Auto Insurance Mandate

Driving a vehicle comes with significant responsibilities, one of the most important being financial accountability for potential damages or injuries.

In most states across the United States, carrying auto insurance is not just a recommendation—it's a legal requirement. The auto insurance mandate exists to ensure that drivers can cover the costs associated with accidents, protecting both themselves and others on the road.

These laws vary by state, specifying minimum coverage levels for liability, bodily injury, and property damage. Failure to comply can result in fines, license suspension, or even vehicle impoundment, underscoring the importance of understanding and adhering to the mandate.

Difference between home insurance endorsements and exclusions

Difference between home insurance endorsements and exclusionsUnderstanding the Auto Insurance Mandate in the United States

The auto insurance mandate in the United States requires most drivers to carry a minimum level of financial protection in case of accidents.

This legal requirement is designed to ensure that individuals can cover costs related to bodily injury, property damage, or other liabilities resulting from motor vehicle collisions. While the federal government does not impose a nationwide auto insurance mandate, each state establishes its own regulations, with most mandating some form of liability coverage.

Drivers who fail to comply may face penalties such as fines, license suspension, or vehicle registration revocation. The foundational principle behind the mandate is to protect not only drivers but also other road users by promoting financial responsibility and reducing the burden of uncompensated accident-related expenses on the public system.

State-by-State Requirements for Auto Insurance Coverage

Auto insurance mandates vary significantly across U.S. states, with each state setting its own minimum coverage limits and requirements. Most states follow a liability insurance model, requiring drivers to carry at least bodily injury liability and property damage liability coverage.

Does home insurance cover electrical fire

Does home insurance cover electrical fireFor example, California mandates minimums of $15,000 for injury or death per person, $30,000 per accident, and $5,000 for property damage, while Florida requires $10,000 personal injury protection (PIP) and $10,000 property damage liability, operating under a no-fault insurance system.

A few states, like New Hampshire and Virginia, allow drivers to opt out under certain conditions—New Hampshire permits drivers to self-insure if they can prove financial responsibility, and Virginia allows a payment of an Uninsured Motor Vehicle (UMV) fee instead. Understanding the specific requirements in each state is essential for legal compliance and financial protection.

| State | Minimum Liability Coverage | Special Provisions |

|---|---|---|

| California | $15,000/$30,000/$5,000 | Requires proof of insurance; no opt-out option |

| Florida | $10,000 PIP / $10,000 PDL | No-fault state; PIP covers driver regardless of fault |

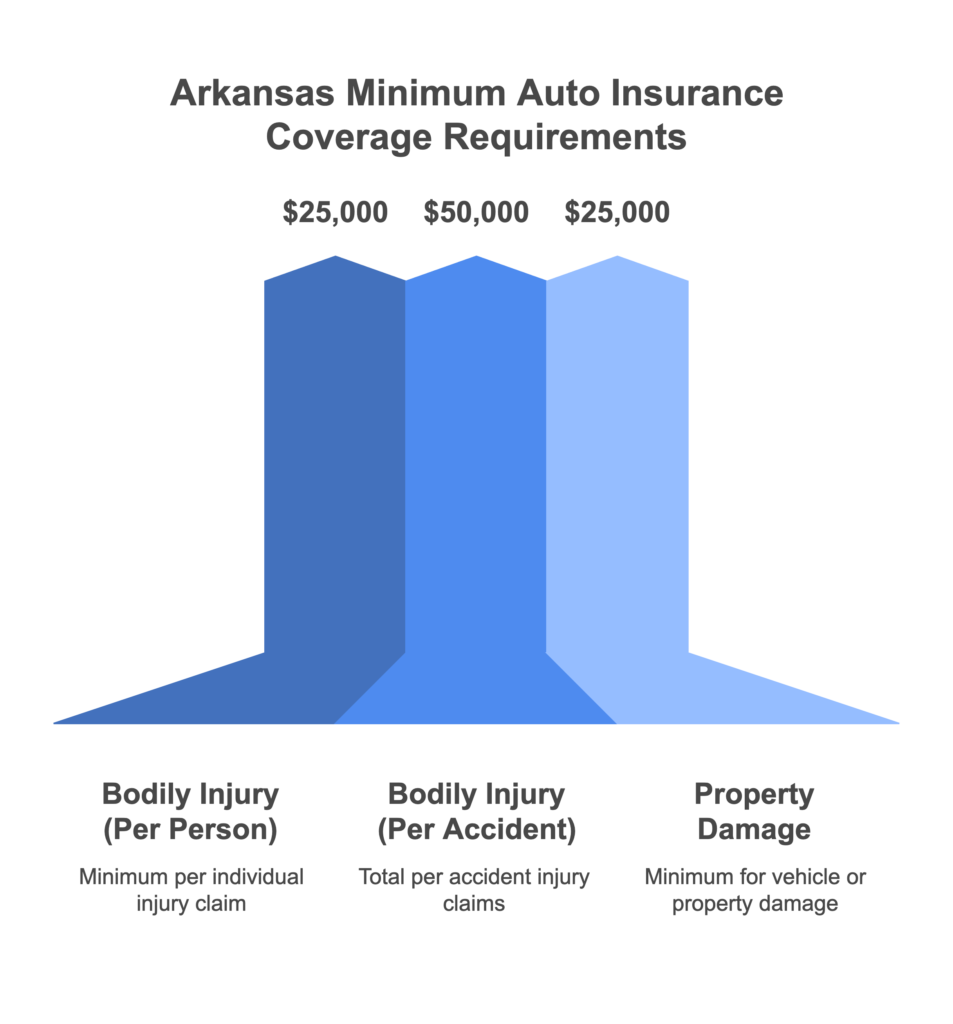

| New York | $25,000/$50,000/$10,000 | Requires uninsured motorist coverage |

| Virginia | Optional with $500 UMV fee | Drivers may opt out by paying fee |

| New Hampshire | No mandate | Must prove financial responsibility if involved in an accident |

Penalties for Driving Without Insurance

Failure to comply with an auto insurance mandate can lead to severe legal and financial consequences. Penalties for driving without insurance include fines, license suspension, vehicle impoundment, and mandatory filing of an SR-22 form to prove future financial responsibility. In states like Texas, fines can range from $175 to $350 for a first offense, along with possible jail time in repeated cases.

California may impose penalties up to $1,000 and a one-year license suspension. Additionally, uninsured drivers involved in accidents could be held personally liable for all damages, which can lead to wage garnishment or liens on property. The long-term impact also includes increased insurance premiums once coverage is obtained, making non-compliance both risky and costly.

Dwelling coverage for home insurance

Dwelling coverage for home insuranceAlternatives to Traditional Auto Insurance

While most drivers obtain coverage through private insurance companies, several states allow alternatives to traditional auto insurance policies to satisfy the mandate.

One common option is self-insurance, available in states like California, Texas, and Washington, where individuals or companies with significant assets (usually $50,000 or more in liquid funds or vehicle equity) can file for a self-insurance certificate. Another alternative is posting a cash bond or surety bond with the state, which acts as a financial guarantee in case of claims.

Motor vehicle liability insurance through a joint underwriting association (JUA) or assigned risk plan is also available for high-risk drivers who cannot obtain coverage in the standard market. These alternatives ensure that the core objective of the mandate—financial responsibility—is met through different mechanisms tailored to individual circumstances.

Understanding the Auto Insurance Mandate: A Comprehensive Guide

Why is auto insurance a legal requirement?

Fast claims processing home insurance providers

Fast claims processing home insurance providersFinancial Responsibility and Protection of Third Parties

Auto insurance is mandated by law primarily to ensure that drivers are financially responsible for damages or injuries they may cause while operating a vehicle.

Without insurance, victims of accidents could face significant out-of-pocket expenses for medical treatment, vehicle repairs, or lost income. Mandatory insurance ensures that individuals who suffer losses due to another driver’s actions receive timely compensation. This protection extends beyond just the driver at fault, reinforcing a system where financial risks are shared and managed effectively.

- Insurance provides a financial safety net for injured parties when the at-fault driver cannot pay for damages.

- It supports medical payments and property damage claims regardless of the victim’s financial status.

- Laws require minimum coverage limits to ensure a baseline level of financial protection for all road users.

Reduction of Uninsured Motorist Risk

A major reason auto insurance is legally required involves minimizing the number of uninsured drivers on the road.

When a large portion of drivers are uninsured, the likelihood of uncompensated losses increases, placing a heavier burden on insured drivers and the legal system. Mandatory insurance laws, combined with enforcement mechanisms like vehicle registration checks and fines, help keep uninsured rates lower and promote accountability among all drivers.

Fort worth home insurance cost

Fort worth home insurance cost- States with compulsory insurance report lower rates of uninsured motorists compared to voluntary systems.

- Insurance verification systems during registration help authorities track compliance and enforce penalties.

- Uninsured motorist coverage, often required alongside liability insurance, protects policyholders when involved in accidents with uninsured drivers.

Support for Legal and Traffic Safety Systems

Auto insurance laws work in tandem with broader traffic safety regulations to promote responsible driving behavior and efficient claims processing.

By requiring proof of insurance, governments can better manage vehicle registration and ensure that drivers meet basic legal standards before being allowed on public roads. Additionally, insurance companies contribute to safer driving by implementing risk-based premiums and supporting accident investigations.

- Proof of insurance is typically required for vehicle registration, linking legal operation of a car to financial responsibility.

- Insurance data helps law enforcement and courts resolve liability in traffic accidents more efficiently.

- Premium structures incentivize safe driving behavior, as risky drivers face higher costs, encouraging improved habits over time.

What Are the Latest Auto Insurance Requirements Under North Carolina’s New Law?

Minimum Liability Coverage Requirements

As of the latest updates to North Carolina’s auto insurance laws, drivers are required to maintain minimum liability coverage to operate a vehicle legally. This type of insurance protects drivers financially in the event they are at fault in an accident that causes injury or property damage to others. The state-mandated minimums include specific coverage amounts that must be met by all registered vehicle owners.

- Bodily injury liability coverage is required at a minimum of $30,000 per person injured in an accident, with a total limit of $60,000 per accident involving multiple individuals.

- Property damage liability coverage must be at least $25,000 per accident to cover damages to other vehicles or property such as fences, buildings, or street fixtures.

- Proof of insurance must be carried at all times while driving and must be presented upon request by law enforcement or during vehicle registration renewal.

Uninsured and Underinsured Motorist Coverage Options

North Carolina law not only requires liability coverage but also mandates that insurance companies offer uninsured and underinsured motorist coverage to policyholders. While drivers have the legal right to reject this coverage in writing, it is strongly recommended for financial protection against accidents involving drivers who lack sufficient insurance.

- Uninsured motorist coverage helps pay for medical expenses, lost wages, and other damages if a driver is hit by someone who has no insurance or in hit-and-run incidents where the at-fault driver is unidentified.

- Underinsured motorist coverage applies when the at-fault driver’s insurance limits are insufficient to cover the full extent of injuries or damages sustained in an accident.

- Insurers must provide a written form that allows policyholders to formally reject this coverage; without a valid rejection, the coverage defaults to the same limits as the driver’s liability insurance.

Proof of Insurance and Penalties for Noncompliance

North Carolina enforces strict regulations regarding proof of insurance, and failure to comply can result in significant penalties. Drivers are required to validate their insurance status both at the point of vehicle registration and during traffic stops, ensuring continuous compliance with state law.

- Drivers must present a physical or electronic insurance card issued by a licensed provider, showing active coverage that meets or exceeds the state minimums.

- Operating a vehicle without valid insurance can lead to fines up to $50, license and registration suspension, and potential vehicle impoundment.

- The North Carolina Department of Motor Vehicles (NCDMV) participates in an electronic insurance verification system, allowing real-time checks to confirm a driver’s insurance status and reduce the number of uninsured vehicles on the road.

Can I legally drive my parents' car without being listed on their auto insurance policy?

Whether you can legally drive your parents' car without being listed on their auto insurance policy depends on several factors, including the laws in your state or country and the specific terms of the insurance policy. In general, most auto insurance policies cover permissive drivers — people who have the owner's permission to drive the vehicle, even if not formally listed on the policy.

This means that as a family member living in the same household, you may be allowed to drive your parents' car occasionally with their consent. However, insurance companies typically expect that anyone who regularly operates the vehicle be listed on the policy, especially if you're a licensed driver.

Failing to add a regular driver could be considered misrepresentation by the insurer and may result in denied claims or policy cancellation. Therefore, while occasional driving may be covered, habitual use without being listed can create significant legal and financial risks.

Permissive Use in Auto Insurance Policies

- Most auto insurance carriers include a permissive use clause, which extends coverage to individuals who are not listed on the policy but have the owner’s consent to drive the vehicle. This is intended for occasional or temporary use, such as borrowing the car for a single trip or running errands.

- Permissive use typically applies to friends, neighbors, or relatives who are not residents of the household. However, rules vary by insurer: some may exclude household members who are not explicitly listed, especially if they are of driving age.

- If an accident occurs while you're driving with permission but are not listed on the policy, the insurance may still provide coverage. However, the insurer could investigate whether you were a regular driver and potentially deny the claim if they determine you should have been formally included.

Risks of Not Being Listed as a Driver

- One major risk is that your parents’ insurance company might deny a claim if you're involved in an accident and were not listed, particularly if you drive the car frequently. Insurers expect that all regular operators of a vehicle are disclosed to accurately assess risk.

- Insurance fraud can be alleged if the insurer believes your parents intentionally omitted you to reduce premiums. This may lead to policy cancellation, legal penalties, and future difficulties in obtaining coverage.

- Financial liability increases significantly if the claim is denied. Without insurance coverage, you and your parents could be held personally responsible for medical expenses, property damage, and legal fees resulting from an accident.

When You Must Be Added to the Policy

- You should be formally added to your parents’ insurance policy if you live in the same household, are licensed, and drive the vehicle regularly. Most insurers require household members with a driver’s license to be listed, regardless of whether they own a car.

- Newly licensed drivers, such as teenagers, are commonly required to be added to the policy shortly after obtaining a license. Failing to do so can violate the terms of the insurance agreement.

- Insurance companies often adjust premiums based on the drivers listed, taking into account age, driving history, and experience. While adding a young driver may increase the premium, it ensures full coverage and compliance with policy terms.

Frequently Asked Questions

What is an auto insurance mandate?

An auto insurance mandate is a legal requirement that drivers must have a minimum level of insurance coverage to operate a vehicle. This helps ensure that drivers can cover costs related to accidents, injuries, or property damage. Most U.S. states require liability insurance as part of this mandate. Failure to comply can result in fines, license suspension, or other penalties.

Why do states require auto insurance?

States require auto insurance to protect drivers, passengers, and the public from financial loss after an accident. It ensures that individuals who cause accidents can pay for damages or medical expenses. Without mandatory insurance, accident victims might face high out-of-pocket costs. The mandate promotes responsible driving and financial accountability on the roads.

What happens if I don’t have auto insurance?

If you're caught driving without auto insurance, you may face penalties like fines, license suspension, vehicle impoundment, or mandatory enrollment in high-risk insurance programs. Some states may require you to file an SR-22 form as proof of future financial responsibility. Driving uninsured can also lead to long-term increases in insurance premiums.

Can I drive legally without insurance in any U.S. state?

No U.S. state allows completely uninsured driving, but two states—New Hampshire and Wisconsin—have different rules. New Hampshire requires drivers to prove financial responsibility instead of carrying insurance, while Wisconsin allows alternative security deposits. However, most drivers in these states still choose to purchase auto insurance to protect against high accident-related costs.

Leave a Reply