Auto Insurance In Nh

Auto insurance in New Hampshire stands apart from other states due to its unique regulatory approach. Unlike most states, New Hampshire does not require drivers to carry auto insurance, making it one of the few states without a mandatory coverage law.

However, drivers must still prove financial responsibility, typically through insurance, and face penalties if unable to cover damages after an accident. This optional system places greater responsibility on individuals to make informed decisions about coverage.

Understanding the risks and benefits of various policies is essential for New Hampshire drivers. With rising vehicle costs and accident rates, having adequate protection ensures both legal compliance and financial security on the road.

Who offers the best unoccupied home insurance in the uk

Who offers the best unoccupied home insurance in the ukUnderstanding Auto Insurance in New Hampshire: What Drivers Need to Know

Auto insurance in New Hampshire operates under a unique framework compared to most other U.S. states. While New Hampshire is often recognized as the only state without a mandatory car insurance requirement, it still enforces a financial responsibility law that holds drivers accountable in the event of an accident.

This means drivers are not legally required to carry insurance, but they must be able to prove they can cover damages or injuries they may cause while operating a vehicle. Many residents choose to purchase auto insurance voluntarily to protect themselves from high out-of-pocket costs and legal liabilities. Common coverage options include liability insurance, collision coverage, comprehensive protection, and uninsured/underinsured motorist coverage.

Insurance providers in the state offer various policies, and premiums are influenced by factors such as driving history, age, vehicle type, and location within New Hampshire. Understanding how financial responsibility works and the risks of driving without insurance is critical for all drivers in the state.

Is Car Insurance Mandatory in New Hampshire?

Contrary to common belief, New Hampshire does not require drivers to carry auto insurance as a condition of vehicle registration or operation. However, under the state's financial responsibility law, drivers must demonstrate the ability to pay for damages or injuries caused in an at-fault accident.

Wichita home insurance cost

Wichita home insurance costThis responsibility can be met by purchasing traditional auto insurance, posting a cash bond, or securing a surety bond worth at least $25,000 for bodily injury per person, $50,000 per accident, and $25,000 for property damage—matching the minimum coverage limits if insurance were required.

Failure to show financial responsibility after an accident or traffic violation can result in penalties, including license suspension and fines. Although the option to forgo insurance exists, the majority of drivers opt for coverage due to the financial risks associated with paying large accident-related expenses out of pocket.

Common Auto Insurance Coverage Options in NH

New Hampshire drivers who choose to purchase auto insurance have access to a range of coverage types tailored to their needs.

Liability coverage remains the most fundamental, protecting drivers financially if they are found at fault in an accident involving injury or property damage. Many also select collision coverage to pay for repairs to their own vehicle after an accident, regardless of fault, and comprehensive coverage to address non-collision incidents like theft, vandalism, or weather damage.

Affordable home insurance for older homes tips

Affordable home insurance for older homes tipsAdditional valuable options include uninsured/underinsured motorist coverage, which protects policyholders if they are hit by a driver with no or insufficient insurance, and personal injury protection (PIP), which covers medical expenses and lost wages regardless of fault. Optional enhancements like roadside assistance, rental reimbursement, and gap insurance are also widely available and can be included based on driver preferences and vehicle value.

Factors That Influence Auto Insurance Rates in New Hampshire

Several key factors contribute to the variation in auto insurance premiums across New Hampshire residents. Driving history plays a major role—drivers with clean records typically receive lower rates, while accidents or traffic violations increase risk and thus premiums.

Age and gender are also considered, with younger drivers, especially males under 25, often facing higher costs due to statistical risk. The type of vehicle insured impacts rates as well; high-performance or expensive cars usually cost more to insure due to higher repair costs or theft risk.

Geographic location within the state matters; urban areas like Manchester or Nashua may have higher premiums due to increased traffic density and accident frequency. Additionally, credit-based insurance scores (where legally permissible), annual mileage, and coverage levels chosen all affect the final price. Shopping around and comparing quotes from multiple insurers can help drivers secure the most competitive rates.

Age uk insurance home

Age uk insurance home| Factor | Impact on Premiums | Typical Examples |

|---|---|---|

| Driving Record | Major influence | Accidents, DUIs, speeding tickets increase rates |

| Age and Experience | Significant | Teens and seniors often pay more; experience lowers cost |

| Vehicle Type | Moderate to high | Sports cars cost more to insure than sedans |

| Location in NH | Moderate | Manchester vs. rural towns—urban areas cost more |

| Coverage Selection | Direct | Higher limits and more options increase premiums |

| Credit History | Varies by insurer | Strong credit may lead to lower rates |

Comprehensive Guide to Auto Insurance in New Hampshire

What is the most affordable auto insurance in New Hampshire?

Top Budget-Friendly Auto Insurance Providers in New Hampshire

- Geico consistently ranks as one of the most affordable auto insurance providers in New Hampshire, offering competitive rates for drivers with clean records and safe driving habits. Their widespread availability and online tools make it easy to obtain quotes tailored to individual needs.

- Progressive is another cost-effective option, known for flexible coverage plans and innovative pricing models such as usage-based insurance through its Snapshot program. This can lead to significant savings for low-mileage or defensive drivers.

- State Farm, while slightly more variable in pricing, often provides affordable rates especially in rural areas of New Hampshire and rewards customer loyalty with multi-policy discounts and safe driving bonuses.

Factors That Influence Auto Insurance Costs in New Hampshire

- Driving history plays a critical role in determining premiums; drivers with accidents, traffic violations, or DUIs typically face higher rates. Insurers review motor vehicle records to assess risk, making responsible driving essential for affordability.

- Vehicle type affects pricing as well—insurers consider the make, model, age, and safety features of a car. High-performance or luxury vehicles often cost more to insure due to higher repair expenses and theft rates.

- Location within New Hampshire also impacts costs. Urban areas like Manchester or Nashua may have higher premiums due to increased traffic density and accident rates, while rural regions generally offer lower rates.

Ways to Reduce Auto Insurance Premiums in New Hampshire

- Maintaining a clean driving record is one of the most effective ways to secure lower rates. Avoiding tickets and accidents over time typically results in eligibility for safe driver discounts, which can reduce annual premiums significantly.

- Opting for higher deductibles can lower monthly payments, though it requires being prepared to pay more out-of-pocket in the event of a claim. This trade-off works best for financially prepared drivers with minimal accident risk.

- Taking advantage of available discounts such as bundling home and auto insurance, completing defensive driving courses, or installing anti-theft devices can further reduce costs across multiple providers.

What company offers the most affordable auto insurance in NH?

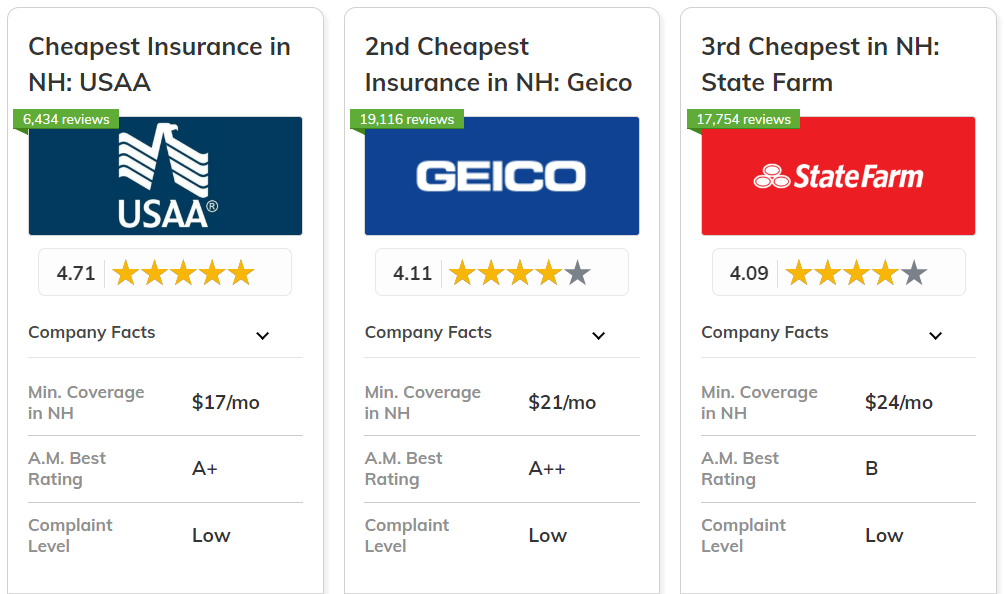

The most affordable auto insurance in New Hampshire is typically offered by USAA, though this is only available to active or former military members and their immediate families. For the general public, State Farm consistently ranks among the cheapest providers in the state.

Auto insurance rates vary significantly based on individual factors such as driving history, age, vehicle type, and location, so while certain companies are known for low average premiums, actual quotes may differ. New Hampshire does not require drivers to carry auto insurance, but it does mandate that drivers prove financial responsibility in the event of an accident, which often leads residents to still purchase coverage.

Average cost of home inspector insurance

Average cost of home inspector insuranceFactors That Influence Auto Insurance Rates in New Hampshire

- Driving Record: A history of accidents, traffic violations, or DUIs can substantially increase insurance premiums, as insurers view these as indicators of higher risk.

- Vehicle Type: Expensive, high-performance, or luxury vehicles generally cost more to insure due to higher repair costs and theft rates.

- Location Within NH: Urban areas such as Manchester or Nashua may have higher premiums due to increased traffic density and higher probabilities of accidents or theft compared to rural towns.

Top Low-Cost Insurance Providers in New Hampshire

- State Farm: Known for competitive rates and strong local agent support, State Farm frequently offers some of the lowest premiums for low-risk drivers across various age groups.

- GEICO: Offers affordability through online tools, safe driver discounts, and usage-based insurance programs like DriveEasy, which can further reduce costs for careful drivers.

- Progressive: Stands out with its price comparison tool, Snapshot, and bundling options, making it a strong contender for budget-conscious consumers seeking flexible coverage.

How to Find the Cheapest Auto Insurance Quote in NH

- Compare Multiple Quotes: Use online comparison tools or contact insurers directly to obtain personalized quotes, as rates can vary widely between companies for the same driver profile.

- Take Advantage of Discounts: Look for discounts such as multi-policy, safe driver, good student, or vehicle safety features, which can lower your premiums significantly.

- Adjust Coverage Levels: While NH has no mandatory insurance requirement, choosing appropriate liability limits and possibly higher deductibles can reduce costs, though this increases out-of-pocket expenses in case of a claim.

What is the top-rated auto and home insurance provider in New Hampshire?

The top-rated auto and home insurance provider in New Hampshire is often considered to be Geico, based on a combination of customer satisfaction, affordability, financial strength, and service accessibility. According to data from sources such as J.D.

Power, the National Association of Insurance Commissioners (NAIC), and customer reviews on platforms like NerdWallet and Bankrate, Geico consistently ranks highly in New England states, including New Hampshire. Factors contributing to its top status include competitive pricing, strong digital tools for policy management, and quick claims processing.

Additionally, Geico offers bundled policies that combine auto and home insurance, resulting in significant discounts for many New Hampshire residents. While other insurers like State Farm, Allstate, and Liberty Mutual are also popular, Geico’s consistent performance across ratings makes it a standout choice.

Factors That Make an Insurance Provider Top-Rated in New Hampshire

- Customer satisfaction scores from independent evaluators like J.D. Power and Consumer Reports play a crucial role, as they reflect real user experiences with claims handling and customer service.

- Financial stability, as assessed by rating agencies such as A.M. Best and Standard & Poor’s, ensures that the insurer can fulfill claims even during economic downturns or extreme weather events common in New Hampshire.

- Premium affordability and availability of discounts—for example, multi-policy, safety device, and good driving discounts—make certain providers more accessible and appealing to a broad range of residents across rural and urban areas.

Comparison of Top Auto and Home Insurance Providers in New Hampshire

- Geico is praised for its low premiums and user-friendly mobile app, making policy management convenient, although it lacks a local agent network, which some customers prefer.

- State Farm offers a strong local presence with agent offices throughout New Hampshire, personalized service, and competitive bundled rates, though its pricing may be slightly higher than Geico’s in some regions.

- Liberty Mutual differentiates itself with customizable coverage options and home system protection add-ons, which are valuable in New Hampshire’s harsh winters, but some customers report variability in claims handling times.

Benefits of Bundling Auto and Home Insurance in New Hampshire

- Bundling often results in a multi-policy discount, typically ranging from 10% to 20%, which can lead to substantial annual savings across both auto and home policies.

- Having both policies with the same provider simplifies management—customers can access both policies through a single online account, receive one renewal notice, and coordinate claims more efficiently.

- Insurers such as Geico and State Farm offer additional perks for bundled customers, including accident forgiveness on auto policies and deductible rewards for maintaining a claims-free home insurance history.

Frequently Asked Questions

What are the minimum auto insurance requirements in New Hampshire?

New Hampshire requires drivers to demonstrate financial responsibility, but doesn’t mandate minimum coverage levels. However, drivers must prove they can cover at least $25,000 for bodily injury per person, $50,000 per accident, and $25,000 for property damage. Most drivers purchase liability insurance to meet this, though they can also post a cash bond or self-insure. Failing to prove financial responsibility can lead to penalties.

Is no-fault insurance required in New Hampshire?

No, New Hampshire does not require no-fault insurance. Drivers must show financial responsibility but can pursue claims directly against the at-fault party after an accident. This means injured parties can sue for damages, including pain and suffering, rather than only seeking coverage through their own insurer. This differs from true no-fault states where personal injury protection (PIP) is required and lawsuits are limited.

Can I drive without auto insurance in NH?

Yes, you can legally drive without auto insurance in New Hampshire if you prove financial responsibility through alternative means, such as paying a cash bond or self-insuring with the DMV. However, most drivers choose to carry liability insurance because it's more practical and affordable than posting large bonds. Driving without coverage and without alternate proof can result in fines, license suspension, and vehicle impoundment.

How do auto insurance rates in NH compare to other states?

Auto insurance rates in New Hampshire are generally lower than the national average, largely due to the state's unique financial responsibility law and competitive market. However, premiums vary based on driving record, age, vehicle type, and coverage choices. While drivers have the legal option to self-insure or post bonds, most still buy insurance, which helps keep rates competitive among insurers serving the state.

Leave a Reply