Do You Need Special Car Insurance For Doordash

Driving for Doordash can be a flexible way to earn extra income, but it raises important questions about car insurance coverage. Standard personal auto policies typically don’t cover accidents or damages that occur while delivering food for pay.

This leaves many dashers vulnerable to financial risk if they’re involved in an incident during an active delivery. Doordash does offer some insurance, but it only applies during specific delivery periods and may not fully protect drivers. Understanding the gaps in coverage and whether you need supplemental insurance is crucial for protecting yourself and your vehicle while on the job.

Do You Need Special Car Insurance for Doordash?

Yes, you do need to consider additional or specialized car insurance coverage when driving for Doordash, although you don’t need a completely separate policy right from the start. While your personal auto insurance may provide some level of coverage during the early stages of your delivery journey—such as driving to pick up an order—it typically excludes commercial use, which includes food delivery.

Do You Need Special Car Insurance For Instacart

Do You Need Special Car Insurance For InstacartThis is where the potential risk lies: if you're involved in an accident while actively delivering for Doordash, your personal insurer might deny the claim due to the commercial nature of your activity. Fortunately, Doordash does provide intermediate insurance coverage once you've accepted a delivery, offering liability, uninsured motorist, and, in some states, collision and comprehensive protection.

However, this coverage has gaps, especially in the time between logging into the app and accepting your first order. To fully protect yourself, many drivers opt for a commercial auto insurance policy or a ridership endorsement on their existing policy that explicitly covers delivery driving.

When Does Doordash’s Insurance Coverage Start?

Doordash provides insurance coverage in two key phases, but it doesn’t cover you at all times while logged into the app. The first phase, known as Period 1, begins the moment you log into the Doordash app and become available for delivery. However, Doordash’s official policy states that it does not provide coverage during this time.

This leaves a critical coverage gap when you're waiting for an order. Coverage officially kicks in during Period 2, which starts when you accept a delivery request. At this point, Doordash offers liability insurance, including bodily injury and property damage coverage to others if you're at fault. Then, during Period 3, which spans from picking up the order to delivering it, the same liability coverage continues.

Do You Need Special Car Insurance To Deliver Food

Do You Need Special Car Insurance To Deliver FoodAlthough this layered approach offers protection, it does not include collision or comprehensive coverage unless provided by the driver’s personal policy or an additional endorsement. Understanding these timing specifics is essential to avoid financial risk in the event of an accident.

Does Your Personal Auto Insurance Cover Delivery Driving?

Most standard personal auto insurance policies exclude commercial activities, which include food delivery services like Doordash. These policies assume your vehicle is being used for personal purposes—such as commuting, errands, or leisure—and not for business use.

If you get into an accident while delivering for Doordash, your insurer may deny your claim upon discovering you were engaged in paid driving, potentially leading to policy cancellation or legal complications. Some insurers may allow you to add a ridership or business-use endorsement to your existing policy to legally cover delivery driving, but this often increases your premium.

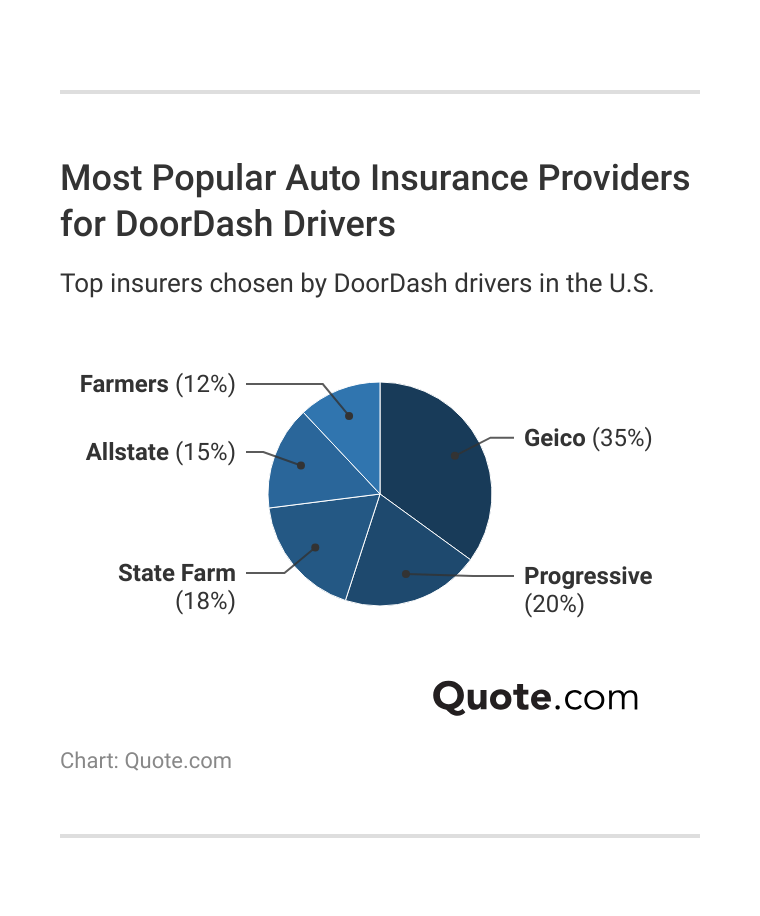

Companies like Progressive, State Farm, and Allstate offer such commercial-use options or specific gig economy insurance plans. Therefore, it’s critical to disclose your delivery work to your insurer to ensure you’re properly covered. Relying solely on personal coverage without disclosure can leave you financially exposed.

Do You Need Special Car Insurance To Deliver Pizza

Do You Need Special Car Insurance To Deliver PizzaWhat Types of Insurance Coverage Are Recommended for Doordash Drivers?

To stay fully protected, Doordash drivers should consider three main types of insurance coverage: personal auto insurance with a business-use endorsement, commercial auto insurance, or gap insurance through a third-party provider. The business-use endorsement is often the most cost-effective upgrade to a standard personal policy, offering coverage while you're actively working.

Commercial auto insurance, though more expensive, provides comprehensive protection tailored for gig drivers and is advisable for those who deliver full-time or frequently. This type of insurance covers liability, collision, and comprehensive damage regardless of the driving phase.

Additionally, drivers should understand the coverage limits provided by Doordash during Periods 2 and 3, which typically offer up to $1 million in liability coverage but may exclude damage to your own vehicle. For optimal protection, combining a Doordash-approved endorsement with Doordash’s own insurance can bridge critical gaps.

| Coverage Type | When It Applies | Key Benefits | Limitations |

|---|---|---|---|

| Personal Auto Insurance | Periods outside active delivery | Covers personal driving and commuting | Excludes commercial use; claims denied during deliveries |

| Doordash Provided Insurance | Period 2 & 3 (after accepting a delivery) | $1M liability coverage for third-party damages | No coverage during Period 1; limited collision/comprehensive outside some states |

| Commercial or Business-Endorsed Insurance | 24/7 while working for Doordash | Full protection including collision & comprehensive | Higher premiums; required for full-time drivers |

Do You Need Special Car Insurance for Doordash Deliveries?

Do You Need Specific Car Insurance to Deliver for DoorDash?

Do You Need Special Car Insurance To Drive For Uber

Do You Need Special Car Insurance To Drive For UberDoes DoorDash Provide Insurance Coverage for Delivery Drivers?

Yes, DoorDash does provide some level of insurance coverage for its delivery drivers, but it's important to understand the scope and limitations. The company offers contingent liability coverage that becomes active only when a driver is actively working on a delivery—specifically, after accepting an order and before delivering it.

This coverage includes liability protection for injuries to others or damage to their property caused by the driver during an eligible delivery. However, this insurance does not cover damage to the driver’s own vehicle, personal items inside the car, or any incidents that occur outside of an active delivery, such as while en route to pick up an order without an accepted job.

- DoorDash's insurance activates only during specific delivery periods—after accepting a trip and before completing the delivery.

- The coverage mainly includes third-party liability, such as bodily injury or property damage the driver may cause to others.

- It does not cover comprehensive or collision damage to the driver's personal vehicle, nor does it provide personal injury protection or uninsured motorist coverage.

Can You Use Personal Auto Insurance for DoorDash Deliveries?

Using standard personal auto insurance for DoorDash deliveries is risky and may violate the terms of your policy. Most personal car insurance policies are designed for personal or commuting use and exclude coverage when the vehicle is used for commercial purposes, such as delivering food for pay.

If you’re involved in an accident while delivering for DoorDash and your insurer determines you were working, they could deny the claim or even cancel your policy. Some insurance companies offer endorsements or specific rideshare coverage that extends protection to app-based delivery work, but this must be formally added to your policy.

- Typical personal auto insurance may not cover accidents that happen during delivery activities, especially when carrying food for compensation.

- Insurers classify delivery driving as commercial use, which often voids standard personal policy protections.

- Adding a rideshare or delivery endorsement to your policy can bridge coverage gaps during different stages of a delivery.

While not legally required by DoorDash, obtaining rideshare or commercial auto insurance can provide essential additional protection. These specialized policies are designed to cover all phases of delivery work, including when you're logged into the app waiting for orders, traveling to pick up food, and actively making deliveries.

Standard personal insurance usually only covers you when you're not working, and DoorDash’s contingent coverage starts later in the process, leaving a potential coverage gap. A rideshare or delivery-specific policy ensures continuous protection and can cover vehicle damage, medical expenses, and legal costs that DoorDash’s insurance or a personal policy might exclude.

- Rideshare or delivery-specific insurance fills the gap between personal policies and when DoorDash’s coverage begins.

- These policies typically cover all periods of delivery activity, including while the app is on but before an order is accepted.

- They often include broader protections such as collision, comprehensive, and personal injury coverage tailored to commercial driving risks.

What is the most affordable car insurance option for Doordash drivers?

- Many standard personal auto insurance policies do not cover commercial activities like food delivery through Doordash, but some insurers now offer rideshare endorsements that extend coverage during specific periods of delivery, such as between accepting a delivery and dropping off the order.

- Companies like GEICO, Progressive, and State Farm provide these endorsements at a relatively low additional cost, typically increasing premiums by 10% to 20%, which makes them one of the most cost-effective options for drivers who only dash occasionally.

- It's crucial to inform your insurer that you drive for Doordash, as failing to disclose this may result in denied claims. With proper disclosure, adding a rideshare endorsement ensures protection during commercial use while keeping rates more affordable than full commercial policies.

Pay-Per-Mile Insurance for Low-Mileage Dashers

- Insurers such as Metromile (now part of Liberty Mutual) and Nationwide offer pay-per-mile plans, where you pay a base rate plus a set fee for every mile driven, making it highly economical for Doordash drivers who work part-time or in low-traffic areas.

- These plans are ideal if your delivery mileage is inconsistent or below average, as you’re not charged for days when you’re not driving, potentially saving hundreds of dollars annually compared to traditional fixed-rate policies.

- Pay-per-mile insurance also includes full coverage during all stages of delivery, including commercial use, without requiring a separate endorsement, simplifying the process and reducing the risk of coverage gaps.

Multi-Policy and Usage-Based Discounts

- Combining your auto insurance with other policies like renters or homeowners insurance under the same provider often results in a multi-policy discount, which can reduce overall insurance costs by 10% to 25%, making it a smart strategy for saving money.

- Many insurers offer usage-based programs such as Progressive's Snapshot or Allstate's Drivewise, which track driving habits through a mobile app or plug-in device and reward safe driving with lower premiums, sometimes up to 30% off after a few months.

- For Doordash drivers who maintain a clean driving record and practice safe habits—such as avoiding late-night driving or hard braking—usage-based programs can significantly cut costs while still providing adequate coverage for delivery activities.

Frequently Asked Questions

Do I need special car insurance to deliver for DoorDash?

Yes, you need to ensure your personal auto insurance covers delivery driving. Most standard policies don't cover commercial use. DoorDash provides secondary liability insurance during active deliveries, but it's wise to get a rideshare or commercial policy for full protection. Always check with your insurer to confirm coverage and avoid potential gaps that could leave you financially responsible in case of an accident.

Does DoorDash provide insurance while I'm driving?

Yes, DoorDash offers insurance coverage during specific periods of delivery. When you're actively dashing—picked up an order and en route to delivery—DoorDash provides commercial liability insurance. This includes bodily injury and property damage coverage. However, this coverage is secondary when you have personal insurance and doesn’t cover items in your car or personal vehicle damage. Always verify your personal policy for protection during inactive periods.

Can I use my personal car insurance for DoorDash deliveries?

Using only personal car insurance for DoorDash deliveries is risky. Most personal policies exclude commercial activities like food delivery. If you’re in an accident while dashing, your claim could be denied. While DoorDash offers some insurance, it's limited. To stay protected, consider upgrading to a rideshare endorsement or commercial policy that explicitly covers food delivery driving.

What type of insurance does DoorDash offer drivers?

DoorDash provides commercial liability insurance with coverage for bodily injury and property damage when you’re actively delivering. This coverage applies after accepting a dash and lasts until delivery completion. It doesn’t cover downtime between orders, vehicle damage, or personal belongings. The policy acts as secondary insurance if you have personal coverage, so having your own rideshare or commercial policy is strongly recommended for comprehensive protection.

Leave a Reply