Auto Insurance In New York Ny

Auto insurance in New York NY is a legal requirement for all drivers, offering essential financial protection in the event of accidents, theft, or property damage. As one of the most densely populated states with heavy traffic congestion, New York enforces strict insurance regulations to ensure road safety and liability coverage.

Drivers must carry minimum liability coverage, no-fault benefits, and uninsured motorist protection. Premiums vary based on factors like driving history, vehicle type, and location. Understanding the state’s unique no-fault system and insurance mandates is crucial for compliance and maximizing coverage.

Understanding Auto Insurance Requirements and Options in New York, NY

Auto insurance in New York, NY is a legal requirement for all drivers and is governed by the state’s Financial Responsibility Law. The state operates under a “no-fault” insurance system, which means that regardless of who causes an accident, each driver’s insurance company covers their own medical expenses and lost wages up to the policy limits.

Who offers the best unoccupied home insurance in the uk

Who offers the best unoccupied home insurance in the ukIn New York, minimum coverage includes $25,000 for bodily injury per person, $50,000 for bodily injury per accident, $10,000 for property damage, and $50,000 for no-fault benefits. Drivers must also carry uninsured/underinsured motorist coverage with the same limits as bodily injury coverage. Failure to maintain valid insurance can result in fines, license suspension, and vehicle registration revocation.

Insurance premiums in New York are influenced by numerous factors such as driving history, vehicle type, location, age, and credit score. To make informed decisions, drivers are encouraged to compare quotes from multiple insurers and consider additional coverage options like collision, comprehensive, and personal injury protection.

Minimum Auto Insurance Coverage Mandates in New York

New York state law requires all drivers to carry a minimum level of auto insurance coverage to legally operate a vehicle on public roads.

The required coverages include bodily injury liability of $25,000 per person and $50,000 per accident, property damage liability of $10,000, and no-fault (personal injury protection) coverage of $50,000. These minimum liability limits ensure that drivers can cover costs associated with injuries and damages they may cause in an at-fault accident.

Wichita home insurance cost

Wichita home insurance costAdditionally, uninsured motorist coverage must match the bodily injury liability limits, providing protection if a driver is hit by an uninsured or underinsured individual. While these are the minimums, many drivers opt for higher coverage limits to better protect their assets and reduce out-of-pocket expenses after an accident.

Factors That Influence Auto Insurance Rates in NYC

Auto insurance premiums in New York City and across the state are determined by a combination of personal and external factors.

Key elements include the driver’s age, driving record, credit history, vehicle make and model, and geographic location—with urban areas like Manhattan often seeing higher rates due to increased traffic congestion and theft risk. Insurance companies also consider annual mileage and usage patterns; drivers who commute long distances or use their vehicle for rideshare purposes may face higher premiums.

The type of coverage selected, including deductible amounts and optional add-ons like rental reimbursement or roadside assistance, also impacts the final cost. Drivers can reduce their rates by maintaining a clean record, taking defensive driving courses, and bundling policies with the same insurer.

Affordable home insurance for older homes tips

Affordable home insurance for older homes tipsHow to Choose the Best Auto Insurance Provider in New York

Selecting the right auto insurance provider in New York involves evaluating not only premium costs but also customer service, claims handling, and available discounts.

Drivers should compare quotes from reputable companies such as State Farm, Geico, Progressive, and Nationwide, using online tools or working with independent insurance agents. Key factors to assess include the insurer’s financial strength rating, customer satisfaction scores, and responsiveness during the claims process.

Many insurers offer multi-policy discounts, safe driver incentives, and pay-per-mile programs that can lead to significant savings. It’s also important to verify whether the provider is licensed in New York and complies with state regulations to ensure full legal protection and support when needed.

| Coverage Type | Minimum Required Limit (NY State) | What It Covers |

|---|---|---|

| Bodily Injury Liability | $25,000 per person / $50,000 per accident | Covers medical expenses and legal fees if you injure someone in an at-fault accident. |

| Property Damage Liability | $10,000 per accident | Pays for damage your vehicle causes to another person's property, such as their car or fence. |

| No-Fault (PIP) | $50,000 per person | Covers your own medical bills, lost wages, and essential services regardless of fault. |

| Uninsured/Underinsured Motorist Coverage | $25,000 per person / $50,000 per accident | Protects you if injured by a driver with no insurance or insufficient coverage. |

Comprehensive Guide to Auto Insurance in New York, NY

What is the most affordable auto insurance option in New York, NY?

Age uk insurance home

Age uk insurance homeThe most affordable auto insurance option in New York, NY varies depending on individual factors such as driving history, vehicle type, age, and location within the city.

However, based on consumer reports and comparative studies, GEICO frequently ranks among the most budget-friendly insurers for minimum liability coverage in New York City. Their competitive pricing is often attributed to strong discounts for safe drivers, electronic policy management, and multi-vehicle bundling.

Other insurers like State Farm and Progressive also offer low rates for qualifying drivers, particularly those with clean records or who take advantage of usage-based programs such as drive-smart monitoring. It is essential to compare quotes from multiple providers since affordability can differ significantly between individuals.

Factors That Influence Auto Insurance Costs in New York

- Urban density plays a major role, as New York City’s high traffic congestion, vehicle theft rates, and frequency of claims lead to increased premiums across most providers. Drivers in Manhattan typically pay more than those in less congested areas of upstate New York.

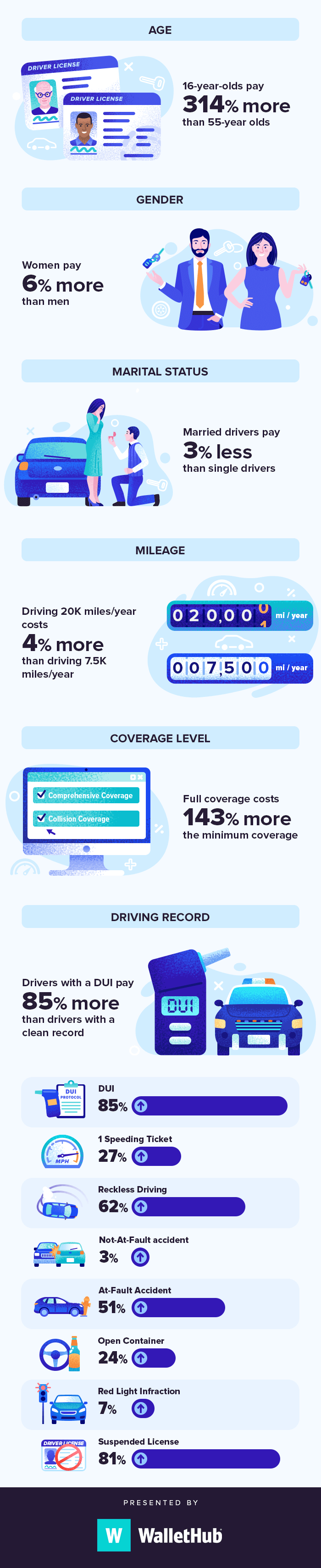

- Driving history is a critical determinant; drivers with tickets, at-fault accidents, or DUI convictions are considered higher risk and therefore face significantly higher premiums. Insurers use this data to assess the likelihood of future claims.

- Credit score is legally considered in New York when calculating premiums. Applicants with stronger credit profiles often receive lower rates, as insurers view them as more financially responsible and less likely to file claims.

Budget-Friendly Insurance Companies Operating in New York

- GEICO consistently appears as one of the most affordable options, especially for drivers seeking basic liability coverage. They offer digital tools for easy policy management and various discount programs, including military, federal employee, and good driver incentives.

- Progressive stands out through its Price Comparison Tool, which allows customers to compare Progressive's rate directly against competitors during the quote process. Their Snapshot program also rewards low-mileage and safe driving behaviors with reduced premiums over time.

- State Farm remains a top contender for affordable rates in suburban areas around New York City. While urban rates are higher, State Farm often undercuts competitors for drivers with clean histories and offers personalized service through local agents.

Ways to Reduce Auto Insurance Premiums in NYC

- Maintaining a clean driving record is one of the most effective ways to keep costs low. Avoiding traffic violations and accidents over time typically leads to lower renewal rates and eligibility for safe driver discounts.

- Opting for higher deductibles can reduce monthly premiums, though this means paying more out of pocket in the event of a claim. This strategy works best for drivers who can afford unexpected expenses and rarely file claims.

- Taking an approved defensive driving course can lead to insurance reductions of up to 10% in New York. The state permits insurers to offer this discount to drivers who complete a DMV-certified course, which also improves road safety knowledge.

What are the best auto insurance companies in New York State for 2024?

Average cost of home inspector insurance

Average cost of home inspector insuranceTop-Rated Auto Insurance Providers in New York for 2024

- Geico consistently ranks among the top choices for auto insurance in New York due to its competitive pricing, strong financial stability, and user-friendly mobile app. The company offers a range of discounts, including those for safe driving, vehicle safety features, and bundling policies, making it an appealing option for many drivers across the state.

- State Farm remains a leader in customer satisfaction, backed by its extensive network of local agents and comprehensive coverage options. In New York, State Farm stands out for its personalized service and ease of claims processing, which contributes to high retention rates and positive feedback from policyholders.

- Progressive is highly regarded for its price comparison tool, Snapshot program for usage-based pricing, and broad coverage selections. It performs exceptionally well in customer service ratings and offers tailored policies for high-risk drivers, making it a versatile and accessible insurer throughout New York State.

Factors That Influence Auto Insurance Rankings in New York

- Premium affordability is a key component in determining the best auto insurance companies. Insurers like Geico and USAA often lead in this category due to their ability to offer lower base rates, although pricing can vary significantly based on driver profile, location, and driving history within New York’s diverse regions.

- Customer service performance, as measured by surveys from J.D. Power and the Better Business Bureau, plays a crucial role. Companies with 24/7 claims support, efficient digital platforms, and high satisfaction scores—such as Amica and Nationwide—tend to rank higher in overall evaluations for the New York market.

- Claims handling efficiency, including speed of settlement and ease of filing, significantly impacts rankings. Insurers that invest in digital claims tools, offer rental car coordination, and maintain clear communication throughout the process, like Allstate and Erie Insurance, are often preferred by New York drivers who experience frequent urban congestion and higher accident rates.

Regional Considerations for New York Drivers

- In densely populated areas like New York City, insurers must navigate high traffic density, elevated theft rates, and costly repairs, leading to higher premiums. Companies that offer urban driving discounts or include robust comprehensive coverage, such as Travelers and Liberty Mutual, can provide better value in these regions.

- Upstate New York drivers often face different challenges, including winter weather conditions and longer commutes. Insurers that provide roadside assistance, accident forgiveness, and snow-related incident support, like Erie Insurance and State Farm, are particularly well-suited for these environments.

- Rural policyholders may benefit from insurers with strong digital infrastructure, as physical agent access can be limited. Progressive and Geico cater well to these drivers by offering fully online policy management and mobile claims submission, ensuring accessibility regardless of geographic location within the state.

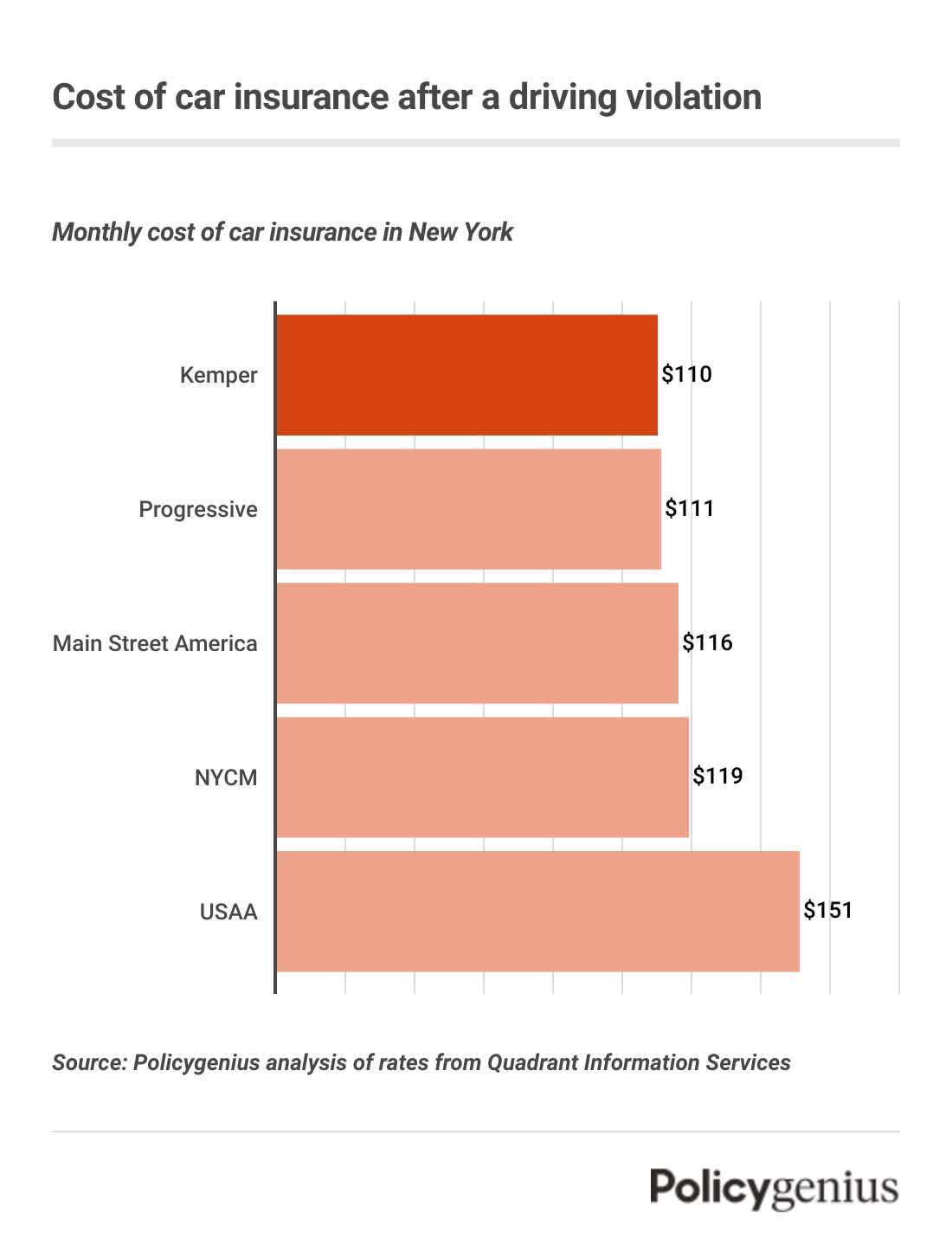

What is NYCM auto insurance and how does it compare for drivers in New York, NY?

What Is NYCM Auto Insurance?

- NYCM, or New York Compensation Mutual, is a specialized auto insurance provider that primarily serves drivers in New York City, with a focus on high-risk and underserved communities. Originally established to address the unique insurance challenges faced by urban drivers, NYCM offers policies that comply with New York State's mandatory minimum liability coverage, including no-fault (Personal Injury Protection), property damage liability, and uninsured/underinsured motorist coverage.

- The company operates with a mission to provide affordable yet compliant insurance solutions for drivers who may face difficulty obtaining coverage from mainstream insurers due to factors such as traffic violations, previous lapses in coverage, or limited insurance history. NYCM is licensed and regulated by the New York State Department of Financial Services, ensuring that it adheres to state-mandated standards and consumer protections.

- Unlike national insurers with broad marketing campaigns, NYCM maintains a localized presence and often partners with community organizations, brokers, and agencies familiar with the needs of New York City residents. This community-based approach allows the company to tailor its offerings to the densely populated, high-traffic environment of New York City, where driving risks and insurance costs are typically higher than in suburban or rural areas.

How Does NYCM Rate in Terms of Affordability and Coverage for NYC Drivers?

- For many New York City drivers, especially those with less-than-perfect driving records, NYCM can offer more accessible rates compared to standard insurers that may deny coverage or quote significantly higher premiums. While not always the cheapest option available, NYCM provides a viable alternative for high-risk drivers who need to meet the state’s legal requirements for insurance.

- The company's coverage options are generally standardized to align with New York's regulatory framework, meaning all policyholders receive essential protections such as No-Fault benefits, which cover medical expenses regardless of fault in an accident. However, optional coverages like collision, comprehensive, and rental reimbursement are available, allowing drivers to customize their policies based on their vehicle value and personal needs.

- Customer reviews and industry assessments often reflect mixed experiences with NYCM, particularly concerning customer service responsiveness and claims processing times. While the affordability factor is a draw, some policyholders report that the trade-off may include less flexibility and fewer digital tools compared to larger carriers. Still, for drivers who prioritize meeting state requirements at a manageable price, NYCM remains a practical choice.

How Does NYCM Compare to Other Auto Insurers in New York City?

- When compared to national insurers like GEICO, Progressive, or State Farm, NYCM typically does not offer the same breadth of discounts, online account management features, or telematics-based programs such as usage-based insurance. However, its niche focus on New York City drivers—particularly those overlooked by larger companies—gives it a distinct market position that broader insurers often don’t fulfill.

- Data from the New York State Department of Financial Services shows that NYCM’s premiums are competitive within the nonstandard insurance segment. While drivers with clean records may find lower rates elsewhere, NYCM often ranks among the more affordable options for those with prior infractions such as speeding tickets, at-fault accidents, or DWI convictions.

- Another key differentiator is NYCM’s claims handling process, which is localized and managed within the state, as opposed to being outsourced or handled through national call centers. This can be beneficial for drivers who prefer direct communication with claims representatives familiar with local traffic laws, accident patterns, and repair shop networks in New York City. However, response times and settlement satisfaction vary, making it essential for consumers to review current customer feedback before committing.

Frequently Asked Questions

What does auto insurance in New York cover?

Auto insurance in New York covers liability for bodily injury and property damage, personal injury protection (PIP), and uninsured/underinsured motorist benefits. New York is a no-fault state, so PIP helps pay medical expenses regardless of who caused the accident. Policies must also include minimum liability coverage of $25,000 per person for injury, $50,000 per accident, and $10,000 for property damage.

Is auto insurance mandatory in New York?

Yes, auto insurance is mandatory in New York State. All drivers must have a minimum amount of liability, no-fault (PIP), and uninsured motorist coverage. Driving without insurance can result in fines, license suspension, and vehicle registration revocation. Proof of insurance must always be carried while driving and provided during traffic stops or accidents. The law ensures financial responsibility and protection for all road users.

How can I lower my auto insurance rates in New York?

You can lower auto insurance rates in New York by maintaining a clean driving record, bundling policies, and taking defensive driving courses. Increasing deductibles, qualifying for discounts (such as safe driver or low-mileage), and driving a vehicle with high safety ratings also help. Comparing quotes from multiple insurers annually ensures you get the best rate. Always check for employer or affiliation-based discounts offered by some providers.

What should I do after a car accident in New York?

After a car accident in New York, ensure safety, call 911 if needed, and exchange insurance and contact information with the other driver. Take photos and gather witness details. Notify your insurer promptly and file a claim. Since New York is a no-fault state, use your PIP coverage for medical expenses. Report the accident to the DMV within 10 days if damages exceed $1,000.

Leave a Reply