Insurance Life Whole

Whole life insurance is a permanent form of coverage designed to provide financial protection for a policyholder’s entire lifetime, as long as premiums are paid.

Unlike term life insurance, which expires after a set period, whole life policies accumulate cash value over time, offering both a death benefit and a savings component. This type of insurance appeals to individuals seeking long-term security and estate planning solutions.

Premiums are typically fixed, allowing for predictable budgeting, while the cash value grows at a guaranteed rate. Whole life insurance can also serve as a tool for wealth transfer, legacy creation, and supplemental retirement income.

What Is An Illustration In Life Insurance

What Is An Illustration In Life InsuranceUnderstanding Whole Life Insurance: A Comprehensive Approach to Lifelong Coverage

Whole life insurance is a type of permanent life insurance that provides coverage for the entire lifetime of the insured, as long as premiums are paid. Unlike term life insurance, which offers protection for a specified period, whole life combines a death benefit with a savings component known as the cash value. This cash value grows at a guaranteed rate over time and can be accessed by the policyholder through loans or withdrawals, offering financial flexibility.

Premiums for whole life policies are typically higher than those for term policies, but they remain level throughout the life of the policy, making long-term planning more predictable. This form of insurance is often used not only to provide for beneficiaries upon death but also as a tool for estate planning, tax-deferred growth, and even supplemental retirement income.

How Whole Life Insurance Builds Cash Value

One of the defining features of whole life insurance is its ability to accumulate cash value over time. A portion of each premium payment is allocated to this savings element, which grows at a guaranteed interest rate set by the insurance company. The cash value increases steadily and is shielded from taxation as long as it is not withdrawn beyond the amount of premiums paid.

Policyholders can borrow against this cash value, and such loans typically do not affect the death benefit unless the loan is outstanding at the time of death. This financial feature makes whole life insurance appealing to individuals seeking not only protection but also a long-term wealth-building mechanism within an insurance framework.

When Must Insurable Interest Exist For Life Insurance

When Must Insurable Interest Exist For Life InsuranceWhole life insurance ensures that beneficiaries receive a death benefit regardless of when the policyholder passes away, provided premiums are maintained.

This permanence offers peace of mind, particularly for families planning to cover final expenses, debts, or to leave a financial legacy. Additionally, premiums are level and fixed for the life of the policy, protecting the policyholder from future increases due to aging or health changes.

This predictability stands in stark contrast to term insurance, which may require renewal at significantly higher rates after the term expires. For individuals seeking stability and long-term security, the lifelong coverage and consistent cost structure of whole life insurance present compelling advantages.

Whole Life Insurance in Financial and Estate Planning

Whole life insurance plays a strategic role in comprehensive financial planning, particularly in areas like estate preservation and wealth transfer. The death benefit is generally paid out tax-free to beneficiaries, making it an efficient way to pass on assets without triggering immediate tax liabilities.

Whole Term Life Insurance Rates

Whole Term Life Insurance RatesHigh-net-worth individuals often use whole life policies to cover estate taxes, ensuring that heirs receive the full value of inherited assets. Moreover, the policy's cash value can serve as a collateral source for loans or be used to fund other financial goals. When integrated properly into a broader financial strategy, whole life insurance becomes more than insurance—it functions as a versatile financial asset.

| Feature | Description | Benefit to Policyholder |

|---|---|---|

| Death Benefit | Guaranteed payout to beneficiaries upon the insured’s death. | Provides financial security for loved ones and covers final expenses. |

| Cash Value Growth | Portion of premium builds value at a guaranteed interest rate. | Offers tax-deferred savings accessible via loans or withdrawals. |

| Fixed Premiums | Level payments throughout the life of the policy. | Protects against future cost increases due to health or age. |

| Dividends (if applicable) | Some policies pay dividends based on insurer’s performance. | Can be used to reduce premiums, buy additional coverage, or taken as cash. |

| Estate Planning Tool | Used to cover estate taxes or transfer wealth efficiently. | Preserves estate value and streamlines inheritance process. |

Comprehensive Guide to Whole Life Insurance: Benefits, Costs, and Coverage Options

Cash Value Accumulation After 20 Years

After paying premiums on a whole life insurance policy for 20 years, one of the most significant outcomes is the substantial accumulation of cash value within the policy.

Whole life insurance is designed to build cash value over time, and by the 20-year mark, this component typically grows significantly due to consistent premium payments and compounded interest or dividends, depending on the policy type (participating or non-participating).

Policyholders can access this cash value through policy loans or partial withdrawals, which may affect the death benefit if not repaid. The cash value continues to grow even after premium payments end, assuming the policy remains in force.

20 Year Term Life Insurance Quote

20 Year Term Life Insurance Quote- The cash value is typically equal to or exceeds the total premiums paid by year 20, depending on policy performance and interest crediting rates.

- Policyholders may use the accumulated cash value for various financial needs, such as supplementing retirement income or covering unexpected expenses.

- Any outstanding loans against the cash value will reduce the death benefit paid to beneficiaries upon the insured's passing.

Premium Payment Status and Policy Maturity

By the 20-year mark, many whole life insurance policies reach a stage where premium payments are no longer required, especially if the policy was structured as a paid-up policy at that duration.

Some whole life policies are designed to be fully paid after a set number of years (e.g., 20-pay life), meaning that after two decades of payments, the policy remains active for the rest of the insured's life without further premiums.

This provides long-term financial security and peace of mind, as the death benefit is guaranteed as long as the policy was properly maintained. It's important to verify the specific terms of the policy, as not all whole life plans cease premium requirements at exactly 20 years.

- 20-pay life policies are structured specifically to end premium obligations after 20 years while maintaining lifelong coverage.

- Policyholders should review their contract to confirm if premiums are truly finished or if additional payments are required beyond year 20.

- Even without premium payments, the policy continues to earn interest or dividends and remains eligible for the full death benefit.

Death Benefit and Policy Performance at Year 20

After 20 years of premium payments, the death benefit of a whole life insurance policy remains guaranteed, provided all required premiums have been paid and no loans or withdrawals have diminished it. The death benefit may also increase over time if the policy earns dividends (in the case of participating policies), which are often used to purchase additional paid-up insurance.

At this stage, the policy is mature in terms of financial structure, with both cash value and death benefit reflecting decades of consistent funding. Beneficiaries will receive the death benefit when the insured passes away, minus any outstanding policy loans.

- The death benefit is typically guaranteed and level, though it may be higher if dividends were used to purchase extra coverage.

- Insurance companies continue to back the death benefit with conservative investments, ensuring long-term stability.

- Policyholders can review annual statements to track the current death benefit amount, cash value, and any dividend allocations.

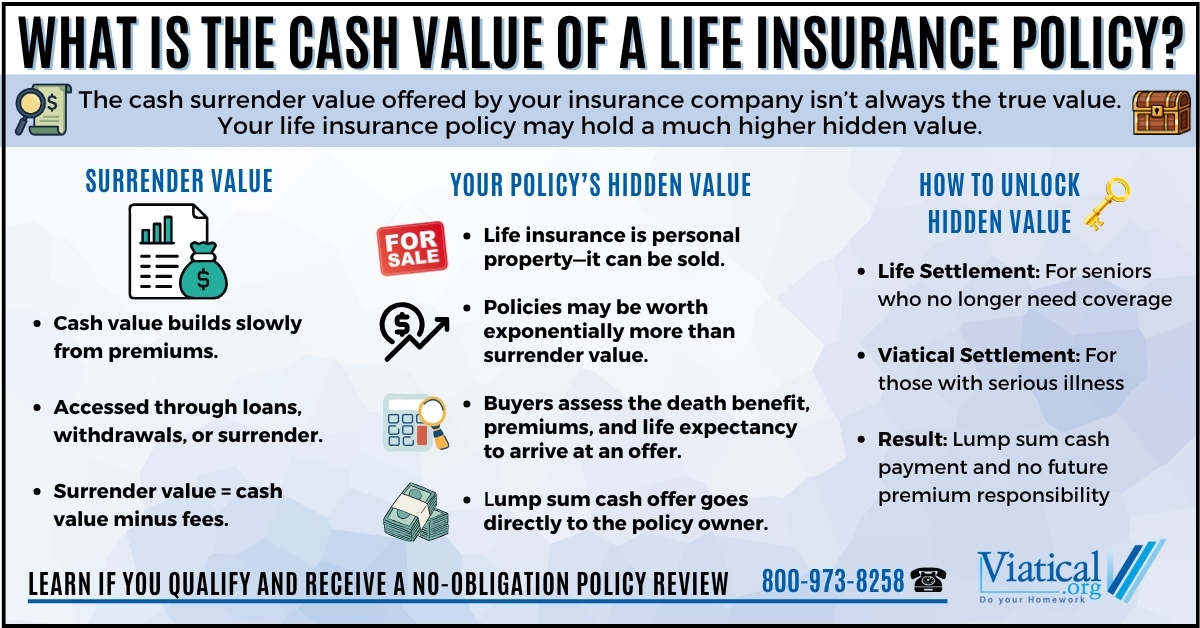

What is the cash surrender value of a $100,000 whole life insurance policy?

The cash surrender value of a $100,000 whole life insurance policy refers to the amount of money the policyholder receives if they choose to terminate the policy before the death of the insured. This value is not fixed and accumulates over time as a portion of the premiums paid is allocated to a savings or investment component within the policy. In the early years, the cash surrender value is typically low because significant portions of the premiums go toward administrative fees, agent commissions, and the cost of insurance.

As the policy matures, usually over a period of 10 to 20 years, the cash value grows due to interest or dividends credited by the insurer. The exact amount depends on the specific terms of the policy, including the premium structure, interest rate, and how long the policy has been in force. For example, after 10 years, a $100,000 whole life policy might have a cash surrender value ranging from $10,000 to $25,000, though actual values vary widely by insurer and policy details.

Factors That Influence Cash Surrender Value

- The length of time the policy has been active plays a major role, as cash value accumulates slowly in the initial years and grows more significantly in later years due to compound interest or dividend reinvestment.

- The premium payment structure, whether it’s a level-premium policy or one with front-loaded premiums, affects how much is available in cash value, with some policies building value faster depending on design.

- Additional riders, such as paid-up additions or dividend options, can accelerate the growth of the cash surrender value by increasing the policy’s internal savings component over time.

Differences Between Face Value and Cash Surrender Value

- The face value, or death benefit, is the amount paid to beneficiaries upon the death of the insured, which in this case is $100,000, and it remains relatively stable throughout the policy term.

- The cash surrender value is entirely separate and represents the accessible portion of the policy while the insured is still alive, and it is typically much lower than the death benefit, especially in early years.

- It is possible for the cash surrender value to increase over time and potentially reach a substantial percentage of the face value in older policies, though it rarely equals the full $100,000 unless specific premium payment arrangements like extended no-lapse guarantees or high cash value riders are in place.

How to Access and Calculate Cash Surrender Value

- Policyholders can determine their cash surrender value by reviewing the annual policy statement provided by the insurer, which outlines the current cash value, accumulated interest, and any surrender charges that may apply.

- To access the funds, the policyholder must formally request a surrender, which terminates the policy and results in a payout of the cash surrender value minus any outstanding loans, fees, or surrender charges.

- Insurance companies use actuarial models to calculate this value, factoring in premiums paid, time elapsed, interest credited, and costs of insurance; online calculators or direct consultation with an agent can provide more precise estimates based on individual policy details.

Frequently Asked Questions

What is Whole Life Insurance?

Whole life insurance is a type of permanent life insurance that provides coverage for the insured’s entire lifetime, as long as premiums are paid. It includes a death benefit and accumulates cash value over time, which grows at a guaranteed rate. Policyholders can borrow against the cash value or withdraw funds under certain conditions. Premiums are typically fixed, offering predictability and long-term financial protection for beneficiaries.

How does the cash value in Whole Life Insurance work?

The cash value in whole life insurance grows at a guaranteed rate over time and is funded by a portion of your premium payments. It accumulates tax-deferred and can be accessed through policy loans or withdrawals. Any unpaid loans may reduce the death benefit. The cash value can also be used to pay premiums or left to grow. It offers a financial resource during your lifetime while maintaining lifelong death benefit protection for your beneficiaries.

Yes, whole life insurance premiums are fixed and remain the same throughout the policyholder’s life. This provides long-term predictability and protection against rising costs due to age or health changes. The initial premium is based on your age, health, and coverage amount at the time of purchase. As long as premiums are paid as agreed, the coverage remains in force for life, offering stability and peace of mind for future financial planning and beneficiary protection.

Can I borrow money from my Whole Life Insurance policy?

Yes, you can borrow money from the cash value of your whole life insurance policy. These loans typically accrue interest, and unpaid balances may reduce the death benefit. Loans are not subject to credit checks since you’re borrowing against your own policy. While it provides financial flexibility, it’s important to manage loans carefully to avoid diminishing the policy’s value and benefits for your beneficiaries in the long term.

Leave a Reply