Term And Whole Life Insurance Difference

Term and whole life insurance are two fundamental types of life insurance, each serving different financial needs and long-term goals.

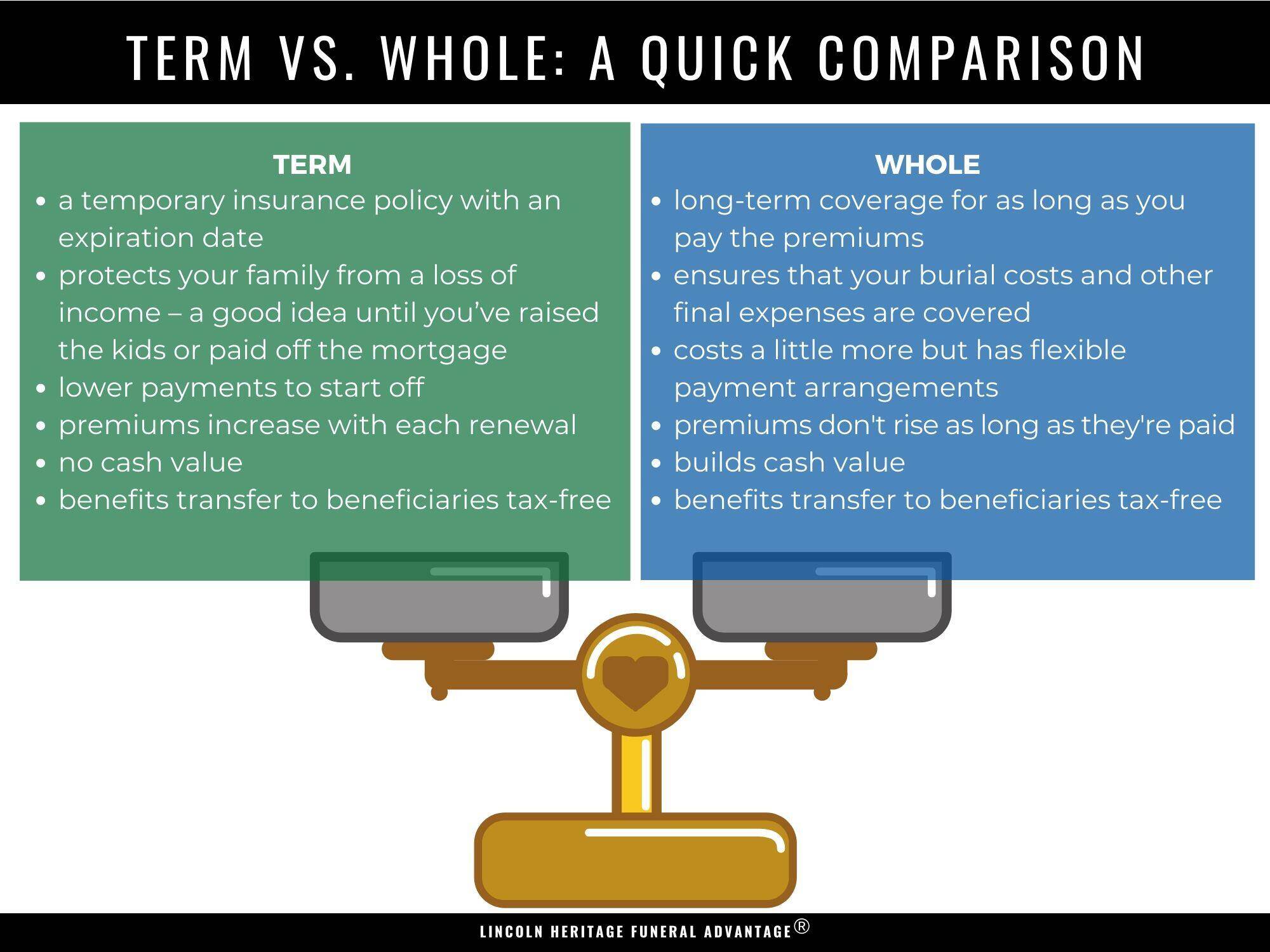

Term life insurance provides coverage for a specific period, typically offering affordable premiums and a death benefit paid only if the policyholder passes away during the term. In contrast, whole life insurance is a form of permanent coverage that lasts a lifetime, includes a cash value component that grows over time, and generally comes with higher premiums.

Understanding the key differences between these policies—such as duration, cost, and benefits—is essential for making an informed decision based on individual financial objectives and family protection needs.

Free Online Business Insurance Quote Quebec

Free Online Business Insurance Quote QuebecKey Differences Between Term and Whole Life Insurance

Understanding the fundamental distinctions between term and whole life insurance is essential when choosing the right coverage for your financial goals. Term life insurance provides coverage for a specific period—typically 10, 20, or 30 years—and pays a death benefit if the insured passes away during that term.

It’s known for its affordability and simplicity, making it an attractive option for those seeking temporary protection, such as covering a mortgage or children’s education. In contrast, whole life insurance is a type of permanent life insurance that offers lifelong coverage and includes a cash value component that grows over time at a guaranteed rate.

This cash value can be borrowed against or withdrawn, adding a financial flexibility that term policies lack. While whole life premiums are significantly higher, they remain fixed throughout the policyholder’s life, ensuring predictability. Choosing between the two depends on your financial needs, long-term goals, and budget.

Coverage Duration and Policy Lifespan

The most apparent difference between term and whole life insurance lies in the duration of coverage. Term life insurance is designed to provide protection for a defined period, such as 10 to 30 years.

Geico Auto Business Insurance

Geico Auto Business InsuranceIf the insured dies within this term, the death benefit is paid to the beneficiaries; however, if the term expires and the policy is not renewed or converted, the coverage ends with no payout. This makes term insurance ideal for individuals who need coverage during specific life stages, like raising children or repaying debt.

In contrast, whole life insurance guarantees coverage for the insured’s entire life, as long as premiums are paid. There is no expiration date, ensuring that the death benefit will be paid regardless of when the policyholder passes away. This lifelong protection is especially valuable for estate planning and leaving a legacy.

When comparing premium costs, term life insurance is generally much more affordable than whole life, particularly for younger and healthier individuals. This is because insurers are only on the hook for a limited time and do not accumulate cash value. Premiums for term policies are fixed for the duration of the term but can increase significantly upon renewal.

Whole life insurance, on the other hand, comes with much higher premiums due to its permanent nature and inclusion of a savings-like cash value component. These premiums are also guaranteed to remain level for life, which provides long-term predictability. While the initial cost may seem prohibitive, the lifetime coverage and financial benefits may justify the expense for some policyholders.

General Liability Business Insurance San Francisco CA

General Liability Business Insurance San Francisco CACash Value Accumulation and Investment Component

One of the defining features of whole life insurance is its ability to build cash value over time. A portion of each premium payment goes into a savings account that grows at a guaranteed interest rate.

This cash value is tax-deferred and can be accessed through withdrawals or policy loans, which can be used for emergencies, retirement income, or other financial goals. Policyholders can also borrow against the cash value without triggering a taxable event, as long as the policy remains active. In contrast, term life insurance does not accumulate any cash value—it solely provides a death benefit.

Because of this, term policies are considered pure insurance, offering no return on investment if the policy expires unused. For those interested in combining life insurance with a forced savings mechanism, whole life offers added financial utility.

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Coverage Duration | Temporary (e.g., 10–30 years) | Lifelong |

| Premium Cost | Lower, especially for younger buyers | Significantly higher |

| Cash Value | No cash value accumulation | Builds guaranteed cash value over time |

| Flexibility | Convertible or renewable in some cases | Loans and withdrawals allowed |

| Best For | Temporary needs, budget-conscious buyers | Estate planning, legacy goals, long-term savings |

Term vs Whole Life Insurance: Key Differences and What to Consider

What are the key differences between term and whole life insurance, and which might be more suitable for long-term coverage?

Key Differences in Policy Duration and Renewability

- Term life insurance provides coverage for a specific period, such as 10, 20, or 30 years, and does not offer lifelong protection. Once the term expires, the policyholder must either renew the policy, often at a significantly higher premium, convert to a permanent policy if the option is available, or let the coverage end.

- In contrast, whole life insurance guarantees coverage for the insured’s entire lifetime, as long as premiums are paid. This permanence makes it inherently different from term insurance, which may expire before the insured’s death, leaving beneficiaries without a death benefit.

- The renewability feature in term life is limited and typically results in cost increases with each renewal period, while whole life maintains a fixed premium schedule that does not rise with age, offering long-term predictability in payments.

Cash Value Accumulation and Investment Component

- One of the fundamental distinctions is that whole life insurance includes a cash value component that grows over time at a guaranteed rate set by the insurer. This cash value acts as a savings or investment feature, which the policyholder can borrow against or withdraw from during their lifetime.

- Term life insurance, on the other hand, does not accumulate any cash value. It is purely protective in nature, designed solely to provide a death benefit if the insured passes away during the policy term.

- The presence of cash value in whole life policies can make them significantly more expensive than term policies with similar death benefits. However, for individuals seeking both life insurance and a forced savings mechanism, this feature adds long-term financial utility beyond a simple death benefit.

Cost Structure and Suitability for Long-Term Coverage

- Premiums for term life insurance are generally much lower than those for whole life, especially for younger and healthier individuals. This affordability makes term insurance an attractive option for those seeking high coverage amounts during peak financial responsibility periods, such as when raising children or paying off a mortgage.

- Whole life insurance premiums are substantially higher due to the lifetime coverage guarantee and cash value accumulation. While the initial cost is steep, it remains level for the life of the policy, which can be beneficial in later years when health issues might make obtaining new coverage difficult or costly.

- For long-term coverage needs, whole life insurance is typically more suitable when the goal includes providing a guaranteed death benefit, estate planning, or leaving a legacy. Term insurance may be insufficient if coverage is needed beyond the policy period, unless it is converted or re-purchased, which can become cost-prohibitive with age.

Frequently Asked Questions

What is the main difference between term and whole life insurance?

The main difference is duration and cost. Term life insurance provides coverage for a specific period, such as 10 to 30 years, and pays a death benefit if you pass away during that term. It’s generally more affordable. Whole life insurance covers you for your entire life and includes a cash value component that grows over time, making it more expensive but also an investment-like feature.

Does term life insurance build cash value?

No, term life insurance does not build cash value. It is designed purely to provide a death benefit if the policyholder dies during the term. There is no savings or investment component. Once the term ends, the policy expires with no value. This makes it simpler and more affordable than whole life insurance, which includes a cash accumulation feature that can be borrowed against or withdrawn.

Can you convert term life insurance to whole life insurance?

Yes, many term life insurance policies are convertible, allowing you to switch to a whole life policy without a new medical exam. This option is usually available within a specific time frame, such as the first 10 years of the policy. Converting lets you gain lifelong coverage and cash value, but premiums will increase significantly due to the permanence and added benefits of whole life insurance.

Which is more expensive: term or whole life insurance?

Whole life insurance is significantly more expensive than term life insurance. Premiums for whole life are higher because it provides lifetime coverage and includes a cash value component that grows over time. Term life, in contrast, offers temporary coverage with no cash value, making it much more affordable, especially for younger, healthy individuals who only need coverage for a set number of years.

Leave a Reply