Home improvement insurance quote

Home improvement projects can significantly enhance the value and comfort of your property, but they also come with risks that homeowners often overlook.

From minor renovations to major overhauls, unexpected accidents or damages can occur at any stage. This is where home improvement insurance becomes essential. A proper insurance quote helps safeguard your investment by covering potential liabilities, property damage, or injuries during construction.

Comparing quotes allows you to find affordable coverage tailored to your project’s scope. Understanding what your policy includes ensures peace of mind while transforming your living space.

Permenent Life Insurance

Permenent Life InsuranceUnderstanding Home Improvement Insurance Quotes: What You Need to Know

When undertaking home improvement projects, securing the right insurance coverage is essential to protect your investment and avoid unexpected liabilities. A home improvement insurance quote provides an estimate of how much it will cost to extend or modify your current homeowner’s insurance policy—or obtain separate coverage—during renovations.

These quotes vary based on the scope of the project, materials used, contractor credentials, and whether the work is DIY or professionally managed. Some improvements, like adding a new bathroom or upgrading electrical systems, may increase your home’s value and therefore require higher coverage limits.

Conversely, failing to notify your insurer about major renovations could result in denied claims in the event of damage or injury. By obtaining accurate quotes early in the planning process, homeowners can budget effectively and ensure continuous protection before, during, and after construction.

What Factors Influence a Home Improvement Insurance Quote?

Several key variables affect the price and terms of a home improvement insurance quote. The size and nature of the renovation—whether it's a kitchen remodel, roof replacement, or basement finishing—play a major role, as larger projects generally involve greater risk.

Term Life Insurance And

Term Life Insurance AndThe location of your home is also considered due to regional differences in labor costs, weather risks, and local building codes. Insurers evaluate whether licensed contractors are being used, as professional work is seen as lower risk. Additionally, the duration of the project can influence premiums since long-term construction increases exposure to theft, vandalism, or accidents.

Materials matter too: high-end finishes or rare components may raise replacement values, thus increasing insured amounts. By understanding these factors, homeowners can provide accurate information to insurers and receive more precise and competitive quotes.

How to Obtain a Reliable Home Improvement Insurance Quote

To get an accurate and dependable home improvement insurance quote, start by gathering detailed project information such as construction plans, contractor licenses, and estimated timelines.

Contact your current homeowner’s insurance provider to determine if your existing policy can be temporarily adjusted to include renovation risks or if you need a separate builder’s risk policy. It’s wise to consult multiple insurers or work with an independent insurance agent who can compare offerings across different companies.

Evaluate The Insurance Company Guardian Life On Absence Management Solutions

Evaluate The Insurance Company Guardian Life On Absence Management SolutionsBe transparent about the project scope and costs to prevent coverage gaps. Always request written quotes that clearly outline coverage limits, exclusions, and liability protections, so you can make informed decisions. Verifying that contractors carry their own liability and workers’ compensation insurance is also critical, as it can impact your own policy requirements and overall risk.

Common Coverage Options Included in Home Improvement Quotes

A comprehensive home improvement insurance quote may include several types of protection tailored to construction-related risks. Builder’s risk insurance is often included, covering damage to materials or partially completed work from fire, storms, or theft during construction.

General liability insurance protects against third-party injuries or property damage caused by the renovation work—crucial even for weekend DIYers. Some policies extend to equipment and tool coverage, safeguarding expensive tools from loss or damage.

If you’re living on-site during renovations, your standard homeowner’s policy might be temporarily enhanced to cover displaced living expenses in case of uninhabitability. Additionally, umbrella policies can provide extra liability protection beyond base limits. Reviewing these inclusions carefully ensures you aren’t over- or under-insured.

Indexed Universal Life Insurance Lawyer Columbia

Indexed Universal Life Insurance Lawyer Columbia| Coverage Type | What It Protects | Why It’s Important |

|---|---|---|

| Builder’s Risk Insurance | Materials, structures under construction | Prevents financial loss from fire, weather damage, or theft during renovations |

| General Liability Insurance | Third-party injuries or property damage | Covers medical expenses or legal fees if someone gets hurt on your property |

| Contractor’s Insurance Verification | Proof of contractor coverage | Protects you from liability if the contractor lacks workers’ compensation or liability policies |

| Temporary Living Expenses | Alternate housing during major renovations | Helps cover hotel or rental costs if your home becomes unlivable |

| Equipment and Tool Coverage | Tools, machinery used in the project | Reimburses for lost, stolen, or damaged tools on-site |

How to Get an Accurate Home Improvement Insurance Quote: A Comprehensive Guide

What factors influence the cost of a home improvement insurance quote?

The cost of a home improvement insurance quote is influenced by a variety of factors that insurers evaluate to assess risk and determine coverage pricing. These factors range from the characteristics of the property and the scope of the planned improvements to the builder’s qualifications and location-specific risks. Understanding these elements can help homeowners anticipate costs and secure more accurate quotes.

- The age and condition of the home significantly affect insurance quotes. Older homes may require more extensive upgrades and are often associated with outdated electrical, plumbing, or roofing systems, increasing the perceived risk for insurers.

- The construction materials used in the property also play a role. Homes built with fire-resistant or durable materials like brick or concrete may receive more favorable rates compared to those made of wood, which is more vulnerable to fire and storm damage.

- Additionally, the size of the property and the square footage involved in the improvements are considered. Larger renovation projects typically require more coverage due to the increased value at risk during construction.

Scope and Type of Renovation

- The nature of the planned work—whether it’s a kitchen remodel, bathroom renovation, or structural addition—impacts the insurance cost. Projects that involve structural changes or affect load-bearing elements are generally seen as higher risk.

- Higher-value renovations, such as adding a swimming pool or a second story, increase the overall insured value of the property and require greater liability and property damage coverage.

- Temporary occupancy status during renovations also matters. If the home will be vacant or partially occupied during construction, insurers may charge more due to increased vulnerability to theft, vandalism, or accidents.

Contractor Credentials and Safety Measures

- Whether a licensed, insured contractor is performing the work is a major factor. Insurers prefer working with licensed professionals who carry their own liability and workers' compensation insurance, as this reduces the homeowner’s exposure to claims.

- The contractor’s track record, including their safety protocols and past claims history, may influence the quote. A contractor with a history of accidents or unfinished projects can make the job appear riskier.

- Security measures on the construction site, such as fencing, lockable storage for tools and materials, and surveillance systems, can mitigate risk and potentially lower insurance premiums by demonstrating proactive hazard control.

What type of insurance is required for home improvement projects?

General Liability Insurance for Home Improvement Projects

- General liability insurance is one of the most essential types of coverage for home improvement projects, particularly when hiring contractors or working on properties where third-party injuries or property damage could occur. This insurance helps cover medical expenses if a worker or visitor is injured on the job site, as well as any damage caused to a client’s home during renovations, such as accidental wall damage or broken fixtures.

- The policy typically covers legal defense costs if the homeowner or contractor is sued due to an accident or oversight during the project. It does not, however, cover injury to the worker themselves—that would fall under workers' compensation insurance. For homeowners, verifying that their contractor carries general liability insurance is a crucial step in protecting their own financial interests.

- For long-term projects involving multiple trades or high-risk elements like demolition or electrical work, general liability insurance provides a safety net that can prevent costly out-of-pocket expenses. It is also commonly required by building permit offices, homeowner associations, or project management companies before work can legally begin.

Workers' Compensation Insurance for Contracted Labor

- When a home improvement project involves multiple workers or hired laborers, workers' compensation insurance becomes a critical requirement. This type of insurance covers medical care, rehabilitation costs, and lost wages for workers who suffer job-related injuries or illnesses. It protects both the worker and the homeowner by ensuring that workplace accidents do not result in damaging legal or financial liability for the property owner.

- Without workers' compensation coverage, a homeowner could be held responsible for an injured worker’s medical bills, especially if the contractor does not carry their own policy. Most reputable contractors will provide proof of workers' comp coverage, and homeowners should always request documentation such as a certificate of insurance before work commences.

- In many states, contractors are legally required to carry workers' compensation insurance if they have employees. Projects involving tasks like roofing, heavy lifting, or excavation increase the risk of injury, making this insurance even more vital. Failing to verify its presence can lead to significant legal exposure for the homeowner.

Builder's Risk Insurance for Major Renovations

- Builder's risk insurance, also known as course of construction insurance, is designed specifically for home improvement projects that involve substantial structural changes, such as additions, kitchen remodels, or full-home overhauls. This policy protects the building structure and materials from damage caused by events like fire, storms, theft, or vandalism during the construction phase.

- Unlike standard homeowners insurance, which may not cover damages that occur during active renovations, builder's risk insurance fills that gap by providing temporary coverage for the duration of the project. It is usually purchased by the property owner or the general contractor and is often required by lenders financing the renovation work.

- The policy typically covers materials stored on site, partially completed work, and temporary structures. It remains in effect until the project is complete and the home is occupied again. For large-scale improvements, especially those lasting several months, builder's risk insurance is a prudent investment to prevent financial loss from unforeseen incidents during construction.

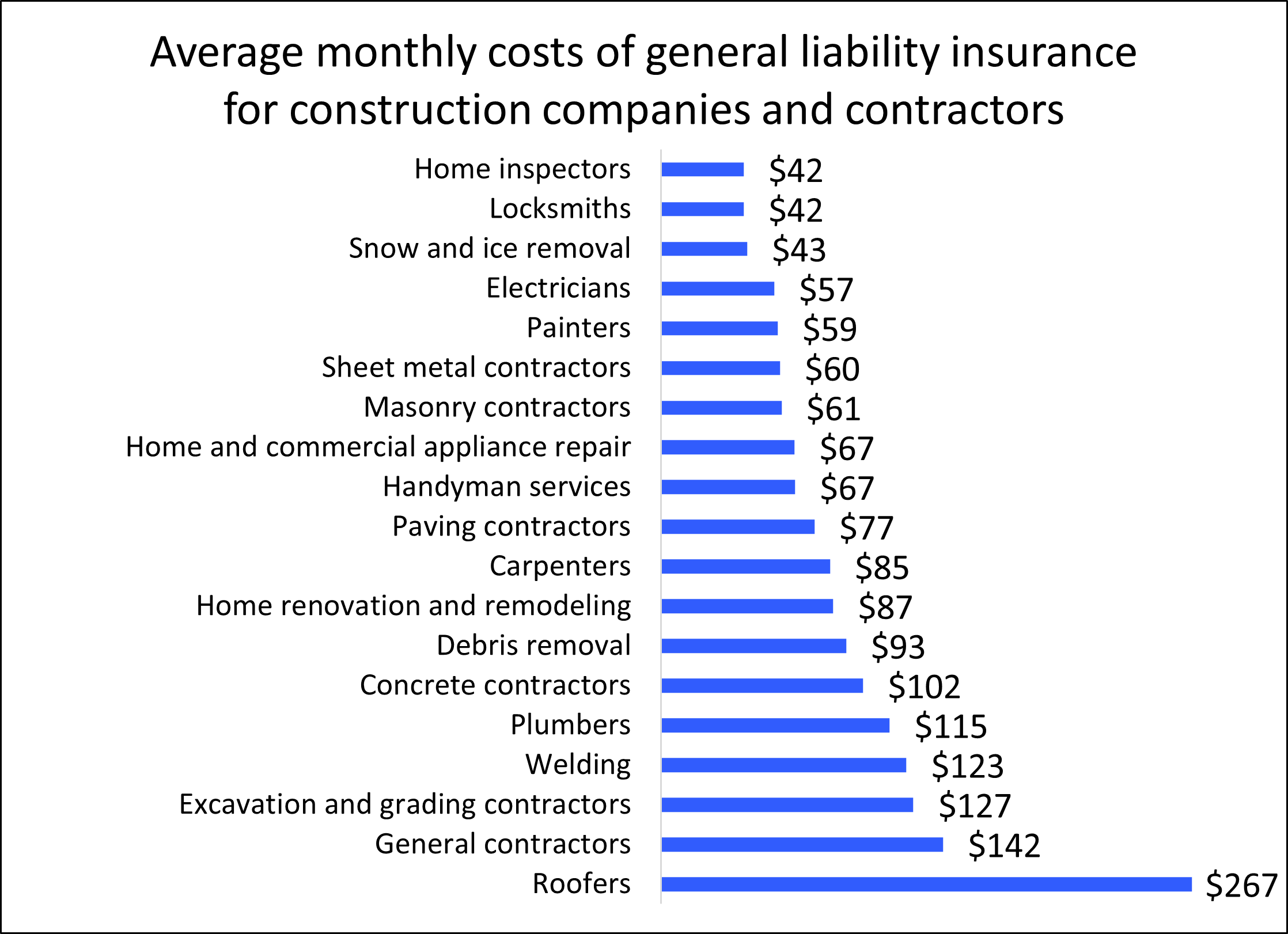

How much does $1,000,000 general liability insurance cost for home improvement contractors?

Factors That Influence the Cost of $1,000,000 General Liability Insurance for Home Improvement Contractors

- The specific type of work performed plays a major role in determining insurance premiums. Contractors involved in high-risk tasks such as roofing, electrical work, or structural remodeling typically face higher rates due to the increased likelihood of accidents and property damage.

- Location is another critical factor; contractors operating in urban areas or regions with high litigation rates may pay more for coverage compared to those in rural or low-risk zones. Local regulations, cost of living, and weather-related risks can also impact pricing.

- The contractor’s experience level, claims history, and the number of employees also influence cost. Businesses with a clean claims record, proper training, and safety protocols in place often receive lower premiums, as they are viewed as lower risk by insurers.

- On average, home improvement contractors can expect to pay between $500 and $2,000 per year for a $1,000,000 general liability insurance policy. The exact amount depends on the scope of services, business size, and geographic region.

- Independent contractors or small operations with limited exposure may pay closer to the lower end of the range, especially if they work on minor remodeling or cosmetic upgrades rather than structural changes.

- Larger firms with multiple employees, specialized equipment, and frequent job site activity will likely face higher premiums, potentially exceeding $2,000 annually, particularly if they perform inherently risky tasks such as demolition or heavy renovation.

How to Reduce the Cost of General Liability Insurance

- Maintaining a strong safety record and implementing formal workplace safety programs can lead to premium discounts. Insurers often reward contractors who proactively reduce job site hazards and employee injuries.

- Combining general liability insurance with other policies such as workers’ compensation or commercial auto insurance into a Business Owner’s Policy (BOP) can yield substantial savings through bundling discounts.

- Shopping around and comparing quotes from multiple insurers allows contractors to find the most competitive rates. Independent insurance agents can provide access to various carriers and help identify cost-effective coverage options tailored to the contractor’s specific needs.

Frequently Asked Questions

What is a home improvement insurance quote?

A home improvement insurance quote estimates the cost of coverage for renovations or upgrades to your home. It protects against potential damages, accidents, or liabilities during the project. This quote considers the scope, materials, and labor involved. It helps homeowners plan their budget while ensuring they’re protected from risks like property damage or worker injuries during the improvement process.

Why do I need insurance for home improvements?

You need insurance for home improvements to protect against accidents, property damage, and liability during construction. Standard homeowners insurance may not cover all renovation risks. Without proper coverage, you could face expensive repairs or legal claims. A dedicated home improvement insurance policy ensures you're financially protected if something goes wrong, giving you peace of mind while work is being done on your property.

How is a home improvement insurance quote calculated?

A home improvement insurance quote is calculated based on project size, materials used, labor costs, and location. Insurers also consider contractor credentials, project duration, and risk level. High-value renovations or those involving structural changes usually cost more to insure. Providing accurate details ensures you receive a fair and appropriate quote that fully covers potential risks associated with your specific home improvement project.

Can I add home improvement coverage to my existing homeowners policy?

Yes, in some cases you can add home improvement coverage to your existing homeowners policy through a rider or endorsement. However, major renovations may require a separate policy. Check with your insurer to understand your options. Temporary coverage during construction might also be recommended. Always update your policy to reflect new improvements, ensuring your home remains adequately protected both during and after the project.

Leave a Reply