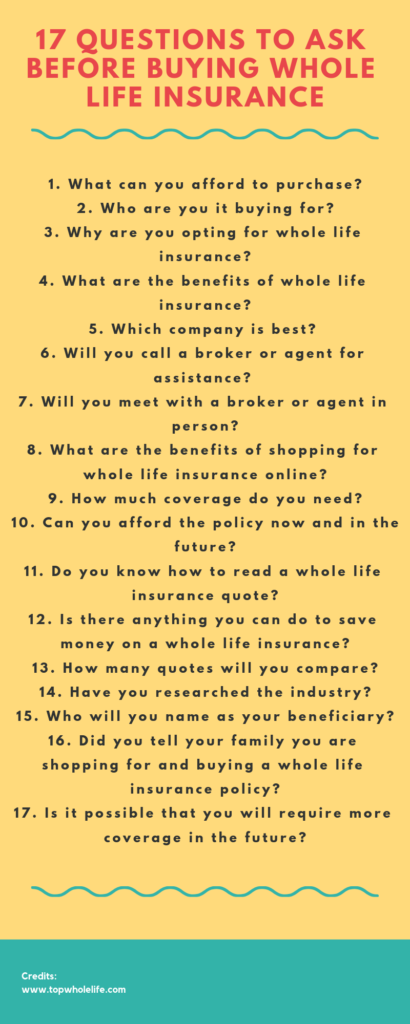

Questions To Ask Before Buying Life Insurance

Choosing life insurance is a critical decision that requires careful thought and planning. With numerous policies and providers available, it’s essential to ask the right questions before making a commitment. Understanding your financial needs, dependents, and long-term goals can help determine the coverage you require.

Key considerations include the type of policy, term length, premium costs, and potential cash value. It’s also important to evaluate the insurer’s reputation, financial strength, and customer service. Asking detailed questions ensures you select a plan that offers real protection and peace of mind for your loved ones.

Key Questions To Ask Before Buying Life Insurance

Understanding what to ask before purchasing life insurance is essential to securing the right coverage for your financial situation and future goals.

Finance And Insurance Business Relocation

Finance And Insurance Business RelocationLife insurance is not a one-size-fits-all product, and making an informed decision requires careful consideration of your needs, budget, and long-term objectives. By asking the right questions upfront, you can avoid underinsuring or overpaying, and ensure that your loved ones are adequately protected in the event of your death.

From determining how much coverage you need to understanding policy types and exclusions, thoughtful inquiry can guide you toward a policy that aligns with your personal and family requirements.

How Much Coverage Do I Really Need?

Determining the appropriate amount of life insurance coverage depends on several personal factors, including your income, debts, living expenses, and future financial obligations such as mortgage payments, children’s education, or retirement planning.

A common rule of thumb is to purchase a policy worth 10–15 times your annual income, but this may vary depending on your specific circumstances. For example, if you have significant savings, investments, or other sources of income for your dependents, you may need less coverage.

Financial Institutions Business Insurance

Financial Institutions Business InsuranceIt's important to evaluate your family's financial needs, account for final expenses like funeral costs and medical bills, and consider any outstanding debts, such as a mortgage or student loans. An accurate assessment ensures that your policy provides meaningful support without creating unnecessary financial strain through excessive premiums.

What Type of Life Insurance Is Best for Me?

Choosing between term life, whole life, or universal life insurance depends on your financial goals and how long you need coverage.

Term life insurance offers affordable protection for a specified period—commonly 10, 20, or 30 years—and is ideal if you need coverage during your working years or until major debts are paid off. In contrast, permanent life insurance (such as whole or universal life) provides lifelong coverage and includes a cash value component that grows over time and can be borrowed against.

While permanent policies have higher premiums, they can serve dual purposes: as insurance and a financial asset. Consider whether you want simple, temporary protection or a long-term investment vehicle when evaluating which type best suits your needs.

Frederick Business Insurance

Frederick Business InsuranceWhat Exclusions or Limitations Should I Be Aware Of?

Every life insurance policy comes with specific exclusions that outline situations in which the insurer will not pay the death benefit.

Common exclusions include suicide within the first two years of the policy, death resulting from illegal activities, or engagement in hazardous hobbies like skydiving or racing. Some policies may also exclude coverage for pre-existing medical conditions if they were not disclosed during the application process.

Contestability periods, typically lasting two years, allow insurers to investigate the cause of death and the accuracy of information provided on the application. Being aware of these limitations helps prevent claim denials and ensures you understand exactly when and how your beneficiaries will receive the benefit.

| Question | Why It Matters | Key Considerations |

|---|---|---|

| How much coverage is needed? | Ensures your dependents are financially protected. | Income replacement, debts, education costs, funeral expenses. |

| What policy type fits my goals? | Determines affordability and duration of coverage. | Term vs. permanent, cash value, premium costs. |

| What exclusions apply? | Prevents claim denials and surprises for beneficiaries. | Suicide clause, hazardous activities, contestability period. |

Essential Questions to Ask Before Purchasing Life Insurance

What should you ask before purchasing life insurance?

Free Online Business Insurance Quote Quebec

Free Online Business Insurance Quote QuebecWhat Coverage Amount Is Right for My Situation?

Determining the appropriate coverage amount is one of the most critical decisions when purchasing life insurance. It’s essential to evaluate your current financial obligations and future needs to ensure your beneficiaries are adequately protected.

A common rule of thumb is to aim for a policy worth 10 to 15 times your annual income, but individual circumstances can vary significantly. Reviewing debts, children's education costs, mortgage balances, and ongoing living expenses helps paint a clearer picture.

- Assess total financial dependents, including children, spouse, or elderly parents who rely on your income.

- Calculate outstanding debts such as mortgages, car loans, credit card balances, and potential future education costs.

- Consider funeral and administrative expenses, which can range significantly and add financial burden to loved ones.

What Type of Life Insurance Policy Fits My Needs?

Life insurance comes in various forms, primarily term life and permanent life insurance, each with distinct features and benefits.

Term life provides coverage for a specific period and is typically more affordable, making it suitable for temporary needs like income replacement during working years. Permanent life insurance, including whole and universal life, offers lifelong coverage and includes a cash value component, but usually comes with higher premiums.

- Determine whether your need for coverage is temporary (e.g., until children are grown) or lifelong (e.g., estate planning or legacy goals).

- Compare the premium costs and duration of term policies with the long-term benefits and investment-like features of permanent policies.

- Ask about policy flexibility, such as options to adjust premiums, extend coverage, or borrow against the cash value in permanent plans.

Insurers use several personal factors to determine your premium rates and whether you qualify for coverage. These factors include age, health history, lifestyle habits, occupation, and even your driving record. Understanding how these variables impact your policy helps you make informed choices and possibly take steps to improve your insurability before applying.

- Review your medical history and be prepared to undergo a medical exam, as conditions like diabetes, high blood pressure, or a family history of serious illness can affect rates.

- Be transparent about habits such as smoking, alcohol use, or participation in high-risk activities like skydiving, as these often lead to higher premiums.

- Consider how your occupation and travel habits influence risk; jobs involving hazardous work or frequent international travel might affect eligibility or pricing.

What key factors should you evaluate before purchasing life insurance?

Assessing Your Financial Needs and Dependents

Before purchasing life insurance, it is essential to evaluate your current financial obligations and identify individuals who depend on your income.

Understanding how much financial support your family would need in your absence helps determine the appropriate coverage amount. This includes ongoing expenses such as mortgage payments, utilities, food, education costs, and any outstanding debts.

Additionally, you should consider future financial goals like college funding for children or retirement savings that may be impacted by your death. By analyzing these factors, you can establish a clear picture of how much life insurance you truly need to provide security for your loved ones.

- Calculate total monthly and annual living expenses for your household to ensure coverage meets day-to-day needs.

- Identify all dependents—such as children, a spouse, or aging parents—who rely on your income for financial stability.

- Estimate future financial commitments including education costs, weddings, or long-term care that should be accounted for in coverage.

Choosing the Right Type of Life Insurance Policy

Selecting the correct type of life insurance is crucial, as different policies serve distinct financial goals and timeframes.

The two primary categories are term life insurance and permanent life insurance. Term life provides coverage for a specific period, such as 10, 20, or 30 years, and is generally more affordable. It suits individuals seeking temporary protection during high-liability periods like raising children or paying off a mortgage.

Permanent life insurance, which includes whole and universal life, offers lifelong coverage and accumulates cash value over time. It is typically more expensive but can serve as both insurance and an investment tool. Your choice should align with your financial strategy, budget, and long-term objectives.

- Evaluate whether you need temporary protection (term life) or lifelong coverage with cash accumulation (permanent life).

- Compare premium costs and long-term value between term and permanent policies based on your financial situation.

- Consider whether the cash value component of permanent insurance fits within your broader wealth-building or estate planning goals.

Reviewing Health, Age, and Lifestyle Factors

Insurers assess your health, age, and lifestyle to determine your risk profile, which directly affects your premium rates and eligibility. Generally, the younger and healthier you are when you purchase a policy, the lower your premiums will be.

Medical conditions such as diabetes, heart disease, or a history of cancer can increase costs or limit coverage options. Lifestyle factors like smoking, alcohol consumption, participation in high-risk hobbies, or even your occupation may also influence your rates. Undergoing a medical exam is often part of the application process, so being aware of your health status beforehand can help you anticipate outcomes and shop more effectively.

- Obtain a current health evaluation to understand any conditions that may impact your insurability or premium costs.

- Consider applying for life insurance at a younger age to lock in lower rates before potential health changes occur.

- Be transparent about lifestyle habits such as smoking or travel to high-risk areas, as inaccuracies can lead to denied claims.

What are the four key elements of life insurance to consider before purchasing a policy?

1. Coverage Amount and Beneficiary Needs

When determining the right life insurance policy, one of the most critical factors is establishing the appropriate coverage amount. This ensures that your beneficiaries can maintain their financial stability after your passing.

The coverage should be sufficient to replace lost income, pay off outstanding debts such as mortgages or loans, cover funeral expenses, and fund future needs like education or retirement. To arrive at an accurate figure, it’s essential to evaluate your current financial obligations and the long-term needs of your dependents.

- Calculate total financial obligations, including debts, mortgage balance, and children’s education costs.

- Estimate future income that your family would lose if you were no longer able to provide.

- Adjust the coverage amount based on inflation and expected lifestyle needs of your beneficiaries.

2. Type of Life Insurance Policy

Selecting the correct type of life insurance is fundamental, as policies vary significantly in structure and benefits. The two primary categories are term life and permanent life insurance.

Term life provides coverage for a specific period—typically 10, 20, or 30 years—and is generally more affordable. Permanent life insurance, such as whole or universal life, offers lifelong coverage and includes a cash value component that grows over time. The choice depends on your financial goals, budget, and how long you need protection.

- Choose term life for temporary coverage needs, such as income replacement during working years.

- Select permanent life insurance if you want lifelong protection and potential cash accumulation.

- Compare premium costs, flexibility, and long-term benefits of each policy type before deciding.

The cost of premiums plays a major role in determining which life insurance policy is sustainable for your budget. Premiums are influenced by factors such as age, health, lifestyle, coverage amount, and policy type. It's important to find a balance between affordable payments and adequate coverage, ensuring that you can maintain the policy without financial strain. Some policies offer level premiums that remain constant, while others may increase over time, especially with certain types of permanent insurance.

- Obtain multiple quotes from different insurers to compare rates for the same coverage level.

- Consider how premium payments will fit into your monthly or annual budget over the long term.

- Understand whether the premium is fixed or can change, and under what conditions adjustments may occur.

What five key factors should you consider when evaluating life insurance coverage?

1. Coverage Amount and Financial Needs

When evaluating life insurance coverage, determining the appropriate amount of protection is essential to ensure that your beneficiaries are financially secure after your death.

A common rule of thumb is to aim for a policy that covers 10 to 15 times your annual income, but this should be tailored to your unique situation. Consider outstanding debts, future expenses such as mortgages or children’s education, and the ongoing cost of living for dependents.

- Evaluate total household expenses to understand how much support dependents will need annually.

- Account for specific future costs like college tuition or wedding expenses.

- Subtract any existing savings, investments, or other sources of income to determine the gap insurance should cover.

2. Type of Life Insurance Policy

Choosing the right type of life insurance—term, whole, universal, or variable life—depends on your financial goals, budget, and coverage duration needs. Term life insurance offers affordable coverage for a set period, making it ideal for temporary needs such as a mortgage or raising children.

Permanent policies, like whole or universal life, provide lifelong coverage with a cash value component, which can be useful for estate planning or as a supplemental savings tool.

- Assess whether you need temporary protection (term) or lifelong coverage (permanent).

- Compare premiums and long-term value, as permanent policies are typically more expensive.

- Understand how cash value accumulation works and whether it aligns with your financial strategy.

3. Health, Age, and Lifestyle Factors

Insurers use your health, age, and lifestyle to determine your risk profile and premium rates. The younger and healthier you are when applying, the lower your premiums will typically be.

Pre-existing medical conditions, smoking, alcohol use, and high-risk hobbies can increase rates or affect eligibility. A medical exam is often required, so being transparent and prepared improves the application process.

- Apply earlier in life to lock in lower rates even if coverage is not immediately needed.

- Improve health markers such as BMI, blood pressure, or cholesterol before applying.

- Avoid or reduce high-risk behaviors like smoking or extreme sports to qualify for better rates.

Frequently Asked Questions

What types of life insurance are available?

There are two main types: term life and permanent life insurance. Term life provides coverage for a specific period, such as 10 to 30 years, and is generally more affordable. Permanent life insurance, including whole and universal life, offers lifelong coverage and includes a cash value component. Each type serves different financial goals, so consider your long-term needs and budget when choosing.

How much coverage do I really need?

To determine the right coverage amount, consider debts, income replacement, funeral costs, and future expenses like education. A common rule is 10–15 times your annual income, but personal circumstances vary. Use online calculators or consult a financial advisor to estimate your needs accurately. The goal is to ensure your family can maintain their lifestyle and meet financial obligations after your passing.

Premiums are influenced by age, health, lifestyle, occupation, and coverage amount. Younger, healthier individuals usually pay less. Smoking, high-risk hobbies, or certain medical conditions can increase costs. Insurers also review your family medical history and may require a medical exam. Shopping around and comparing quotes helps find the best rate for your situation and coverage needs.

Can I modify my policy after purchasing it?

Some policies allow adjustments, such as increasing coverage, extending terms, or adding riders. Term policies may offer conversion to permanent insurance. However, changes often require underwriting and could affect premiums. Review your policy’s terms and discuss options with your provider. Planning ahead and choosing a flexible policy can help accommodate future life changes like marriage, children, or increased financial responsibilities.

Leave a Reply