Best Life Insurance For 40 Year Old

Choosing the best life insurance at age 40 involves balancing affordability, coverage needs, and long-term financial goals.

This pivotal age often brings increased responsibilities, including mortgages, children’s education, and aging parents, making adequate protection essential. Term life insurance remains a popular choice for its low premiums and straightforward structure, while permanent policies offer lifelong coverage and cash value accumulation.

Evaluating financial strength, customer service, and policy flexibility among top insurers helps ensure reliable protection. With the right plan, individuals at 40 can secure peace of mind and financial stability for their loved ones.

Best Life Insurance For 50 Year Old

Best Life Insurance For 50 Year OldBest Life Insurance Options for 40-Year-Olds: Finding the Right Coverage

At age 40, individuals are often at a pivotal point in life—balancing growing families, mortgages, and long-term financial goals. This makes it an ideal time to secure life insurance, as premiums are typically more affordable than later in life, and health is generally still favorable.

The best life insurance for 40-year-olds depends on individual needs such as budget, length of coverage, and whether the goal is temporary protection or permanent financial planning. Term life insurance is often the top choice due to its affordability and straightforward structure, offering coverage for 10, 20, or 30 years.

However, whole life or universal life insurance may be appropriate for those seeking lifelong coverage with a cash value component. Evaluating financial obligations, dependents' needs, and future goals is essential when selecting the most suitable policy.

Why Life Insurance at Age 40 Is a Smart Financial Decision

Purchasing life insurance at 40 is a strategic financial move because it locks in lower premiums before advancing age or potential health issues increase costs.

Costco Business Insurance For Small Business

Costco Business Insurance For Small BusinessMost 40-year-olds are in relatively good health, making them ideal candidates for competitive rates. This is especially crucial for those with dependents, such as children or a spouse, who rely on their income. Life insurance can cover mortgage payments, college tuition, and daily living expenses if the policyholder passes away unexpectedly.

Additionally, buying earlier allows for longer-term coverage that aligns with financial commitments. Securing a policy now ensures peace of mind and helps protect your family’s long-term stability.

Term vs. Permanent Life Insurance: Which Is Right at 40?

When evaluating the best life insurance at 40, the primary decision lies between term and permanent policies.

Term life insurance provides coverage for a set period—commonly 15, 20, or 30 years—and is significantly more affordable, making it ideal for individuals needing coverage during key financial responsibility years. It’s perfect for replacing income until retirement or until children are financially independent.

Drywall Business Insurance Georgia

Drywall Business Insurance GeorgiaOn the other hand, permanent life insurance, such as whole or universal life, offers lifelong protection and builds cash value over time, which can be borrowed against. While more expensive, permanent policies may appeal to those with estate planning goals or who wish to leave a financial legacy. Most 40-year-olds benefit most from term life due to cost-effectiveness and flexibility.

Top Factors to Consider When Choosing a Life Insurance Policy at 40

Selecting the best life insurance at 40 requires careful evaluation of several key factors. First, assess your coverage needs by calculating debts, future expenses (like education), and income replacement goals.

Next, consider your budget—premiums should be sustainable over the policy’s duration. Your health status plays a major role in determining eligibility and rates; non-smokers and those with clean medical histories receive the best offers.

It’s also important to evaluate the financial strength of the insurer, ensuring the company is reputable and rated highly by agencies like AM Best or Moody’s. Finally, decide whether convertible term policies or riders like accelerated death benefits add value to your plan based on your long-term goals.

Drywall Business Insurance Massachusetts

Drywall Business Insurance Massachusetts| Insurance Type | Average Annual Premium (Non-Smoker) | Coverage Duration | Key Benefits |

|---|---|---|---|

| 20-Year Term Life | $400–$600 | 20 years | Affordable, ideal for income replacement and mortgage protection |

| 30-Year Term Life | $600–$900 | 30 years | Long-term coverage, suitable for young families |

| Whole Life Insurance | $2,500–$4,000 | Lifetime | Builds cash value, fixed premiums, estate planning tool |

| Universal Life Insurance | $3,000–$5,000 | Lifetime | Flexible premiums, adjustable death benefit, investment component |

Best Life Insurance Options for 40-Year-Olds: A Comprehensive Guide

What is the most suitable life insurance policy for a 40-year-old seeking long-term coverage?

Term Life Insurance: Affordable Long-Term Protection

Term life insurance is often the most suitable choice for a 40-year-old seeking long-term coverage due to its affordability and simplicity.

A term policy provides coverage for a specific period—commonly 15, 20, or 30 years—making it ideal for covering long-term financial responsibilities such as a mortgage, children’s education, or income replacement.

At age 40, individuals typically qualify for favorable rates, as they are generally considered lower risk by insurers. While term life does not build cash value, it offers substantial death benefits at a lower cost compared to permanent policies.

- Selecting a 20- or 30-year term aligns well with major financial goals that extend into retirement or beyond, ensuring dependents are protected during critical years.

- Many term policies come with a conversion option, allowing the policyholder to switch to a permanent plan later without medical underwriting, which is valuable if needs change.

- Due to lower premiums, individuals can purchase higher coverage amounts, which maximizes financial protection for beneficiaries.

Whole Life Insurance: Lifelong Coverage with Cash Accumulation

Whole life insurance is a form of permanent life insurance that provides coverage for the insured’s entire life, as long as premiums are paid. For a 40-year-old considering long-term legacy planning or estate protection, whole life offers guaranteed death benefits and a savings component known as cash value, which grows at a guaranteed rate over time.

Premiums are higher than those for term life, but they remain level throughout the policyholder's life. This predictability makes whole life appealing for individuals seeking stability and additional financial tools beyond pure insurance.

- The cash value component can be borrowed against or withdrawn to help fund large expenses such as college tuition or emergency needs.

- Because the death benefit is guaranteed, whole life can serve as a reliable tool for estate planning, charitable giving, or leaving a financial legacy.

- Premiums are fixed, so even as the policyholder ages and health may decline, the cost of insurance does not increase.

Universal Life Insurance: Flexible Coverage with Adjustment Options

Universal life insurance offers more flexibility than whole life, making it a strong option for a 40-year-old who wants long-term coverage with the ability to adjust premiums and death benefits over time.

This type of permanent policy also accumulates cash value, typically based on current interest rates, giving the policyholder more control over how the policy performs financially. While it requires more active management, universal life can be tailored to evolving financial circumstances, such as changes in income, family size, or retirement plans.

- Adjustable premium payments allow policyholders to increase or decrease payments within certain limits, helping manage cash flow during different life stages.

- The death benefit can often be modified based on changing needs, such as reducing coverage after a mortgage is paid off or increasing it during periods of higher financial responsibility.

- Cash value growth, while not always guaranteed, can outperform traditional whole life policies if interest rates are favorable, providing a potential boost to long-term value.

What is the best term life insurance for a 40-year-old?

The best term life insurance for a 40-year-old depends on a combination of financial needs, health status, lifestyle, and long-term goals. At age 40, individuals often have growing families, mortgages, or children’s education to plan for, making this a strategic time to secure affordable coverage.

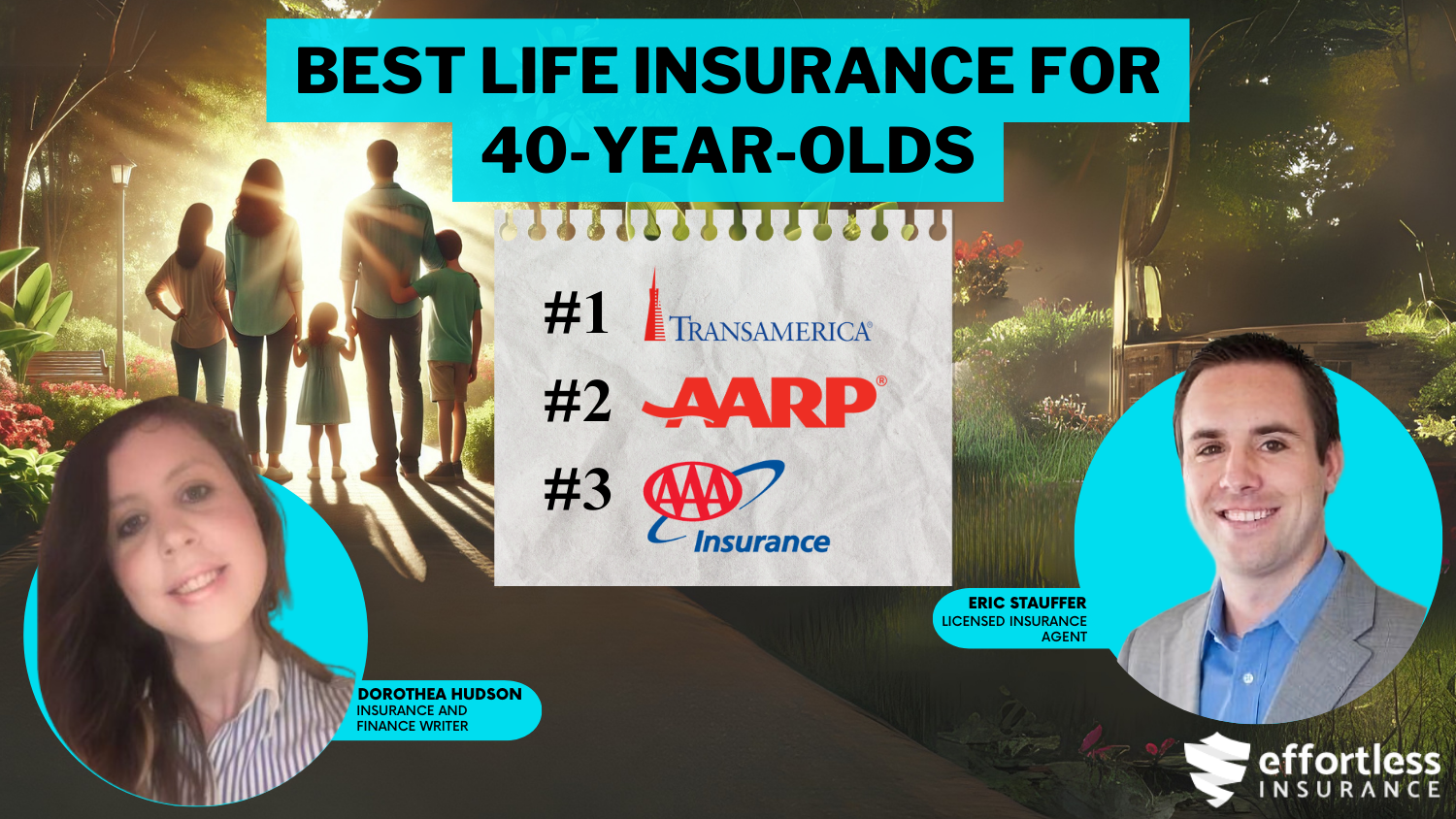

Term life insurance typically offers the most cost-effective solution with high coverage amounts for a fixed period, usually between 10 to 30 years. Top providers like Haven Life, Policygenius, and Northwestern Mutual are frequently recommended due to their strong financial ratings, streamlined application processes, and flexible policy options.

Term lengths of 20 or 30 years are commonly chosen to align with major financial obligations such as a mortgage or college tuition. The key is to assess how much coverage is needed—often 10 to 15 times annual income—and compare quotes across reputable insurers to balance affordability with reliability.

Factors to Consider When Choosing a Term Life Insurance Policy at Age 40

- Health history and current medical status play a crucial role in determining premium rates. Individuals in good health can qualify for preferred underwriting classes, resulting in significantly lower monthly payments. It's advisable to undergo a medical exam or consider no-exam policies if time is a constraint, though these may cost slightly more.

- Coverage amount should reflect current and future financial responsibilities. This includes remaining mortgage balances, children's education costs, daily living expenses, and potential end-of-life costs. A thorough assessment of these obligations helps determine whether a $500,000 or $1 million policy (or more) is appropriate.

- Term length is another critical factor. A 30-year term might be ideal for a 40-year-old with young children, ensuring protection until they become financially independent. In contrast, a 15- or 20-year term may suffice for someone primarily covering a mortgage or building savings.

Top Term Life Insurance Providers for 40-Year-Olds

- Haven Life offers the Haven Term policy, backed by MassMutual, and is known for its fully online, streamlined application process with quick approval times. It provides coverage up to $3 million and includes an accelerated death benefit at no extra cost, ideal for those seeking convenience and reliability.

- Policygenius acts as a digital broker that allows users to compare multiple insurers such as Banner Life, AIG, and Brighthouse Financial. Their platform offers personalized guidance and side-by-side comparisons, helping 40-year-olds find the most competitive rates based on individual profiles.

- Northwestern Mutual stands out for its exceptional financial strength and ability to convert term policies to permanent life insurance later. While the application process may be longer, the long-term flexibility and personalized service appeal to individuals planning comprehensive financial protection.

Additional Features to Look for in a Term Life Policy

- Convertible term options allow policyholders to switch to a permanent life insurance policy (such as whole life) without undergoing another medical exam. This is particularly valuable for 40-year-olds who may want lifelong coverage in the future but currently prefer lower premiums.

- Renewable terms enable policyholders to extend coverage at the end of the initial term, even if their health has declined. While premiums will increase upon renewal, this feature ensures continued protection without needing to requalify medically.

- Riders such as a waiver of premium for disability or a child protection rider can enhance a base policy. The waiver of premium rider, for example, suspends payments if the policyholder becomes disabled, maintaining coverage during financial hardship.

What’s the best life insurance for a 40-year-old and is age 40 too late to start?

Is Age 40 Too Late to Start Life Insurance?

Starting life insurance at age 40 is not too late, and in fact, it remains an excellent time to secure coverage.

While premiums are generally lower when you're younger, the rates at age 40 are still considered relatively affordable compared to later decades. Many people in their 40s have growing families, mortgages, or other financial obligations, making this a strategically important time to obtain life insurance.

Insurers typically view individuals in their 40s as moderate-risk, especially if they maintain good health, which means qualifying for preferred rates is still very possible. Additionally, locking in a policy now can protect against future health issues that may make coverage more difficult or expensive later.

- Premiums at age 40 are significantly lower than those in the 50s and 60s, offering a cost-effective window for long-term planning.

- Many with dependents, such as children or a spouse, use this stage to ensure financial protection in case of unexpected loss.

- Health conditions often begin developing in later years, so securing coverage before any diagnosis helps avoid exclusions or higher premiums.

Types of Life Insurance Best Suited for a 40-Year-Old

For individuals at age 40, term life insurance is often the most recommended option due to its affordability and simplicity. It provides coverage for a specific period—commonly 10, 20, or 30 years—aligning with major financial responsibilities like a mortgage or children's education.

However, whole life and universal life insurance may be appropriate for those seeking lifelong coverage and cash value accumulation. The choice depends on personal goals, budget, and financial complexity. For most people in their 40s with dependents and limited investment portfolios, term life offers the right balance of protection and cost-efficiency.

- Term life insurance is ideal for covering specific financial responsibilities such as a mortgage, college tuition, or income replacement over 20–30 years.

- Whole life insurance provides permanent coverage with fixed premiums and builds cash value over time, suitable for estate planning or long-term wealth transfer.

- Universal life insurance offers flexibility in premiums and death benefits, allowing policyholders to adjust coverage as financial situations evolve.

Factors That Influence Life Insurance Choices at Age 40

Several personal and financial factors determine the best life insurance policy for someone at 40. Health status is a primary consideration, as it directly affects premium rates and eligibility. Lifestyle habits such as smoking, alcohol consumption, and participation in high-risk activities can also influence costs.

Financial obligations—including income level, debt, number of dependents, and future goals like funding education or retirement—play a crucial role in determining the appropriate type and amount of coverage. Additionally, employment benefits, such as employer-provided life insurance, may not offer sufficient protection, making a supplemental personal policy necessary.

- Health evaluations, including blood pressure, cholesterol, and BMI, are key in qualifying for preferred underwriting classes with the lowest rates.

- Smokers or those with chronic conditions may still find affordable options, but they should expect higher premiums compared to non-smokers in good health.

- People with complex financial goals, such as wealth transfer or business succession, may benefit from combining term with permanent policies for comprehensive protection.

Frequently Asked Questions

What type of life insurance is best for a 40-year-old?

The best life insurance for a 40-year-old is typically a 20- or 30-year term life policy. These offer affordable premiums and enough coverage during key financial years. Term life provides a death benefit to beneficiaries if the insured dies within the term. At age 40, health is usually still good, making it an ideal time to lock in low rates for long-term financial protection.

How much life insurance should a 40-year-old get?

A 40-year-old should generally get life insurance equal to 10–15 times their annual income or enough to cover debts, future expenses, and family needs. This includes mortgage payments, children’s education, and income replacement. Online calculators can help determine precise amounts. Having adequate coverage ensures financial stability for dependents and eases the burden of unexpected loss.

Is it worth getting life insurance at 40?

Yes, getting life insurance at 40 is highly worthwhile. Premiums are still relatively low compared to later years, and health is often good, leading to better rates. Life insurance at this age protects growing families, covers significant financial obligations, and locks in affordability. It also provides peace of mind knowing loved ones will be financially secure if the unexpected occurs.

Can I change my life insurance policy after age 40?

Yes, you can adjust your life insurance policy after 40 by converting, increasing, or switching coverage. Term policies may allow conversion to permanent life insurance. Adding riders or buying supplemental policies is also an option. However, changes later in life may come with higher premiums or medical underwriting. Reviewing coverage every few years helps ensure it meets evolving financial needs.

Leave a Reply