Best Life Insurance Rates For Smokers

Smokers often face higher life insurance premiums due to the increased health risks associated with tobacco use.

However, affordable coverage is still within reach for those who know where to look. Many insurers evaluate applicants based on smoking frequency, type of tobacco product, and overall health, allowing some flexibility in rate determination.

Term life policies typically offer the most competitive rates, while preferred smoker programs can significantly reduce costs for those in good health. Comparing quotes from multiple providers is essential to finding the best value. With the right strategy, smokers can secure reliable life insurance protection without overpaying.

Costco Business Insurance For Small Business

Costco Business Insurance For Small BusinessBest Life Insurance Rates For Smokers: How to Find Affordable Coverage Despite Tobacco Use

Finding affordable life insurance as a smoker can be challenging, as tobacco use significantly increases risk in the eyes of insurers, often leading to substantially higher premiums. However, many insurance providers recognize that not all smokers present the same level of risk and offer tiered pricing based on factors like frequency of use, type of tobacco product, and efforts to quit.

Some companies even classify certain nicotine products—like nicotine replacement therapy or vaping—differently from traditional cigarettes, allowing for more competitive rates under specific conditions.

By shopping around, disclosing accurate health information, and understanding how insurers classify tobacco users, smokers can still access competitive life insurance rates and secure vital financial protection for their families.

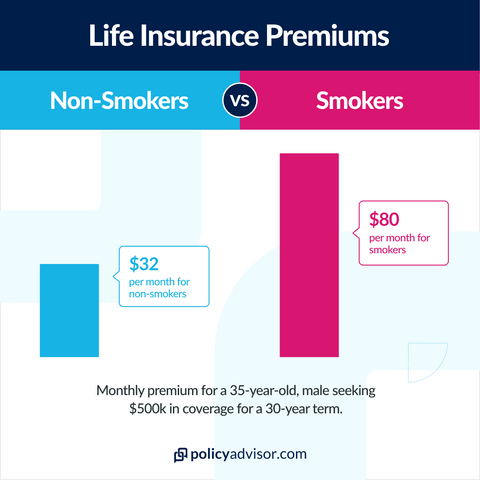

Life insurance companies categorize applicants based on health risks, and smoking remains one of the most significant factors that drive up premiums.

Drywall Business Insurance Georgia

Drywall Business Insurance GeorgiaSmokers typically pay 2 to 3 times more than non-smokers for the same coverage due to the elevated risk of life-threatening conditions such as heart disease, cancer, and respiratory illnesses. Insurers define a smoker as anyone who has used tobacco products—including cigarettes, cigars, chewing tobacco, or even nicotine patches or vapes—within a specific period, usually the past 12 months.

Even occasional or social smokers are often grouped with regular users, leading to higher classification rates. However, some insurers offer preferred smoker rates for applicants with otherwise excellent health, making it worthwhile to compare multiple providers to find the most favorable terms.

Types of Life Insurance Policies Available for Smokers

Smokers have access to the same types of life insurance policies as non-smokers, including term life, whole life, and universal life insurance, but the cost and eligibility vary significantly.

Term life insurance is often the most affordable option, providing coverage for a specified period—typically 10 to 30 years—and is ideal for those seeking temporary protection at a lower cost. Permanent life insurance, such as whole or universal life, offers lifelong coverage with a cash value component, but premiums are considerably higher, especially for smokers.

Drywall Business Insurance Massachusetts

Drywall Business Insurance MassachusettsSome insurers also offer guaranteed issue or simplified issue policies that don’t require a medical exam, though these come with higher premiums and lower coverage limits. For smokers, choosing the right type of policy depends on budget, long-term financial goals, and health status.

Top Insurance Companies Offering Competitive Rates for Smokers

While most insurers charge higher premiums for tobacco users, some companies are known for offering more favorable life insurance rates for smokers due to flexible underwriting guidelines and preferred smoker categories.

Companies like Banner Life, Lincoln Financial, and Haven Life are frequently cited for their competitive pricing and clear classification systems for tobacco users. These insurers may offer discounted rates if you use nicotine replacement products without tobacco or if you can demonstrate a plan to quit.

Additionally, some carriers re-evaluate your smoker status after a few years of tobacco-free living, potentially allowing you to reclassify as a non-smoker and reduce your premiums. Shopping through independent brokers or online comparison tools can help identify the best available options across multiple providers.

| Insurance Provider | Premium for $500,000 20-Year Term (Male, 40) | Smoker Classification | Notable Features |

|---|---|---|---|

| Banner Life | $72/month | Preferred smoker rate available | Offers competitive pricing and strong financial ratings |

| Lincoln Financial | $78/month | Tobacco rates based on frequency and type | Flexible underwriting; considers nicotine replacement therapy |

| Haven Life | $80/month | Requires disclosure of all nicotine use | Fast, fully digital application and no medical exam options |

| Prudential | $95/month | Strict tobacco classification | Good for long-term planning but less competitive for smokers |

Compare the Best Life Insurance Rates for Smokers in 2024

What are the most affordable life insurance options available for smokers?

Term Life Insurance for Smokers

Term life insurance is often the most affordable option for smokers seeking coverage, as it provides a high amount of death benefit for a set period at a lower cost compared to permanent policies.

Insurers typically classify smokers based on nicotine use, which results in higher premiums than non-smokers, but term policies still offer competitive rates due to their temporary nature.

It's essential for smokers to compare quotes from multiple providers, as underwriting guidelines and rate structures vary significantly between companies. Some insurers are more lenient with tobacco use, especially if the applicant has not used nicotine for a certain period.

- Select a term length that aligns with your financial obligations, such as 10, 20, or 30 years, to balance affordability and coverage needs.

- Shop around using online comparison tools or an independent agent who can access multiple carriers to find the best smoker rates.

- Be honest about tobacco use during the application process to avoid policy denial or claims issues later, even if it increases premiums.

Guaranteed Issue Life Insurance Options

Guaranteed issue life insurance is another affordable route for smokers, particularly those who may face health complications or difficulty qualifying for traditional coverage.

These policies do not require a medical exam or health questions, making them accessible but usually limited in death benefit amounts, often ranging from $5,000 to $25,000. Because of the minimal underwriting, premiums per unit of coverage are generally higher than term policies, but they offer guaranteed acceptance regardless of smoking status or health condition.

- Consider guaranteed issue policies if you have chronic health conditions in addition to smoking, as approval is not based on medical history.

- Understand that most policies include a graded death benefit, meaning full coverage only takes effect after two to three years of consistent premium payments.

- Evaluate whether the long-term cost matches your needs, as high premiums relative to the payout may not be cost-effective for younger, healthier smokers.

Reducing Costs by Quitting Smoking

One of the most effective ways for smokers to reduce life insurance costs is to quit tobacco and reapply for coverage after meeting an insurer’s required cessation period, typically 12 months.

Once you no longer use nicotine products, including cigarettes, vapes, or smokeless tobacco, you may qualify for non-smoker rates, which can cut premiums by 50% or more. Insurers usually require proof such as a medical exam with a nicotine test, so maintaining a smoke-free lifestyle is essential.

- Keep records of your efforts to quit, like counseling sessions or nicotine replacement therapy, which can support your case during underwriting.

- Wait at least one year after quitting before applying for a new policy to meet most insurers’ non-smoker classification requirements.

- Re-evaluate your existing policy or shop for a new one once you qualify as a non-smoker to secure substantially lower premiums.

What is the best term life insurance for smokers seeking low rates?

Understanding Term Life Insurance Options for Smokers

- Smokers are typically classified into different risk categories by life insurance providers, such as tobacco users or nicotine users, which directly influences premium rates. Understanding this classification helps smokers identify insurers that offer fair pricing structures.

- Term life insurance policies for smokers often come with higher premiums compared to non-smokers due to the increased health risks associated with tobacco use. However, some insurers are more lenient in their underwriting and may offer competitive rates based on overall health rather than just tobacco use.

- It's essential for smokers to shop around and compare multiple quotes because underwriting guidelines vary significantly between companies. Some insurers may consider occasional tobacco use differently or allow reclassification after a period of cessation, which can drastically lower costs over time.

Top Insurance Providers Offering Low Rates for Smokers

- Companies like Banner Life and Pacific Life are known for offering some of the most affordable term life insurance rates for smokers. These insurers take a balanced approach to risk evaluation and often provide level premiums that remain stable throughout the policy term.

- Prudential Financial offers competitive rates and unique underwriting criteria that may benefit smokers who have made efforts to reduce or quit tobacco use. Their Grace Period program allows for temporary lapses in nicotine testing without immediate rate increases.

- Brighthouse Financial is another provider that offers favorable pricing for tobacco users, particularly those in good overall health. Their simplified underwriting process can speed up approval and provide quick access to coverage at lower-than-average smoker rates.

- Maintaining good health beyond tobacco use—such as managing weight, blood pressure, and cholesterol—can improve risk classification and lead to lower premiums, even for current smokers. Insurers evaluate overall health, so excelling in other areas may partially offset tobacco-related risks.

- Quitting smoking and remaining tobacco-free for at least 12 months can allow individuals to reapply for coverage under non-smoker rates. Some insurers require a 5-year smoke-free period, but even reductions to occasional use may help in qualifying for better pricing tiers.

- Opting for shorter term lengths, such as 10- or 15-year policies instead of 20- or 30-year terms, can significantly reduce premiums. Smokers can later reassess their needs and reapply for new coverage when in better health or after quitting tobacco completely.

Frequently Asked Questions

Why are life insurance rates higher for smokers?

Smokers face higher life insurance rates because tobacco use increases health risks like heart disease, cancer, and stroke. Insurers view smokers as higher-risk applicants due to shorter average life expectancy. This increased risk leads to higher premiums to offset potential claims. Even occasional smoking can trigger higher rates, regardless of general health, making it essential for smokers to compare quotes for the best available options.

Can I get life insurance if I vape or use nicotine products?

Yes, you can get life insurance if you vape or use nicotine products, but insurers typically classify you as a smoker. Most companies require a nicotine test, and a positive result usually leads to higher premiums. However, some insurers offer more favorable rates for vapers compared to traditional smokers. It's best to shop around and disclose your usage honestly to find the most competitive policy.

How can smokers find the best life insurance rates?

Smokers can find the best life insurance rates by shopping around and comparing quotes from multiple insurers. Some companies specialize in high-risk applicants and offer better rates for smokers. Improving overall health, quitting smoking, and choosing term life insurance can also reduce costs. Working with an independent agent helps identify insurers with favorable underwriting guidelines for tobacco users.

Yes, quitting smoking can significantly lower your life insurance premiums. Most insurers require you to be nicotine-free for at least 12 months before reclassifying you as a non-smoker. After reclassification, you may qualify for lower rates. Be prepared to pass a medical exam showing no nicotine use. Inform your provider to potentially reduce your premiums and save money over the policy term.

Leave a Reply