Buy Life Insurance For Seniors

Life insurance for seniors is an essential financial planning tool that offers peace of mind during retirement years.

As people age, protecting loved ones from unexpected expenses becomes increasingly important. Senior life insurance provides a reliable way to cover final expenses, outstanding debts, or leave a legacy for family members. Many policies are designed specifically for older adults, with flexible options and simplified underwriting processes.

Whether you're in good health or managing medical conditions, coverage is often accessible. Investing in life insurance later in life ensures dignity and financial stability for your family when it matters most.

Guardian Life Disability Insurance Lawyer

Guardian Life Disability Insurance LawyerWhy Seniors Should Consider Buying Life Insurance

Purchasing life insurance during the senior years can offer essential financial protection for loved ones and help cover final expenses such as funeral costs, outstanding debts, and medical bills.

While many people believe that life insurance is only for younger individuals, seniors can still benefit significantly from having a policy in place. Whether seeking to leave a legacy, support a charitable cause, or ensure family members aren't burdened by expenses, life insurance for seniors provides peace of mind.

Various options exist, including guaranteed issue, simplified issue, and final expense policies, which are specifically designed for older applicants who may have health concerns. These policies typically involve little or no medical underwriting, making them accessible even for those with pre-existing conditions.

Types of Life Insurance Available for Seniors

Seniors have access to several types of life insurance, each designed to meet different needs and health conditions. Term life insurance may be available to seniors in good health, offering coverage for a set period at a lower premium, though it may not be renewable into advanced age.

Guardian Life Insurance Review

Guardian Life Insurance ReviewWhole life insurance is a permanent option with fixed premiums and a cash value component, making it suitable for long-term planning. For those with health issues, guaranteed issue life insurance requires no medical exam and no health questions, though it often comes with lower death benefits and a waiting period before full coverage begins.

Simplified issue policies ask a few health questions but skip the medical exam, striking a balance between accessibility and affordability. Choosing the right type depends on health, budget, and the intended use of the death benefit.

Benefits of Life Insurance for Older Adults

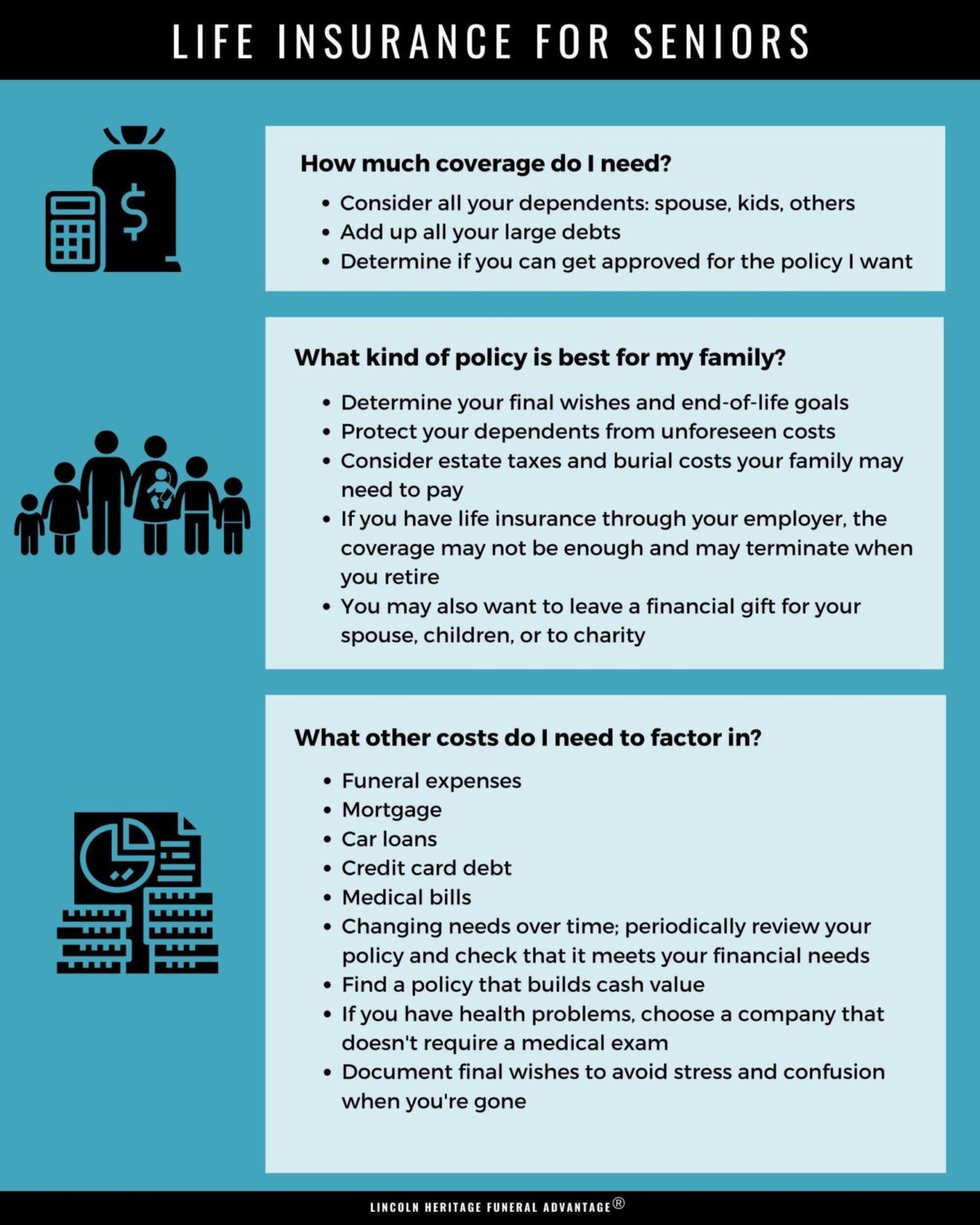

Life insurance for seniors offers multiple financial and emotional advantages. One of the most significant benefits is covering final expenses, which can average between $7,000 and $10,000, relieving family members of unexpected costs during an already difficult time.

It can also be used to pay off debts, such as credit card balances or mortgages, preventing these from becoming a burden on heirs. Some policies build cash value over time, which can be borrowed against or withdrawn in case of emergencies.

Health Conditions Impact On Life Insurance Premiums

Health Conditions Impact On Life Insurance PremiumsAdditionally, seniors can use life insurance to leave a legacy or make charitable donations, ensuring their values and intentions live on. Even on a fixed income, affordable plans like final expense insurance make coverage attainable for most older adults.

How to Choose the Right Policy at an Older Age

Selecting the appropriate life insurance as a senior requires evaluating personal health, financial goals, and budget. Start by determining how much coverage is needed—whether it's to cover funeral costs, debts, or to provide income replacement for a spouse.

Compare policies from multiple insurers to find competitive rates and favorable terms, paying special attention to waiting periods, exclusions, and premium stability. Work with a licensed insurance agent experienced in senior products to understand policy details and avoid misleading terms.

Guaranteed issue policies are ideal for those with serious health conditions, while simplified underwriting can offer better rates for relatively healthy seniors. Always read the fine print and confirm that the benefits align with your long-term objectives.

Indexed Universal Life Insurance Attorney

Indexed Universal Life Insurance Attorney| Policy Type | Best For | Medical Exam | Key Features |

|---|---|---|---|

| Guaranteed Issue | Seniors with significant health issues | No exam, no health questions | Immediate but partial coverage during waiting period (typically 2–3 years) |

| Simplified Issue | Relatively healthy seniors seeking faster approval | No exam, basic health questions | Faster underwriting, higher coverage limits than guaranteed issue |

| Final Expense Insurance | Covering funeral and burial costs | Varies (often no exam) | Low death benefit (usually $5,000–$25,000), affordable premiums |

| Whole Life | Long-term protection and cash value growth | May require exam depending on age | Lifetime coverage, fixed premiums, builds cash value |

Comprehensive Guide to Buying Life Insurance for Seniors

What is the best way to purchase life insurance for seniors online?

Compare Multiple Insurance Providers

When purchasing life insurance for seniors online, it's essential to compare multiple providers to find the most suitable and affordable policy. Different companies offer varying rates, coverage options, and underwriting standards, especially for older applicants.

Start by researching reputable insurers that specialize in senior life insurance, such as AARP, State Farm, or Mutual of Omaha. Use comparison tools on independent insurance marketplaces or broker websites to evaluate premiums, policy durations, and customer reviews. This research allows seniors to make informed decisions based on financial stability, transparency, and ease of claims processing.

- Visit independent insurance comparison websites to view side-by-side quotes from multiple companies.

- Look for insurers with strong financial ratings from agencies like AM Best or Standard & Poor’s.

- Check customer service ratings and read reviews to assess responsiveness and claims satisfaction.

Understand the Types of Life Insurance Available

Seniors have different life insurance options, and understanding these helps in selecting the right policy. The primary choices include term life, whole life, and guaranteed issue life insurance.

Term life provides coverage for a set number of years and is often more affordable, but may not be ideal for seniors over 80. Whole life insurance offers lifelong coverage with a cash value component, though premiums are higher. Guaranteed issue policies require no medical exam and are accessible even with health issues, but they come with higher premiums and graded benefits during the first few years.

- Consider term life if you need coverage for a specific period, such as to cover final expenses or debts.

- Explore whole life insurance for permanent coverage and potential cash accumulation over time.

- Opt for guaranteed issue life insurance if you have pre-existing health conditions or want a no-exam option.

Use Online Application Tools and Licensed Brokers

Leveraging online tools and professional guidance streamlines the process of buying life insurance for seniors. Many insurers provide user-friendly online quote calculators and application portals that allow seniors or their families to initiate coverage from home.

However, working with a licensed insurance broker who specializes in senior policies can offer personalized advice, clarify confusing terms, and help navigate medical underwriting. Brokers often have access to multiple carriers and can identify policies tailored to specific health or financial situations.

- Fill out online applications carefully, ensuring all health and personal information is accurate to avoid delays.

- Use secure, official insurer websites or trusted broker platforms to protect personal data.

- Contact a licensed agent via phone or video call if you need help understanding policy details or comparing offers.

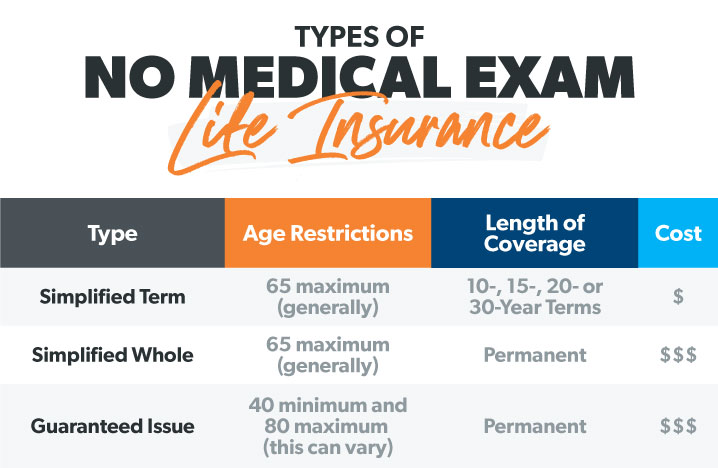

What are the best no-exam life insurance options for seniors over 60?

Top No-Exam Life Insurance Policies for Seniors Over 60

- Guaranteed Universal Life Insurance: This policy is one of the most popular no-exam options for seniors because it provides lifelong coverage with fixed premiums. Approval is based on a simplified application process with minimal health questions, making it ideal for individuals over 60 who may have existing medical conditions.

- Final Expense Insurance: Also known as burial insurance, this type of policy is specifically designed to cover funeral costs, medical bills, and other end-of-life expenses. Many providers offer no-exam versions with quick approval, and death benefits typically range from $5,000 to $25,000.

- Group Life Insurance through Associations: Some organizations, including AARP and fraternal groups, offer group life insurance plans that require no medical exam. These plans often feature simplified underwriting and can be particularly accessible for seniors seeking affordable coverage without the hassle of a physical exam.

How No-Exam Life Insurance Works for Senior Applicants

- Simplified Issue Policies: These policies require applicants to answer a few health-related questions, but no lab tests or doctor visits are needed. Insurers use this information to assess risk quickly, often approving coverage within days. This process is well-suited for seniors who want fast results without invasive procedures.

- Instant Approval and Digital Applications: Many insurers now offer fully online applications with instant decisions. Seniors over 60 can complete the process from home, uploading required documents and receiving a policy in as little as 24 to 48 hours, depending on the company and their health profile.

- Graded Benefits and Waiting Periods: Some no-exam policies include a graded death benefit, meaning full coverage is not available immediately. If the policyholder passes away during the first two or three years, beneficiaries may receive a return of premiums or a portion of the death benefit, which increases over time.

Factors to Consider When Choosing a No-Exam Policy

- Premium Costs and Affordability: Premiums for no-exam life insurance can be higher than traditional policies due to increased risk for insurers. It’s important for seniors to compare multiple quotes and consider policies that offer level premiums to avoid unexpected rate increases later.

- Coverage Limits and Policy Flexibility: Different insurers offer varying maximum death benefits for no-exam policies. Seniors should assess how much coverage they actually need and whether the policy allows for future adjustments, such as adding riders or converting to a permanent plan.

- Reputation and Financial Strength of the Insurer: Choosing a company with strong financial ratings from agencies like A.M. Best or Standard & Poor’s ensures the insurer will be able to pay claims when needed. Customer service quality and claim processing speed are also important considerations for policyholders and their families.

What is the most affordable life insurance option for seniors over 70?

The most affordable life insurance option for seniors over 70 is typically guaranteed issue whole life insurance. This type of policy requires no medical exam and does not ask health-related questions, making it accessible to those with significant health concerns.

While premiums are higher per dollar of coverage compared to other types, the ease of qualification and immediate acceptance make it a practical and cost-effective choice for many seniors. Coverage amounts are usually limited—often between $5,000 and $25,000—which helps keep premiums more affordable. These policies build cash value over time and never expire as long as premiums are paid.

What Is Guaranteed Issue Life Insurance and Why Is It Suitable for Seniors Over 70?

- Guaranteed issue life insurance is a form of whole life insurance that guarantees approval regardless of health status, which is especially beneficial for seniors over 70 who may have chronic conditions or a history of serious illnesses.

- These policies do not require a medical exam or health questionnaire, eliminating the risk of being declined based on pre-existing conditions such as heart disease, diabetes, or cancer.

- The main drawback is a waiting period—typically two to three years—during which only a portion of the death benefit is paid if the insured passes away, but after that period, full benefits are available, providing long-term financial security.

- Premiums for senior life insurance are generally higher due to increased age and mortality risk, but guaranteed issue policies offer level premiums that remain the same for life, allowing for predictable monthly budgeting.

- Coverage amounts are intentionally modest, often capped between $10,000 and $25,000, which aligns with typical end-of-life expenses like funeral costs, medical bills, or small debts, making the overall cost more manageable.

- Some insurers offer graded premiums, where costs start lower and increase slightly in the first few years before stabilizing, providing initial affordability for fixed-income retirees.

Are There Alternatives to Guaranteed Issue Policies for Healthier Seniors Over 70?

- Simplified issue life insurance is an alternative that involves answering a few health questions but still no medical exam, often resulting in lower premiums than guaranteed issue policies for applicants in relatively good health.

- Joyored life insurance, if the senior was already insured earlier in life, allows for continued coverage without needing a new medical evaluation, and may include affordable options to increase coverage.

- Group life insurance through veterans’ organizations, alumni associations, or employer retiree plans can offer competitively priced coverage with minimal underwriting, providing a cost-effective alternative for eligible seniors.

Frequently Asked Questions

What types of life insurance are available for seniors?

Seniors can choose from term life, whole life, and guaranteed issue life insurance. Term life offers coverage for a set period, while whole life provides lifelong protection with a cash value component. Guaranteed issue policies require no medical exam and are easier to qualify for, though they often have lower coverage amounts and higher premiums. Each type has pros and cons, so it’s important to evaluate individual needs, health, and budget.

Why should seniors consider buying life insurance?

Seniors buy life insurance to cover final expenses like funeral costs, medical bills, or outstanding debts, ensuring their loved ones aren’t burdened financially. It can also leave a legacy, support charitable causes, or provide liquidity to heirs. Even at an older age, life insurance offers peace of mind and financial security. Policies like final expense insurance are specifically designed to meet these end-of-life financial needs.

Do seniors need a medical exam to get life insurance?

Not always. While traditional policies may require a medical exam, many insurers offer no-exam options like guaranteed issue or simplified issue life insurance. Guaranteed issue policies accept applicants regardless of health, though they often include a waiting period and higher premiums. Simplified issue policies involve health-related questions but no physical exam. These options make coverage accessible for seniors with health concerns or those seeking convenience.

How much life insurance do seniors really need?

The right amount depends on individual goals, such as covering funeral costs, debts, or leaving a legacy. Many seniors opt for $10,000 to $25,000 in coverage, which is often sufficient for final expenses. It's important to consider outstanding bills, family needs, and future costs. A financial advisor or insurance agent can help determine an appropriate coverage amount based on personal circumstances and financial objectives.

Leave a Reply