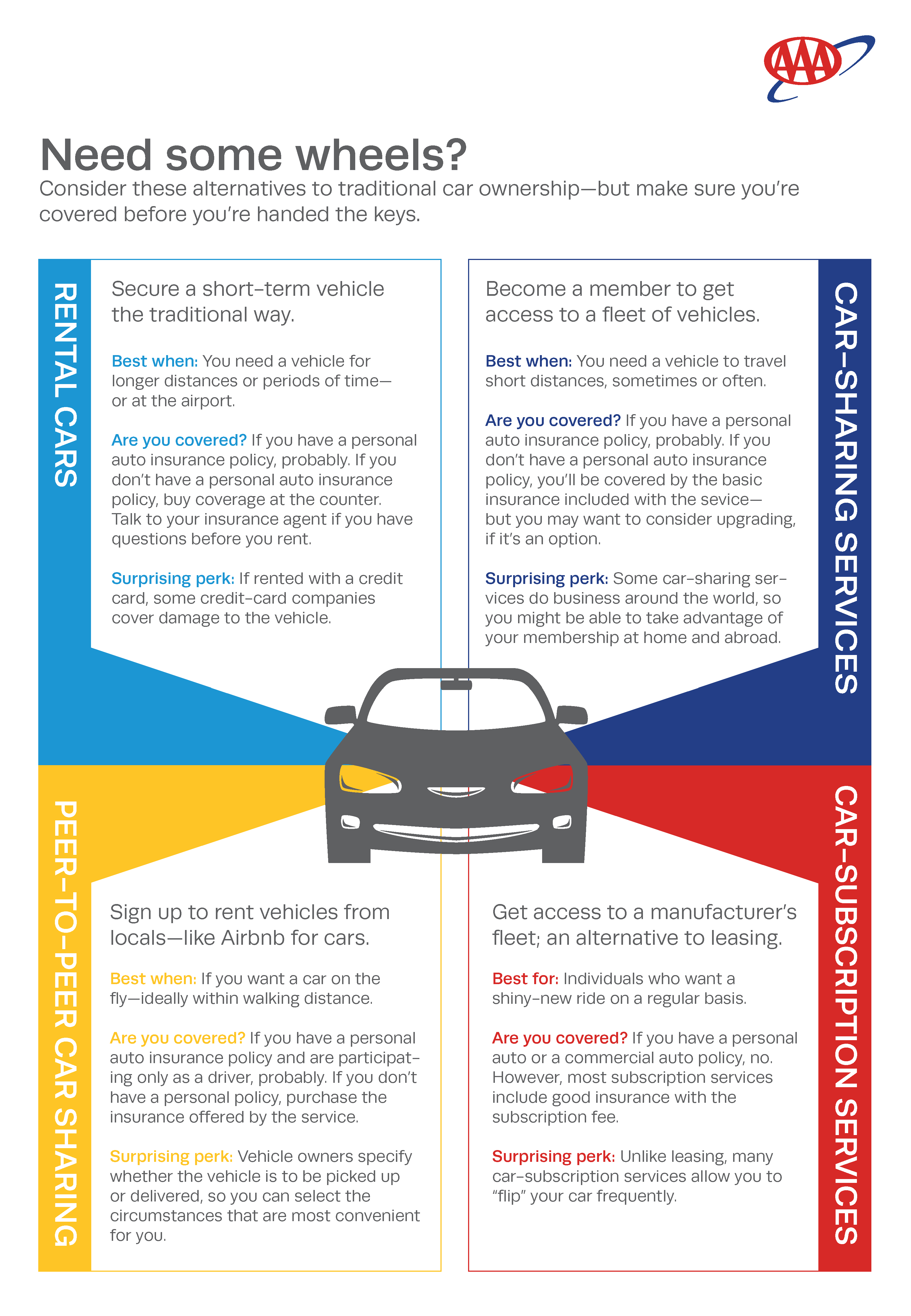

Renting a car without personal auto insurance is possible, but it comes with important considerations. Most rental agencies do not require customers to have their own insurance policy, yet they strongly encourage coverage to protect against liability and damages.

Rental companies typically offer their own insurance options, such as collision damage waiver and liability protection, which can increase the overall cost. Some credit cards also provide rental car insurance as a benefit, though coverage varies.

Understanding what protections are already available and what gaps need filling is crucial. Ultimately, while auto insurance isn’t mandatory to rent a car, driving without adequate coverage can lead to significant financial risk in the event of an accident.

Home insurance claim requirements

Home insurance claim requirementsCan You Rent a Car Without Auto Insurance?

Yes, it is possible to rent a car without having personal auto insurance, but there are important conditions and alternatives to consider. Car rental companies do not require renters to have their own auto insurance policy, but they do require the rental agreement to include some form of financial protection against damage or liability.

If you don’t have personal auto insurance, rental agencies typically offer optional coverage plans—such as Collision Damage Waiver (CDW), Loss Damage Waiver (LDW), Liability Insurance Supplement (LIS), and Personal Accident Insurance (PAI)—which can be purchased at the time of rental. While these options provide essential protection, they can significantly increase the rental cost. Additionally, some credit cards offer secondary or even primary rental car insurance coverage as a cardholder benefit, provided the rental charges are paid using the card and certain terms are met.

It’s crucial to review both credit card policies and rental agreements carefully before declining coverage, as going completely unprotected could expose you to large out-of-pocket expenses in case of an accident or vehicle damage.

What Types of Insurance Are Offered by Rental Car Companies?

Rental car companies typically offer several types of optional insurance to protect drivers who don’t have personal auto insurance.

How to choose home insurance with best claims process

How to choose home insurance with best claims processOne of the most common is the Collision Damage Waiver (CDW), which reduces or eliminates your financial responsibility if the rental car is damaged or stolen. Another key option is the Loss Damage Waiver (LDW), which combines CDW with theft protection. For liability concerns, the Liability Insurance Supplement (LIS) provides coverage for damages or injuries you may cause to others while driving the rental vehicle.

Personal Accident Insurance (PAI) covers medical expenses for the driver and passengers in the event of an injury, while Personal Effects Coverage (PEC) insures personal belongings inside the car against theft or damage. Although these coverages offer valuable protection, they come at an added cost—often $10 to $30+ per day—making it essential to assess whether you already have overlapping coverage through a personal auto policy or credit card.

Can Your Credit Card Provide Rental Car Insurance?

Many credit cards offer some level of rental car insurance as a complimentary benefit to cardholders, which can reduce or eliminate the need to purchase coverage directly from the rental company. Typically, this coverage applies only when the full rental cost is charged to the card and all rental terms are met, including declining the rental agency’s Collision Damage Waiver (CDW).

The coverage offered varies by card issuer and card tier—for example, premium travel cards like Chase Sapphire or American Express Platinum often provide primary rental car coverage, meaning the card’s insurance pays first without requiring you to file a claim with a personal insurer.

Mercury home owners insurance

Mercury home owners insuranceOther cards may offer secondary coverage, which only reimburses after your personal auto insurance pays out. It’s important to review the specific terms and limitations, such as rental duration limits, excluded vehicle types, and geographic restrictions, before relying solely on credit card insurance.

What Are the Risks of Renting Without Any Insurance Coverage?

Choosing to rent a car without any form of insurance coverage—whether personal, through a credit card, or from the rental company—poses substantial financial risks. If an accident occurs, you could be held personally liable for all repair costs, towing fees, loss of use charges, and third-party damages or injuries, which can amount to tens of thousands of dollars.

Rental agencies often impose strict policies and may charge you for even minor damages covered under typical insurance waivers. Without liability protection, you're also exposed to legal and medical costs if you cause an accident involving others.

Furthermore, lack of Personal Accident Insurance (PAI) could leave you responsible for emergency medical bills. While skipping insurance can reduce up-front rental costs, the potential for significant unexpected expenses makes this a highly risky decision.

| Coverage Type | What It Covers | Typical Cost | Key Notes |

|---|---|---|---|

| Collision Damage Waiver (CDW) | Damage or theft of the rental vehicle | $10–$20/day | Reduces out-of-pocket costs; often included in credit card coverage |

| Liability Insurance Supplement (LIS) | Damage or injury to others | $10–$15/day | Minimum coverage varies by state; essential if no personal auto policy |

| Personal Accident Insurance (PAI) | Medical expenses for driver/passengers | $3–$7/day | Covers emergency treatment and accidental death |

| Personal Effects Coverage (PEC) | Stolen or damaged personal items | $3–$5/day | Often redundant with homeowner’s/renter’s insurance |

| Credit Card Rental Insurance | Varies: CDW, sometimes primary or secondary | Free (with eligible card) | Must charge entire rental to card; read terms carefully |

Can You Rent a Car Without Auto Insurance? A Comprehensive Guide

Is It Possible to Rent a Car Without Personal Auto Insurance?

Yes, it is possible to rent a car without personal auto insurance in many cases. Car rental companies typically offer their own insurance options, and some travelers may rely on alternative coverage from credit card policies or other sources. However, the ability to rent without personal insurance depends on several factors such as the rental company's policies, the state or country where the rental occurs, and the renter's age and driving history.

While personal auto insurance is not always required, rental agencies do require some form of financial responsibility, usually met through their own insurance products or third-party coverage. It’s essential to understand what protections are already available and what gaps may need filling before declining the rental company’s insurance offer.

Understanding Rental Company Insurance Options

- Rental car companies commonly offer several insurance products, including collision damage waiver (CDW) or loss damage waiver (LDW), which do not technically provide insurance but rather a promise not to hold the renter responsible for damage to the rental vehicle under certain conditions. These waivers often come at an additional daily cost but can offer significant peace of mind.

- Many agencies also offer liability insurance coverage, which protects third parties if the renter causes injury or property damage. This type of coverage is especially important in locations where minimum liability coverage is legally required, and the renter does not have their own policy in place.

- Supplemental liability insurance, personal accident insurance, and personal effects coverage are other available options that address medical expenses, death benefits, or loss of personal belongings during the rental period. These policies can be purchased individually or bundled together, depending on the rental agency and geographic location.

Leveraging Credit Card Rental Car Coverage

- Many premium credit cards provide rental car insurance as a cardholder benefit, typically covering collision damage and theft when the rental is charged in full to the card. This coverage often acts as secondary insurance, meaning it pays after other available policies have been exhausted, but some cards offer primary coverage.

- To qualify for credit card insurance, renters must decline the rental company’s CDW or LDW and pay for the rental entirely using the eligible credit card. Renters should also verify the specific terms, limits, and exclusions of their card’s policy, as coverage varies by issuer and card type.

- It's important to check whether the credit card coverage applies internationally and for all vehicle types. Some policies exclude luxury cars, large trucks, or rentals in certain countries, so understanding the limitations is critical before assuming protection is in place.

Legal and Practical Considerations by Location

- State laws in the U.S. and local regulations internationally often dictate minimum insurance requirements for operating a vehicle. In some states, rental cars are considered commercially insured, meaning the rental company maintains liability coverage on the vehicle, which may fulfill legal requirements even if the renter has no personal policy.

- Renters without personal insurance should review the rental agreement carefully to understand what liability protection is automatically included by law or policy and what they must purchase separately. For example, in New York and New Jersey, rental companies are required to offer a minimum level of liability insurance that renters can accept or decline in writing.

- Foreign countries may have different rules; some require renters to purchase local insurance regardless of home country coverage. In certain European countries or in Mexico, separate liability or border coverage might be mandatory. Understanding these requirements before arrival can prevent legal issues and unexpected charges at the rental counter.

What are the legal consequences of driving uninsured in Tennessee when renting a car?

Driving a rental car without insurance in Tennessee carries serious legal and financial consequences. State law mandates that all vehicles operated on public roads must have minimum levels of liability insurance.

This requirement applies regardless of whether the vehicle is personally owned or rented. Failure to maintain valid insurance coverage while operating a rental car can result in citations, fines, license suspension, and personal liability for damages in the event of an accident.

Additionally, rental car companies may charge significantly higher fees or pursue legal action if their vehicle is operated without proper coverage. Understanding the legal framework and available insurance options is crucial to avoid penalties and remain compliant with Tennessee law.

Penalties for Driving Uninsured in Tennessee

- Tennessee imposes strict penalties on drivers caught operating any vehicle, including rental cars, without valid liability insurance. First-time offenders may face fines ranging from $100 to $300, depending on the county and court discretion.

- Drivers may experience immediate suspension of their driver’s license and vehicle registration. The Tennessee Department of Safety and Homeland Security will not reinstate a license until proof of insurance is provided and reinstatement fees are paid.

- Repeat offenses within a three-year period result in increased fines, mandatory proof of future insurance (SR-22 filings), and potential impoundment of the vehicle. Using a rental car without insurance does not exempt the driver from these penalties.

Rental Car Company Insurance Policies and Liability

- Rental car companies typically offer supplemental liability insurance (SLI), personal accident insurance (PAI), and loss damage waiver (LDW) options at the time of rental. While these are not mandatory under state law, declining coverage leaves the renter personally responsible for damages.

- If a renter drives uninsured and causes an accident, the rental company may charge the full replacement cost of the vehicle, administrative fees, and lost rental income. These charges can amount to thousands of dollars and may be sent to collections or result in civil litigation.

- Even if personal auto insurance or credit card benefits provide some coverage, the renter must verify that these policies extend to rental vehicles in Tennessee and meet state minimum requirements: $25,000 for bodily injury per person, $50,000 per accident, and $10,000 for property damage.

Financial and Legal Risks After an Accident

- In the event of an accident, an uninsured driver operating a rental car is personally liable for all damages exceeding any limited coverage from the rental agreement or third parties. This includes medical expenses, third-party vehicle repairs, and legal costs if sued.

- Victims of accidents caused by uninsured renters may file civil lawsuits seeking compensation. If a judgment is entered, it could lead to wage garnishment, bank account levies, or liens on personal property.

- Being involved in an accident while uninsured may also result in long-term increases in future insurance premiums or difficulty obtaining coverage from insurers, as it is considered a high-risk behavior.

What Do You Need to Rent a Car in Ohio Without Personal Auto Insurance?

Rental Company Requirements and Eligibility Criteria

- Rental car companies in Ohio typically require renters to be at least 21 years of age, although drivers under 25 may be subject to a young renter surcharge. This policy varies by company, so it is important to check with the specific rental agency in advance.

- A valid government-issued driver’s license is mandatory. The license must be current and issued by the renter’s state or country of residence. International renters may need an International Driving Permit in addition to their home country license.

- Renters must provide a major credit card in their own name to secure the rental. Debit cards are sometimes accepted but often come with additional verification steps such as credit checks, proof of return travel, or a larger security hold on funds.

Supplemental Insurance Options at Rental Counters

- When renting a car without personal auto insurance in Ohio, customers can purchase supplemental liability coverage directly from the rental company. This coverage helps pay for damage or injuries caused to others during the rental period and may be required depending on state regulations or the rental company's policy.

- Rental agencies typically offer a Loss Damage Waiver (LDW) or Collision Damage Waiver (CDW), which is not insurance but a service that limits the renter's financial responsibility for damage to or theft of the rental vehicle. While optional, most renters without personal coverage choose this protection.

- Some rental counters also provide additional protection products such as Personal Accident Insurance (PAI) for medical expenses and Personal Effects Coverage (PEC) for stolen belongings. These are optional add-ons but may provide additional peace of mind during the rental period.

Alternative Sources of Coverage for Uninsured Renters

- Some credit cards provide secondary or even primary rental car insurance benefits when the rental is charged in full to the card. It is essential to contact the card issuer before renting to confirm the level of coverage, eligible rental companies, and any exclusions.

- Travel insurance policies often include rental car coverage as part of their protection plans. Renters should carefully review the policy documents to ensure that the rental car usage in Ohio is covered, including liability and physical damage.

- Non-owner auto insurance policies are another option for individuals who frequently rent vehicles. This type of policy provides liability, and sometimes collision and comprehensive coverage, for vehicles the renter does not own, serving as a longer-term solution for those without personal auto insurance.

Can you rent a car in Florida without having auto insurance?

Yes, you can rent a car in Florida without having personal auto insurance, but with important caveats. Rental car companies in Florida are required by law to offer certain levels of insurance coverage, and while you are not legally obligated to purchase additional insurance if you already have coverage, you cannot rent a car without some form of insurance protection active during the rental period.

If you don’t have a personal auto insurance policy, the rental company will typically require you to purchase their own insurance options, such as a Collision Damage Waiver (CDW) or Loss Damage Waiver (LDW), to cover potential damages.

Additionally, Florida does not require drivers to carry personal injury protection (PIP) on rental cars since the rental company’s fleet insurance usually covers the minimum required liability. However, declining all insurance options is possible but comes with significant financial risk if an accident occurs.

What Insurance Coverage Is Required to Rent a Car in Florida?

- Rental car companies in Florida must ensure that every rented vehicle has at least the state’s minimum liability coverage, which currently includes $10,000 in personal injury protection (PIP) and $10,000 in property damage liability (PDL). This coverage is typically included automatically in the rental agreement through the company's own insurance fleet policy.

- If you do not have a personal auto insurance policy, you may be required to purchase supplemental liability insurance or a damage waiver directly from the rental company to proceed with the rental. These terms protect you financially if you cause injury or damage to others.

- While you can decline additional coverage, such as a Collision Damage Waiver (CDW), you will remain financially responsible for any damage to the rental vehicle. Most major credit cards offer some form of rental car coverage, but this often only applies if you decline the rental company’s CDW and charge the full rental to an eligible card.

What Happens If You Decline All Rental Car Insurance in Florida?

- When you decline all insurance options at the rental counter, you are accepting full financial liability for any damage to the rental vehicle, theft, or damage to third parties. This includes scratches, dents, or more serious accidents.

- Rental companies may place a hold on your credit card for a large deposit, often ranging from $200 to over $500, which serves as a security deposit against potential damages. This hold can remain for several days or even weeks after returning the car, depending on your financial institution.

- If an accident occurs and you lack insurance—either personal, credit card, or from the rental agency—you will be responsible for all repair costs, administrative fees, and potential loss-of-use charges. These fees can accumulate quickly, sometimes exceeding thousands of dollars.

How Can You Avoid Purchasing Rental Car Insurance in Florida?

- Check your personal auto insurance policy first. Many personal car insurance policies extend coverage to rental vehicles, including liability and physical damage, when traveling in-state or out-of-state, especially for short-term rentals. Confirm the extent of this coverage with your provider before renting.

- Review the benefits of your credit card. Many premium credit cards, such as Visa Infinite, Mastercard World Elite, or certain American Express cards, offer rental car insurance when you use the card to pay for the rental and decline the rental company’s damage waiver. This coverage typically includes collision and theft protection but may exclude liability coverage or exclude rentals over a certain number of days.

- Ask the rental agent for a detailed breakdown of the included insurance coverage. In Florida, the rental company’s fleet insurance usually covers the state-mandated liability minimums, so if you have personal insurance or credit card coverage for damage, you may only need to verify that all required layers are properly accounted for to legally drive the vehicle.

Frequently Asked Questions

Can You Rent A Car Without Personal Auto Insurance?

Yes, you can rent a car without personal auto insurance. Most rental companies offer their own insurance options, like collision damage waivers and liability coverage.

These protect you in case of accidents or damage. While not legally required, having coverage is strongly recommended to avoid high out-of-pocket costs. Credit cards may also provide some rental insurance benefits, so check your card’s policy before declining the rental company’s offers.

What Happens If I Decline Rental Car Insurance?

If you decline rental car insurance, you become financially responsible for any damage or theft to the vehicle. Without coverage, you could face significant repair or replacement costs.

Some credit cards offer limited protection, but it may not cover all scenarios. Additionally, you may still be liable for loss-of-use fees and administrative charges. Carefully review your options and existing coverage before deciding to decline the rental company’s insurance plans.

Does My Credit Card Cover Rental Car Insurance?

Many credit cards offer rental car insurance as a perk, but coverage varies. Typically, it includes collision damage waiver protection but not liability insurance.

You must charge the entire rental to the card and decline the rental company’s similar coverage. Always verify the terms, limits, and exclusions with your card issuer. Some cards require you to file claims through them and may not cover luxury vehicles, long-term rentals, or certain countries.

Is Rental Car Insurance Required By Law?

Rental car insurance isn’t universally required by law, but liability coverage is often mandatory depending on the state or country. Rental companies usually include basic liability insurance, but limits may be low. You must meet local legal requirements for liability protection.

While you can decline additional coverage like personal accident insurance or personal effects protection, doing so leaves you exposed to related risks and costs. Always confirm legal minimums before renting.

Leave a Reply