Does home insurance cover electrical fire

Electrical fires pose a significant risk to homeowners, often resulting from faulty wiring, overloaded circuits, or malfunctioning appliances.

When such a fire occurs, one pressing question arises: does home insurance cover electrical fire damage? In most cases, standard homeowners insurance policies do provide coverage for electrical fires, including structural damage and personal property loss.

However, coverage depends on the cause of the fire, maintenance history, and policy specifics. Negligence or lack of upkeep may lead to denied claims. Understanding your policy’s terms and taking preventative measures is crucial for protection.

Home insurance guaranteed replacement cost coverage 2025

Home insurance guaranteed replacement cost coverage 2025Does Home Insurance Cover Electrical Fire Damage?

Yes, most standard home insurance policies do cover damage caused by electrical fires, as long as the fire was accidental and not the result of neglect, improper maintenance, or intentional actions.

Homeowners insurance typically falls under named perils or open perils (also called comprehensive coverage) policies, both of which usually include fire damage as a covered event. An electrical fire that starts due to a sudden and unexpected malfunction—like a short circuit, overloaded power strip, or faulty appliance—is generally considered accidental and thus eligible for a claim.

However, insurers may investigate the cause thoroughly to ensure that the homeowner wasn’t aware of pre-existing electrical hazards, such as outdated wiring or repeated circuit breaker trips that were not addressed properly. Coverage generally extends to structural damage to the home, destruction of personal belongings, and additional living expenses if the home becomes uninhabitable during repairs.

What Types of Electrical Fires Are Typically Covered?

Standard homeowners insurance policies cover electrical fires that occur due to sudden and accidental causes, such as a surge, appliance malfunction, or issues with internal home wiring that are not due to long-term deterioration or lack of maintenance.

Home insurance in fair oaks ranch

Home insurance in fair oaks ranchFor example, if a space heater shorts circuit and ignites nearby curtains, the resulting fire damage would typically be covered. Similarly, if an electrical panel fails unexpectedly and sparks a fire within the walls, the structural and personal property damage would likely be included under dwelling and personal property coverage.

However, it's important to note that gradual wear and tear, outdated knob-and-tube wiring not brought up to code, or issues arising from DIY electrical work done incorrectly are often excluded. Insurers expect homeowners to maintain their electrical systems responsibly, and failure to do so can jeopardize a claim.

What Expenses Are Included in an Electrical Fire Insurance Claim?

When an electrical fire is covered, home insurance can reimburse various types of expenses depending on the policy terms.

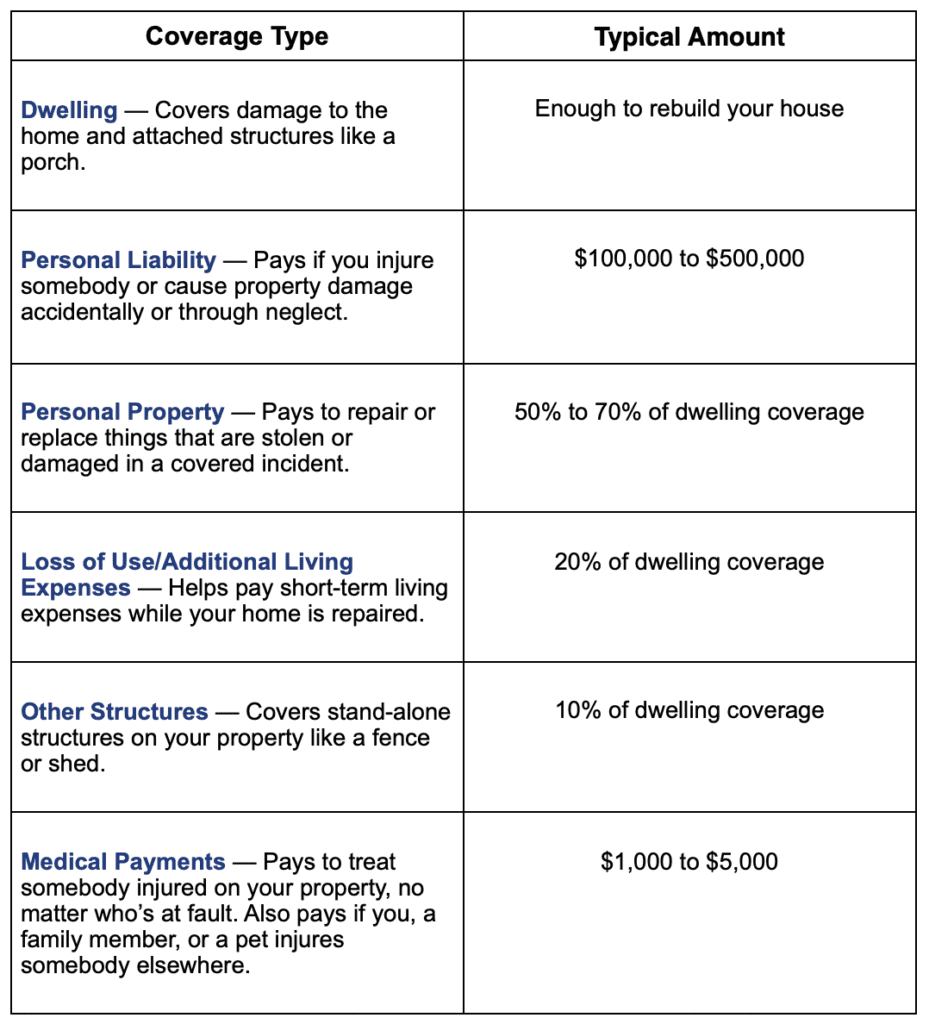

The dwelling coverage pays for repairs or rebuilding of the home's structure, including walls, floors, and built-in appliances damaged by fire or smoke. Personal property coverage compensates for lost or damaged belongings like furniture, clothing, and electronics, either at actual cash value or replacement cost, depending on the policy.

Home insurance insurance quote

Home insurance insurance quoteAdditionally, loss of use coverage, also known as additional living expenses (ALE), helps pay for hotel stays, meals, and other necessary costs if the home is unlivable during repairs. Some policies may also cover removal of debris and fire department service charges, though these specifics can vary. Keeping a detailed home inventory can greatly streamline the claims process and maximize reimbursement.

How Can You Ensure Your Electrical Fire Claim Is Approved?

To increase the likelihood of a successful claim after an electrical fire, homeowners should take immediate and documented steps following the incident. First, report the fire to emergency services and your insurance company as soon as it's safe to do so.

It's important not to discard damaged items before an adjuster inspects them, as proof of loss is crucial. You should also maintain records of any repairs or temporary living expenses. Preventative steps before a fire—such as having your electrical system inspected, upgrading outdated wiring, and avoiding overloading circuits—can also support your claim by demonstrating responsible maintenance.

If the cause of the fire is contested, insurers may require a report from a licensed electrician or fire investigator. Providing detailed documentation, cooperating with the adjuster, and clearly showing that the fire was accidental rather than due to negligence will strengthen your case.

| Coverage Type | What It Covers | Limitations/Exclusions |

|---|---|---|

| Dwelling Coverage | Repairs to home structure damaged by fire (walls, roof, floors, etc.) | Excludes damage due to long-term electrical deterioration or unpermitted modifications |

| Personal Property Coverage | Reimbursement for damaged belongings (furniture, electronics, clothing) | Depends on actual cash value or replacement cost basis; limits apply |

| Loss of Use (ALE) | Costs for temporary housing, meals, and other living expenses if home is uninhabitable | Subject to policy limits and duration; must be reasonably necessary |

| Other Structures | Detached structures like garages or sheds damaged by fire | Usually capped at a percentage (e.g., 10%) of dwelling coverage |

Does Home Insurance Cover Electrical Fires? A Comprehensive Guide

What common fire damages are excluded from standard home insurance policies?

Damaged Caused by Illegal Activities

Standard home insurance policies typically exclude fire damages that result from illegal activities conducted on the property. Insurers consider such actions as intentional risks that violate the terms of coverage. When a fire occurs due to unlawful behavior, the policyholder is often held responsible, and compensation is denied.

- If a fire starts in a marijuana grow operation that violates local laws, the damage may not be covered, even in regions where such use is partially legalized, especially if safety codes are breached.

- Arson committed by the homeowner or someone acting on their behalf is strictly excluded, as it constitutes fraud and intentional destruction.

- Fire damage occurring during the commission of a crime, such as drug manufacturing or possession of illegal substances, typically voids coverage under the policy.

Damage from Poor Maintenance or Negligence

Insurance companies do not cover fire damages that stem from long-term neglect or failure to maintain the property. These exclusions exist because insurers expect homeowners to take reasonable steps to prevent hazards. When fires result from avoidable conditions, claims may be denied.

- Fires caused by severely deteriorated electrical wiring that hadn't been addressed despite visible signs of wear are often deemed preventable and thus not covered.

- Accumulated combustible materials, such as piles of newspapers or stored flammable liquids in garages without proper containment, can lead to exclusions if they contribute to a fire.

- Failure to clean chimneys or furnace vents, resulting in a chimney fire due to creosote buildup, is commonly excluded due to lack of routine maintenance.

Damage from War, Nuclear Risk, or Acts of Terrorism

Standard home insurance policies universally exclude fire damages caused by large-scale events such as war, nuclear reactions, or terrorism. These risks are considered beyond the scope of typical homeowner policies and are often managed through specialized or government-backed programs.

- Fire damage resulting from military attacks or acts of war, even if occurring domestically during a conflict, is not covered under standard residential policies.

- Nuclear radiation or explosions, including accidents at nuclear facilities, are specifically excluded regardless of the distance from the site or how the fire spreads.

- Acts of terrorism that lead to fire damage are generally excluded unless the policy includes a specific rider or endorsement that extends coverage for such events.

Does homeowners insurance cover electrical fires?

Does Homeowners Insurance Typically Cover Electrical Fires?

- Yes, standard homeowners insurance policies generally cover damage caused by electrical fires, provided the fire was accidental and not due to negligence or lack of maintenance. This coverage typically falls under the dwelling protection portion of the policy, which helps pay for repairs or rebuilding of the home's structure.

- Personal property damage resulting from an electrical fire—such as furniture, electronics, and clothing—is also usually covered under the personal property component of the policy. Depending on the plan, this can include replacement or repair costs, minus the deductible.

- It’s important to note that insurance companies assess each claim individually. If an electrical fire resulted from intentional acts, known hazards left unaddressed (like outdated wiring not reported), or illegal activities, the claim may be denied.

What Types of Damages Are Included in Coverage?

- Structural damage to the home’s walls, roof, floors, and built-in appliances caused by an electrical fire is typically covered under the dwelling protection section. This includes immediate fire damage as well as smoke and soot residue cleanup.

- Additional living expenses (ALE) are often included if the home becomes uninhabitable during repairs. This may cover costs for temporary housing, meals, and other essential expenses while the policyholder is displaced.

- Damage to personal belongings such as electronics, clothing, and furniture is covered under personal property protection, either at actual cash value (depreciated value) or replacement cost value, depending on the policy terms.

What Should You Do After an Electrical Fire?

- Ensure safety first by evacuating the premises and contacting emergency services. Do not re-enter the home until it is declared safe by authorities, as structural instability and lingering electrical hazards may exist.

- Document the damage thoroughly by taking photos or videos of affected areas, appliances, wiring, and personal property. This evidence supports the insurance claim and speeds up the assessment process.

- Contact your insurance provider as soon as possible to report the incident. Be ready to provide details such as the cause of the fire, any witness statements, and supporting documentation. Follow the insurer’s instructions for inspections and claim processing.

What home damages are typically excluded from electrical fire coverage in home insurance?

Gradual Damage from Wear and Tear

Home insurance typically excludes damage resulting from long-term deterioration or lack of maintenance, even if an electrical fire is involved. Insurers consider wear and tear as preventable through routine care, so any failure due to outdated wiring, frayed cords, or aging electrical systems is generally not covered. For example, if old, deteriorated insulation around wires ignites over time due to insufficient upkeep, the resulting fire may be classified as stemming from neglect rather than an unforeseen event.

- Damage from corroded or degraded wiring not maintained over years

- Electrical malfunctions due to failing breakers that weren’t replaced despite obvious warning signs

- Fire originating from a DIY electrical installation completed poorly and not up to code

Damage from Rodent or Pest Infestation

Another common exclusion is fire damage caused by pests such as rodents that have chewed through electrical wires. While the fire itself may seem sudden and accidental, insurers often view infestations as preventable household issues tied to negligence or poor property upkeep. If gnawed wires spark a fire, the root cause is traced back to the pest problem, which many policies exclude from coverage under “maintenance-related” or “preventable hazard” clauses.

- Fire triggered by exposed wiring after mice or rats have damaged insulation in walls or attics

- Insurance denial due to lack of pest control measures despite visible infestation signs

- Damage to electrical panels caused by insects or rodents nesting near critical systems without regular inspection

Unapproved Modifications and Code Violations

Electrical work that doesn’t comply with local building codes or was performed without proper permits is typically excluded from fire coverage. Home insurance requires that electrical systems meet recognized safety standards; if a fire results from a renovated circuit installed by an unlicensed individual or one that bypasses grounding requirements, the insurer may refuse to pay for damages due to the violation of policy terms.

- Electrical fire stemming from a homeowner-built addition with unpermitted rewiring

- Damage caused by overloaded circuits due to a non-compliant solar panel or EV charger installation

- Fire originating from improper use of extension cords as permanent wiring solutions in violation of electrical codes

Does homeowners insurance cover damage from electrical fires?

Yes, homeowners insurance typically covers damage from electrical fires, but the extent of coverage depends on the specific policy and circumstances surrounding the incident.

Most standard homeowners insurance policies include dwelling coverage, which pays to repair or rebuild the home's structure if damaged by a covered peril, including fire. Electrical fires are generally considered a covered peril unless they resulted from negligence, intentional acts, or lack of maintenance.

The policy may also cover personal property damaged in the fire and additional living expenses if the home becomes uninhabitable during repairs. However, it’s essential to review your policy's declarations page and consult with your insurer to understand limitations, exclusions, and required documentation.

What Types of Electrical Fire Damage Are Covered?

- Dwelling damage: If an electrical fire damages the structure of your home—such as walls, floors, roofing, or built-in appliances—homeowners insurance typically covers repair or reconstruction costs, up to the policy limit.

- Personal property loss: Items like furniture, electronics, and clothing destroyed in an electrical fire are usually covered under the personal property portion of the policy, either at actual cash value or replacement cost, depending on your plan.

- Loss of use or additional living expenses: If the fire makes your home temporarily unlivable, insurance can pay for hotel stays, meals, and other necessary expenses until repairs are complete, within the policy's specified limits.

What Factors Can Affect Coverage for Electrical Fires?

- Cause of the fire: Insurance companies investigate the origin of the fire. If it resulted from outdated wiring, faulty appliances, or accidental overloads, coverage is likely. However, if the fire was caused by intentional acts or severe neglect (like ignoring known electrical hazards), the claim may be denied.

- Policy exclusions: Some older policies or specific insurers may exclude certain electrical issues, especially if the home has outdated systems like knob-and-tube wiring. Disclosing upgrades such as electrical panel replacements can help maintain eligibility.

- Proper maintenance and documentation: Insurers expect homeowners to maintain their properties. Regular electrical inspections, updated service panels, and records of repairs can strengthen your claim and prevent disputes over negligence.

Steps to Take After an Electrical Fire for Insurance Claims

- Ensure safety first: Evacuate the home if necessary and contact emergency services. Do not re-enter until authorities confirm it's safe, and shut off power if possible to prevent further damage.

- Notify your insurer promptly: Report the incident as soon as possible. Delayed reporting can affect claim processing. Your insurer will assign an adjuster to assess the damage and guide you through the documentation process.

- Gather evidence: Photograph the damage, keep damaged items, and collect any receipts related to repairs or temporary housing. Providing a detailed inventory of lost belongings can speed up reimbursement under personal property coverage.

Frequently Asked Questions

Does home insurance cover electrical fires?

Yes, standard homeowners insurance policies typically cover damage caused by electrical fires. This includes destruction to the structure of your home, personal belongings, and additional living expenses if you need to stay elsewhere during repairs. However, coverage depends on the cause of the fire and whether negligence or lack of maintenance contributed. Always report incidents promptly and document damages for a smoother claims process.

What types of electrical fire damage are covered by home insurance?

Home insurance usually covers structural damage, destroyed personal property, and costs for temporary housing if an electrical fire makes your home unsafe. The policy typically pays for repairs or replacements based on actual cash value or replacement cost, depending on your plan. However, damage due to poor maintenance or outdated wiring may be excluded. Review your policy details to understand specific covered perils and limitations.

Are there situations where home insurance won't cover an electrical fire?

Yes, home insurance may deny coverage if the electrical fire resulted from neglect, like ignoring faulty wiring or failing to maintain electrical systems. Insurance also won’t cover fires caused by illegal activities or DIY electrical work that violates code. If the home was vacant for an extended period, coverage might be limited. Always keep systems updated and follow safety codes to avoid claim denials.

How do I file a claim for an electrical fire with my home insurance?

To file a claim, contact your insurer as soon as it’s safe to do so. Document the damage with photos and videos, and keep records of all communication. Provide a detailed account of how the fire started and list damaged items. Your insurer may send an adjuster to assess the loss. Follow their instructions, submit required documents promptly, and keep receipts for any emergency repairs or temporary housing.

Leave a Reply