Home and auto insurance in anaheim

Home and auto insurance in Anaheim provide essential protection for residents navigating the unique challenges of this dynamic Southern California city.

With its mix of urban neighborhoods, busy roadways, and exposure to regional risks like earthquakes and wildfires, having comprehensive coverage is crucial. Anaheim’s high population density and traffic congestion increase the likelihood of auto accidents, making reliable auto insurance a necessity.

At the same time, homeowners face rising property values and potential hazards, driving demand for robust home insurance policies. Local insurers offer tailored solutions that reflect these realities, balancing affordability with adequate coverage.

Accelerated Death Benefits Life Insurance

Accelerated Death Benefits Life InsuranceUnderstanding Home and Auto Insurance in Anaheim

In Anaheim, California, both home and auto insurance are essential for protecting one’s property and financial well-being.

As a city located in Orange County with a mix of urban neighborhoods and suburban communities, Anaheim presents unique risks—from wildfire threats in dry seasons to high traffic congestion contributing to auto accidents. Homeowners must consider coverage for natural disasters, liability protection, and rebuilding costs, while drivers need adequate liability, collision, and comprehensive insurance due to California’s mandatory requirements and high population density.

Insurance rates in Anaheim are influenced by location-specific factors such as crime rates, proximity to freeways, and local weather patterns. Choosing the right policies involves comparing multiple providers, understanding coverage limits, and ensuring discounts—like bundling home and auto insurance—are fully utilized to reduce premiums.

Factors Affecting Home Insurance Rates in Anaheim

Home insurance premiums in Anaheim are shaped by several localized factors, including the age and construction type of the home, its proximity to fire stations, and the neighborhood’s historical crime data.

Permenent Life Insurance

Permenent Life InsuranceHomes built before modern seismic codes may face higher premiums due to earthquake vulnerability, even though standard policies do not cover earthquake damage—requiring a separate policy. Insurers also evaluate local wildfire risk, especially in areas bordering hills or open spaces, and may require enhanced fire-resistant materials for coverage eligibility.

Additionally, homes with security systems, fire alarms, or storm shutters may qualify for discounts. Market demand, rising construction costs in Southern California, and increasing insurance claims due to extreme weather are also causing steady increases in home insurance rates across the city.

Auto Insurance Requirements and Coverage Options in Anaheim

California law mandates minimum auto insurance coverage, which in Anaheim includes $15,000 for injury or death to one person, $30,000 for injury or death to more than one person, and $5,000 for property damage (15/30/5).

However, many residents opt for higher liability limits to ensure greater financial protection, especially in a high-cost area like Anaheim where medical expenses and vehicle repairs can be substantial. Optional coverages such as collision, comprehensive, uninsured/underinsured motorist, and medical payments (MedPay) are frequently added to policies. Insurance companies use driving history, vehicle type, annual mileage, and credit-based insurance scores to determine rates.

Term Life Insurance And

Term Life Insurance AndDue to heavy traffic on major routes like the 5 and 91 freeways, accident frequency remains high, which influences premiums. Safe driving discounts, multi-policy bundling, and usage-based programs can help Anaheim drivers lower their insurance costs.

Bundling Home and Auto Insurance: Benefits for Anaheim Residents

Bundling home and auto insurance is a widely recommended strategy for Anaheim residents seeking to reduce their overall insurance expenses. Most major insurers, including State Farm, Allstate, and Farmers, offer multi-policy discounts that can save policyholders anywhere from 10% to 25% on combined premiums.

These bundles not only lower costs but also simplify billing and claims management by consolidating policies under a single provider. For families with multiple vehicles or homes, such as rental properties, the savings and administrative convenience become even more significant.

Additionally, insurers often prioritize customer service and loyalty benefits for bundled accounts, including faster claims processing and dedicated agents. When shopping for bundled insurance, it’s crucial to compare not just upfront discounts but also the strength of coverage, customer satisfaction scores, and financial stability of the insurance company.

| Insurance Type | Average Annual Cost in Anaheim | Key Coverage Factors | Common Discounts |

|---|---|---|---|

| Home Insurance | $1,200 – $1,800 | Property value, construction type, wildfire & burglary risk | Security systems, multi-policy, claims-free |

| Auto Insurance | $1,600 – $2,400 | Driving record, vehicle model, annual mileage, location | Bundling, safe driver, low mileage, anti-theft devices |

| Bundled (Home + Auto) | $2,600 – $3,600 (potential 15% savings) | Coverage limits, shared insurer, claim history | Multi-policy, loyalty, electronic billing |

Comprehensive Guide to Home and Auto Insurance in Anaheim

What is the most affordable home and auto insurance in Anaheim, California?

Top Affordable Home and Auto Insurance Providers in Anaheim

When looking for the most affordable home and auto insurance in Anaheim, California, several insurance providers stand out due to their competitive rates and strong service records.

Based on customer reviews, pricing comparisons, and coverage options, companies such as Progressive, Nationwide, and State Farm consistently rank among the most cost-effective choices for bundling home and auto policies. These insurers offer multi-policy discounts, safe driver incentives, and tools to help customers manage premiums effectively.

Additionally, they provide localized rate assessments that consider Anaheim-specific risks such as property values, traffic density, and natural disaster exposure. To get the lowest rates, it's essential to compare quotes from multiple providers and ensure accurate input of personal and property details.

- Progressive offers a user-friendly online platform where drivers can compare bundled rates and access real-time discounts based on driving behavior through its Snapshot program.

- Nationwide provides a unique bundling discount called SafeDiscount, which rewards customers for combining home and auto policies along with other safety-related factors.

- State Farm, one of the largest insurers in California, frequently offers local agent support in Anaheim, enabling personalized quotes and faster claims processing.

Factors That Influence Insurance Rates in Anaheim

Insurance premiums in Anaheim are influenced by several location-specific and individual factors that can significantly impact affordability.

The city's proximity to fault lines increases earthquake risk, which often leads to higher home insurance costs unless a separate earthquake policy is declined. Auto insurance rates are affected by traffic congestion, accident frequency, and vehicle theft rates—Anaheim’s central location in Orange County contributes to moderate-to-high traffic exposure.

On the individual level, credit score, claims history, home age, and the type of vehicle driven all play a crucial role in determining final premiums. Additionally, insurers consider local crime statistics and fire protection resources when calculating home insurance rates, making neighborhood differences important.

- Home age and construction type influence underwriting decisions; older homes may lack modern safety features, leading to higher premiums.

- Drivers with clean records and higher credit scores typically qualify for the lowest auto insurance rates, especially when bundling policies.

- Neighborhood-specific crime and fire protection ratings, such as Insurance Services Office (ISO) scores, directly affect home insurance pricing in different Anaheim ZIP codes.

How to Lower Your Combined Insurance Costs

Reducing the cost of home and auto insurance in Anaheim involves strategic planning, regular comparisons, and taking advantage of available discounts. The most effective method is bundling both policies with the same provider, which typically results in savings of 15% to 25%.

Installing home security systems, maintaining a good driving record, and raising deductibles can also contribute to lower premiums. Customers should review their coverage annually and request personalized quotes, as rates can change based on market conditions and personal circumstances. Using comparison tools from websites like Insurify, NerdWallet, or Bankrate allows residents to evaluate multiple options without affecting their credit score.

- Bundling home and auto insurance policies is one of the most reliable ways to lower premiums, with many companies offering automatic discounts for multi-policy holders.

- Increasing deductibles on both home and auto policies can reduce monthly payments, though customers should ensure they can afford the out-of-pocket costs if a claim occurs.

- Regularly shopping around and requesting updated quotes every six to twelve months helps identify new discounts and prevents rate creep from long-term loyalty without reward.

Why did Geico exit the California home and auto insurance market, especially in Anaheim?

Regulatory and Financial Challenges in California's Insurance Market

- California’s insurance regulatory environment has become increasingly complex and costly for insurers to navigate. The California Department of Insurance (CDI) enforces strict rate approval processes, which limit an insurer's ability to adjust premiums in response to rising claims and operational costs.

- Geico specifically cited an inability to obtain timely and adequate rate increases as a key factor in its decision to withdraw. The company argued that without reasonable rate adjustments, it could not sustainably cover the high costs associated with fire, theft, and accident claims in the state.

- Additionally, the rising cost of reinsurance—the insurance that companies buy to protect themselves from large-scale losses—has weighed heavily on profitability, making it difficult for Geico to maintain competitive rates while remaining financially sound.

High Risk Exposure and Natural Disaster Costs

- California’s susceptibility to wildfires, earthquakes, and extreme weather events has significantly increased risk exposure for property insurers. Areas near Anaheim, while not directly in high-wildfire zones, are still affected by regional disaster risks and proximity to mountainous or semi-arid regions prone to fire outbreaks.

- Geico, like many insurers, has seen a surge in claims related to wildfire damage and weather-related accidents. The frequency and severity of these events have led to massive payout obligations that outpace premium revenues.

- The unpredictability of natural disasters makes long-term risk modeling difficult, prompting Geico to retreat from markets where potential losses could destabilize its balance sheet, especially in densely populated and high-exposure areas across Southern California.

Strategic Business Realignment and Market Competition

- Geico has been streamlining its operations to focus on markets where it can maintain profitability and growth. Exiting California allows the company to redirect resources toward regions with lower regulatory hurdles and more stable risk profiles.

- The California auto and home insurance market is intensely competitive, with numerous local and national carriers offering aggressive pricing. This competition further pressures margins, particularly when combined with high claims costs and regulatory constraints.

- Although Anaheim itself does not represent a unique risk compared to other cities in the region, it falls within a broader geographic area where underwriting conditions have deteriorated. Geico’s withdrawal was not targeted solely at Anaheim but applied to the entire state, reflecting a comprehensive reassessment of its presence in California.

What auto and home insurance providers does Dave Ramsey recommend in Anaheim?

Top Insurance Providers Recommended by Dave Ramsey

Dave Ramsey does not directly endorse specific insurance companies based on location, such as Anaheim, but he does recommend working with providers that meet his standards for customer service, value, and financial strength.

Through his network of endorsed local providers (ELPs), Ramsey refers individuals to insurance agents who have been vetted for their integrity, adequate coverage offerings, and competitive pricing. While the exact providers vary by region, in California—including areas like Anaheim—common ELPs include companies such as State Farm, Allstate, and Liberty Mutual.

These insurers are frequently highlighted because they offer personalized service and align with Ramsey’s principles of responsible financial planning. The key factor is not the national brand itself, but rather the local agent’s adherence to Ramsey’s guidelines.

- State Farm – Often recommended due to its extensive agent network and strong customer satisfaction ratings.

- Allstate – Recognized for customizable policies and discounts that support budget-conscious consumers.

- Liberty Mutual – Known for bundling home and auto insurance effectively, helping clients save significantly.

How to Find a Ramsey-Endorsed Provider in Anaheim

To locate an insurance provider in Anaheim who is officially endorsed by Dave Ramsey, individuals should visit the Ramsey Solutions website and use the “Endorsed Local Providers” directory. This tool allows users to input their ZIP code and select the service they need—such as auto or home insurance—to find qualified local agents.

These agents are trained to follow Ramsey’s financial principles, including advising clients to carry high deductibles to keep premiums low and purchasing only necessary coverages. In Anaheim, multiple agents from national carriers as well as independent agencies appear in the directory, giving consumers options to compare pricing and service firsthand.

- Visit RamseySolutions.com and navigate to the ELP section to begin the search.

- Enter your Anaheim ZIP code and select “Insurance” to filter for auto and home coverage experts.

- Contact at least three agents to compare quotes, customer service experiences, and policy options.

Insurance Coverage Principles Promoted by Dave Ramsey

Dave Ramsey emphasizes a strategic approach to insurance that prioritizes protection over profit for insurance companies. He advocates for carrying only the necessary coverage to avoid overspending while ensuring protection against major financial loss. For auto insurance, he recommends liability, collision, and comprehensive coverage with a deductible of at least $1,000.

For home insurance, he encourages an 80/20 split—80% coverage on the structure and 20% on personal property—with additional umbrella liability protection. These principles are designed to reduce premium costs while maintaining adequate protection, and Ramsey-endorsed providers in Anaheim typically structure policies accordingly.

- Choose higher deductibles to lower monthly premiums and reserve insurance for significant claims.

- Avoid unnecessary add-ons such as rental car reimbursement unless critical to your financial situation.

- Bundle home and auto policies with one provider to maximize savings while ensuring adequate coverage.

Frequently Asked Questions

What does home and auto insurance in Anaheim typically cover?

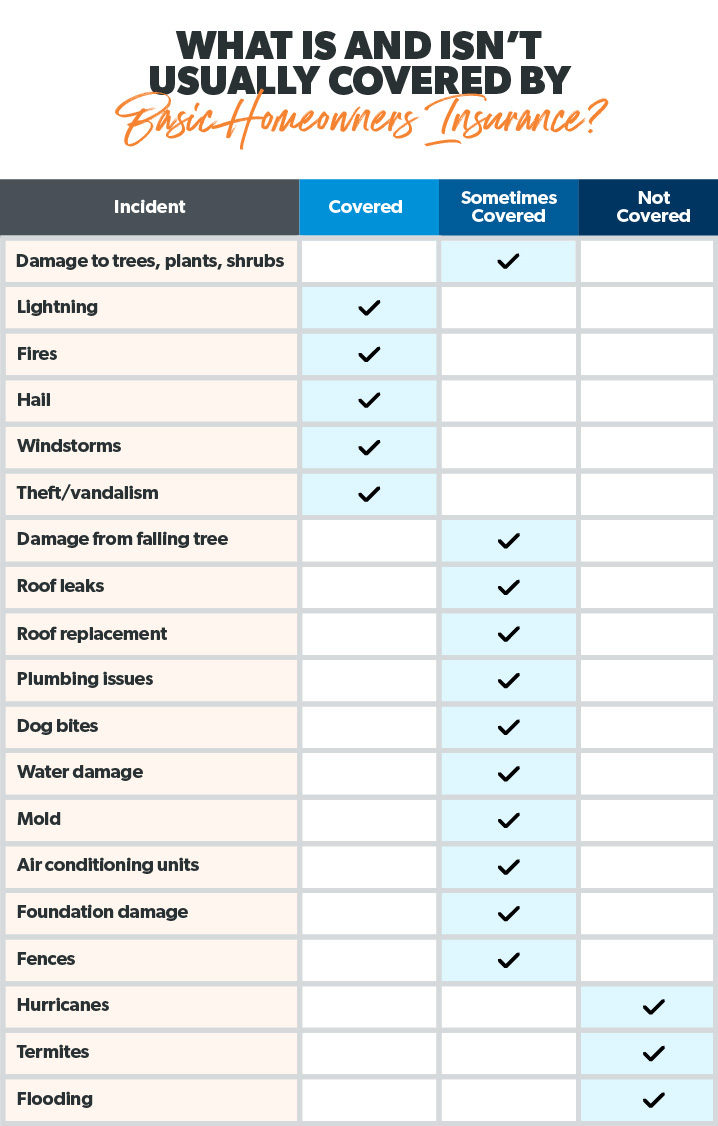

Home and auto insurance in Anaheim generally covers property damage, liability, and personal injury. Home policies protect against fire, theft, and certain natural disasters common in Southern California. Auto insurance includes liability, collision, and comprehensive coverage. Many insurers offer bundled policies for savings. Coverage specifics vary by provider, so it’s important to review individual policy details to ensure adequate protection for your home and vehicle.

Why should I bundle home and auto insurance in Anaheim?

Bundling home and auto insurance in Anaheim can lead to significant savings, often up to 25% on combined premiums. It simplifies billing and policy management with a single provider. Bundling also strengthens customer loyalty, potentially leading to additional discounts. Most major insurers offer bundle options. Plus, having coordinated coverage can streamline the claims process. Always compare bundled rates with separate policies to ensure you're getting the best value.

How do I find the best home and auto insurance rates in Anaheim?

To find the best home and auto insurance rates in Anaheim, compare quotes from multiple reputable insurers. Check customer reviews, coverage options, and financial stability. Use online comparison tools or consult a licensed insurance agent. Consider discounts for bundling, safety features, or good driving records. Review each policy’s deductibles and limits. Updating coverage annually and adjusting for lifestyle changes can also help secure optimal rates.

Are there specific risks in Anaheim that affect home and auto insurance?

Yes, Anaheim residents face risks like earthquakes, wildfires, and vehicle theft that influence insurance costs. Standard home policies don’t cover earthquakes, so additional coverage is recommended. Wildfire risk in nearby areas may increase premiums. Auto insurance is affected by local traffic density and theft rates. Insurers consider these factors when pricing policies. Ensuring proper coverage for regional risks helps protect your home and vehicle effectively.

Leave a Reply