What Is An Illustration In Life Insurance

An illustration in life insurance is a detailed projection that outlines how a policy is expected to perform over time based on specific assumptions.

It provides a breakdown of premiums, death benefits, cash values, and other policy details, helping policyholders understand the financial dynamics of their coverage. These illustrations are commonly used with permanent life insurance, such as whole or universal life, where cash value accumulation and performance projections are key features.

While illustrations offer valuable insights, they are not guarantees, as actual results may vary based on interest rates, policy performance, and individual circumstances. Understanding an illustration is essential for making informed decisions about long-term coverage and financial planning.

General Liability Insurance For Texas Businesses

General Liability Insurance For Texas BusinessesWhat Is an Illustration in Life Insurance?

An illustration in life insurance is a detailed projection document provided by insurers to help policyholders or prospective buyers understand how a life insurance policy—particularly permanent life insurance such as whole or universal life—may perform over time under various assumptions.

It outlines projected values including the death benefit, cash value accumulation, premiums, and other policy features based on a set of estimated or guaranteed rates, such as interest rates, mortality charges, and expense fees. These illustrations serve as educational tools, not guarantees, allowing consumers to visualize the long-term financial behavior of a policy under different scenarios, including best-case, worst-case, and assumed interest rate performance.

According to regulations from bodies like the National Association of Insurance Commissioners (NAIC), insurers must clearly disclose which values are guaranteed and which are non-guaranteed, helping to prevent misleading sales practices.

Types of Life Insurance Illustrations

There are primarily two types of illustrations in life insurance: illustrated illustrations and narrated illustrations.

Gym Business Insurance Cost

Gym Business Insurance CostA replacement illustration is used when a policyholder is considering replacing an existing policy with a new one, and it must include side-by-side comparisons of both policies to highlight differences in benefits, costs, and performance. Meanwhile, a surrender illustration may be provided when a policy is being surrendered for its cash value, showing the financial consequences of that decision.

Additionally, insurers often provide policy illustrations at the time of application, showing how premiums, cash value, and death benefits may grow over time. These documents must adhere to strict regulatory standards to ensure transparency, including the separation of guaranteed versus non-guaranteed elements.

Key Components of a Life Insurance Illustration

A comprehensive life insurance illustration includes several critical components that help assess the policy's potential performance.

These include the premium amount and payment frequency, death benefit (both level and increasing options), cash value accumulation, policy loans, surrender charges, and projected dividends (in the case of participating whole life policies). The illustration also specifies assumed interest rates, mortality costs, and expense charges, with clear distinctions between what is guaranteed and what relies on future performance.

Health Insurance Company Business Plan

Health Insurance Company Business PlanFor example, a non-guaranteed interest rate may be used to project higher cash value growth, but must be accompanied by a low-end scenario using minimum guaranteed rates to show downside risk. This transparency allows consumers to make informed decisions based on both optimistic and conservative projections.

Regulatory Standards and Consumer Protections

Life insurance illustrations are subject to regulatory oversight to prevent misleading or overly optimistic sales presentations. In the United States, the NAIC Life Insurance Illustrations Model Regulation sets guidelines that require insurers to use standardized formats, disclose assumptions clearly, and emphasize non-guaranteed elements.

Agents must deliver illustrations only with a policy summary and obtain a signed acknowledgment from the client. Additionally, illustrations must include disclaimers stating that projected values are not guarantees and that policy performance may vary.

The regulations also prohibit the use of unrealistic interest rate assumptions and require that illustrations show performance under various economic scenarios, including a 120% benchmark, which assumes a 1% higher cost of insurance, to assess policy resilience under less favorable conditions.

Health Insurance For Large Businesses

Health Insurance For Large Businesses| Component | Description | Guaranteed? |

|---|---|---|

| Premium Payments | The amount and frequency of payments required to keep the policy active. | Yes, if specified |

| Death Benefit | The amount paid to beneficiaries upon the insured’s death, which may be level or increase. | Partially (basic benefit guaranteed) |

| Cash Value | The savings or investment portion of the policy that grows over time, often used for loans or withdrawals. | No (non-guaranteed in most cases) |

| Dividends | Profits returned to policyholders in participating whole life policies; used to reduce premiums or increase cash value. | No (non-guaranteed) |

| Surrender Charges | Fees applied if the policy is surrendered early; usually decrease over time. | Yes |

Understanding Illustrations in Life Insurance: A Comprehensive Guide

How do you obtain a life insurance illustration for policy comparison?

How to Request a Life Insurance Illustration from an Agent or Broker

To obtain a life insurance illustration for policy comparison, the first step is to contact a licensed insurance agent or broker.

These professionals have direct access to insurer software that generates official illustrations based on your personal information, health profile, and financial goals. You will need to provide details such as your age, gender, health history, lifestyle habits (like smoking), and the coverage amount you're considering.

Once you submit this information, the agent inputs it into the insurance company’s illustration system to produce a detailed document showing projected premiums, death benefits, cash values (for permanent policies), and other key financial details over time. Reviewing illustrations from multiple agents representing different insurers can give you a broader perspective on available options.

Health Insurance Small Business Arizona

Health Insurance Small Business Arizona- Contact a licensed life insurance agent or broker with experience in the type of policy you're considering.

- Share your personal and medical history accurately to ensure the illustration reflects realistic projections.

- Request formal illustrations for specific policies you’re interested in and verify that the document includes all required disclosures.

Obtaining Illustrations Directly from Insurance Companies

Many insurance carriers allow consumers to receive life insurance illustrations through their official websites or customer service departments.

While a direct request might require working with a representative, some companies offer online tools or portals where you can begin the process independently. You typically complete a preliminary application or inquiry form, after which a company representative follows up to gather additional details and generate a personalized illustration.

This approach ensures that the figures come straight from the source and are fully compliant with regulatory standards. Additionally, requesting illustrations from multiple insurers directly enhances transparency and helps avoid potential bias from third-party agents.

- Visit the websites of reputable life insurance companies to check if they offer online illustration tools.

- Submit an inquiry form with your basic information and request a personalized policy illustration.

- Follow up with the insurer’s representative to clarify assumptions used in the illustration, such as interest rates or premium increases.

Using Online Comparison Platforms to Access Illustrations

Digital insurance marketplaces and independent comparison platforms provide another efficient way to obtain life insurance illustrations for side-by-side evaluation. These platforms often partner with multiple insurance carriers and licensed agents, enabling users to input their details once and receive several illustrated policies from different companies.

While these tools typically don’t generate standalone illustrations as formal documents, they summarize key elements such as premiums, benefits, and policy performance in an easy-to-compare format. It’s essential to ensure the platform is reputable and that the information presented is based on current insurer data and not generic estimates.

- Select a trusted online insurance comparison platform that works with A-rated insurers and provides detailed policy breakdowns.

- Enter your demographic and health information accurately to generate relevant policy options and projected costs.

- Request full illustrations through the platform’s agent network to get official documents for thorough analysis and legal compliance.

What Is an Illustration in Life Insurance and How Does It Work?

What Is a Life Insurance Illustration?

- A life insurance illustration is a document provided by insurance companies that outlines the projected performance of a life insurance policy, particularly permanent life insurance such as whole life or universal life.

- It includes details like premium payments, cash value accumulation, death benefits, and potential policy loans or withdrawals over time, based on certain assumptions.

- These illustrations are not guarantees but rather projections designed to help applicants understand how the policy might perform under specific conditions, such as assumed interest rates or dividend scales.

How Are Life Insurance Illustrations Used During the Application Process?

- During the underwriting process, agents use illustrations to demonstrate how different policy features, such as premium amounts and coverage levels, affect long-term benefits and costs.

- They help applicants compare various policy options by showing side-by-side projections of cash values, surrender charges, and coverage duration.

- Regulators require that illustrations disclose whether they are based on current or guaranteed values, ensuring transparency so consumers can distinguish between optimistic scenarios and minimum contractual obligations.

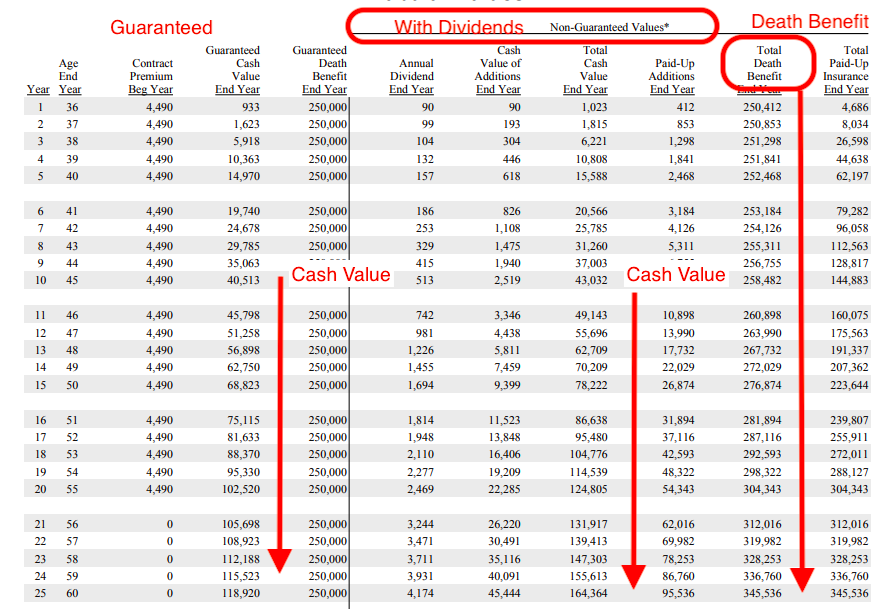

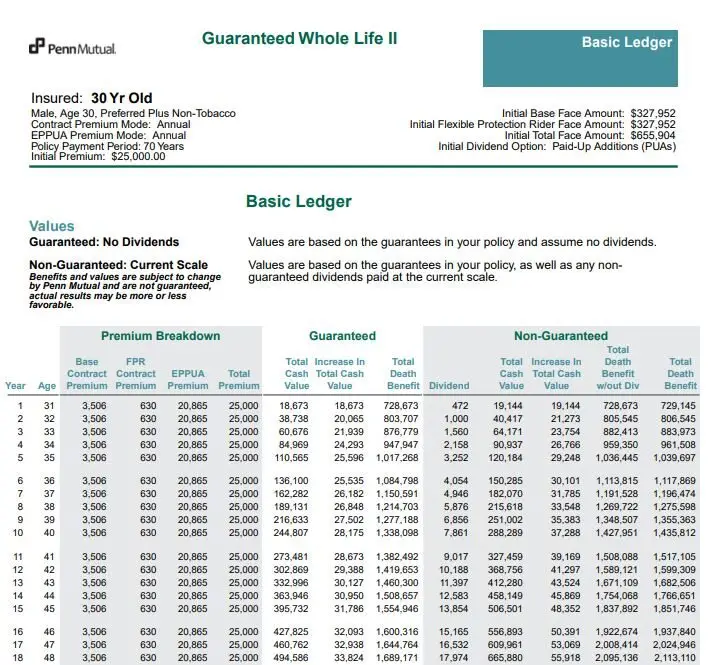

What Key Elements Are Included in a Life Insurance Illustration?

- A typical illustration includes the policy's face amount (death benefit), scheduled premium payments, and the breakdown of how premiums are allocated between insurance costs, administrative fees, and cash value growth.

- It displays projected cash surrender values over time, showing how much the policyholder could access if they surrender the policy or take out a loan.

- The illustration also notes any assumptions used, such as interest crediting rates, mortality charges, and expense loads, which can significantly impact long-term performance if actual experience differs from projections.

Is a life insurance benefit illustration a guaranteed payout?

No, a life insurance benefit illustration is not a guaranteed payout. It is a projection or estimate of future benefits and policy values based on a set of assumptions, including interest rates, mortality costs, and expense charges.

While it provides valuable insight into how a policy might perform under certain conditions, especially for permanent life insurance policies like whole or universal life, the numbers shown—particularly those related to cash value growth and death benefits—are often based on non-guaranteed elements.

Only the guaranteed values, typically shown in a separate column within the illustration, represent what the policyholder is contractually entitled to receive if all premiums are paid and no changes occur. Non-guaranteed elements, such as projected dividends or credited interest rates, may change over time and are subject to the insurer's future experience and discretion.

What Is Included in a Life Insurance Benefit Illustration?

A life insurance benefit illustration includes various components that outline both guaranteed and non-guaranteed elements of the policy over time. Insurers use these documents to show policyholders how premiums paid may accumulate in cash value, how death benefits could grow, and when the policy might be considered fully paid up (if applicable).

The illustration typically presents information in a year-by-year format and includes details such as annual premiums, cost of insurance charges, administrative fees, illustrated interest rates, and potential dividends.

It also differentiates between guaranteed values—those backed by the insurance company’s contract—and non-guaranteed values, which are speculative and based on current assumptions that may not hold true in the future.

- The illustration includes both guaranteed minimums and illustrated (projected) values, allowing comparison between conservative and optimistic scenarios.

- For participating whole life policies, projected dividends are often included, though these are not guaranteed and depend on the insurer’s future financial performance.

- Some illustrations show multiple scenarios, such as low and high interest rate environments, to demonstrate how changes in economic conditions could affect policy performance.

What Makes Certain Elements of an Illustration Non-Guaranteed?

Certain aspects of a life insurance illustration are labeled as non-guaranteed because they are based on current assumptions that insurers may adjust over time.

These assumptions include credited interest rates, dividend scales, riders, and expense factors. For example, a universal life policy might show a current interest rate that exceeds the minimum guaranteed rate; while the policy may earn this higher rate initially, there is no assurance it will continue in future years.

Similarly, dividend payments on participating whole life policies depend on the insurance company’s investment returns, claims experience, and operating expenses—all of which can fluctuate. As a result, high-performing projections in the illustration may not reflect the actual benefits received over the life of the policy.

- Interest rates above the minimum guaranteed rate are subject to change annually and are influenced by market performance and company policy.

- Dividends, while historically paid by mutual insurers, are not contractual obligations and can be reduced or discontinued.

- Riders, such as accelerated death benefits or cost-of-living adjustments, may have conditions that affect their future availability or cost.

How to Interpret Guaranteed vs. Non-Guaranteed Values in an Illustration?

Understanding the difference between guaranteed and non-guaranteed values is essential when evaluating a life insurance benefit illustration.

Guaranteed values are the minimum amounts the policy will provide if all required premiums are paid and no withdrawals or loans are taken. These are the only figures the insurer is legally bound to deliver. Non-guaranteed values, often displayed in a separate column, represent potential outcomes based on ideal conditions but are not assured.

Policyholders should pay close attention to the guaranteed section to assess worst-case scenario performance. Regardless of how attractive the illustrated non-guaranteed numbers may appear, they should not be relied upon as the expected outcome.

- Always look for the Guaranteed column in the illustration, which shows the minimum death benefit, cash surrender value, and premium requirements throughout the policy’s life.

- Be cautious of illustrations emphasizing high cash value growth or early premium pay-off, especially when based on non-guaranteed assumptions that are unlikely to persist over decades.

- Request updated illustrations periodically, particularly during significant interest rate changes or policy anniversaries, to compare how projections align with actual performance.

Frequently Asked Questions

What Is An Illustration In Life Insurance?

An illustration in life insurance is a document that shows how a policy is expected to perform over time. It includes projections of premiums, cash values, death benefits, and other values based on assumptions like interest rates and mortality costs. While not guaranteed, it helps policyholders understand potential outcomes. It's commonly used with permanent life insurance policies like whole or universal life to demonstrate long-term financial benefits under various scenarios.

Why Are Life Insurance Illustrations Important?

Life insurance illustrations are important because they help consumers understand how a policy might perform in the future. They provide a clear view of projected premiums, cash value growth, and death benefits, aiding in decision-making. Illustrations allow comparisons between policies and highlight the impact of different premium payments or policy changes. While projections are not guarantees, they offer valuable insights into the potential long-term value and performance of permanent life insurance under various financial assumptions.

Are The Projections In A Life Insurance Illustration Guaranteed?

No, the projections in a life insurance illustration are not guaranteed. They are estimates based on assumptions about future interest rates, investment performance, and expenses. Actual policy performance may differ due to changes in these factors. For example, lower-than-expected interest rates can reduce cash value growth. While insurers must follow regulations when creating illustrations, policyholders should understand that illustrated values represent potential, not promised, outcomes and should review them critically with an agent.

What Should I Look For In A Life Insurance Illustration?

When reviewing a life insurance illustration, look for key details like premium amounts, death benefit projections, cash value growth, and policy loans or withdrawals. Check the assumed interest rates and expense charges, as these impact performance. Compare guaranteed vs. non-guaranteed elements. Ensure the time frame matches your financial goals. Review how changes in payments or loans affect the policy. Always ask your agent to explain terms you don't understand and consider requesting multiple scenarios to assess long-term viability and risks.

Leave a Reply