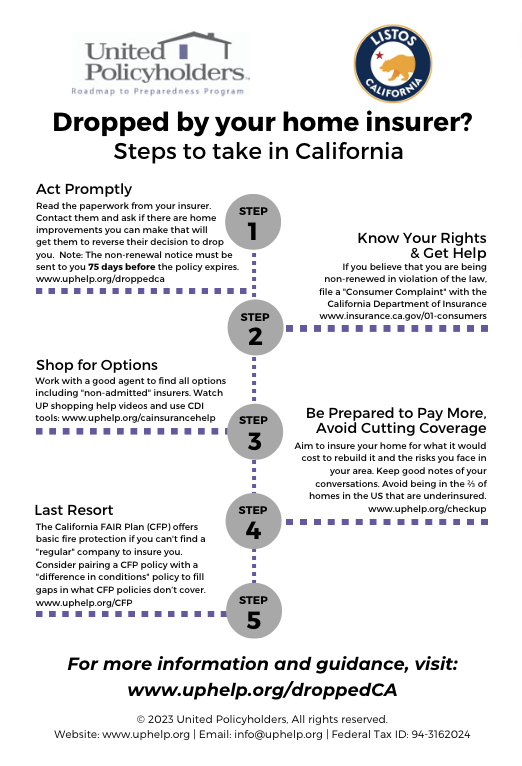

Buying extra protection for home insurance gaps

Many standard home insurance policies leave homeowners exposed to unexpected risks not fully covered under basic plans.

From natural disasters to liability concerns, coverage gaps can result in significant out-of-pocket expenses. As property values rise and extreme weather events become more frequent, understanding these vulnerabilities is crucial. Buying extra protection—through endorsements, riders, or separate policies—can bridge these gaps, offering peace of mind and financial security.

Flood insurance, earthquake coverage, and increased liability limits are just a few options worth considering. Assessing your home’s unique risks and consulting with insurance professionals helps determine which supplemental protections are worthwhile investments for long-term safety and stability.

Home insurance companies columbus

Home insurance companies columbusFilling the Gaps: How to Buy Extra Protection for Your Home Insurance

Home insurance is essential for protecting your property and belongings, but standard policies often come with limitations and exclusions that leave homeowners vulnerable to uncovered losses. These uncovered risks—commonly referred to as gaps in coverage—increase the importance of purchasing additional protection beyond basic policies.

While a typical home insurance plan may cover perils like fire, windstorms, or theft, it often excludes events such as floods, earthquakes, sewer backups, or high-value items like fine art and jewelry. To address these shortcomings, insurers offer optional endorsements, riders, or standalone policies that extend coverage where it's needed most.

Identifying the gaps in your current policy by reviewing your policy documents, assessing your property's location and risk factors, and consulting with an insurance professional allows you to make informed decisions about supplemental protection. By investing in tailored coverage, homeowners can significantly reduce financial risk and gain peace of mind knowing their home and assets are thoroughly protected.

Identifying Common Gaps in Standard Home Insurance Policies

Standard home insurance policies typically cover a broad range of perils, but numerous risks are explicitly excluded, leaving policyholders unaware until a claim arises.

Home insurance document management solutions

Home insurance document management solutionsFrequent gaps include damage from floods, earthquakes, landslides, and sewer or sump pump backups, all of which require separate policies or endorsements. Additionally, personal property coverage may have sub-limits on high-value items such as jewelry, electronics, or collectibles, meaning reimbursement might fall short of replacement costs.

Identity theft protection, home business equipment, and damage from pests like termites are also generally not included. Furthermore, if you live in a high-risk area—such as near a river or in an earthquake-prone zone—these exclusions can have costly consequences. Understanding what your policy does not cover is the first step toward building comprehensive protection by adding the right supplemental coverage.

Types of Additional Coverage to Address Home Insurance Gaps

To close the vulnerabilities left by standard insurance, several types of extra protection are available. Flood insurance, typically provided through the National Flood Insurance Program (NFIP) or private insurers, protects against water damage from overflowing rivers, heavy rains, or storm surges—events not covered under traditional policies.

Earthquake insurance provides financial relief for damages caused by seismic activity, a critical endorsement in tectonically active regions. Scheduled personal property endorsements allow you to itemize and insure high-value possessions at appraised values, ensuring full replacement if they are lost or stolen.

Home insurance flood cover

Home insurance flood coverWater backup and sump overflow coverage safeguards against indoor flooding from plumbing failures. Other valuable add-ons include equipment breakdown coverage for HVAC systems and appliances, and umbrella liability insurance to extend personal liability protection beyond home and auto policies. Choosing the right supplements depends on geographical risks, home value, and lifestyle needs.

How to Evaluate and Purchase Supplemental Home Insurance

Evaluating and purchasing extra home insurance protection starts with a thorough policy review and risk assessment. Begin by reading your current policy’s declarations page and exclusions section to pinpoint coverage shortfalls. Next, consider your geographic location—do you live in a flood zone or near fault lines? Assess the value of your belongings, especially expensive items like jewelry or electronics, and determine if standard limits are sufficient.

Consulting with a licensed insurance agent or broker can provide valuable insight into available options and help you prioritize cost-effective endorsements. Compare quotes from multiple insurers for standalone policies like flood or earthquake coverage, and pay attention to deductibles, which are often percentage-based for catastrophe-related policies.

Timing also matters—some coverages, such as flood insurance, have waiting periods before becoming active. Making informed, proactive choices ensures your supplemental protection aligns with your unique risk profile.

Home insurance gilbert

Home insurance gilbert| Insurance Gap | Solution | Key Benefits |

|---|---|---|

| Flood damage | Flood insurance (NFIP or private) | Covers structural and content damage from overflowing water; essential for homes in high-risk areas |

| Earthquake damage | Earthquake insurance endorsement | Pays for repairs due to seismic events, including foundation cracks and structural collapse |

| High-value personal items | Scheduled personal property rider | Provides full replacement value for items like jewelry, artwork, or heirlooms that exceed standard limits |

| Sewer or sump backup | Water backup coverage | Covers cleanup, repairs, and replacement for damage caused by plumbing backups |

| Extended liability risk | Umbrella liability policy | Increases personal liability coverage across home and auto policies, protecting assets from lawsuits |

How to Buy Extra Protection for Home Insurance Coverage Gaps

What are the risks of a home insurance coverage gap and how can supplemental protection help?

What Happens During a Home Insurance Coverage Gap?

- When a home insurance coverage gap occurs, it means there is a period when your property is not protected by a standard homeowner’s policy, which can happen during transitions like switching insurers, policy cancellation due to non-payment, or after selling and buying a new home without continuous coverage.

- During this vulnerable window, any damage caused by covered perils—such as fire, theft, or windstorms—is typically not reimbursed, leaving the homeowner responsible for all repair or replacement costs out of pocket.

- Additionally, mortgage lenders often require active home insurance, so a coverage lapse can trigger a default condition on your loan, potentially leading to penalties or the lender forcing (and charging you for) a more expensive insurance policy.

Common Risks Associated with Coverage Gaps

- One of the most significant risks is financial exposure: if a disaster like a fire or burst pipe happens while you're uninsured, you’ll have to cover every expense, which could amount to tens or even hundreds of thousands of dollars depending on the damage.

- Another risk involves diminished insurability; insurers may view a history of coverage gaps as a sign of higher risk, which can result in higher premiums or even denial of future coverage.

- Legal liabilities are also a concern—without liability protection, you could be personally sued if a guest is injured on your property during the gap, and you would lack the legal defense and settlement support that insurance normally provides.

How Supplemental Protection Can Help Fill the Gap

- Supplemental protection policies, such as extended reporting endorsements (also known as “tail coverage”) or stand-alone liability insurance, can provide temporary coverage during transitions and help bridge short-term lapses that standard policies don’t cover.

- Products like umbrella insurance increase liability limits and can remain effective across policy changes, offering continuous protection for lawsuits or third-party injury claims even if your primary home policy lapses momentarily.

- Some insurers offer interim or gap-specific insurance designed for homeowners in transition—for example, during renovations or between property purchases—providing targeted protection for perils like theft, water damage, or vandalism when standard policies may be inactive.

Is additional protection for home insurance gaps, like extended coverage or warranties, a worthwhile investment?

:max_bytes(150000):strip_icc()/dotdash-home-warranty-vs-home-insurance-5081270-Final-b2fa2539ff3c475296bae8529873651f.jpg)

Understanding Home Insurance Gaps and Where Coverage Falls Short

- Standard home insurance policies typically cover common risks such as fire, theft, and wind damage, but they often exclude a range of perils that can still cause significant financial loss. For example, floods, earthquakes, and sewer backups are commonly excluded and require separate policies or endorsements.

- Other gaps may emerge from underestimating the replacement cost of your home or high-value personal property, such as jewelry or artwork. Without scheduled personal property endorsements, your insurer may only reimburse you up to a small limit for such items, even if they are damaged or stolen.

- Depreciation of building materials and labor costs over time may also create a gap between your policy’s dwelling coverage and the actual cost to rebuild. These discrepancies underscore the importance of regularly reviewing your policy and understanding the limitations in your existing coverage.

Assessing the Value of Extended Coverage and Home Warranties

- Extended coverage endorsements, such as those for ordinance or law, service line protection, or equipment breakdown, can fill critical gaps in standard policies. These protections may be particularly valuable if you live in an older home or an area prone to specific risks like power surges or underground utility failures.

- Home warranties, although not insurance, provide service agreements for repairing or replacing major systems and appliances like HVAC units, plumbing, and electrical systems due to normal wear and tear. This complements insurance by addressing risks that insurers typically exclude.

- The value of these add-ons depends on your home’s age, location, and condition. For newer homes with modern systems, a warranty may seem unnecessary, but for older properties, especially those without recent upgrades, the repair and replacement costs covered by a warranty can justify the annual fee.

Factors That Determine Whether Additional Protection Is Worth the Cost

- Geographic location plays a major role—homeowners in regions susceptible to natural disasters may benefit more from flood or earthquake insurance than those in low-risk areas. Similarly, homes in cold climates may need water backup or sump pump overflow coverage due to frequent ice blockages.

- Your financial risk tolerance also influences whether additional protection is worthwhile. If paying out-of-pocket for a major appliance failure or system repair would strain your budget, then extended coverage provides a valuable financial buffer.

- Finally, consider the age and quality of your home’s systems and structure. Older roofs, plumbing, and electrical systems are more likely to fail, making extended coverage or warranties a prudent investment. Analyzing the premium cost against the potential repair bills helps determine if the long-term benefits outweigh the ongoing expense.

When is gap insurance unnecessary for home coverage?

When the mortgage balance is equal to or less than the home's market value

- If the amount owed on the mortgage is the same as or lower than the current market value of the home, gap insurance is not necessary because the insurance payout from a standard homeowner's policy would cover the mortgage in the event of a total loss.

- Over time, as homeowners make payments and reduce their principal, the loan balance decreases. In many cases, especially later in the mortgage term, the home’s appraised value may exceed the remaining loan amount, eliminating the financial gap.

- Additionally, if the housing market in the area is stable or appreciating, the home is less likely to lose value rapidly, making it improbable that a shortfall would occur between coverage and mortgage balance.

When comprehensive homeowner's insurance provides adequate coverage

- Standard homeowner's insurance policies typically cover the cost to rebuild or repair a home up to the policy limit following a covered loss, such as fire or storm damage. If this limit is set at the full replacement cost of the home, there's no need for gap insurance.

- Homeowners who regularly update their policy to reflect current construction costs and renovations ensure that their coverage remains sufficient to cover reconstruction expenses without a shortfall.

- Insurers often include extended replacement cost or guaranteed replacement cost endorsements, which can cover costs above the policy limit in extreme cases, further reducing or eliminating the risk that gap insurance is designed to address.

When the homeowner has significant equity in the property

- Homeowners who have paid off a large portion of their mortgage—or purchased the home with a substantial down payment—typically have significant equity, meaning the home’s value far exceeds the outstanding loan.

- In such cases, even if the home is totaled and the insurance payout goes toward the mortgage, the proceeds are more than enough to settle the debt, making additional gap protection redundant.

- Equity acts as a financial buffer, ensuring that fluctuations in market value or minor underinsurance do not result in a deficiency. This built-in margin makes gap insurance an unnecessary expense for well-established homeowners.

Frequently Asked Questions

What does extra protection for home insurance gaps cover?

Extra protection covers risks not included in standard home insurance, such as floods, earthquakes, sewer backups, or valuable item losses. It helps fill coverage gaps that could leave you financially exposed. This protection is often added via endorsements or separate policies, depending on the risk. Assess your home’s location and valuables to determine what extra coverage you may need for comprehensive protection.

Home insurance guaranteed replacement cost coverage 2025

Home insurance guaranteed replacement cost coverage 2025How do I know if I need additional home insurance protection?

You may need extra protection if you live in a high-risk area—like flood zones or earthquake-prone regions—or own expensive items like jewelry or art. Review your current policy to identify uncovered risks. Also, consider past claims or local weather patterns. Consulting with your insurance agent can help determine which endorsements or standalone policies offer appropriate gap coverage for your specific needs.

Can I add extra protection to my existing home insurance policy?

Yes, you can typically add extra protection through endorsements or riders to your current home insurance policy. Common additions cover floods, earthquakes, or increased coverage for valuables. However, some perils may require separate policies. Contact your insurer to discuss available options, costs, and coverage limits. Adding endorsements is often simple and enhances protection without replacing your entire policy.

How much does extra home insurance protection cost?

Costs vary based on location, coverage type, home value, and risk level. For example, flood insurance may cost a few hundred dollars annually, while earthquake coverage could be higher in seismic zones. Enhancing personal property coverage for valuables usually has lower premiums. Get quotes from your insurer for specific add-ons. While extra protection increases premiums, it can save significant money if a gap-covered loss occurs.

Leave a Reply