New York Life Insurance Company Bga Imo

New York Life Insurance Company BGA IMO operates as a key intermediary in the life insurance and financial services sector, connecting independent agents with comprehensive insurance solutions.

As a Brokerage General Agency (BGA) and member of the Insurance Marketing Organization (IMO) network, it plays a vital role in distributing New York Life’s wide range of products, including term life, whole life, and retirement planning tools.

Focused on empowering financial professionals, BGA IMO provides training, support, and resources to help agents serve their clients effectively. This structure enhances market reach while maintaining the financial strength and reputation synonymous with New York Life, one of the oldest and most trusted insurers in the United States.

Guardian Life Disability Insurance Lawyer

Guardian Life Disability Insurance LawyerNew York Life Insurance Company BGA IMO: An Overview of Its Role in Independent Distribution

New York Life Insurance Company, one of the largest and most financially stable life insurers in the United States, partners with numerous independent marketing organizations (IMOs) to extend its distribution network.

One such partner is BGA (Best insurance Agency), a notable IMO that collaborates with New York Life to connect independent agents with competitive life insurance and financial products. The BGA IMO acts as a conduit, offering training, support, and access to New York Life’s portfolio, which includes term life, whole life, and universal life insurance policies.

This relationship allows independent agents who are not directly employed by New York Life to represent the company’s products, helping expand market reach while maintaining underwriting integrity and brand standards. The BGA IMO-New York Life affiliation emphasizes strategic growth, agent development, and client-focused financial protection solutions.

What Is BGA IMO and How Does It Relate to New York Life?

BGA (Best insurance Agency) is a prominent Independent Marketing Organization (IMO) that functions as a third-party distributor for various life insurance carriers, including New York Life Insurance Company.

Guardian Life Insurance Review

Guardian Life Insurance ReviewWhile BGA is not owned by New York Life, it maintains an appointed partnership that enables its network of independent agents to sell New York Life’s products. BGA provides agents with resources such as product training, sales support, compliance guidance, and commission structures, making it easier for independent advisors to represent top-tier insurers.

This affiliation benefits both parties: New York Life extends its market penetration through a broader agent base, while BGA enhances its value proposition by offering high-quality, financially sound insurance solutions from a well-established carrier. The relationship underscores the importance of strategic alliances in the insurance distribution ecosystem.

Key Benefits of the New York Life and BGA IMO Partnership

The collaboration between New York Life and the BGA IMO offers multiple advantages for agents and policyholders alike.

Agents affiliated with BGA gain access to New York Life’s A+ rated financial strength (as rated by AM Best), allowing them to offer clients one of the most trusted names in life insurance. The partnership also provides agents with competitive commission schedules, advanced underwriting support, and customized marketing materials tailored to New York Life’s product suite.

Health Conditions Impact On Life Insurance Premiums

Health Conditions Impact On Life Insurance PremiumsFor consumers, this means access to robust life insurance solutions backed by a company known for policyholder dividends, long-term stability, and customer service excellence. Moreover, BGA’s ongoing agent education initiatives ensure that representatives are well-equipped to match clients with appropriate New York Life products based on individual needs and financial goals.

Products and Services Offered Through BGA’s New York Life Platform

Through the BGA IMO platform, independent agents can offer a comprehensive array of New York Life insurance and financial products.

These include Term Life Insurance, ideal for temporary coverage needs; Whole Life Insurance, which provides lifelong protection and builds cash value; and Universal Life Insurance, offering flexibility in premiums and death benefits. In addition, New York Life’s retirement solutions, such as annuities and long-term care-integrated policies, are available through this distribution channel.

BGA supports agents in navigating these offerings with tools like illustration software, needs analysis guides, and product comparison charts. This ensures that agents can confidently present tailored financial strategies that align with clients’ objectives, whether it's income replacement, estate planning, or legacy creation.

Indexed Universal Life Insurance Attorney

Indexed Universal Life Insurance Attorney| Feature | New York Life | BGA IMO Support |

|---|---|---|

| Financial Strength Rating | A+ (AM Best) | Promoted in agent training and materials |

| Life Insurance Products | Term, Whole, Universal Life | Product training and sales scripts provided |

| Agent Commissions | Competitive and structured | Fully detailed in BGA compensation plans |

| Underwriting Support | Efficient and consultative | Access to BGA underwriting specialists |

| Training & Development | Limited direct agent training | Extensive BGA-led programs and webinars |

New York Life Insurance Company BGA IMO: A Comprehensive Guide

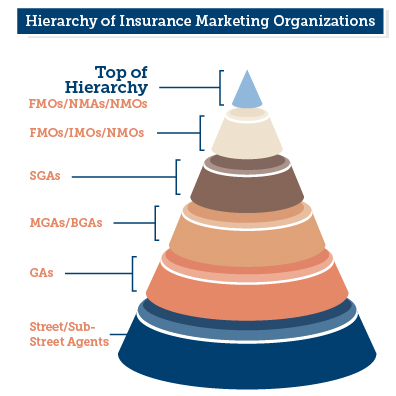

What distinguishes New York Life Insurance Company's BGA from its IMO structure?

Ownership and Operational Control Differences

- New York Life Insurance Company's Brokerage General Agency (BGA) model involves independent agencies that maintain ownership autonomy while partnering with New York Life to distribute its insurance products. These BGAs operate as third-party entities but are closely aligned with the company’s standards and training protocols, allowing them to function with a degree of independence in their operations and agent recruitment.

- In contrast, the Independent Marketing Organization (IMO) structure encompasses a broader network of producers or groups that may represent multiple insurance carriers, including but not limited to New York Life. IMOs prioritize flexibility and product variety, often acting as multi-carrier distribution channels, meaning they are not exclusively tied to New York Life and may emphasize products from competing companies based on commissions or market demand.

- The key distinction lies in the level of integration and exclusivity. BGAs typically have a preferred or exclusive relationship with New York Life, which influences their operational directives, training curriculum, and performance benchmarks, while IMOs retain full independence in carrier selection and are not bound by the same alignment requirements.

Compensation and Incentive Models

- Under the BGA structure, compensation plans are often designed in collaboration with New York Life, featuring incentives that promote long-term policy sales, agent retention, and adherence to corporate sales practices. These agencies may receive overrides, bonuses, and support resources directly from New York Life based on production volume and quality of business.

- IMOs, by comparison, usually operate on a more transactional compensation basis, where income is derived from multiple carriers. Their incentive structures are not standardized across the board and may shift depending on carrier promotions, leading to variable focus on New York Life products based on short-term profitability.

- This creates a fundamental difference in motivation: BGA leaders are more likely to foster a culture centered on New York Life’s values and product strengths, while IMO leaders may shift strategic priorities frequently based on external financial incentives from various insurers.

Training, Support, and Brand Alignment

- New York Life provides comprehensive training, sales tools, and marketing support to its BGA partners, ensuring consistent messaging and brand representation. These agencies often participate in proprietary development programs, such as leadership academies or field mentorship initiatives, designed to align agent behavior with the company’s long-term service philosophy.

- IMOs generally source training materials independently or compile resources from multiple carriers. While some IMOs may offer effective training, it lacks the uniformity and depth of New York Life's direct BGA support, leading to variability in agent preparedness and client experience.

- As a result, BGAs reflect a tighter brand integration, with agents more likely to embody New York Life’s customer-centric approach and ethical sales standards, whereas IMO agents may exhibit diverse selling styles influenced by exposure to competing carrier cultures and priorities.

What is the lawsuit involving New York Life Insurance Company and BGA IMO?

![]()

Background of the Lawsuit Between New York Life and BGA IMO

- The lawsuit involving New York Life Insurance Company and BGA IMO (Independent Marketing Organization) centers around allegations of deceptive sales practices, contract violations, and unfair competition in the distribution of life insurance policies.

- BGA, one of the largest independent marketing organizations in the U.S., reportedly entered into agreements with New York Life to recruit and train agents who would sell the insurer's products.

- Over time, tensions arose, leading BGA IMO to file a legal complaint asserting that New York Life abruptly terminated contracts with agents affiliated with BGA without proper cause, allegedly undermining contractual agreements and disrupting ongoing business relationships.

Allegations and Legal Claims in the Dispute

- BGA IMO claims that New York Life engaged in practices that interfered with agent contracts, including pressuring agents to disassociate from BGA in favor of exclusive arrangements with the insurer.

- The suit includes allegations of tortious interference with contractual relationships, breach of good faith and fair dealing, and violation of certain state business codes related to fair competition and agent rights.

- BGA is seeking financial damages for lost commissions and business opportunities, as well as injunctive relief to prevent further interference with its agent network.

Implications for the Insurance Industry and Agents

- The outcome of this lawsuit could set a precedent for how insurers interact with third-party marketing organizations and manage distribution networks.

- Agents affiliated with IMOs may face uncertainty regarding job stability and commission structures if insurers increasingly shift toward direct or exclusive hiring models.

- Industry stakeholders are closely monitoring the case as it highlights growing tension between traditional insurance carriers and independent distribution platforms over control, compensation, and contractual obligations.

Frequently Asked Questions

What is New York Life Insurance Company BGA IMO?

New York Life Insurance Company BGA IMO refers to Brokerage General Agency Independent Marketing Organizations affiliated with New York Life.

These organizations support independent agents by providing resources, training, and access to New York Life’s insurance and financial products. BGA IMOs help streamline operations for producers while maintaining independence, enabling them to serve clients effectively using New York Life’s trusted brand and product offerings.

How does a BGA IMO partner with New York Life?

A BGA IMO partners with New York Life by becoming an authorized distribution channel for its insurance and annuity products. These organizations recruit and support independent agents, offering operational support, compliance guidance, and product training.

The partnership allows agents to represent New York Life while benefiting from the BGA IMO’s administrative services, helping expand market reach and ensure high standards of service and integrity.

Can independent agents join New York Life through a BGA IMO?

Yes, independent agents can join New York Life through a BGA IMO. These organizations act as intermediaries that onboard agents, provide training, and facilitate appointments with New York Life.

Agents gain access to New York Life’s products, competitive commissions, and marketing support while retaining their independent status. The BGA IMO structure offers flexibility and support, making it easier for agents to build successful practices under the New York Life brand.

What benefits do agents gain from the New York Life BGA IMO structure?

Agents benefit from the New York Life BGA IMO structure through enhanced support, training, and administrative services. They gain access to New York Life’s strong financial products and high customer satisfaction ratings while maintaining independence.

BGA IMOs provide tools for compliance, marketing, and business development, helping agents grow their client base efficiently. This model combines the stability of a leading insurer with the flexibility of independent practice.

Leave a Reply