Health Insurance For Foreigners In Malaysia

Navigating the healthcare system in a foreign country can be challenging, and for expatriates living in Malaysia, securing reliable health insurance is a crucial step toward ensuring peace of mind.

Malaysia offers high-quality medical services at relatively affordable costs, making it an attractive destination for foreigners. However, without proper coverage, medical expenses can quickly become overwhelming. Health insurance for foreigners in Malaysia varies widely in terms of coverage, cost, and provider options.

Understanding local regulations, eligibility criteria, and the differences between public and private healthcare access is essential. This article explores the available options, key considerations, and practical tips for expats seeking comprehensive health insurance in Malaysia.

Common Complaints In Auto Insurance Reviews

Common Complaints In Auto Insurance ReviewsUnderstanding Health Insurance Options for Foreigners in Malaysia

Malaysia has become an increasingly popular destination for expatriates, digital nomads, and foreign workers, all of whom require reliable healthcare coverage during their stay.

While the country boasts a high standard of medical care at relatively affordable costs, access to public healthcare is generally limited to citizens and permanent residents. As such, private health insurance is essential for foreigners living in or visiting Malaysia. There are numerous insurance providers offering tailored plans that cover inpatient and outpatient treatments, emergency services, maternity care, and even dental and optical benefits.

These policies can be purchased locally or internationally, but it's crucial for expatriates to thoroughly understand the terms, including coverage limits, exclusions, and procedures for filing claims. Moreover, certain visa types—like the Malaysia My Second Home (MM2H) program or employment passes—require proof of valid health insurance as part of the application or renewal process, making it a mandatory rather than optional consideration.

Types of Health Insurance Available for Foreigners

Foreigners in Malaysia have access to a variety of health insurance plans, including international private medical insurance (IPMI), local private health insurance, and employer-sponsored group medical coverage.

Does Personal Auto Insurance Cover Turo Rental

Does Personal Auto Insurance Cover Turo RentalInternational health insurance plans are often preferred by expatriates due to their portability and global coverage, allowing policyholders to receive medical treatment not only in Malaysia but also in their home country or while traveling. These plans typically offer higher coverage limits and access to a wider network of hospitals and specialists. In contrast, local private insurance policies are more affordable but may have stricter limitations on coverage and provider networks.

Employer-provided health benefits are common among foreign professionals with work visas, but the extent of coverage can vary significantly depending on the company and contract terms. It’s essential to compare plans carefully to ensure they meet individual healthcare needs and comply with visa requirements.

Legal Requirements and Visa-Linked Health Coverage

Malaysian immigration authorities require certain categories of foreign residents to have valid health insurance as a condition of their stay. For instance, participants in the Malaysia My Second Home (MM2H) program must demonstrate they have comprehensive medical insurance that covers hospitalization and treatment in Malaysia.

Similarly, foreign workers on Employment Passes or Professional Visit Visas are often required by their employers to have medical coverage as part of the expatriate package. Although there is no universal mandate for all foreigners, having proof of insurance can be critical during visa applications, renewals, or medical emergencies.

Downsides Of Bundling Home And Auto Insurance

Downsides Of Bundling Home And Auto InsuranceSome government-linked hospitals may also request insurance verification before admitting foreign patients, especially for non-emergency procedures. Therefore, obtaining compliant and reliable health insurance is not only a practical necessity but also a legal and administrative requirement for long-term residency.

Top Insurance Providers and Coverage Comparison

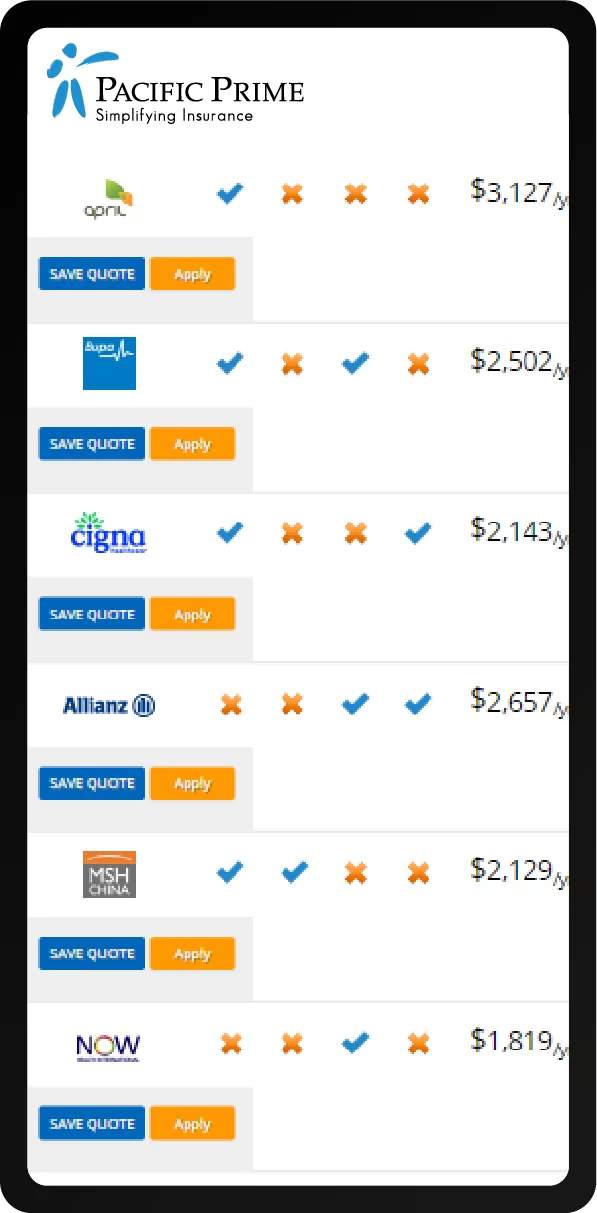

Several reputable insurance companies offer specialized health plans for foreigners in Malaysia, including AXA Affin, Allianz Malaysia, Tune Insurance, and international providers like Cigna Global, Aetna International, and Bupa.

These insurers offer a range of plans with varying levels of coverage, premiums, and service networks. Local insurers typically provide cost-effective solutions with coverage focused on Malaysian healthcare facilities, while global insurers offer broader access, including medical evacuation and treatment abroad.

When comparing plans, it's important to consider factors such as annual and lifetime benefit limits, deductible amounts, waiting periods, pre-existing condition clauses, and direct billing arrangements with hospitals. Many expatriates choose plans that include 24/7 multilingual customer support and streamlined claims processing to ensure hassle-free medical care.

E Insurance Auto Quote

E Insurance Auto Quote| Insurance Provider | Plan Type | Coverage Scope | Key Benefits | Notable Limitations |

|---|---|---|---|---|

| Cigna Global | International | Global including Malaysia | High coverage limits, medical evacuation, 24/7 support | Higher premiums, stricter underwriting |

| AXA Affin | Local Private | Malaysia only | Affordable premiums, local hospital network | Limited international coverage |

| Bupa Global | International | Worldwide | Comprehensive outpatient and inpatient care | Premium pricing, annual renewals |

| Allianz Malaysia | Local/Expat Plans | Malaysia-focused | Customizable packages, maternity coverage | Exclusions on pre-existing conditions |

| Tune Insurance | Budget-Friendly | Limited hospitals in Malaysia | Low-cost plans, simple claims | Narrow provider network, lower caps |

Comprehensive Guide to Health Insurance for Expatriates in Malaysia

Can expatriates purchase private health insurance in Malaysia?

Eligibility of Expatriates to Purchase Private Health Insurance in Malaysia

- Yes, expatriates residing in Malaysia are generally eligible to purchase private health insurance. The Malaysian private healthcare system is well-developed and welcomes foreign nationals, especially those holding valid work permits, employment passes, or long-term social visit passes. Insurance providers recognize the need for comprehensive medical coverage among expatriates and offer tailored plans to meet their requirements.

- Most insurance companies require proof of legal residency or employment in Malaysia as part of the application process. This ensures that expatriates are authorized to stay in the country for an extended period and reduces administrative risks for insurers. Common documentation includes a valid passport, visa status, employment contract, or a letter from the employer.

- Some insurers may also require a medical screening or health declaration before issuing a policy, particularly for individuals over a certain age or those applying for comprehensive coverage. However, many plans are designed to provide immediate coverage with minimal waiting periods, making it convenient for expats relocating to Malaysia for work or retirement.

Types of Health Insurance Plans Available for Expatriates

- Expatriates in Malaysia can choose from a range of private health insurance plans, including individual policies, family plans, and group coverage through employers. Individual plans offer flexibility and customization, allowing expats to select coverage limits, inclusions, and add-ons such as dental or maternity benefits.

- International health insurance plans are especially popular among expats, as they often provide coverage beyond Malaysia, including emergency medical evacuation, repatriation, and access to top-tier hospitals worldwide. These plans are usually offered by global insurers with a strong presence in the region and can be maintained even if the policyholder relocates to another country.

- Local private health insurance plans, offered by Malaysian insurers, are typically more affordable and focused on in-country medical services. They usually cover hospitalization, specialist consultations, surgeries, and day-care procedures at private hospitals across Malaysia. Expatriates should carefully compare benefits, exclusions, claim procedures, and network hospitals before selecting a plan.

Considerations When Choosing Health Insurance as an Expat in Malaysia

- One of the most important factors for expatriates is whether the insurance plan covers treatments at private hospitals, which are preferred by most expats due to shorter waiting times and English-speaking staff. It is essential to verify that the policy includes access to major private healthcare providers such as Gleneagles, Sunway Medical Centre, or KPJ Healthcare.

- Premium costs vary significantly depending on age, health condition, coverage scope, and deductible levels. Expatriates should assess their healthcare needs—routine check-ups, chronic condition management, or potential emergencies—and select a plan that balances cost with adequate protection.

- Understanding the claims process is crucial. Most insurers offer direct billing (cashless treatment) at network hospitals, which simplifies access to care. However, for out-of-network providers or overseas treatment, reimbursement-based claims may apply, requiring expats to pay upfront and submit documentation later. Reading the policy terms thoroughly and clarifying doubts with the insurer or broker is strongly advised.

What is the average cost of health insurance for foreigners in Malaysia?

Factors That Influence Health Insurance Costs for Foreigners in Malaysia

- Age and medical history play a significant role in determining premiums; older individuals or those with pre-existing conditions typically face higher costs due to increased health risks.

- The type of coverage selected—whether basic hospitalization or comprehensive plans that include outpatient care, dental, and maternity services—affects the overall price.

- The geographical scope of the insurance, such as local-only coverage versus regional or global access, also influences the monthly or annual premium amount.

- On average, foreigners in Malaysia can expect to pay between MYR 150 to MYR 600 per month (approximately USD 35 to USD 140) for a standard health insurance plan.

- For more extensive coverage, including private hospital access and international treatment options, annual premiums may range from MYR 10,000 to MYR 25,000 (USD 2,100 to USD 5,300).

- Short-term plans, often used by expatriates on work assignments or students, generally cost less but offer limited benefits compared to long-term expatriate health insurance policies.

Popular Insurance Providers and Plan Options for Expatriates

- International providers such as Aetna International, Cigna Global, and NOW Health offer tailored expatriate health plans with customizable coverage levels and customer support in multiple languages.

- Local insurers like Pacific & Orient (P&O) and Tune Protect also provide affordable health insurance options, though these often have more restrictions and limited network hospitals compared to international plans.

- Many employers in Malaysia sponsor health insurance as part of expatriate employment packages, typically opting for group plans that reduce individual costs and streamline claims processing.

Is health insurance necessary for foreigners living in Malaysia?

Why Health Insurance Is Important for Foreigners in Malaysia

- Healthcare in Malaysia, while relatively affordable compared to Western countries, can still be costly for foreigners who are not covered by insurance. Without proper coverage, medical treatments, hospitalization, and emergency services can lead to significant out-of-pocket expenses, especially for long-term or critical illnesses.

- Expatriates and foreign workers often do not qualify for subsidized public healthcare, which is primarily reserved for Malaysian citizens. This makes private healthcare the main option, and private hospitals typically charge higher rates, making health insurance a crucial financial safeguard.

- Having health insurance also provides access to a wider network of hospitals and shorter waiting times, particularly in high-quality private medical facilities. This ensures timely medical attention and peace of mind, especially in urgent situations.

Legal and Visa Requirements Regarding Health Insurance

- While Malaysia does not universally mandate health insurance for all foreign residents, certain visa types do require proof of coverage. For instance, applicants for the Malaysia My Second Home (MM2H) program must show evidence of medical insurance valid in Malaysia.

- Employers sponsoring foreign workers are generally required to provide medical benefits as part of employment contracts, and some work permits or passes may include insurance as a condition of approval. Failing to meet these requirements can result in visa delays or denials.

- Even when not legally required, having health insurance supports smoother immigration processing and demonstrates financial responsibility, which can be beneficial during visa renewals or residency applications.

Coverage Options and Types of Health Insurance Available

- Foreigners in Malaysia can choose from international health insurance plans, which offer broader coverage across multiple countries, or local expatriate health insurance tailored specifically for medical care within Malaysia. International plans are ideal for those who travel frequently or plan to move between countries.

- Local private health insurance plans typically cover inpatient care, outpatient consultations, maternity services, vaccinations, and emergency treatments. Some policies also include dental and optical benefits, though these may come at an additional cost.

- It is important to compare policies based on coverage limits, exclusions, network hospitals, claim procedures, and premium costs. Many expatriates also opt for top-up plans to supplement basic employer-provided coverage and ensure more comprehensive protection.

Are public hospitals in Malaysia accessible to foreigners without local health insurance?

Evaluate The Auto Insurance Company Allstate On Claims Process

Evaluate The Auto Insurance Company Allstate On Claims ProcessAccess to Public Hospitals for Foreigners in Malaysia

Foreigners are allowed to access public hospitals in Malaysia even without local health insurance. The Malaysian public healthcare system provides medical services to both citizens and non-citizens, though foreigners are generally charged higher fees compared to locals.

These services are available in emergency situations as well as for non-emergency treatments, depending on the hospital’s capacity and policies. While citizens benefit from subsidized care through government funding, foreigners must pay out-of-pocket for consultations, diagnostics, treatments, and hospitalization. It is important to note that access does not require proof of residency or insurance, but proper identification such as a passport is required.

- Public hospitals in Malaysia do not deny treatment to foreigners during emergencies, ensuring immediate care regardless of insurance status.

- Patients without local insurance must present a valid passport and may be asked to provide contact information and financial guarantees for ongoing treatment.

- Some specialized treatments or long-term care may require upfront payment or deposits before services are rendered.

Cost Implications for Uninsured Foreigners

Receiving treatment in Malaysian public hospitals as a foreigner without local health insurance comes with significant financial responsibilities. Since the government subsidizes healthcare for citizens, foreigners are charged the full cost of services, which can be substantially higher in comparison.

Fees vary depending on the hospital, type of treatment, and duration of stay. Diagnostic tests, surgical procedures, and intensive care services are priced at international or near-private hospital rates. While these costs are often lower than those in private hospitals or Western countries, they can still be considerable, especially for prolonged or complex medical conditions.

- Foreign patients are typically required to settle medical bills at the time of service or upon discharge, with no billing arrangements usually available.

- Costs for common procedures—such as X-rays, blood tests, and minor surgeries—are published, but additional charges may apply depending on complications or extended stays.

- Some hospitals provide cost estimates upon request, which can help patients plan for treatment expenses in advance.

Documentation and Administrative Requirements

Foreigners seeking medical care in Malaysian public hospitals must comply with specific documentation and administrative processes. While emergency cases are treated immediately, registration is mandatory and usually requires presenting a valid passport upon admission.

In non-emergency cases, individuals may need to schedule appointments and provide personal and contact details. Hospitals may also record visa status for record-keeping, though this does not affect eligibility for treatment. Additionally, patients are often required to pay for services before receiving certain medical reports or referrals to other facilities.

- A valid passport is essential for registration, and in some cases, a copy may be kept on file during the treatment period.

- Patients may be asked to provide a local contact number or emergency contact in Malaysia to facilitate communication.

- Non-emergency services might require advance payment or confirmation of financial responsibility before treatment begins.

Frequently Asked Questions

Do foreigners need health insurance in Malaysia?

Yes, foreigners in Malaysia are strongly advised to have health insurance. While public hospitals offer affordable care, private healthcare can be expensive. Many visa types, such as the Malaysia My Second Home (MM2H) program, require proof of health coverage. Insurance ensures access to quality medical services and protects against high out-of-pocket costs in private facilities.

Can expatriates use Malaysia’s public healthcare system?

Yes, expatriates can use Malaysia’s public healthcare system, but access may be limited and waiting times longer than in private clinics. Public hospitals often prioritize citizens. Foreigners usually pay higher fees and may need to show proof of insurance or payment ability. Many expats prefer private hospitals for faster, more comprehensive care despite higher costs.

What does expat health insurance in Malaysia typically cover?

Expat health insurance in Malaysia typically covers hospitalization, specialist consultations, emergency care, maternity (with waiting periods), and outpatient services. Some plans include dental and optical benefits. Coverage varies by provider and plan—international policies often offer broader networks and evacuation services. Always review policy details for exclusions, limits, and pre-existing condition rules before purchasing.

How do I choose the best health insurance as a foreigner in Malaysia?

To choose the best health insurance, assess your medical needs, length of stay, and budget. Compare local and international providers for coverage scope, hospital network, customer service, and claim processes. Prioritize plans with access to private hospitals and emergency support. Ensure the policy meets visa requirements if applicable, and confirm inclusion of chronic conditions or maternity care if needed.

Leave a Reply