Permenent Life Insurance

Permanent life insurance offers lifelong coverage with a cash value component that grows over time, making it a powerful financial tool for long-term planning.

Unlike term life insurance, which expires after a set period, permanent policies remain in force as long as premiums are paid. These policies include whole life, universal life, and variable life, each offering distinct features and benefits. The accumulated cash value can be borrowed against or withdrawn, providing financial flexibility.

While premiums are typically higher than term insurance, the combination of a death benefit and savings element makes permanent life insurance a strategic option for estate planning, wealth transfer, and creating lasting financial security.

Top Benefits Of Buying Whole Life Insurance Young

Top Benefits Of Buying Whole Life Insurance YoungUnderstanding Permanent Life Insurance: Lifelong Coverage with Cash Value Benefits

Permanent life insurance is a comprehensive financial product designed to provide lifelong protection and a cash value accumulation component that distinguishes it from term life insurance. Unlike term policies, which offer coverage for a specified period, permanent life insurance remains in force for the insured’s entire life as long as premiums are paid.

This type of policy combines a death benefit—the amount paid to beneficiaries upon the policyholder’s death—with a savings element that grows over time on a tax-deferred basis. The cash value can be accessed through policy loans or withdrawals, offering flexibility for emergencies, supplemental retirement income, or other financial needs.

Because of its added features, permanent life insurance typically comes with higher premiums than term life, but it serves not only as a protection tool but also as a potential long-term wealth-building strategy. It is often used in estate planning, business succession planning, and for leaving a legacy.

Types of Permanent Life Insurance: Whole, Universal, and Variable Policies

There are several key variations within permanent life insurance, each tailored to different financial goals and risk tolerances. Whole life insurance offers guaranteed premiums, a fixed death benefit, and steadily growing cash value at a rate determined by the insurer, often with potential dividends.

Universal life insurance provides more flexibility, allowing policyholders to adjust premium payments and death benefits within certain limits, while the cash value earns interest based on current market rates or a minimum guarantee.

Variable life insurance enables policyholders to invest the cash value in a range of sub-accounts (similar to mutual funds), which means the cash value and death benefit can fluctuate with market performance, offering higher growth potential but also greater risk. Understanding these differences helps individuals choose the type that aligns best with their financial priorities and risk appetite.

How the Cash Value Component Works in Permanent Life Insurance

The cash value component is one of the hallmark features of permanent life insurance and functions as a tax-advantaged savings account within the policy.

A portion of each premium payment goes toward this cash value, which grows over time, typically on a tax-deferred basis, meaning you won’t pay taxes on the growth as long as the funds remain in the policy. This value can be borrowed against via policy loans, which usually don’t require credit checks or repayment schedules, although unpaid loans can reduce the death benefit.

What About Life Insurance

What About Life InsuranceAdditionally, policyholders may make partial withdrawals, although these can also affect the death benefit and may incur taxes if gains are withdrawn. The cash value continues to grow even as it’s accessed, depending on policy design, and can serve as a financial safety net or supplement retirement funds when planned strategically.

Advantages and Considerations of Permanent Life Insurance

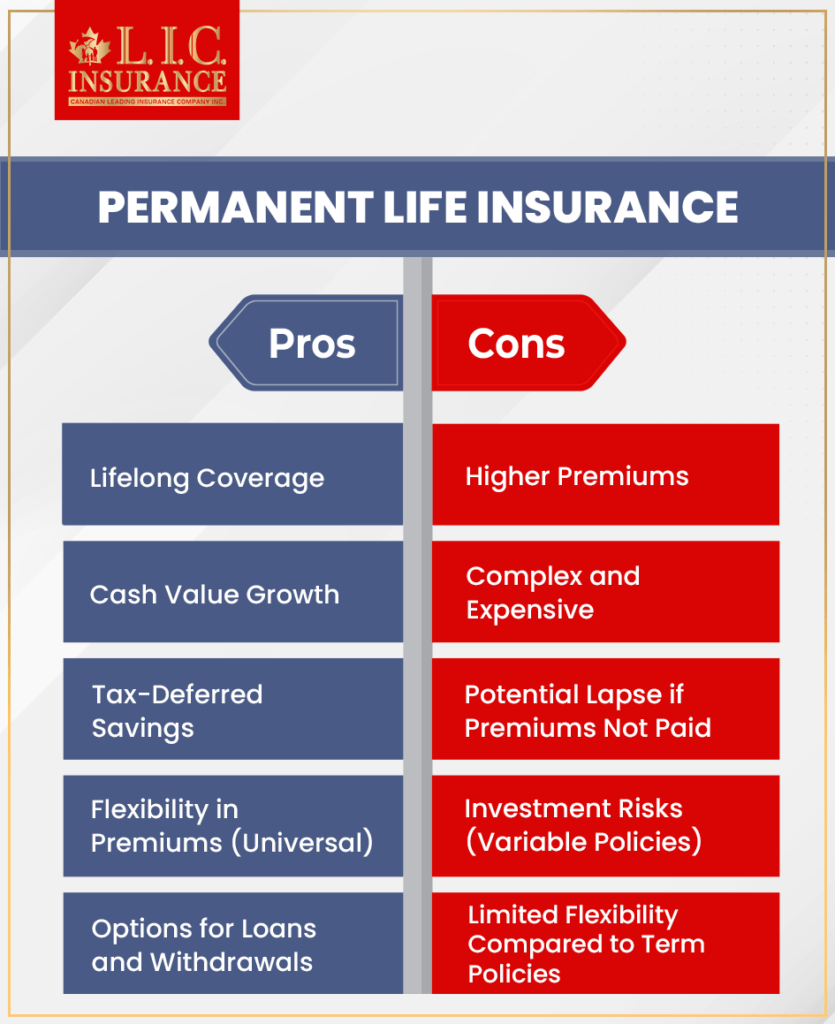

Permanent life insurance offers several advantages, including a guaranteed death benefit, lifelong coverage, and the opportunity to build cash value that can be leveraged during the policyholder’s lifetime. It also provides tax benefits, such as tax-deferred growth on the cash value and tax-free death benefits for beneficiaries in most cases.

Furthermore, it can play a role in estate planning, particularly for covering estate taxes or transferring wealth. However, there are important considerations: premiums are significantly higher than those for term life insurance, and the complexity of policies—especially universal and variable types—requires careful review.

Surrender charges, fees, and the impact of loans or withdrawals on the death benefit must be clearly understood. As such, working with a knowledgeable financial advisor is crucial to ensure the policy meets long-term objectives.

What Is An Illustration In Life Insurance

What Is An Illustration In Life Insurance| Feature | Whole Life | Universal Life | Variable Life |

|---|---|---|---|

| Premiums | Fixed and guaranteed | Flexible within limits | Usually fixed |

| Cash Value Growth | Guaranteed at set rate | Based on interest rates | Market-based (investments) |

| Death Benefit | Fixed or with dividends | Adjustable | Variable based on account performance |

| Risk Level | Low | Moderate | High |

| Best For | Stable, predictable growth | Flexibility in payments and benefits | Higher growth potential with risk tolerance |

Understanding Permanent Life Insurance: A Comprehensive Guide

Is Permanent Life Insurance a Wise Financial Decision?

Understanding Permanent Life Insurance and How It Works

- Permanent life insurance is a type of life insurance designed to provide lifetime coverage as long as premiums are paid, in contrast to term life insurance, which only lasts for a specified period. It includes a death benefit that is paid to beneficiaries upon the policyholder’s passing, ensuring financial protection for dependents.

- One defining feature of permanent life insurance is its cash value component, which grows over time on a tax-deferred basis. This cash value can be accessed during the policyholder’s lifetime through withdrawals or loans, offering a potential source of liquidity for emergencies or other financial needs.

- There are several types of permanent life insurance, including whole life, universal life, and variable life, each with different premium structures, investment options, and levels of flexibility. Whole life offers fixed premiums and guaranteed cash value growth, while universal life allows for adjustable premiums and death benefits, and variable life permits investment in sub-accounts similar to mutual funds.

Potential Advantages of Choosing Permanent Life Insurance

- One of the primary benefits of permanent life insurance is lifelong coverage, ensuring that beneficiaries will receive a death benefit regardless of when the policyholder dies, provided premiums are maintained. This can offer peace of mind for individuals with long-term financial responsibilities, such as supporting a child with special needs or covering estate taxes.

- The cash value accumulation can serve as a supplemental savings vehicle, especially in policies with guaranteed growth or dividend participation. Over time, this value can be used to fund various goals, such as supplementing retirement income, financing education, or covering large expenses without triggering taxable events, as long as withdrawals do not exceed the policy basis.

- From an estate planning perspective, permanent life insurance can play a strategic role by providing liquidity to heirs, helping them avoid forced asset sales to settle debts or tax liabilities. Additionally, when structured properly through irrevocable life insurance trusts (ILITs), the death benefit may be excluded from the taxable estate.

Drawbacks and Financial Considerations of Permanent Life Insurance

- Premiums for permanent life insurance are significantly higher than those for term life insurance, often costing five to fifteen times more for similar death benefit amounts. This cost can strain household budgets, particularly for younger individuals or families with limited disposable income, potentially diverting funds from other essential investments like retirement accounts.

- The complexity of policy structures, fees, and rate of return on cash value can make it difficult for consumers to fully understand their contracts. Some policies may take years to build meaningful cash value, and early surrender charges can erode value if the policy is canceled prematurely.

- From a pure investment standpoint, the returns on the cash value component of many permanent policies may underperform compared to low-cost, diversified investment alternatives such as index funds. Individuals who opt for permanent life insurance should carefully analyze whether the benefits justify the higher costs, especially if their primary goal is investment growth rather than insurance coverage.

What are the drawbacks of permanent life insurance coverage?

- Permanent life insurance typically requires significantly higher premiums than term life insurance because it provides lifelong coverage and includes a cash value component. These elevated costs can make permanent policies unaffordable for many individuals, especially when compared to the lower premiums of term policies that offer similar death benefits over a set period.

- The cost difference is due to the complexity of permanent policies, which combine insurance protection with a savings-like investment feature. Insurers must cover administrative fees, investment management, and other operational costs, all of which are passed on to the policyholder in the form of higher premiums.

- For budget-conscious consumers, the ongoing expense of permanent life insurance may limit their ability to invest in other financial goals, such as retirement savings or college funds, making it a less efficient choice for those who primarily need death benefit protection.

Limited Investment Returns and Cash Value Growth

- The cash value component of permanent life insurance grows at a relatively slow pace, often earning modest interest rates that may not keep up with inflation. Compared to other investment vehicles like mutual funds, index funds, or retirement accounts, the returns on cash value accumulation are typically underwhelming over the long term.

- Policyholders may face various fees and charges that reduce the effective growth of the cash value, including administrative fees, cost of insurance charges, and premium loads. These expenses can significantly erode the overall value, particularly in the early years of the policy.

- Accessing the cash value through withdrawals or loans can reduce the death benefit and may result in tax consequences if the policy lapses. Additionally, borrowing from the policy can create a debt that accrues interest, further diminishing the total financial benefit over time.

Complexity and Lack of Transparency

- Permanent life insurance policies often come with intricate terms, multiple fee structures, and various riders or optional features, which can make it difficult for consumers to fully understand how the policy works. This complexity increases the risk of misunderstandings about costs, benefits, and long-term performance.

- Many policyholders rely on agents or brokers for guidance, but misrepresentation or oversimplification during the sales process can lead to unrealistic expectations. For example, projected cash value growth may be based on optimistic assumptions that are unlikely to materialize under real-world conditions.

- The lack of standardized reporting and long-term performance metrics makes it challenging to compare different permanent life insurance products. Without clear, transparent information, consumers may end up with policies that do not align with their financial goals or risk tolerance.

Frequently Asked Questions

What is permanent life insurance?

Permanent life insurance provides lifelong coverage as long as premiums are paid and includes a cash value component that grows over time. Unlike term life insurance, it doesn't expire after a set period. It offers a death benefit to beneficiaries and allows policyholders to borrow against the accrued cash value, making it a financial tool for long-term protection and wealth-building strategies.

How does the cash value in permanent life insurance work?

The cash value in permanent life insurance grows over time on a tax-deferred basis. A portion of each premium payment funds this savings component, which accumulates interest or investment gains depending on the policy type. Policyholders can withdraw funds, take loans, or use it to pay premiums. Withdrawals up to the amount paid in premiums are typically tax-free.

What are the main types of permanent life insurance?

The main types of permanent life insurance are whole life, universal life, and variable life. Whole life offers fixed premiums and guaranteed cash value growth. Universal life provides flexible premiums and adjustable death benefits. Variable life allows investment in sub-accounts with potential for higher returns but increased risk. Each type balances stability and growth differently to meet diverse financial goals and risk tolerances.

Is permanent life insurance more expensive than term life insurance?

Yes, permanent life insurance is typically more expensive than term life insurance because it provides lifelong coverage and includes a cash value component. Premiums are higher due to the extended duration and additional financial features. While term life is cost-effective for temporary needs, permanent life is designed for long-term financial planning, estate planning, and wealth transfer, justifying its higher cost.

Leave a Reply