Common insurance types bundled with australian home loans

Many Australian home loan borrowers opt to bundle insurance products with their mortgages to enhance financial protection and streamline payments.

Commonly included policies are life insurance, total and permanent disability (TPD) cover, and income protection insurance. Some lenders also offer home and building insurance as part of the package.

Bundling can provide convenience and potential cost savings, but it's essential to assess whether the coverage meets individual needs. Not all bundled policies offer the same level of protection, and exclusions may apply. Borrowers should carefully review terms, compare standalone options, and consider professional advice before committing.

Home insurance companies columbus

Home insurance companies columbusCommon Insurance Types Bundled with Australian Home Loans

When securing a home loan in Australia, lenders often offer or require borrowers to take out certain types of insurance to protect both the lender's and borrower’s interests.

These insurance products are frequently bundled with the mortgage to provide convenience and potentially lower costs. The most common types include lenders mortgage insurance (LMI), building insurance (home insurance), and income protection insurance.

While some of these insurances are optional, others—like building insurance—are typically mandatory under loan agreements. Bundling helps streamline payments and may offer package discounts, but borrowers should carefully assess the coverage and cost to avoid paying for unnecessary features or duplicates of existing policies.

Lenders Mortgage Insurance (LMI)

Lenders Mortgage Insurance (LMI) is a common insurance product associated with Australian home loans, particularly for borrowers who make a deposit of less than 20% of the property’s purchase price. It protects the lender, not the borrower, in the event the borrower defaults on their loan repayments.

Home insurance document management solutions

Home insurance document management solutionsWhile LMI can allow borrowers to enter the property market sooner with a smaller deposit, the cost can be substantial—often amounting to thousands of dollars—and is typically added to the loan balance. It’s important to note that LMI is a one-time cost and does not cover the borrower's financial hardship, unemployment, or death, which are addressed by other insurance types.

| Insurance Type | Cost Responsibility | Protects | Typically Mandatory? |

|---|---|---|---|

| Lenders Mortgage Insurance (LMI) | Borrower (via loan or upfront) | Lender against borrower default | Yes, if deposit <20% |

Building and Home Insurance

Building insurance, often referred to as home insurance, is usually mandatory when obtaining a home loan in Australia. This coverage protects the physical structure of the property against damage from events such as fire, storms, and vandalism.

Lenders require borrowers to maintain building insurance to safeguard the asset that secures the mortgage. While lenders may offer bundled home insurance through affiliated providers, borrowers are free to choose their own policy as long as it meets the lender’s minimum requirements. It’s essential to understand the level of coverage—whether it's sum insured or indemnity value—to ensure the property can be adequately rebuilt or repaired if damaged.

| Insurance Type | Covers | Loan Requirement | Can You Choose Provider? |

|---|---|---|---|

| Building/Home Insurance | Permanent structure (walls, roof, etc.) | Yes, typically required | Yes, with conditions |

Income Protection and Life Insurance

Although not usually compulsory, income protection and life insurance are frequently promoted by lenders as part of a home loan package. Income protection insurance replaces a portion of your income—typically up to 75%—if you’re unable to work due to illness or injury, helping you continue making loan repayments.

Home insurance flood cover

Home insurance flood coverLife insurance, on the other hand, pays out a lump sum upon the policyholder's death, which can be used to settle the outstanding mortgage balance. These insurances are optional but can offer significant financial security for borrowers and their families. Bundled policies may offer convenience and potential premium discounts; however, standalone policies from specialist insurers may provide better coverage or value.

| Insurance Type | Financial Benefit | Policy Duration | Bundling Advantage |

|---|---|---|---|

| Income Protection | Replaces income during disability | Up to retirement age | Potential cost savings, simplified billing |

| Life Insurance | Lump sum to cover mortgage or family needs | Fixed term or lifelong | Ease of application through lender |

Common Insurance Types Bundled with Australian Home Loans

What insurance types are commonly included with home loans in Australia?

Home Loan Insurance: Key Types Commonly Included in Australia

When securing a home loan in Australia, lenders often recommend or require certain types of insurance to protect both the borrower and the financial institution. The most commonly included or recommended insurance types are lender's mortgage insurance (LMI), building insurance (also known as home and contents insurance), and income protection insurance.

While not all of these are automatically bundled with the loan, they are frequently discussed during the loan application process to mitigate financial risks associated with homeownership and loan repayment. LMI, for instance, is typically required when a borrower has a deposit of less than 20% of the property’s value, while building insurance is often mandated as a condition of the loan to safeguard the property securing the mortgage.

Home insurance gilbert

Home insurance gilbert- Lender's Mortgage Insurance (LMI) protects the lender if the borrower defaults on the loan and the sale of the property does not cover the outstanding debt.

- Building insurance covers damage to the structure of the home due to events like fire, storms, or vandalism and is usually required by lenders.

- Income protection insurance helps cover loan repayments if the borrower loses income due to illness, injury, or unemployment, although it is typically optional.

Understanding Lender's Mortgage Insurance (LMI) in the Australian Market

Lender's Mortgage Insurance is a common feature of home loans in Australia, particularly for first-time homebuyers who may not have saved a 20% deposit. Despite its name, LMI does not protect the borrower; instead, it protects the lender in the event the borrower defaults and the property sale proceeds are insufficient to repay the loan.

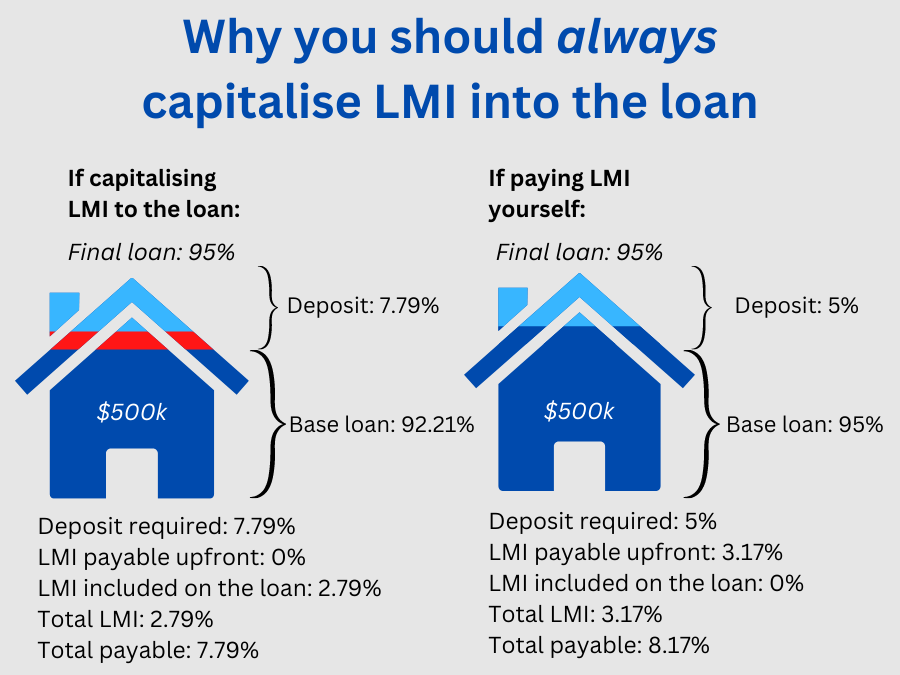

The premium for LMI can be significant and is often capitalized into the loan amount, increasing the total amount borrowed. It is important to note that LMI is a one-time cost and does not need to be renewed, and while it adds to the loan cost, it enables many Australians to enter the property market earlier than they otherwise could.

- LMI is generally required when the loan-to-value ratio (LVR) exceeds 80%, meaning the deposit is less than 20% of the property’s purchase price.

- The cost of LMI varies based on the loan amount, deposit size, and the lender’s policies, and can range from a few thousand to tens of thousands of dollars.

- Borrowers can compare LMI costs across lenders or use mortgage insurers like Genworth or QBE to estimate premiums before finalizing a loan.

Property and Income Protection: Additional Insurances Linked to Home Loans

Beyond LMI, lenders in Australia often encourage or require borrowers to obtain building insurance and may offer bundled packages that include life insurance, trauma insurance, and income protection. Building insurance is nearly always a condition of the loan, ensuring the physical asset (the home) is protected against structural damage.

Meanwhile, income protection and life insurance are optional but frequently promoted through bank-affiliated financial advisers. These policies help safeguard the borrower’s ability to meet repayment obligations during periods of financial stress, thereby reducing the risk of default from the lender’s perspective.

Home insurance guaranteed replacement cost coverage 2025

Home insurance guaranteed replacement cost coverage 2025- Building insurance must cover the full replacement value of the home and is typically reviewed annually to ensure adequate coverage.

- Life insurance pays out a lump sum upon the borrower’s death, which can be used to settle the outstanding loan balance, relieving financial pressure on family members.

- Income protection insurance replaces up to 75% of the borrower’s income if they are unable to work due to illness or injury, ensuring ongoing loan repayments are met.

What types of mortgage insurance are commonly included in Australian home loans?

What Is Lenders Mortgage Insurance (LMI) and How Does It Work?

- Lenders Mortgage Insurance (LMI) is a type of insurance commonly required by lenders in Australia when a homebuyer borrows more than 80% of a property’s value, meaning they have a deposit of less than 20%. Its primary purpose is to protect the lender, not the borrower, in the event the borrower defaults on the loan.

- The cost of LMI is typically paid by the borrower either as a one-time premium at the beginning of the loan or capitalized into the loan amount, increasing the total repayment amount over time. Premiums vary based on the loan-to-value ratio (LVR), the size of the loan, and the lender’s policies.

- While LMI increases upfront borrowing costs, it enables many Australians to enter the property market earlier, even with smaller deposits. However, borrowers should carefully evaluate whether the benefits of entering the market sooner outweigh the added expense of LMI.

What Is Mortgage Protection Insurance and What Does It Cover?

- Mortgage Protection Insurance, sometimes referred to as mortgage repayment insurance, is designed to help borrowers meet their loan repayments if they are unable to work due to illness, injury, unemployment, or death. Unlike LMI, this insurance protects the borrower and their family, not the lender.

- This type of coverage can be structured as a standalone policy or bundled with life or income protection insurance. It typically provides monthly benefits for a specified period, helping to prevent loan default during times of financial hardship.

- Borrowers should consider their personal circumstances when deciding whether to purchase Mortgage Protection Insurance, as premiums depend on factors such as age, occupation, health, and the level of cover selected.

- Yes, in addition to LMI and mortgage protection, other insurance types often associated with home loans include building insurance (commonly required by lenders to protect the property against damage) and, in some cases, income protection insurance, which replaces a portion of lost income.

- Some lenders may also recommend or bundle combined products like loan protection plans that integrate cover for death, disability, and involuntary unemployment. These can be useful but should be compared thoroughly with standalone policies for value and coverage.

- It’s important to note that none of these insurance products are usually mandatory by law (except for building insurance on the lender’s collateral), but lenders may make them conditions of loan approval to mitigate their risk exposure.

What distinguishes PMI from LMI in Australian home loans with bundled insurance?

Definition and Purpose of PMI and LMI

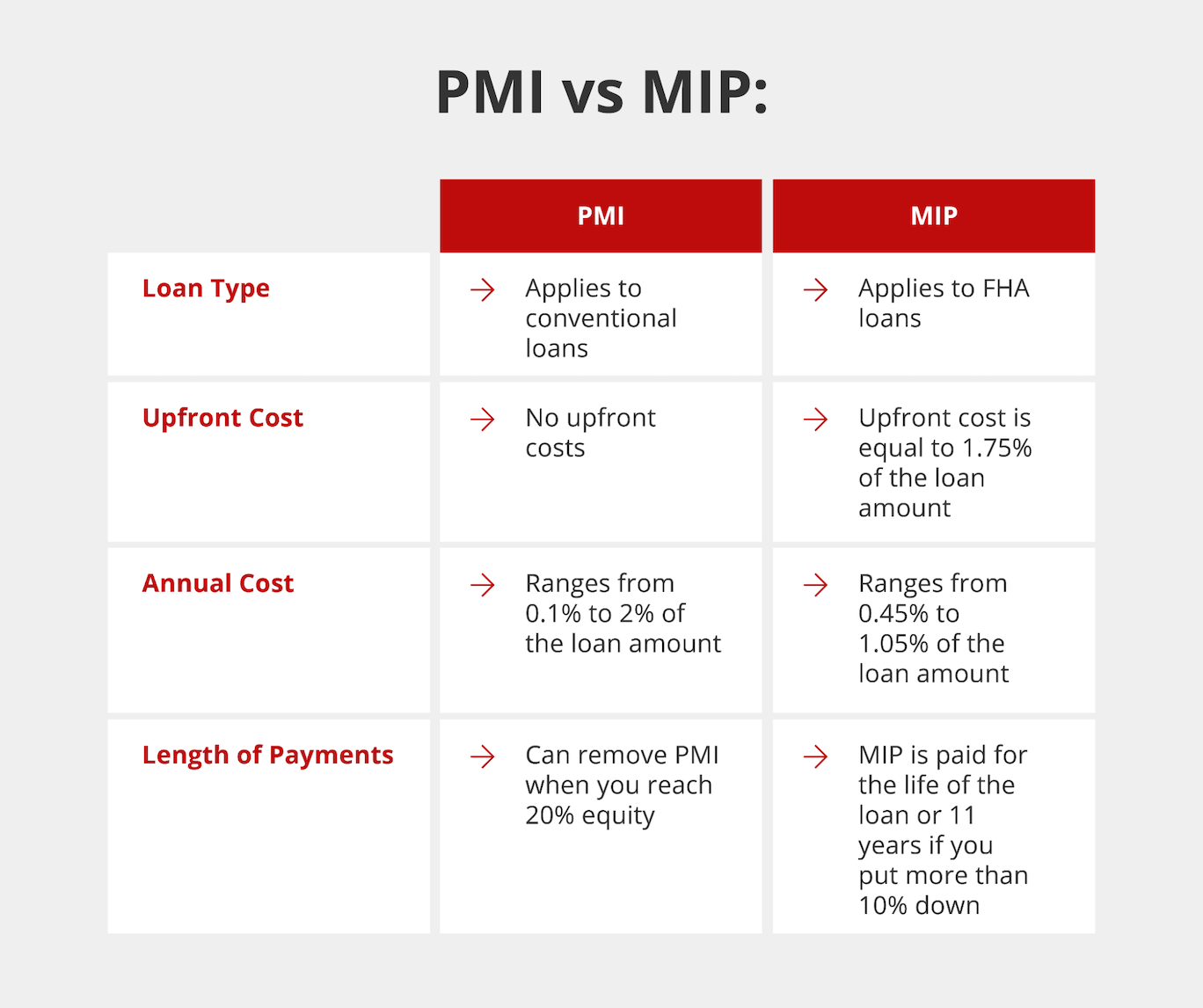

- Private Mortgage Insurance (PMI) is a term commonly used in the United States and is not typically applied in the Australian context. It refers to insurance that protects lenders when borrowers make a down payment of less than 20% on a home. In Australia, the equivalent protection for lenders is provided by Lenders Mortgage Insurance (LMI), not PMI.

- Lenders Mortgage Insurance (LMI) is a type of insurance used in Australia to protect the lender when a borrower takes out a home loan with a Loan-to-Value Ratio (LVR) exceeding 80%. This means if the borrower defaults and the property sale does not cover the loan balance, LMI compensates the lender for the shortfall.

- Although PMI and LMI serve a similar purpose—reducing lender risk for high-ratio loans—PMI is not a standard or recognized product in the Australian mortgage market. Therefore, when discussing bundled insurance in Australian home loans, LMI is the relevant financial product.

Differences in Cost and Payment Responsibility

- In systems where PMI is used, such as in the U.S., borrowers pay a monthly premium, and under certain conditions, the insurance can be canceled once sufficient equity is achieved. In contrast, in Australia, LMI is usually paid as a one-time, upfront premium by the borrower, although it can be capitalized into the loan amount and paid off over time through interest.

- The cost of LMI in Australia depends on factors such as the size of the deposit, the loan amount, and the borrower’s profession (with discounts sometimes available for doctors, lawyers, and other low-risk occupations). There is no recurring monthly cost like with typical PMI, and the payment does not automatically get removed—it is a single charge regardless of future equity levels.

- Borrowers in Australia are responsible for paying LMI even though it benefits the lender, which is similar to how PMI functions in the U.S. However, unlike PMI where borrowers can request cancellation, LMI in Australia is non-refundable and non-cancellable once paid, making it a permanent cost of the loan.

Impact on Borrowers and Loan Structures

- For Australian borrowers, LMI enables access to homeownership with a deposit as low as 5%, removing the need to save for a 20% down payment. This makes it a key component of many bundled home loan packages offered by banks and mortgage brokers, especially to first-time buyers.

- Because LMI is tied to the loan and not the property or borrower’s changing financial status, it does not provide direct benefits like reduced interest rates or insurance payouts to the borrower. This differs from other bundled insurances such as income protection or life insurance, which protect the borrower and are sometimes integrated into loan packages.

- When comparing loan structures, borrowers should understand that LMI increases the total loan cost and initial debt level, especially if the premium is capitalized. Although it facilitates loan approval, it does not reduce the borrower’s liability in case of default—it only protects the lender, not the borrower.

Frequently Asked Questions

What types of insurance are commonly bundled with Australian home loans?

Lenders in Australia often bundle home loan insurance products such as building insurance, lender's mortgage insurance (LMI), income protection, and life insurance. Building insurance covers structural damage to the property. LMI protects the lender if the borrower defaults. Income and life insurance safeguard repayments in case of illness, injury, or death. Bundling can offer convenience and sometimes discounts, but borrowers should compare standalone policies for better value.

Is building insurance mandatory when taking out a home loan in Australia?

Yes, building insurance is typically mandatory when securing a home loan in Australia. Lenders require it to protect their investment in the property against damage from fire, storms, or other disasters. While the borrower pays for the policy, it covers the structure of the home—not contents. Borrowers can choose their provider or accept a lender-recommended option, but they must maintain coverage for the loan’s duration.

What is lender's mortgage insurance (LMI) and when is it required?

Lender's mortgage insurance (LMI) protects the lender, not the borrower, if loan repayments are not met. It's typically required when the deposit is less than 20% of the property’s value. Although it benefits the lender, the borrower pays the premium, which can be added to the loan. LMI enables Australians with smaller deposits to enter the property market but adds to the overall borrowing cost.

Can I save money by bundling insurance with my home loan?

Bundling insurance with a home loan may offer convenience and occasional discounts, but it doesn’t always save money. Lender-packaged insurance can be more expensive or less comprehensive than standalone policies. It’s essential to compare coverage, premiums, and exclusions. Customers should assess their individual needs and shop around to ensure they’re getting competitive rates and adequate protection, rather than assuming bundled options are the best value.

Leave a Reply