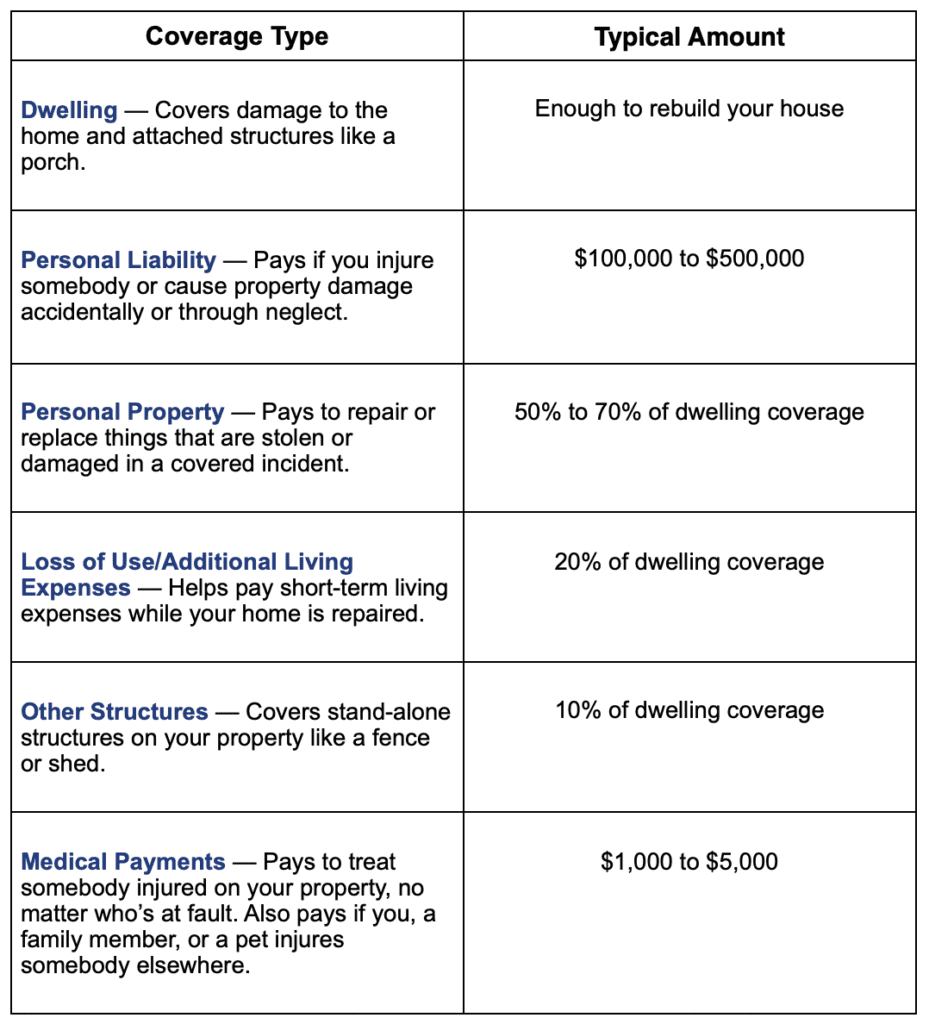

Dwelling coverage for home insurance

Dwelling coverage is a crucial component of any homeowner’s insurance policy, providing financial protection for the physical structure of a home.

It helps cover repair or rebuilding costs if the home is damaged or destroyed by covered perils such as fire, windstorms, or vandalism. This coverage typically extends to walls, roofs, floors, built-in appliances, and other structural elements.

Understanding dwelling coverage ensures homeowners choose an appropriate limit based on reconstruction costs, not market value. Factors like location, construction type, and square footage influence coverage needs. Regular policy reviews help maintain adequate protection as home values and rebuilding costs change over time.

Home insurance in fair oaks ranch

Home insurance in fair oaks ranchUnderstanding Dwelling Coverage in Home Insurance

Dwelling coverage is a fundamental component of most standard homeowners insurance policies, designed to protect the physical structure of your home from covered perils such as fire, windstorms, hail, lightning, and vandalism.

This type of coverage typically includes not only the main residence but also attached structures like garages, decks, and built-in appliances. It's important to note that dwelling coverage does not extend to land or personal belongings—those are addressed under separate parts of a policy, such as personal property coverage or land value exclusions.

Policyholders should ensure their dwelling coverage limit reflects the reconstruction cost of their home, rather than its market value, to avoid being underinsured after a loss. Accurate assessment helps prevent out-of-pocket expenses during rebuilding, especially in areas where construction costs fluctuate.

What Does Dwelling Coverage Include?

Dwelling coverage typically protects the physical framework of your home, including exterior and interior walls, the roof, foundation, windows, doors, and permanently installed systems such as plumbing, electrical, and heating.

Home insurance insurance quote

Home insurance insurance quoteIt also extends to any attached structures—like a garage or porch—that share utilities or structural components with the main house. Additionally, built-in appliances such as ovens, dishwashers, and central air conditioning units are covered under this section.

However, coverage applies only to damages caused by named perils listed in the policy, such as fire, wind, or hail, and may exclude damage from floods, earthquakes, or general wear and tear unless additional endorsements are purchased. Understanding these inclusions ensures homeowners have a clear picture of what is financially protected.

How Much Dwelling Coverage Do You Need?

The appropriate amount of dwelling coverage depends on the cost to rebuild your home from the ground up using similar materials and labor costs in your area, not its market value or purchase price.

Market value can be influenced by location and real estate trends, but insurers focus on construction costs, which can vary significantly by region and building codes. To estimate accurately, insurers often use tools like replacement cost estimators or consult with contractors.

Home insurance kernersville nc

Home insurance kernersville ncUnderestimating this amount can result in out-of-pocket expenses if repairs exceed coverage limits, while overestimating may lead to unnecessarily high premiums. It’s advisable to review your dwelling coverage annually or after major renovations to maintain adequate protection.

Common Exclusions in Dwelling Coverage

While dwelling coverage provides robust protection for many structural risks, several exclusions are standard across most policies.

Notable exclusions include flood damage, which requires a separate flood insurance policy through the National Flood Insurance Program or a private insurer, and earthquake damage, which typically requires an added endorsement. Other common exclusions involve damage from poor maintenance, mold (unless resulting from a covered peril), pests like termites, and surface water runoff.

Additionally, damage caused by neglect or intentional acts by the homeowner is not covered. Being aware of these exclusions helps homeowners make informed decisions about supplemental coverage and preventative maintenance.

| Coverage Aspect | Typically Included | Typically Excluded |

|---|---|---|

| Roof and Walls | Yes, when damaged by fire, wind, hail, or other named perils | Wear and tear, lack of maintenance |

| Attached Structures | Garages, decks, porches connected to the home | Detached structures like sheds (covered under other policy sections) |

| Plumbing & Electrical Systems | Yes, if damage results from a covered peril | Gradual leaks, aging systems without sudden incident |

| Natural Disasters | Limited to wind, lightning, and certain storms | Floods, earthquakes, sinkholes (require endorsements) |

| Personal Belongings | No | Covered under separate personal property section |

Dwelling Coverage for Home Insurance: A Comprehensive Guide

What exclusions apply to dwelling coverage in home insurance?

Flood and Water Damage Exclusions

Home insurance policies typically do not cover damage caused by flooding or general water-related incidents that originate from outside the home.

This exclusion is one of the most significant and frequently misunderstood aspects of dwelling coverage. Homeowners must understand that standard policies are not designed to protect against rising water from storms, hurricanes, overflowing rivers, or similar natural events.

To obtain protection, a separate flood insurance policy is usually required, often available through government-backed programs such as the National Flood Insurance Program (NFIP) in the United States. Additionally, backup from sewers or drains may also be excluded unless a specific endorsement is added.

- Flood damage from external sources like overflowing rivers or severe storms is not covered under standard dwelling policies.

- Water seepage through basement walls or foundation cracks due to hydrostatic pressure is typically excluded.

- Damage from sewer or drain backups is generally not included unless an additional endorsement or rider is purchased.

Earth Movement and Natural Disasters

Standard homeowners insurance does not protect against damage caused by earthquakes, landslides, sinkholes, or other earth movement-related perils. These exclusions exist because such events can cause catastrophic and widespread losses, making them high-risk for insurers.

As a result, dwelling coverage under a typical home insurance policy specifically removes protection for any structural damage caused by seismic activity or ground instability. Homeowners living in regions prone to these risks are advised to purchase separate policies or endorsements to achieve adequate protection, especially in geologically active areas.

- Earthquake damage, including structural cracks or collapse due to seismic activity, is excluded from standard policies.

- Landslide or mudflow damage that shifts or destroys part of the home’s foundation is not covered under dwelling insurance.

- Sinkhole damage, even if gradual, typically requires a separate policy or specific endorsement for coverage.

Dwelling coverage is designed to protect against sudden and accidental damage, not issues resulting from neglect, lack of maintenance, or the natural aging of building materials. Insurers consider deterioration due to poor upkeep as preventable, and therefore not insurable under standard policies.

This means that damage caused by long-term leaking roofs, rusted plumbing, rotting wood, or worn-out siding will not be covered. Homeowners are expected to maintain their properties in good condition, and claims arising from deferred maintenance are routinely denied.

- Roof damage due to long-term wear or lack of repairs is not covered, even if a storm later exacerbates the issue.

- Plumbing failures caused by aging or corroded pipes are considered maintenance issues and are excluded.

- Wood rot or mold stemming from prolonged moisture exposure due to poor home maintenance is typically not covered.

What is the ideal dwelling coverage limit for home insurance?

Understanding Dwelling Coverage in Home Insurance

- Dwelling coverage is the part of a homeowners insurance policy that pays to repair or rebuild the physical structure of your home if it’s damaged by a covered peril, such as fire, windstorms, or vandalism. It does not cover the land your home sits on, as land is not subject to damage in the same way structures are.

- The ideal dwelling coverage limit should match the full cost of rebuilding your home from the ground up, which is often different from your home’s market value. Market value includes land and local real estate trends, while rebuild cost considers labor, materials, permits, and architectural design.

- To determine the right amount, insurers typically use replacement cost estimators based on your home’s square footage, construction type, age, roof style, and location. It's essential to review these calculations carefully, as underestimating can leave you financially exposed after a loss.

Factors That Influence Your Ideal Coverage Limit

- The square footage and layout of your home significantly impact rebuilding costs. Larger homes or those with complex designs (like multi-story or custom floor plans) generally require higher coverage limits due to increased material and labor needs.

- Geographic location plays a major role, as construction costs vary widely between regions. Homes in areas with high labor rates or strict building codes (such as coastal regions or earthquake zones) may require more coverage to comply with local regulations after damage.

- Upgrades and special features, such as high-end finishes, custom cabinets, or energy-efficient materials, can substantially increase rebuilding expenses. Standard insurance calculators may not account for these details, so a professional appraisal or builder’s quote may be necessary for accuracy.

How to Ensure Your Coverage Limit Remains Accurate Over Time

- Inflation and rising construction material costs mean that the rebuild cost of your home can increase over time, even if no renovations are made. It's recommended to review your dwelling coverage annually or after major economic shifts in your area.

- After any home improvement project—such as adding a room, finishing a basement, or upgrading your roof—you should notify your insurer to adjust your coverage limit accordingly. Failure to do so may result in insufficient funds to cover full reconstruction after a claim.

- Consider opting for extended or guaranteed replacement cost coverage, which provides a buffer beyond your stated dwelling limit. This type of endorsement can cover unexpected cost overruns due to supply shortages or code upgrades, giving you greater financial protection.

What is included in basic dwelling coverage for home insurance?

Structure and Attached Components

Basic dwelling coverage in home insurance primarily protects the physical structure of your home and any components permanently attached to it. This includes critical elements such as walls, floors, roofs, and built-in appliances.

When your home suffers damage from covered perils like fire, windstorms, or vandalism, the insurance helps pay for repairs or rebuilding, up to the policy limit. It's important to understand that the coverage applies only to the structure itself and not to personal belongings inside.

- The main residential building on your property, including all rooms and interior walls

- Permanent installations such as built-in cabinets, ceiling fixtures, and plumbing systems

- Attached structures like garages, decks, and porches that are physically connected to the home

Covered Perils Under Standard Policies

Standard dwelling coverage typically protects against specific named perils or provides broader open-peril protection, depending on the policy type. These perils are events that can cause significant structural damage and are clearly outlined in the insurance contract. Common examples include fire, lightning strikes, windstorms, hail, explosions, and damage from aircraft or vehicles that unexpectedly crash into the home. Not all risks are covered—floods and earthquakes generally require separate policies or endorsements.

- Fire and smoke damage resulting from accidental ignition or electrical faults

- Wind and hail damage to roofs, windows, and exterior walls during storms

- Sudden and accidental structural damage caused by falling objects or vehicle impacts

Additional Structures and Extensions

While the primary focus of dwelling coverage is the main house, some related structures are also included under certain conditions. Detached structures such as tool sheds, freestanding garages, and storage buildings are often covered, but typically up to a percentage of the main dwelling's coverage limit, often around 10%. This extension ensures that damage to these secondary buildings is financially manageable without requiring a separate policy solely for outbuildings.

- Detached garages or workshops located on the same residential property

- Unattached storage sheds or garden structures used for personal purposes

- Boundary features like fences or driveway extensions that are not attached to the home but contribute to property function

Frequently Asked Questions

What is dwelling coverage in home insurance?

Dwelling coverage is part of a home insurance policy that helps pay to repair or rebuild the physical structure of your home if it's damaged by covered perils, such as fire, windstorms, or lightning. It typically covers walls, roof, floors, and built-in appliances. This coverage does not include the land your home sits on or personal belongings inside. Always check your policy for specific inclusions and limits.

How much dwelling coverage do I need?

You need enough dwelling coverage to fully rebuild your home at current construction costs. This amount is different from your home’s market value, as it doesn’t include land value. Insurance companies often use square footage, building materials, and local labor costs to estimate rebuild costs. Review your coverage regularly, especially after renovations or major upgrades, to ensure it still matches your home’s replacement value.

Does dwelling coverage include detached structures like garages or sheds?

No, dwelling coverage typically does not include detached structures like garages, sheds, or fences. These are usually covered under a separate part of your policy called other structures coverage, which generally offers protection up to a percentage of your dwelling coverage—often 10%. Check your policy details to confirm limits and ensure valuable detached buildings are adequately protected.

Are natural disasters covered under dwelling insurance?

Dwelling coverage includes damage from many natural disasters like windstorms, hail, and lightning. However, it typically excludes floods and earthquakes. For protection against these perils, you’ll need to purchase separate policies or endorsements. Always review your policy to understand which natural disasters are included or excluded, and consider additional coverage based on your location and risk exposure.

Leave a Reply