Guaranteed Auto Protection Insurance Market

The Guaranteed Auto Protection (GAP) insurance market has emerged as a critical component of automotive financial protection, offering consumers peace of mind in the event of vehicle total loss. As auto loan terms extend and vehicle depreciation accelerates, the gap between a car’s actual cash value and the remaining loan balance continues to widen.

GAP insurance effectively bridges this financial exposure, making it increasingly attractive to lenders and borrowers alike. Fueled by rising vehicle prices and growing consumer awareness, the market is experiencing steady growth across both developed and emerging economies.

Understanding the Guaranteed Auto Protection Insurance Market

The Guaranteed Auto Protection (GAP) Insurance Market has emerged as a critical component within the broader auto insurance landscape, offering financial security to vehicle owners in the event of a total loss.

Bundling home insurance claims service improvement

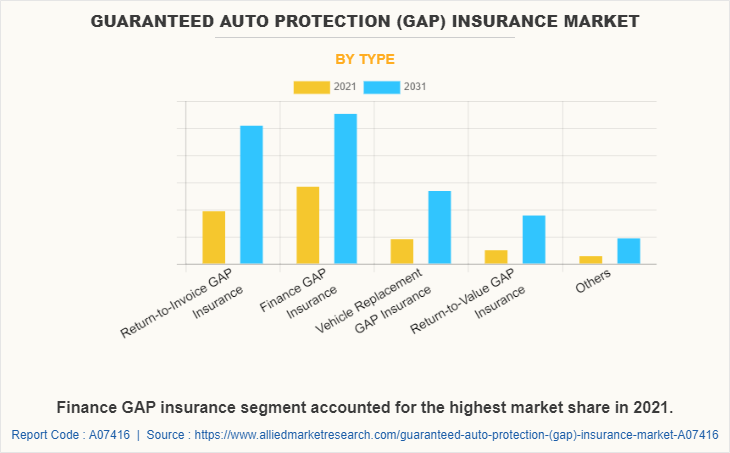

Bundling home insurance claims service improvementGAP insurance covers the difference between what a vehicle owner owes on a lease or loan and the actual cash value (ACV) paid by a primary insurance provider after an accident or theft. This type of insurance is particularly valuable for consumers purchasing new vehicles that depreciate rapidly, often leaving them upside down on their auto loans.

Over the years, the GAP insurance market has grown steadily, driven by increasing vehicle financing rates, rising car prices, and evolving consumer awareness. As more drivers rely on auto loans to purchase vehicles, the demand for protection against negative equity has intensified, making GAP insurance an essential financial safeguard for many households.

Market Drivers and Growth Trends in the GAP Insurance Industry

Several key factors are fueling the expansion of the Guaranteed Auto Protection Insurance Market, including rising automobile prices, longer loan terms, and increased consumer reliance on vehicle financing.

With the average price of new cars surpassing $45,000 and loan durations extending to 72 or even 84 months, drivers are more vulnerable to negative equity during the early years of ownership. This financial exposure creates a strong incentive to purchase GAP insurance. Moreover, the integration of GAP coverage within dealership financing packages and partnerships with major insurers and lenders has broadened its accessibility.

Buying extra protection for home insurance gaps

Buying extra protection for home insurance gapsTechnological advancements have also enabled automated underwriting and streamlined claims processing, enhancing customer experience and market efficiency. As a result, the GAP insurance market is projected to maintain robust growth, especially in regions with high auto loan penetration and economic volatility.

Key Players and Competitive Landscape

The Guaranteed Auto Protection Insurance Market is characterized by a mix of specialized insurance providers, large multi-line insurers, and financial institutions offering GAP coverage directly through their financing platforms. Major players include Allstate, Progressive, Liberty Mutual, GEICO, and dealerships affiliated with automakers such as Ford Motor Credit and GM Financial.

These companies dominate the market by leveraging strong distribution channels, brand recognition, and strategic partnerships with auto lenders and credit unions. Competition is intense, with providers differentiating through price, bundling options, and digital customer service tools.

Some insurers offer standalone GAP policies, while others integrate coverage into comprehensive protection packages, enabling greater flexibility and customization. The trend toward digital distribution and mobile-based claims management continues to reshape the competitive environment, favoring companies that invest in user-friendly platforms and real-time data integration.

Common insurance types bundled with australian home loans

Common insurance types bundled with australian home loansRegulatory Environment and Consumer Considerations

Regulations governing the Guaranteed Auto Protection Insurance Market vary by jurisdiction but generally focus on transparency, fair pricing, and consumer protection. In the United States, regulatory oversight comes primarily from state insurance departments, which require clear disclosure of policy terms, cost, and cancellation rights.

One critical aspect is the regulation of add-on sales practices at dealerships, where GAP insurance is often promoted during vehicle financing. Critics have raised concerns about aggressive selling tactics and lack of price comparison options, leading several states to implement cooling-off periods and mandatory disclosures.

Consumers are advised to compare standalone policies from insurers with those offered by lenders or dealerships, as prices and coverage terms can differ significantly. Understanding eligibility criteria, exclusions, and the claims settlement process is essential to ensure the policy delivers the intended protection.

| Factor | Description | Market Impact |

|---|---|---|

| Rising Vehicle Prices | Increased cost of new and used vehicles leads to higher loan amounts. | Boosts demand for GAP coverage as more consumers face negative equity. |

| Extended Loan Terms | Loans now commonly extend to 72–84 months, slowing equity buildup. | Increases risk of being upside down on a loan, elevating GAP relevance. |

| Digital Distribution | Insurers offer GAP policies online and through mobile apps. | Enhances accessibility and customer engagement, driving market growth. |

| Regulatory Scrutiny | States enforce transparent pricing and disclosure requirements. | Promotes fair consumer practices but may affect sales volume at dealerships. |

Comprehensive Guide to the Guaranteed Auto Protection Insurance Market

What is the market size of Guaranteed Auto Protection (GAP) insurance?

Global Market Size and Growth Trends of GAP Insurance

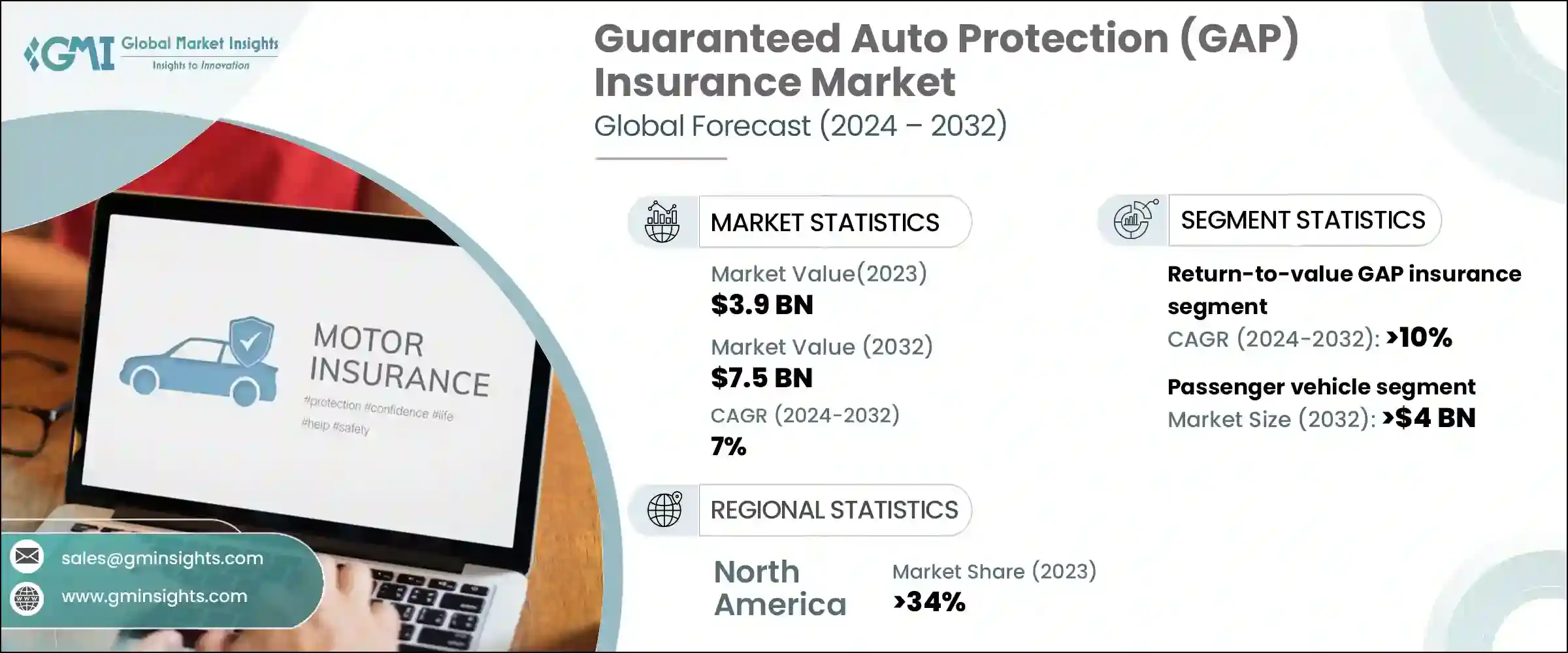

- The global Guaranteed Auto Protection (GAP) insurance market was valued at approximately USD 4.8 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of around 5.2% from 2024 to 2030. This expansion is driven by increasing auto loan financing, rising vehicle prices, and a growing number of leased vehicles, all of which heighten financial exposure in case of total loss or theft.

- North America currently dominates the market, primarily due to widespread auto financing practices and strong consumer awareness. The United States, in particular, accounts for a significant share, as lenders and leasing companies frequently offer GAP insurance as an add-on product through dealerships and financial institutions.

- Technological advancements in telematics and digital distribution platforms are further accelerating market growth. Insurers are integrating GAP coverage into bundled auto protection packages, making it more accessible to consumers through online portals and mobile applications.

Regional Market Distribution and Key Players

- North America holds the largest market share, representing over 60% of global revenue, with the U.S. serving as the primary contributor. Major insurance providers such as Allstate, Nationwide, and USAA dominate the landscape, often partnering with auto dealerships and finance companies to distribute GAP products.

- Europe follows with a growing, albeit smaller, market presence. Countries like the United Kingdom and Germany are witnessing increased adoption, particularly among lessees, due to supportive regulations and rising vehicle financing rates. However, consumer awareness remains lower compared to the U.S., presenting opportunities for education and market expansion.

- The Asia-Pacific region is experiencing gradual growth, led by emerging economies such as China and India. As vehicle ownership increases and financing becomes more common, demand for GAP insurance is expected to rise. However, limited regulatory frameworks and underdeveloped insurance cultures currently temper growth in this region.

Factors Influencing Demand for GAP Insurance

- Rising new vehicle prices have increased the gap between a car's market value and the outstanding loan or lease balance, making GAP insurance more essential. With the average price of new vehicles exceeding USD 48,000 in the U.S., depreciation can quickly outpace loan repayment, leaving consumers financially vulnerable.

- An increase in auto loan terms extending to 72 or 84 months contributes to negative equity situations early in the loan cycle. Longer financing periods mean monthly payments reduce the principal slowly, increasing the likelihood that an insured will owe more than the car is worth at the time of loss.

- Automotive lending institutions and leasing companies often encourage or require GAP coverage as part of financing agreements. Additionally, regulatory bodies in some markets are beginning to mandate clearer disclosure of GAP options, which enhances transparency and consumer uptake.

What is Toyota's Guaranteed Auto Protection (GAP) Program and How Does It Fit into the GAP Insurance Market?

Toyota's Guaranteed Auto Protection (GAP) Program is a specialized insurance option offered by Toyota Financial Services (TFS) designed to protect vehicle owners in the event of a total loss due to theft or an accident.

When a car is declared a total loss, standard auto insurance typically pays only the current market value of the vehicle, which may be substantially less than the outstanding balance on the auto loan or lease—especially in the early years when depreciation is highest.

Toyota's GAP coverage bridges this financial gap by paying the difference between the primary insurance settlement and the remaining loan or lease balance, up to a specified limit. This program is particularly beneficial for customers who finance or lease their vehicles with low down payments or long loan terms, as these factors increase the risk of being “upside down” on a loan.

What Does Toyota’s GAP Program Cover?

- Covers the difference between the insurance payout for a totaled or stolen vehicle and the unpaid balance on a Toyota lease or loan, which helps prevent out-of-pocket expenses during a claim.

- Includes additional protection for certain secondary costs, such as unrecovered lease security deposits (for leased vehicles) and up to $1,000 in deductible reimbursement in some cases, depending on the contract terms.

- Applies only to eligible Toyota and Lexus vehicles financed or leased through Toyota Financial Services, making it a brand-specific product compared to third-party GAP insurance providers.

How Does Toyota’s GAP Compare to the Broader GAP Insurance Market?

- Unlike independent or third-party GAP insurance providers, Toyota’s program is integrated directly into the financing agreement through Toyota Financial Services, offering seamless administration and claims handling.

- While many aftermarket GAP policies are transferable between vehicles or available for non-Toyota brands, Toyota’s GAP is non-transferable and limited exclusively to Toyota and Lexus models, reducing flexibility for some consumers.

- Pricing for Toyota’s GAP is typically bundled into the vehicle’s financing, which may result in slightly higher interest charges over time, whereas other insurers often offer GAP as a one-time, upfront purchase, potentially providing cost savings in the long term.

When Should a Consumer Consider Toyota’s GAP Protection?

- When making a low down payment (less than 20%) on a new Toyota, as vehicles depreciate rapidly in the first few years, increasing the likelihood of an upside-down loan in case of a total loss.

- When leasing a vehicle, since leasing agreements inherently involve lower equity buildup, and Toyota’s GAP for leases includes repayment of lease termination fees and security deposits under qualifying conditions.

- When driving high-depreciation models or planning to sell or trade the vehicle within a few years, as these scenarios elevate the risk of loan imbalance that GAP coverage is designed to mitigate.

What is guaranteed value car insurance in the context of the Guaranteed Auto Protection Insurance market?

What Is Guaranteed Value Car Insurance?

- Guaranteed value car insurance, often associated with Guaranteed Asset Protection (GAP) insurance, refers to a type of coverage that ensures a vehicle's financial value in the event of a total loss, such as theft or accident. Unlike standard auto insurance, which pays only the current market value of the vehicle, guaranteed value policies bridge the gap between what the vehicle is worth and what the owner still owes on a loan or lease.

- This type of policy is particularly beneficial for drivers who have financed or leased vehicles with high depreciation rates. New cars can lose 20% to 30% of their value within the first year, which means that traditional insurance payouts may not cover the full balance of an auto loan if the car is totaled.

- Guaranteed value coverage is not standalone insurance but an add-on product that works in conjunction with comprehensive and collision coverage. It is commonly purchased at the time of vehicle financing through dealerships, lenders, or insurance providers and serves as a financial safety net during the early years of vehicle ownership when depreciation outpaces loan repayment.

How Does Guaranteed Auto Protection (GAP) Insurance Work?

- GAP insurance is a key component of the Guaranteed Auto Protection Insurance market and directly supports the concept of guaranteed value. When a vehicle is declared a total loss, the primary auto insurer calculates its actual cash value (ACV), which often falls short of the remaining loan or lease balance due to depreciation.

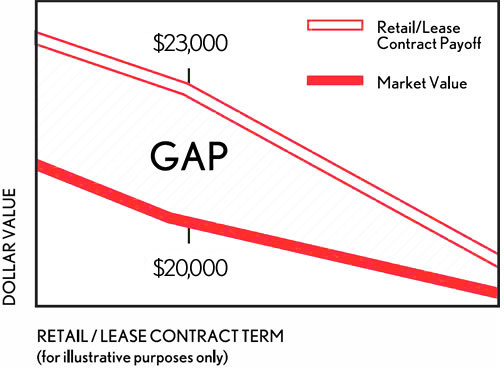

- The GAP policy then steps in to cover the difference between the ACV payout and the outstanding debt on the vehicle. For example, if a car is worth $20,000 at the time of loss but the owner owes $24,000 on the loan, GAP insurance would cover the $4,000 shortfall, preventing the owner from having to pay it out of pocket.

- Some GAP policies also cover the deductible from the primary insurance claim, further reducing financial burden. This protection typically lasts for a set term, often three to five years, aligning with the high-depreciation phase of a vehicle’s life cycle and the most vulnerable period for being upside-down on a loan.

Who Should Consider Guaranteed Value Coverage?

- Individuals who make low down payments—typically less than 20%—are at higher risk of being underwater on their auto loans and should strongly consider guaranteed value coverage. Since they start with little to no equity, even minor depreciation can result in a significant negative balance after a loss.

- Borrowers with long loan terms, such as 60 to 84 months, often experience extended periods where the car's value drops faster than the loan balance is paid down. These buyers benefit from guaranteed value insurance because it protects them over a longer financial exposure period.

- Lessees of new vehicles also gain substantial value from this coverage. Leasing agreements often include GAP insurance by default or as an optional extra, ensuring that if the vehicle is totaled, the lessee isn't responsible for the remaining payments or depreciation penalties outlined in the lease contract.

Frequently Asked Questions

What is Guaranteed Auto Protection (GAP) Insurance?

Guaranteed Auto Protection (GAP) insurance is a specialized auto insurance policy that covers the difference between a vehicle’s actual cash value and the outstanding balance on a loan or lease if the car is totaled or stolen.

It helps prevent out-of-pocket expenses for consumers. GAP insurance is especially beneficial for those who owe more on their vehicle than it's worth, commonly occurring with new cars that depreciate rapidly.

Who Should Consider Purchasing GAP Insurance?

Individuals who lease vehicles or finance a car with a low down payment, long loan term, or who drive high-mileage should consider GAP insurance. It’s also ideal for buyers of vehicles with rapid depreciation rates, like many new cars.

Since standard auto insurance only pays actual cash value, which may be significantly less than the loan balance after an accident, GAP insurance offers valuable financial protection for those at risk of owing more than their car’s worth.

How Does GAP Insurance Work in the Event of a Total Loss?

In the event of a total loss due to theft or accident, standard auto insurance pays the vehicle’s actual cash value. If this amount is less than the remaining loan or lease balance, GAP insurance covers the difference.

The policyholder must file a claim, and once processed, the GAP insurer pays the lender directly. This prevents the consumer from being responsible for continued payments on a vehicle they no longer have, offering crucial financial relief during a difficult time.

Is GAP Insurance Worth the Cost?

GAP insurance is often worth the cost for drivers who finance or lease vehicles with little equity. Premiums are typically low, and the coverage can save thousands in case of a total loss.

It’s especially valuable during the first few years of ownership when depreciation is highest. While not necessary for everyone, those with long loan terms, low down payments, or vehicles that lose value quickly can benefit significantly from the added protection GAP insurance provides.

Leave a Reply