Home inspection ateviatch insurance calligraphy

A home inspection provides critical insights into the condition of a property, revealing potential issues before purchase or sale.

While often associated with structural integrity and safety, this process intersects with broader considerations like homeowners insurance, where findings can influence coverage and premiums. Less directly related but equally intricate, the art of calligraphy represents a meticulous craft requiring precision and patience—qualities mirrored in both inspections and policy evaluation.

Though seemingly unrelated, these fields share an emphasis on detail, documentation, and foresight. Understanding each element—inspection reports, insurance requirements, or even fine penmanship—enhances clarity and confidence in decision-making, whether in real estate, risk management, or creative expression.

Term Life Insurance And

Term Life Insurance AndUnderstanding the Connection Between Home Inspection, Ataviach Insurance, and Calligraphy

While the terms home inspection, ateviatch insurance, and calligraphy appear unrelated at first glance, a closer examination reveals potential intersections—particularly in the context of document authentication, property record maintenance, and legal compliance in certain administrative or cultural practices.

A home inspection is a standard procedure to assess a property’s condition, typically before purchase or insurance coverage. The term ateviatch insurance may be a typographical or phonetic variation of insurance for property or could refer to a niche or regional insurance product meant to cover property-specific risks.

If intended to mean insurance related to property or home, it aligns closely with home inspection outcomes. Calligraphy, the art of elegant handwriting, may seem out of place here, but it can play a role in formal documentation, such as handwritten deeds, historic property records, or official insurance forms in regions where stylized writing is used for authenticity.

Some cultures still value hand-lettered documents for legal or ceremonial weight, and in rare cases, insurance policies or inspection certifications might be preserved or issued in calligraphic form for tradition or fraud prevention due to unique handwriting identifiers. Thus, while not a mainstream technological link, the convergence lies in the domain of documentation integrity and ceremonial or localized administrative practices.

Evaluate The Insurance Company Guardian Life On Absence Management Solutions

Evaluate The Insurance Company Guardian Life On Absence Management SolutionsHome Inspection: Purpose and Importance in Property Evaluation

A home inspection is a comprehensive evaluation of a residential property’s physical structure and major systems, including plumbing, electrical, roofing, HVAC, and foundation. Typically conducted by a licensed inspector prior to a real estate transaction, the process aims to uncover existing or potential issues that could affect the property’s value, safety, or insurability.

Buyers rely on inspection reports to negotiate repairs, request price adjustments, or even withdraw from a deal. For insurers, the inspection data can influence risk assessment models and determine whether to underwrite a policy.

A clean inspection often leads to lower premiums or easier approval, while significant structural or safety flaws might require remediation before coverage is granted. In this context, the inspection serves as a bridge between tangible property conditions and intangible financial protections like insurance.

Clarifying Ataviatch Insurance: Possible Meanings and Relevance

The term ateviatch insurance does not correspond to any known insurance category in standard English usage, suggesting it may be a misspelling, phonetic transcription, or regional variant. Potential interpretations include a mishearing of a-the-vat-ch as atviatch or a typographical error for phrases like attestation insurance or property catch-all insurance.

Indexed Universal Life Insurance Lawyer Columbia

Indexed Universal Life Insurance Lawyer ColumbiaIn some linguistic contexts, particularly involving non-English languages, the word might resemble terms related to property safeguarding or asset endorsement. Assuming it refers to a form of home or property insurance, its relevance emerges when tied to inspection outcomes—insurance providers often require inspection reports to validate coverage terms.

If ateviatch implies a specialized policy, such as one covering art, antiques, or culturally significant items (which might include calligraphic works), it could pertain to niche home-based valuables coverage. Thus, the correct interpretation depends on linguistic context and regional insurance practices.

The Role of Calligraphy in Property and Insurance Documentation

Though seemingly unrelated to modern real estate processes, calligraphy holds historical and symbolic significance in legal and official documentation, particularly in cultures where handwritten artistry conveys authenticity, respect, or permanence.

In some jurisdictions, land deeds, wills, or notarized agreements may be drafted in calligraphic script to signify their solemnity and reduce tampering—each stroke serving as a unique identifier of the scribe. In the context of home ownership records or insurance certificates, especially for heritage properties, one might encounter ornamental documentation where calligraphy enhances the legal document’s perceived legitimacy.

Insurance Life Whole

Insurance Life WholeFurthermore, insurance companies dealing with high-value estates or culturally significant homes may commission calligraphic certificates as part of premium services. Digitization has largely replaced this practice, yet archival records or ceremonial documents may still feature calligraphic elements, linking the art form indirectly to the broader ecosystem of property verification and insurance.

| Term | Possible Meaning | Relevance to Home & Insurance |

|---|---|---|

| Home Inspection | Professional assessment of a property’s condition | Used by buyers and insurers to assess risk, determine value, and set policy terms |

| Ataviatch Insurance | Unclear term; likely a misspelling of property or attestation insurance | Potential link to home coverage or specialized policies for high-value items |

| Calligraphy | Artistic handwriting used in formal or ceremonial documents | May appear in historical records, deeds, or ornamental policies to convey authenticity |

Comprehensive Guide to Home Inspection, Insurance, and Calligraphy Services

Why do insurers conduct random home inspections for policy verification?

Ensuring Accurate Risk Assessment

- Insurers rely on up-to-date and accurate information about a property to assess the level of risk involved in providing coverage. Over time, homes undergo changes such as renovations, additions, or deterioration, which can significantly affect their insurability.

- Random home inspections allow insurance companies to verify claims data against the actual condition of the property, helping them determine whether the premium charged aligns with the current risk profile.

- By physically inspecting the property, insurers can identify hazards like outdated electrical systems, structural issues, or potential fire risks that may not be disclosed in standard policy applications.

Detecting Fraud and Misrepresentation

- Fraudulent claims and inaccuracies on insurance applications—such as underreporting the presence of a swimming pool or failing to disclose previous water damage—can lead to improper coverage and financial loss for insurers.

- Random inspections serve as a deterrent to policyholders who may be tempted to misrepresent facts to secure lower premiums or file dishonest claims.

- Through surprise visits, insurers can cross-check what was reported during underwriting with the real-world state of the home, helping uncover discrepancies that may indicate intentional deception.

Compliance with Policy Terms and Conditions

- Most home insurance policies include clauses requiring the homeowner to maintain the property in good condition and to promptly report major changes.

- Random inspections help ensure that policyholders are adhering to these contractual obligations, such as keeping the roof in repair or maintaining proper security systems.

- If significant violations are found—like unpermitted construction or a severely damaged HVAC system—the insurer may require corrective action, adjust premiums, or in some cases, non-renew the policy to mitigate exposure.

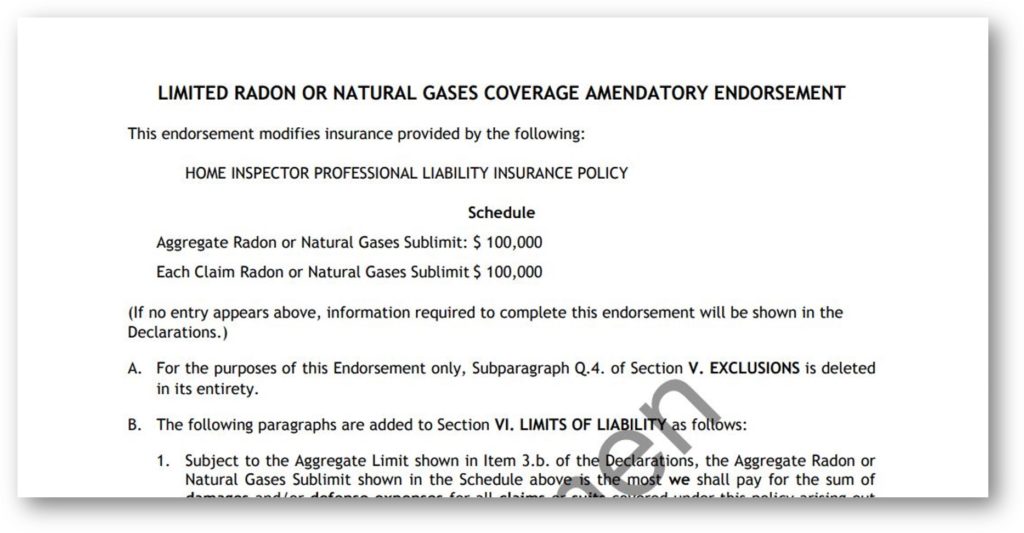

What insurance coverage is essential for a home inspector to protect against professional liabilities?

A home inspector must have specific insurance coverages to protect against professional liabilities that may arise during inspections. The most essential type of insurance is Errors and Omissions (E&O) Insurance, also known as Professional Liability Insurance.

This coverage protects inspectors if a client claims they missed a significant defect during an inspection, provided the mistake was unintentional. Without this coverage, inspectors could face substantial out-of-pocket expenses from lawsuits, even if the claim is unfounded.

In addition to E&O, General Liability Insurance and, in some cases, Workers' Compensation Insurance are also important, especially if clients visit the inspection site or if the inspector has employees. Carrying the right insurance not only safeguards the inspector’s financial stability but also enhances credibility with clients and real estate partners.

Errors and Omissions (E&O) Insurance

- Errors and Omissions Insurance is the cornerstone of professional protection for home inspectors, as it specifically covers claims related to missed defects, incorrect assessments, or inadequate reporting. For example, if a home inspector fails to identify a major structural issue that later causes damage, the client may file a claim seeking compensation—E&O insurance would help cover legal fees, settlements, or judgments.

- This type of policy typically includes defense costs, even in cases where the claim is deemed baseless, which is critical because defending a lawsuit can be financially draining. Coverage limits vary, so inspectors should carefully assess their risk exposure and choose limits that match the average home values in their service area.

- It’s also important to note that E&O policies are usually claims-made, meaning coverage is based on when the claim is filed, not when the inspection occurred. Inspectors changing providers or retiring should consider tail coverage to protect against future claims related to past work.

General Liability Insurance

- General Liability Insurance protects home inspectors from third-party claims involving bodily injury or property damage that may occur during an inspection. For instance, if a client trips over equipment left in a hallway or if a window is accidentally damaged while testing, this policy would cover medical expenses or repair costs.

- This coverage is essential even for independent contractors who work alone, as accidents can happen despite best practices. The policy may also cover personal and advertising injury, such as defamation claims that could arise from written inspection reports.

- Many real estate agencies and clients require proof of General Liability Insurance before hiring an inspector. Having it not only fulfills contractual obligations but also demonstrates professionalism and due diligence in risk management.

Workers’ Compensation Insurance

- Workers’ Compensation Insurance becomes necessary if a home inspector has employees or hires subcontractors in certain states where it is legally mandated. This coverage provides medical benefits and wage replacement to employees who suffer work-related injuries or illnesses, such as slips on rooftops or exposure to mold during inspections.

- Even in states where it's not legally required for small teams or sole proprietors, obtaining workers’ comp can be a strategic decision to avoid high medical costs and potential lawsuits from injured workers. Without it, the business owner would be personally liable for such expenses.

- Some inspection firms operate with assistants or part-time staff, making this insurance critical for comprehensive protection. It also helps maintain business continuity by ensuring that injured employees receive prompt care and return-to-work support.

Is a home inspection necessary to obtain homeowners insurance?

No, a home inspection is not typically required to obtain homeowners insurance. Most insurance companies do not mandate a formal home inspection before issuing a policy.

Instead, they often rely on their own assessment methods, such as data from property records, aerial imagery, and drive-by evaluations. However, insurers may request specific details about the condition of the home, especially regarding the roof, electrical system, plumbing, and HVAC systems.

In some cases, particularly for older homes, properties in high-risk areas, or when applying for certain types of coverage, an inspection might be requested to evaluate potential risks. Ultimately, while a pre-policy inspection is not standard, insurers retain the right to evaluate the property's condition as part of their underwriting process.

When Might an Insurance Company Request a Home Inspection?

- An insurance company may request a home inspection if the property is older, typically over 30 to 40 years, to assess the condition of major systems like the roof, plumbing, and electrical wiring.

- Homes located in areas prone to natural disasters—such as flood zones, wildfire-prone regions, or hurricane-affected coastlines—might trigger a more detailed evaluation to gauge risk exposure.

- If a home has had previous insurance claims, lapses in coverage, or known structural issues, the insurer might require an inspection to confirm that repairs have been made and the property is insurable.

- The findings from a home inspection can directly influence the cost of premiums; for example, a newer roof or updated electrical system may qualify the homeowner for lower rates due to reduced risk.

- If an inspection reveals safety hazards such as faulty wiring, outdated plumbing, or structural damage, the insurer may require corrective actions before issuing or renewing a policy.

- In some cases, significant issues uncovered during an inspection could lead to coverage limitations, higher deductibles, or even denial of coverage until repairs are completed.

Can a Voluntary Home Inspection Benefit the Homeowner?

- Conducting a voluntary home inspection before applying for insurance can help homeowners identify and fix potential issues proactively, improving insurability and possibly reducing premiums.

- Having a recent inspection report can speed up the underwriting process, as it provides insurers with detailed, reliable information about the home’s condition.

- A thorough inspection can also uncover hidden problems that could lead to future claims, allowing homeowners to address them early and avoid costly damages down the line.

Frequently Asked Questions

What is a home inspection and why is it important?

A home inspection is a thorough evaluation of a property’s condition, covering systems like plumbing, electrical, and structural integrity. It's important because it helps buyers identify potential issues before purchasing, avoiding costly repairs. Sellers also benefit by addressing problems early. A professional inspection provides peace of mind and strengthens negotiation power, ensuring transparency and informed decision-making in real estate transactions.

How does home insurance differ from a home inspection?

A home inspection assesses a property’s physical condition, while home insurance provides financial protection against damages or losses. Inspections help identify risks, which can influence insurance coverage and premiums. Insurance policies cover events like fires or theft, whereas inspections highlight existing or potential issues. Both are essential: inspections inform buyers, and insurance safeguards owners after purchase, ensuring long-term security and compliance with lender requirements.

When should I schedule a home inspection during the buying process?

Schedule a home inspection after your offer is accepted but before closing. This timing allows you to uncover issues while still having room to negotiate repairs, price reductions, or even cancel the contract if major problems arise. Most real estate contracts include an inspection contingency, giving buyers this window. Prompt scheduling ensures enough time for follow-up evaluations or repairs, helping avoid delays and ensuring you make a confident, informed purchase decision.

Can calligraphy play a role in home inspection or insurance documents?

Calligraphy is not typically involved in home inspection or insurance processes, as these rely on standardized digital or printed documentation for clarity and legal validity. However, calligraphy may be used decoratively for certificates, commemorative deeds, or personalized home records. While beautiful, it doesn’t impact the technical or legal aspects of inspections or policies. Official documents require legibility and compliance, so professional formatting takes precedence over artistic writing styles.

Leave a Reply