Best Life Insurance For 50 Year Old

As people reach age 50, securing the right life insurance becomes increasingly important for protecting loved ones and ensuring financial stability.

At this stage, factors like health, coverage needs, and budget play a crucial role in determining the best policy. Whether you're looking for affordable term life insurance or a permanent solution like whole or universal life, understanding your options is essential.

Many insurers offer competitive rates and flexible plans tailored to individuals in their 50s. This guide explores the top life insurance policies available, helping you make an informed decision based on value, reliability, and long-term benefits.

Costco Business Insurance For Small Business

Costco Business Insurance For Small BusinessBest Life Insurance Options for 50-Year-Olds: Finding the Right Coverage

At age 50, many individuals begin reevaluating their financial protection strategies, making it a pivotal time to secure or reassess life insurance. With increasing responsibilities—such as mortgage payments, college funding for children, or planning for retirement—it's essential to have a policy that provides both security and peace of mind.

The best life insurance for a 50-year-old typically balances affordability, coverage duration, and flexibility, depending on personal and family needs. Options like term life insurance, whole life insurance, and universal life insurance offer distinct benefits. For instance, term life is often more cost-effective for those seeking coverage for a set number of years, while permanent policies provide lifetime protection and potential cash value accumulation.

Health, lifestyle, and financial goals play a significant role in selecting the most suitable plan, and shopping around through reputable providers can yield competitive rates despite rising premiums at this age.

Term Life Insurance: Affordable and Time-Specific Protection

Term life insurance is often the most cost-effective choice for 50-year-olds who need substantial coverage for a defined period, such as until retirement or until a mortgage is paid off.

Drywall Business Insurance Georgia

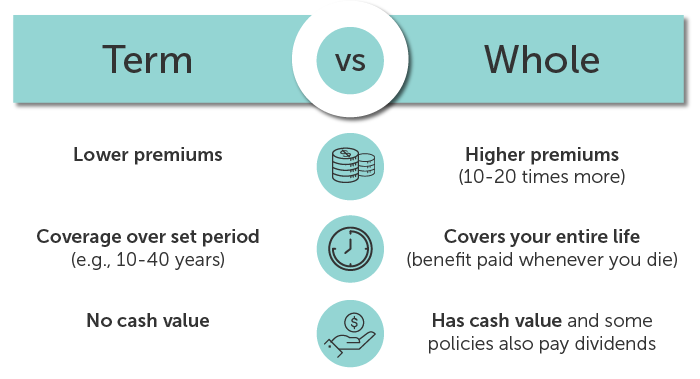

Drywall Business Insurance GeorgiaThese policies offer a level premium for the duration of the term—typically 10, 15, 20, or 30 years—and provide a death benefit if the insured passes away during that time. Since they do not accumulate cash value, term policies come with lower premiums than permanent options, making them ideal for budget-conscious individuals.

For someone turning 50 in good health, securing a 15- or 20-year term can lock in favorable rates before age further increases mortality risk and insurance costs. Convertible term policies also offer the flexibility to switch to a permanent plan later, without requiring additional medical underwriting, which can be valuable if health declines over time.

Whole Life Insurance: Lifelong Coverage with Cash Value Growth

Whole life insurance provides permanent coverage with guaranteed death benefits, fixed premiums, and the ability to build cash value over time—a feature that appeals to 50-year-olds looking for both protection and financial planning tools.

The premiums are significantly higher than term life, but they remain level for life, and a portion of each payment goes into a tax-deferred cash account that grows at a guaranteed rate. This accumulated cash can be borrowed against or withdrawn for emergencies, supplementing retirement income, or funding other long-term goals.

Drywall Business Insurance Massachusetts

Drywall Business Insurance MassachusettsFor individuals with dependents, estate planning needs, or final expense concerns, whole life offers predictability and stability. While less flexible than other permanent policies, its guaranteed benefits make it a trusted option for those prioritizing long-term security over cost savings.

Universal life insurance stands out for its flexibility, making it an attractive option for 50-year-olds seeking customizable coverage and the potential for cash value growth.

Unlike whole life, universal life allows policyholders to adjust their premium payments and death benefit within certain limits, adapting to changing financial circumstances. There are different types—such as indexed universal life and variable universal life—which tie cash value growth to market indices or investment performance, offering higher return potential (with increased risk).

This makes it suitable for those who are financially literate and interested in integrating life insurance into broader wealth-building strategies. However, it requires careful management to avoid lapse due to insufficient cash value, especially if premiums are lowered for extended periods.

Drywall Business Insurance Ohio

Drywall Business Insurance Ohio| Policy Type | Best For | Average Monthly Cost (Age 50) | Key Benefits | Considerations |

|---|---|---|---|---|

| Term Life | Temporary coverage, budget-conscious buyers | $40–$80 (20-year term, $500k coverage) | Low premiums, simple structure, convertible options | No cash value; expires after term |

| Whole Life | Lifetime protection, estate planning | $300–$600 (policy with $250k coverage) | Guaranteed cash value, fixed premiums, forced savings | High cost, less flexibility |

| Universal Life | Customizable policies, cash value growth | $200–$500 (based on coverage and type) | Flexible premiums, adjustable death benefit, market-linked growth (in some types) | Requires active management; risk of lapse |

Best Life Insurance Options for 50-Year-Olds: A Comprehensive Guide

What is the most suitable life insurance policy for a 50-year-old?

Types of Life Insurance Policies Suitable for a 50-Year-Old

At age 50, individuals have several life insurance options tailored to their financial situation, health, and long-term goals.

The most commonly considered policies include term life insurance, whole life insurance, and universal life insurance. Term life insurance provides coverage for a specific period, typically 10 to 30 years, and is often more affordable, making it ideal for those seeking temporary protection such as covering a mortgage or children's education.

Whole life insurance offers lifelong coverage with a cash value component that grows at a guaranteed rate, appealing to individuals looking for both protection and an investment element. Universal life insurance offers flexibility in premium payments and death benefits, allowing policyholders to adjust their coverage as financial needs evolve. Each type has pros and cons, so the choice depends on the individual’s objectives, budget, and risk tolerance.

Evaluate The Insurance Company Insureon On Business Personal Property Insurance

Evaluate The Insurance Company Insureon On Business Personal Property Insurance- Term life insurance is often the most cost-effective choice for healthy 50-year-olds who need coverage for a defined period, such as until retirement or when a mortgage is paid off.

- Whole life insurance may suit those who want lifelong protection and are interested in building cash value that can be borrowed against in the future.

- Universal life insurance is ideal for individuals seeking adjustable premiums and death benefits, offering more control over the policy’s structure based on changing financial needs.

Factors to Consider When Choosing a Policy at Age 50

Selecting the right life insurance policy at 50 requires evaluating several personal and financial factors. Health status plays a critical role, as insurers use medical history and current conditions to determine eligibility and premium rates.

A person in good health may qualify for lower premiums, especially with term insurance. Financial obligations are another key consideration—individuals supporting dependents, paying off a mortgage, or saving for a spouse’s retirement may need higher coverage amounts. Additionally, future income needs, such as replacing lost wages or covering final expenses, should influence the decision.

Premium affordability is also essential; while permanent policies offer lifelong benefits, they can be significantly more expensive than term options. Finally, long-term goals like leaving a legacy or funding estate taxes may make permanent insurance more attractive despite the higher cost.

- Health plays a major role in determining eligibility and premium costs, making medical underwriting a crucial step in the application process.

- Assessing existing debts, income replacement needs, and future financial responsibilities helps in determining the adequate coverage amount.

- Long-term financial planning, including estate considerations and potential tax liabilities, can influence the decision to choose permanent over term coverage.

Benefits of Purchasing Life Insurance at Age 50

Purchasing life insurance at 50 offers several strategic benefits, even though premiums are higher than for younger applicants. One advantage is the opportunity to lock in coverage before potential health declines in later years, which could make obtaining insurance more difficult or expensive.

A well-chosen policy can provide financial security for a spouse, especially if retirement savings are insufficient or one spouse earns significantly less. It can also help cover estate taxes, ensuring that assets are passed on to heirs without being liquidated.

Furthermore, permanent life insurance policies accumulate cash value over time, which can serve as a supplemental source of funds during retirement. Even term policies purchased at 50 can be valuable in protecting dependents during critical financial transition periods like paying off long-term debts or funding college tuition.

- Securing coverage at 50 allows individuals to get favorable rates before potential health issues arise in their 60s or beyond.

- Life insurance enhances financial stability for surviving spouses, particularly in covering day-to-day living expenses after the loss of income.

- Certain policies, especially those with cash value, offer dual benefits by providing a death benefit and a potential source of financial liquidity in retirement.

Is whole life insurance a smart choice for a 50-year-old seeking long-term coverage?

Long-Term Financial Protection and Stability

For a 50-year-old seeking lasting coverage, whole life insurance provides guaranteed protection as long as premiums are paid, making it a reliable vehicle for long-term financial planning.

Unlike term life insurance, which expires after a set period, whole life remains in force for the insured’s entire life, ensuring beneficiaries receive a death benefit regardless of when the policyholder passes away. This permanence is particularly valuable for individuals concerned about leaving behind final expenses, debt, or a financial legacy.

- Whole life policies offer a fixed death benefit that does not decrease over time, offering consistent peace of mind for estate planning and end-of-life costs.

- Premiums remain level throughout the policyholder’s life, allowing for predictable budgeting without the risk of future increases due to aging or health changes.

- The forced savings component, through cash value accumulation, can serve as a supplemental financial resource during retirement or emergencies.

Cash Value Accumulation and Living Benefits

One of the defining features of whole life insurance is its ability to build cash value over time, which grows at a guaranteed rate and can be accessed during the policyholder’s lifetime. For a 50-year-old, this presents a unique opportunity to grow a tax-advantaged asset that supports long-term financial goals. The cash value serves as a financial cushion and can be borrowed against or withdrawn, albeit with certain restrictions and implications.

- Cash value grows tax-deferred, meaning gains are not subject to annual income taxes as long as funds remain within the policy.

- Policy loans allow access to funds without triggering taxable events, provided the policy remains active and loans are managed responsibly.

- Over time, the cash value can become a substantial portion of the policy’s total value, offering flexibility for retirement income or legacy planning strategies.

Cost and Affordability Considerations at Age 50

While whole life insurance delivers numerous benefits, its higher premiums compared to term insurance can be a significant consideration for individuals approaching retirement. At age 50, applicants are often balancing competing financial priorities such as mortgage payments, children’s education, and retirement savings, making cost a critical factor in determining suitability.

- Premiums for whole life insurance are substantially higher than term policies, sometimes costing five to ten times more for similar death benefit amounts.

- Committing to lifelong premium payments requires long-term financial stability, which may not align with everyone’s retirement income projections.

- Alternatives such as term life with living benefits riders or a combination of term and investment accounts may deliver similar outcomes at a lower cost, depending on individual goals.

What Is the Best Life Insurance Policy for Someone Turning 50?

Understanding Life Insurance Needs at Age 50

Turning 50 is a pivotal moment to reevaluate personal finances and long-term protection strategies. At this stage, individuals often have a clearer picture of their financial responsibilities and future goals.

Assessing life insurance needs becomes essential, especially if dependents, a mortgage, or future estate planning are factors. Many people in their 50s still carry financial obligations such as children’s education, retirement savings, or supporting aging parents.

Life insurance at this age provides a safety net that ensures loved ones won’t face financial hardship if something unexpected occurs. Additionally, health changes around this age can affect insurability and premiums, making it a prime time to secure coverage.

- Identify current financial obligations such as mortgages, debts, or college tuition that would impact your family.

- Evaluate future expenses like funeral costs or estate taxes that your beneficiaries might incur.

- Consider how much income replacement your family would need if you were no longer there to provide.

Comparing Term vs. Permanent Life Insurance

The two main types of life insurance—term and permanent—offer different advantages suited to varying financial goals.

Term life insurance provides coverage for a set period, typically 10, 20, or 30 years, and is often the most cost-effective option for individuals around age 50 who need substantial coverage without a high premium. It’s ideal if the goal is to protect income during the remaining working years or until major debts are paid off.

Permanent life insurance, on the other hand, such as whole or universal life, lasts a lifetime and includes a cash value component that grows over time. While significantly more expensive, it may be suitable for estate planning or leaving a legacy.

- Choose term life insurance if you need affordable, temporary protection aligned with specific financial timelines.

- Opt for permanent life insurance if you seek lifelong coverage and are interested in accumulating cash value.

- Compare quotes from multiple insurers to assess affordability, especially since premiums rise with age and health status.

Factors That Influence Policy Choice After 50

Selecting the best life insurance policy after turning 50 depends on several personal factors including health, budget, and long-term objectives. Your current medical history plays a major role; many applicants undergo medical underwriting, which can affect both eligibility and premium rates.

Smokers, for example, typically pay higher premiums. The amount of coverage needed varies widely—some may only require a small policy to cover final expenses, while others may need larger policies to replace income or fund trusts. Additionally, financial flexibility, such as access to savings or other assets, can influence whether a term or permanent policy makes more sense.

- Review your health status and consider applying sooner rather than later, as health often declines with age.

- Assess how much you can comfortably spend on monthly or annual premiums without straining your budget.

- Determine whether your goals include burial expense coverage, income replacement, or wealth transfer across generations.

What is the average cost of the best life insurance for a 50-year-old?

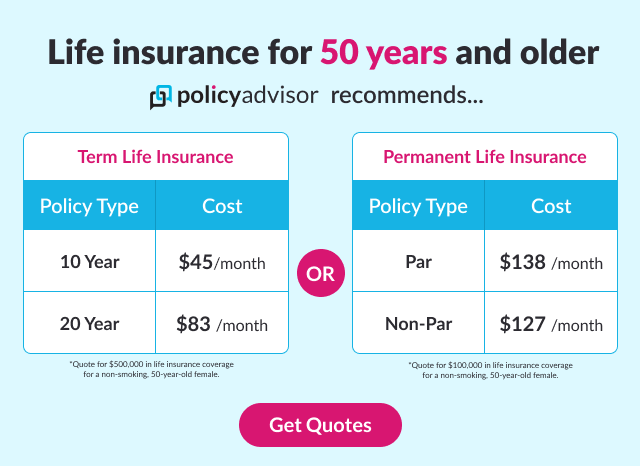

The average cost of the best life insurance for a 50-year-old varies significantly based on multiple factors, including health, coverage amount, policy type, and lifestyle. Generally, a healthy 50-year-old can expect to pay between $40 and $100 per month for a 20-year term life insurance policy with a death benefit of $500,000.

Permanent life insurance policies, such as whole life, are considerably more expensive, often ranging from $300 to $800 monthly for similar coverage. Premiums are typically lower for individuals in excellent health, non-smokers, and those with no significant medical history. Shopping around and comparing quotes from top-rated insurers ensures access to the most competitive rates tailored to personal circumstances.

Factors Influencing Life Insurance Costs at Age 50

- Health status is one of the most critical determinants; insurers evaluate conditions like high blood pressure, diabetes, or heart disease, which can raise premiums or lead to policy denial.

- Lifestyle choices such as smoking, excessive alcohol consumption, or participation in high-risk activities (e.g., skydiving) can result in higher rates due to increased mortality risk.

- Family medical history and personal medical records obtained through underwriting play a substantial role, as genetic predispositions to certain illnesses may affect long-term risk assessment.

Term vs. Permanent Life Insurance for 50-Year-Olds

- Term life insurance is often the most cost-effective choice, providing coverage for a set period (e.g., 10, 20, or 30 years), ideal for those needing protection through retirement or while dependents are financially dependent.

- Permanent life insurance, including whole or universal life, offers lifelong coverage and includes a cash value component that grows over time, making it suitable for estate planning or legacy goals, though at a significantly higher cost.

- Many 50-year-olds opt for term policies to maximize coverage within a budget, especially when the primary goal is income replacement or mortgage protection rather than asset accumulation.

How to Obtain the Best Rates at Age 50

- Compare multiple quotes from reputable insurers, as pricing models differ; even individuals with similar profiles can receive varying offers based on the company’s risk evaluation criteria.

- Improve insurability by quitting smoking, managing chronic conditions, and maintaining a healthy weight, which could lead to better underwriting classifications and lower premiums.

- Consider purchasing coverage sooner rather than later, as delaying increases both age-based premiums and the risk of developing health issues that could disqualify applicants from preferred rate tiers.

Frequently Asked Questions

What type of life insurance is best for a 50-year-old?

The best life insurance for a 50-year-old often depends on their financial goals. Term life insurance is typically more affordable and ideal for temporary needs like mortgage protection or income replacement. Whole life insurance offers lifelong coverage and builds cash value, making it suitable for long-term estate planning. Many people at this age choose 10- to 20-year term policies to cover debts or support dependents until retirement.

How much life insurance should a 50-year-old have?

A 50-year-old should generally have life insurance that covers 7–10 times their annual income, but exact needs vary. Consider outstanding debts, mortgage balance, children’s education, and funeral costs. Also, factor in income replacement if dependents rely on your earnings. A common approach is using the DIME method (Debt, Income, Mortgage, Education). Consulting a financial advisor helps determine a precise coverage amount based on personal circumstances and future goals.

Is life insurance more expensive at age 50?

Yes, life insurance is more expensive at age 50 compared to younger ages because insurers consider older applicants higher risk due to increased health concerns and shorter life expectancy. Premiums rise significantly with age, so purchasing coverage before 50 can save money. However, healthy 50-year-olds can still find competitive rates by shopping around, maintaining good health, and choosing term life insurance, which is generally more affordable than permanent policies.

Can a 50-year-old with health issues get life insurance?

Yes, a 50-year-old with health issues can still get life insurance, though options may be more limited and premiums higher. Insurers evaluate conditions like high blood pressure, diabetes, or heart disease during underwriting. Some companies specialize in high-risk applicants. Guaranteed issue or simplified issue policies require no medical exam but have higher rates and lower coverage amounts. Disclosing all medical information accurately ensures the best possible offer based on your health profile.

Leave a Reply