Home building insurance calculator

Building a home is a significant investment, and protecting it from the start is crucial. A home building insurance calculator helps future homeowners estimate the cost of insuring their property during and after construction.

This tool considers factors like location, materials, square footage, and project duration to provide accurate coverage estimates. Choosing the right insurance ensures protection against unexpected events such as fires, theft, or weather damage. Using a calculator simplifies decision-making, allowing builders and owners to compare policies and select affordable, comprehensive coverage tailored to their specific needs.

How a Home Building Insurance Calculator Helps You Estimate Coverage Needs

A home building insurance calculator is an essential online tool that enables homeowners and builders to estimate the cost of insuring a property under construction or renovation.

Permenent Life Insurance

Permenent Life InsuranceBy inputting specific details such as the property's location, size, construction type, and material costs, users can receive a tailored estimate of their required insurance coverage. This helps prevent underinsurance, which could leave a homeowner financially vulnerable in the event of damage or loss during construction.

The calculator typically considers factors like rebuilding costs, local labor rates, and potential risks associated with the area, such as floods or storms. Using a calculator not only simplifies the process but also empowers users to compare different insurance quotes effectively and make informed decisions based on accurate data.

What Is a Home Building Insurance Calculator?

A home building insurance calculator is a digital tool designed to help individuals estimate the cost of insuring a residential structure during its construction phase.

This calculator typically requires users to enter key project details such as the home’s square footage, construction materials (e.g., brick, timber), build quality (standard, premium), and location. Based on these inputs, the calculator computes the rebuild cost—the amount it would take to reconstruct the home from the ground up if destroyed.

Term Life Insurance And

Term Life Insurance AndIt differentiates from standard home insurance by focusing exclusively on the construction phase, covering risks like fire, theft, weather damage, or contractor errors. By providing a clear estimate, this tool helps builders and homeowners secure adequate coverage without overpaying.

Key Factors That Influence the Calculator’s Results

Several critical variables affect the output of a home building insurance calculator, ensuring that the estimate reflects the actual risk and cost of coverage.

Among the most influential factors are geographic location, which determines exposure to natural disasters such as hurricanes or earthquakes; construction type and materials, since more expensive or fire-resistant materials affect rebuild costs and risk levels; and project duration, as longer builds increase the window of exposure to potential damage.

Other important considerations include the sum insured (the maximum payout), security measures on site (e.g., fencing, alarms), and whether professional contractors or DIY builders are involved. Accurate data entry is essential, as underreporting any factor could lead to insufficient coverage when making a claim.

Evaluate The Insurance Company Guardian Life On Absence Management Solutions

Evaluate The Insurance Company Guardian Life On Absence Management SolutionsBenefits of Using an Online Home Building Insurance Calculator

Using an online home building insurance calculator offers numerous advantages, making it a preferred starting point for anyone arranging construction coverage. It provides instant, transparent estimates without requiring personal details, allowing users to explore options anonymously.

This promotes price comparison across insurers and increases financial literacy around construction risks and costs. Additionally, calculators reduce the risk of human error associated with manual cost estimation and help homeowners align their budgets with realistic insurance premiums.

By encouraging early assessment of coverage needs, the tool supports compliance with lender or legal requirements, especially when building a new home or undertaking major renovations. Ultimately, it fosters proactive financial planning and risk management.

| Factor | Description | Impact on Insurance Cost |

|---|---|---|

| Construction Type | Refers to whether the build is brick, timber, steel, or another material. | High – Fire-resistant materials may reduce premiums. |

| Location Risk Level | Indicates susceptibility to floods, bushfires, or storms. | High – High-risk areas increase premiums. |

| Build Size (sqm) | Total floor area of the structure. | Medium – Larger homes cost more to rebuild. |

| Project Duration | Estimated time from groundbreaking to completion. | Medium – Longer builds may incur higher risk. |

| Security Measures | On-site precautions like fencing, lighting, or guards. | Low to Medium – Can lower premiums slightly. |

How to Use a Home Building Insurance Calculator: A Comprehensive Guide

What is the average insurance cost for a $400,000 home using a home building insurance calculator?

The average insurance cost for a $400,000 home typically ranges between $1,200 and $3,000 annually, depending on various factors such as location, construction type, coverage limits, and local risk exposure.

A home building insurance calculator can provide a more precise estimate by incorporating specific details about the property, including square footage, building materials, and proximity to fire services. These calculators often rely on industry-standard data and underwriting criteria to generate a realistic premium range. While national averages can offer a general idea, individual quotes may vary significantly based on personalized risk assessments.

Factors That Influence Insurance Costs for a $400,000 Home

- Geographic location plays a major role, as homes in areas prone to natural disasters like hurricanes, wildfires, or floods generally face higher premiums due to increased risk of damage.

- The construction materials and age of the home affect the cost—newer homes built with fire-resistant materials may qualify for lower rates compared to older structures with outdated electrical or plumbing systems.

- Local crime rates and proximity to fire stations or hydrants also factor into the calculation, with safer neighborhoods and better emergency access leading to reduced insurance expenses.

How Home Building Insurance Calculators Work

- These calculators begin by collecting key property details such as replacement cost, square footage, roof type, and number of stories to estimate the cost to rebuild the home.

- Next, they incorporate regional data on weather risks, crime statistics, and local building costs per square foot to adjust the base rate accordingly.

- Finally, user inputs like desired deductible, coverage endorsements (e.g., for water backup or earthquakes), and claims history are used to refine the final premium estimate.

Ways to Reduce the Cost of Insurance on a $400,000 Home

- Installing safety and security features such as smoke detectors, monitored alarm systems, and storm shutters can qualify homeowners for discounts from insurers.

- Choosing a higher deductible lowers the premium, though it means the homeowner would pay more out-of-pocket in the event of a claim.

- Bundling home insurance with auto or other policies through the same provider often results in significant multi-policy savings.

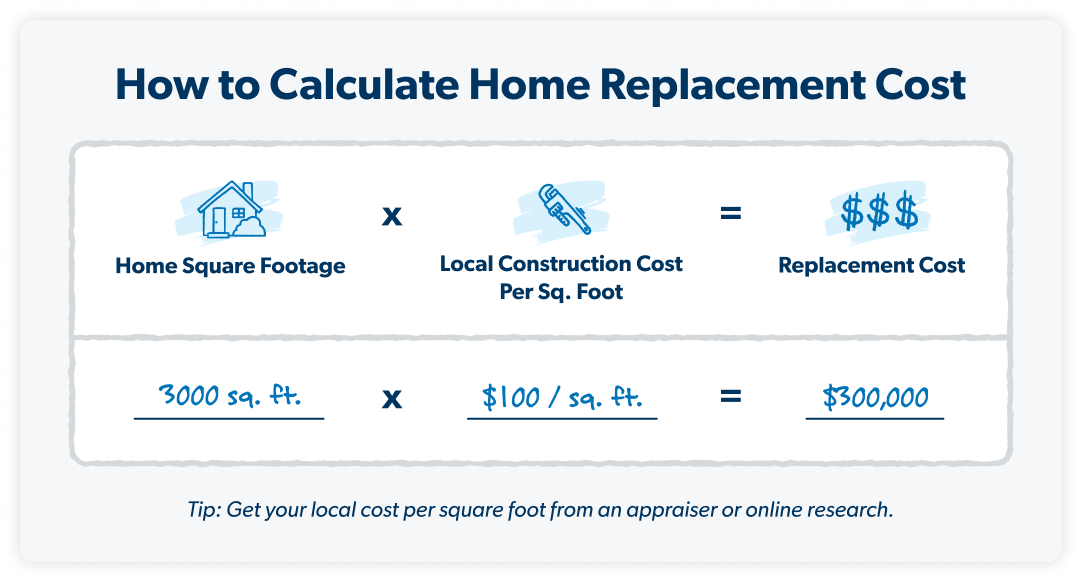

How to determine the sum insured for a building using a home building insurance calculator

Understanding the Purpose of Sum Insured in Building Insurance

- The sum insured represents the maximum amount an insurance provider will pay to rebuild or repair your home in the event of total destruction, such as from fire or natural disasters. It is not based on the market value of the property but on the reconstruction cost, which includes labor, materials, debris removal, and professional fees.

- Using a home building insurance calculator helps ensure that the sum insured is accurate and sufficient to cover full rebuilding expenses without underinsurance. Underestimating this value can lead to out-of-pocket expenses during a claim, while overestimating may result in unnecessarily high premiums.

- These calculators utilize data such as construction type, location, floor area, and property age to estimate rebuilding costs. It's important to update the sum insured periodically, especially after renovations or changes in construction costs, to maintain adequate coverage.

How a Home Building Insurance Calculator Works

- A home building insurance calculator collects key details about the property, such as total covered area in square feet or meters, number of floors, roof type, wall construction materials, and finish quality. This information directly affects rebuilding estimates since brick-and-mortar homes cost differently to rebuild than timber or steel-frame structures.

- The calculator applies regional construction cost rates per square foot, which vary by location due to labor rates, material availability, and local regulations. For example, rebuilding costs in urban areas are typically higher than in rural regions, and the tool adjusts accordingly.

- Additional features like garages, verandas, swimming pools, or detached structures are factored in as optional inputs. The total cost estimation from the calculator forms the recommended sum insured, which should ideally match the actual reconstruction cost at the time of policy purchase or renewal.

Factors to Consider When Using the Calculator Accurately

- Ensure all structural additions or modifications made since the house was built are included, such as extensions, loft conversions, or solar panel installations. Omitting these can result in an underinsured policy, leading to partial compensation during a claim.

- Use up-to-date calculators provided by reputable insurers or independent construction cost services, as outdated tools may use obsolete construction rates. Inflation in material and labor costs can significantly alter rebuilding estimates over time.

- Verify the calculator’s assumptions by comparing its output with quotes from licensed builders or chartered surveyors. This cross-check enhances accuracy and provides confidence that the determined sum insured reflects real-world rebuilding expenses.

What is the average homeowners insurance cost for a $300,000 house using a home building insurance calculator?

The average homeowners insurance cost for a $300,000 house typically ranges from $1,200 to $1,800 per year, depending on various factors such as location, coverage options, home age, and claims history. When using a home building insurance calculator, users input specific details about the property and desired coverage, allowing for a more accurate estimate.

These tools consider the dwelling coverage needed to rebuild the home, which for a $300,000 house usually amounts to around $250,000 to $300,000 in coverage, excluding the land value. Regional differences play a major role—for example, homes in areas prone to natural disasters like hurricanes or wildfires may have significantly higher premiums.

Factors That Influence Homeowners Insurance Costs on a $300,000 House

- Geographic location is one of the most influential factors; homes in regions with high crime rates or susceptibility to extreme weather such as tornadoes, floods, or earthquakes will have higher premiums due to increased risk exposure.

- The age and condition of the home significantly affect insurance pricing; older homes might require more expensive coverage due to outdated electrical systems, plumbing, or roofing, which increase the likelihood of claims.

- Personal factors such as credit score, insurance history, and claims frequency also impact the final cost, as insurers use these metrics to assess the homeowner’s risk profile and likelihood of filing future claims.

How a Home Building Insurance Calculator Determines Your Rate

- A home building insurance calculator starts by estimating the reconstruction cost of the home, which differs from market value; it factors in local labor and material costs required to rebuild the structure after a total loss.

- The tool incorporates coverage options selected by the user, such as dwelling protection, personal property, liability, and additional living expenses, each contributing to the overall premium estimate.

- Risk modifiers like protective devices (e.g., security systems, smoke detectors), roof type, and proximity to fire stations are considered to adjust the base rate, often leading to discounts or surcharges based on safety features.

Regional Variations in Insurance Costs for a $300,000 Home

- In states like Texas or Florida, where hurricanes and strong storms are common, annual premiums for a $300,000 house can exceed $2,500 due to the high risk of property damage and subsequent claims.

- Conversely, states such as Vermont or Maine often report lower average premiums—sometimes under $1,000 annually—thanks to fewer natural catastrophes and lower rates of insurance fraud.

- Urban versus rural settings also create cost differences; homes in densely populated areas may face higher rates due to increased theft and vandalism risks, while isolated rural properties might pay more due to limited fire protection access.

Frequently Asked Questions

What is a home building insurance calculator?

A home building insurance calculator is an online tool that estimates the cost of insuring the structure of your home. It considers factors like property size, location, construction type, and rebuild value. This helps homeowners compare quotes and choose suitable coverage. The calculator provides a quick, accurate approximation to assist in budgeting for insurance and ensuring adequate protection against structural damage or loss.

How does a home building insurance calculator work?

A home building insurance calculator works by collecting key property details such as address, square footage, building materials, and age of the structure. It uses this data to estimate the rebuild cost and assess potential risks like flooding or fire. Based on these factors, the tool calculates a projected insurance premium. This process allows users to receive instant, personalized estimates and compare different policy options efficiently and accurately.

Why should I use a home building insurance calculator?

You should use a home building insurance calculator to save time and money when choosing a policy. It provides transparent, customized estimates based on your home’s specific features. This helps ensure you’re neither underinsured nor paying for excessive coverage. The tool simplifies comparison shopping across insurers and increases understanding of what influences premiums, helping you make informed decisions and secure the best value for your home insurance needs.

Is a home building insurance calculator accurate?

Yes, a home building insurance calculator provides a reasonably accurate estimate based on the information you input. While it may not replace a professional assessment, it uses industry-standard data and algorithms to predict rebuild costs and risks. For the most precise quote, ensure all details are correct. It serves as a reliable starting point to guide your insurance choices and discussions with providers.

Leave a Reply