Individual Health Insurance In India

Health insurance in India has become increasingly essential as medical costs continue to rise and healthcare demands grow more complex.

With a vast and diverse population, the Indian healthcare system faces challenges in accessibility and affordability, making individual health insurance a crucial safeguard. Unlike group plans tied to employment, individual health insurance offers personalized coverage, allowing people to choose plans that best fit their specific medical needs and financial capabilities.

As awareness increases and digital platforms simplify enrollment, more Indians are opting for private coverage. This article explores the landscape of individual health insurance in India, examining benefits, key considerations, popular providers, and the evolving role of insurance in achieving long-term health security.

Great Rates Auto Insurance

Great Rates Auto InsuranceUnderstanding Individual Health Insurance in India

Individual health insurance in India refers to a medical coverage plan designed to protect a single person against financial losses due to hospitalization, illness, or medical emergencies.

Unlike family floater policies, individual health insurance covers only one person, making premium calculations more personalized based on age, medical history, and lifestyle. With rising healthcare costs and increasing prevalence of lifestyle diseases, individual health insurance has become a critical tool for managing out-of-pocket medical expenses.

These policies typically include coverage for hospitalization, pre- and post-hospitalization expenses, day-care procedures, and ambulance charges, with optional riders for enhanced protection. Choosing the right individual health plan in India allows for greater control over coverage limits, claim histories, and renewal terms without being impacted by the medical claims of family members.

Benefits of Opting for Individual Health Insurance

One of the primary advantages of individual health insurance in India is the customization it offers to policyholders.

Gto Auto Insurance And Multi Services

Gto Auto Insurance And Multi ServicesEach policy is tailored to the specific health profile, age, and financial capacity of the individual, allowing for more accurate premium pricing. Since claims made by one person do not affect others, maintaining a claim-free record can lead to benefits like no-claim bonus (NCB) accumulation and lower future premiums.

Additionally, individuals have the freedom to choose higher sum insured amounts, add relevant riders such as critical illness or personal accident cover, and switch providers at renewal without affecting family members’ coverage. This autonomy makes individual health plans ideal for young professionals, single adults, or senior citizens seeking focused medical protection.

Key Factors to Consider Before Buying a Policy

When selecting an individual health insurance plan in India, several critical factors should guide the decision-making process.

The sum insured should be adequate to cover potential medical expenses in the individual’s city of residence, factoring in inflation and rising treatment costs. It's essential to evaluate the network hospitals associated with the insurer, as cashless treatment is only available at these facilities.

Guaranteed Auto Protection Insurance Market

Guaranteed Auto Protection Insurance MarketOther important considerations include the waiting period for pre-existing conditions, which may range from 2 to 4 years, co-payment clauses that require the insured to pay a portion of the claim, and the claim settlement ratio (CSR) of the insurance provider, which reflects their reliability in honoring claims. Reading the policy documents carefully ensures transparency and helps avoid surprises during claim settlements.

Top Health Insurance Providers and Plan Comparison

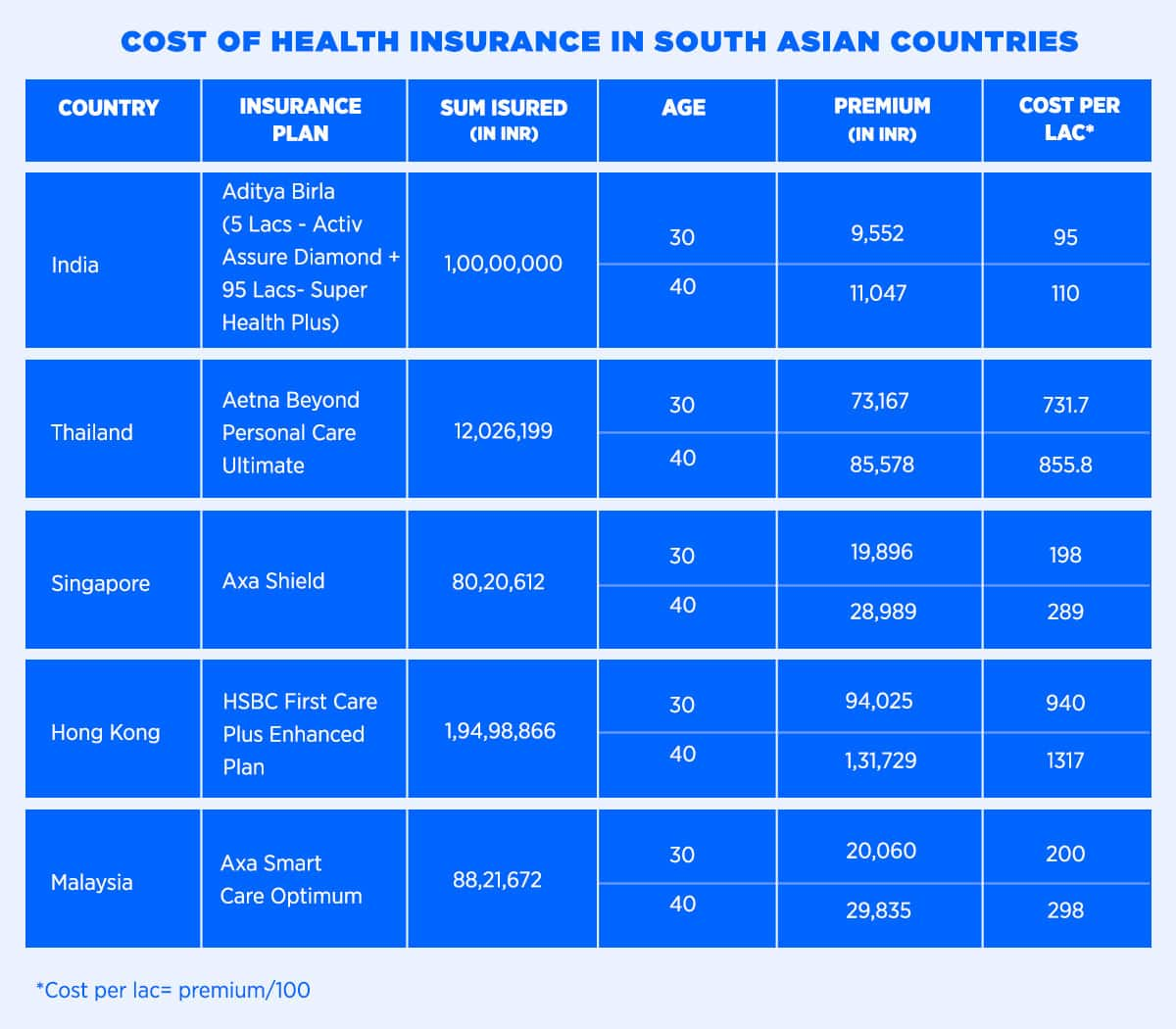

India’s health insurance market features a wide range of reputable insurers offering competitive individual health plans. Companies like HDFC ERGO, ICICI Lombard, Star Health, Max Bupa, and National Insurance provide diverse coverage options, coverage limits, and value-added services. Below is a comparison table highlighting key features of individual health insurance policies offered by leading providers:

| Insurance Provider | Starting Sum Insured | Waiting Period (Pre-Existing) | Cashless Hospitals | Claim Settlement Ratio (2023) | Notable Features |

|---|---|---|---|---|---|

| HDFC ERGO | ₹1 lakh | 4 years | 8,000+ | 98.2% | Quick claim processing, mobile app support |

| ICICI Lombard | ₹2 lakh | 3 years | 7,500+ | 96.8% | Global health coverage, maternity option |

| Star Health | ₹50,000 | 3 years | 10,000+ | 94.7% | Senior citizen-focused plans, no room rent cap |

| Max Bupa | ₹3 lakh | 4 years | 7,000+ | 95.1% | Wellness rewards, zero depreciation on implants |

| National Insurance (Public) | ₹5 lakh | 4 years | 5,500+ | 92.0% | Low premiums, government-backed reliability |

This comparison allows individuals to assess different plans based on coverage scope, hospital network accessibility, and insurer reliability, helping them select a plan that aligns best with their medical and financial needs in India.

Comprehensive Guide to Individual Health Insurance in India

What is the average cost of individual health insurance in India?

Hartford Insurance Aarp Auto Insurance

Hartford Insurance Aarp Auto InsuranceFactors Influencing the Cost of Individual Health Insurance in India

- The age of the policyholder is one of the primary determinants of health insurance premiums in India. Younger individuals typically pay lower premiums because they are statistically less likely to make claims, whereas older applicants face higher costs due to increased health risks.

- Geographic location plays a significant role, as medical costs vary across cities. Residents of metropolitan areas such as Mumbai, Delhi, and Bangalore often pay higher premiums compared to those in smaller towns or rural areas due to the higher cost of healthcare services in urban centers.

- The sum insured, or coverage amount, greatly affects the premium. Policies offering higher coverage, such as ₹5 lakh or ₹10 lakh, naturally have higher costs compared to basic plans with lower coverage, reflecting the insurer’s potential financial risk.

- For a healthy adult under 30 years of age, the annual premium for a basic health insurance plan with a sum insured of ₹5 lakh typically ranges from ₹8,000 to ₹12,000. These plans offer essential hospitalization coverage and may include critical illness riders as optional add-ons.

- For individuals between the ages of 30 and 50, the average cost increases to between ₹12,000 and ₹20,000 per year for the same coverage, depending on the insurer, inclusion of maternity benefits, and pre-existing condition coverage.

- Senior citizens (60 years and above) often face higher premiums, with annual costs ranging from ₹25,000 to ₹50,000 or more for a ₹5 lakh cover, especially if the policy includes pre-existing disease coverage and no-claim bonuses.

- Insurance riders such as critical illness cover, personal accident cover, or top-up plans can increase the base premium. For example, adding a critical illness rider that pays a lump sum on diagnosis of specified diseases may add ₹2,000 to ₹5,000 annually to the premium.

- Cashless hospitalization, day-care procedures, and AYUSH treatment coverage are common features that can influence pricing. Policies with broader inclusions usually have higher premiums but offer more comprehensive protection.

- Insurers also consider lifestyle factors such as smoking or high BMI in some cases, and applicants may be subject to medical underwriting, which can lead to higher premiums or exclusions based on health assessments.

Which individual health insurance plan offers the best coverage in India?

Top Individual Health Insurance Plans with Comprehensive Coverage in India

- One of the most highly regarded individual health insurance plans in India is offered by HDFC ERGO General Insurance through their Optima Restore policy. This plan stands out due to its unique replenishment benefit, which reinstates the sum insured for critical illnesses even if the full amount has been used, enabling continued protection within the same policy year.

- Another leading option is the ICICI Lombard Complete Health Insurance plan, known for its extensive network of over 9,000 cashless hospitals and comprehensive coverage that includes day-care treatments, organ donor expenses, and even second opinions for major surgeries.

- Aditya Birla Health Insurance’s Activ Health Platinum plan combines traditional indemnity coverage with wellness incentives, allowing policyholders to earn rewards for healthy behavior while receiving high coverage limits and lifelong renewability, making it a strong contender for best overall coverage.

Key Features That Define the Best Health Insurance Coverage

- The best individual health insurance plans typically include a high sum insured with the option to increase it over time, along with no upper age limit for renewal, ensuring long-term protection through all life stages.

- Comprehensive coverage extends beyond hospitalization to include pre- and post-hospitalization expenses (usually 60 days pre and 90 days post), ambulance charges, AYUSH treatments, and home care treatment, all of which enhance the scope of protection.

- Additional benefits such as zero depreciation on implants, no claim bonus accumulation, and coverage for critical illnesses or surgeries provide added financial security and differentiate top-tier plans from basic offerings.

Factors to Consider When Choosing the Best Individual Health Plan

- It is essential to assess your medical history, family health background, and lifestyle risks before selecting a plan, as these factors determine the level of coverage and specific benefits like maternity or dental that may be needed.

- The claim settlement ratio (CSR) of the insurer is a critical indicator of reliability; insurers like Niva Bupa and Star Health have consistently maintained high CSRs, reflecting their efficiency in processing and approving claims.

- Consider the ease of policy management through mobile apps, availability of 24/7 customer support, and the presence of a wide hospital network in your city or travel destinations to ensure seamless access to healthcare services when needed.

What is the most affordable individual health insurance plan in India?

Factors That Influence the Affordability of Individual Health Insurance in India

- Age plays a significant role in determining the premium of a health insurance plan. Younger individuals generally pay lower premiums because they are considered lower risk by insurers, making entry-level plans more affordable for people in their 20s and 30s.

- The sum insured directly impacts the cost of the policy. Plans with lower coverage amounts, such as ₹1 lakh or ₹2 lakh, tend to have lower premiums and are often marketed as budget-friendly options for individuals with minimal healthcare needs.

- Geographical location also affects pricing. Premiums can vary between metro cities and rural or semi-urban areas due to differences in healthcare costs and claim frequencies, influencing which plans are considered most affordable in different regions.

Popular Low-Cost Individual Health Insurance Plans in India

- The Arogya Sanjeevani Plan, a standardized product introduced by the Insurance Regulatory and Development Authority of India (IRDAI), is one of the most affordable options available across multiple insurers. It offers a base coverage of ₹1 lakh with defined benefits and co-payment clauses, making it accessible for low-income individuals.

- Aditya Birla Health Insurance’s Activ Health Platinum Basic plan provides essential coverage with optional add-ons and is competitively priced for young and healthy adults seeking cost-effective protection with access to a network of hospitals.

- Digit Simple Health Insurance is known for its transparent pricing and digital-first approach, offering customizable plans starting with low sum insured options. Its minimalistic structure without unnecessary frills helps keep premiums low.

Tips to Find and Maintain an Affordable Health Insurance Plan

- Compare plans across multiple insurers using online comparison portals. This allows individuals to evaluate premiums, inclusions, exclusions, and claim settlement ratios to identify the most value-driven and affordable option.

- Opting for a higher deductible can reduce the premium significantly. While this means paying more out-of-pocket during a claim, it can make the overall plan more affordable for those who anticipate infrequent medical needs.

- Maintaining a healthy lifestyle and avoiding claims in initial policy years may qualify individuals for no-claim bonuses or loyalty discounts, which can lower renewal premiums and contribute to long-term affordability.

What is the 80/20 rule in individual health insurance in India?

The 80/20 rule in individual health insurance in India refers to a regulatory guideline established by the Insurance Regulatory and Development Authority of India (IRDAI).

Auto Insurance Glass Deductible

Auto Insurance Glass DeductibleThis rule mandates that health insurance providers must spend at least 80% of the premiums collected from policyholders on actual claim settlements. The remaining 20% can be utilized for administrative costs, operational expenses, commissions, marketing, and generating profits.

If an insurer fails to meet this threshold in a given financial year, it is required to reduce its premium rates in the subsequent year to ensure greater value is passed on to customers. The primary objective of the 80/20 rule is to enhance transparency, promote fair claim practices, and ensure that policyholders receive adequate benefits for the premiums they pay.

What Does the 80/20 Rule Aim to Achieve?

- The 80/20 rule is designed to protect consumers by ensuring that a major portion of the premiums they pay goes directly toward claim settlements rather than being absorbed by overhead costs or profits.

- It encourages insurance companies to streamline their operations and focus on efficient claims processing, reducing instances of unjustified claim rejections.

- By holding insurers accountable for claim payout ratios, the rule fosters greater trust in the health insurance sector and promotes healthier competition among providers.

How Is the 80/20 Rule Enforced by IRDAI?

- IRDAI regularly monitors the claim settlement ratios and financial statements of health insurers to verify compliance with the 80% claim expenditure mandate.

- Insurers are required to submit audited financial data annually, which includes detailed breakdowns of premiums collected and claims paid.

- If an insurer spends less than 80% of collected premiums on claims, IRDAI mandates a proportional reduction in future premiums to offset the shortfall, ensuring customers benefit from excess profits.

Impact of the 80/20 Rule on Policyholders

- Policyholders benefit from increased claim approval rates, as insurers are incentivized to settle valid claims to meet the 80% payout threshold.

- The rule can lead to more affordable premiums over time, especially for insurers with high operational efficiency, as compliance may result in lower pricing.

- It empowers consumers to make informed choices by promoting transparency, allowing them to compare insurers based on actual claim settlement performance rather than marketing claims.

Frequently Asked Questions

What is individual health insurance in India?

Individual health insurance in India is a policy that provides medical coverage for a single person. It covers hospitalization costs, pre- and post-hospitalization expenses, and critical illnesses, depending on the plan. Unlike family floater plans, it's specific to one individual, allowing personalized coverage. Premiums are based on age, health, and coverage needs. It ensures financial protection against unexpected medical emergencies and can be customized with add-ons for enhanced benefits.

Why should I buy individual health insurance instead of a family plan?

You should consider individual health insurance if you want coverage tailored to your specific health needs and medical history. It prevents claims made by family members from affecting your no-claim bonus and allows higher personal coverage. Premiums are also often lower when younger. Individual plans provide better flexibility and control, especially if other family members have different health requirements or you prefer not to combine medical risks.

The premium for individual health insurance in India depends on age, medical history, sum insured, lifestyle habits (like smoking), geographical location, and chosen add-ons. Older individuals pay higher premiums due to increased health risks. Pre-existing conditions may also raise costs. Insurers evaluate these factors to assess risk. Choosing a higher deductible or a longer waiting period can help lower premiums while maintaining essential coverage.

Can I renew my individual health insurance policy for life in India?

Yes, most individual health insurance policies in India offer lifelong renewability, meaning you can continue your coverage indefinitely as long as you pay premiums on time. This ensures continued protection, even in old age. Insurers cannot deny renewal due to age or previous claims, though premiums may increase with age. Some policies also offer continuous coverage for pre-existing diseases after the waiting period, enhancing long-term security.

Leave a Reply