Compare Surrogate Life Insurance Policies Across Agencies

Choosing the right surrogate life insurance policy requires careful consideration and comparison across multiple agencies. With various providers offering different terms, premiums, and coverage options, navigating the market can be overwhelming.

These specialized policies are designed to protect intended parents and surrogates during the complex journey of surrogacy, addressing unique risks and financial concerns. Understanding the nuances between plans—such as payout structures, exclusions, and underwriting criteria—is essential.

Comparing policies from top insurance agencies ensures you secure comprehensive coverage that aligns with legal agreements and medical requirements. This guide examines leading providers, highlighting key features to help you make an informed, confident decision.

Insurance Business Strategy

Insurance Business StrategyCompare Surrogate Life Insurance Policies Across Agencies

When considering financial protection for intended parents during the surrogacy journey, surrogate life insurance plays a crucial role. These specialized policies are designed to cover the surrogate mother in case of death or critical illness during pregnancy or delivery, ensuring that the intended parents are not left with unexpected financial burdens.

However, coverage and eligibility vary significantly among insurance providers, making it essential to compare policies across multiple agencies. Factors such as the surrogate's age, medical history, geographic location, and the specific terms related to pregnancy complications can influence premiums and coverage limits.

A thorough comparison helps intended parents select a policy that offers optimal protection at a competitive price, while also meeting the legal and medical requirements of the surrogacy arrangement. Working with knowledgeable insurance brokers and using side-by-side evaluations can streamline this complex decision-making process.

Understanding What Surrogate Life Insurance Covers

Surrogate life insurance is designed to provide financial security in the event of a surrogate’s death during pregnancy or shortly after delivery. Most policies include a lump-sum death benefit payable to the intended parents or estate, which can be used to cover medical expenses, legal fees, or lost compensation paid to the surrogate.

Insurance For A Landscaping Business

Insurance For A Landscaping BusinessSome plans also offer a dismemberment or critical illness rider, providing partial payouts if the surrogate suffers a severe medical condition that prevents her from continuing the pregnancy. Importantly, coverage typically excludes pre-existing conditions or high-risk behaviors unless explicitly approved.

Understanding the specific inclusions and exclusions in each policy is critical—especially regarding complications like preeclampsia, gestational diabetes, or cesarean section risks—so intended parents can ensure the policy fully aligns with potential medical scenarios during the surrogacy process.

| Coverage Feature | Typical Inclusions | Common Exclusions |

|---|---|---|

| Death Benefit | Lump-sum payout (ranging from $250,000 to $2 million) | Deaths resulting from illegal activities or undisclosed pre-existing conditions |

| Critical Illness | Coverage for conditions like preeclampsia, organ failure, or stroke | Pre-symptomatic conditions not disclosed at application |

| Medical Expense Reimbursement | Partial reimbursement for hospitalization linked to pregnancy complications | Elective procedures or non-emergency treatments |

| Global Coverage | Valid in the U.S. and selected international clinics | War zones or high-risk travel locations |

Key Agencies Offering Surrogate Life Insurance Policies

Several specialized insurance agencies and underwriters provide surrogate life insurance, each with distinct underwriting standards and policy structures. Companies like Gallagher Assistance, Umbrella Life, and Global Financial Benefits are known for offering robust coverage tailored to third-party reproduction arrangements.

These agencies often partner with fertility clinics and surrogacy agencies to streamline the application process. Gallagher, for example, offers rapid underwriting with minimal medical red tape, while Umbrella Life provides customizable benefit tiers based on surrogate health profiles.

Insurance For Towing Business

Insurance For Towing BusinessIt's important to note that not all traditional life insurers cover surrogates—many standard policies exclude pregnancy-related death—so working with an agency experienced in reproductive health insurance significantly increases approval chances and ensures appropriate coverage terms.

Factors That Influence Policy Costs and Approval

The cost and approval of a surrogate life insurance policy depend on several risk assessment factors evaluated during underwriting. The surrogate’s age is a major consideration—women under 35 typically receive lower premiums due to lower maternal risk.

Pre-pregnancy health metrics such as BMI, smoking status, and reproductive history (including prior C-sections or fertility treatments) are thoroughly reviewed. Geographic location also impacts pricing, as states with higher maternal mortality rates may trigger higher premiums or stricter clauses.

Additionally, policies may require a paramedical exam or urine analysis to verify health disclosures. Intended parents should be prepared to provide detailed medical records and surrogacy agreements, as insurers often require proof that the arrangement complies with legal and ethical standards to approve coverage.

Insurance New Business Checklist

Insurance New Business ChecklistCompare Surrogate Life Insurance Policies Across Leading Agencies

Which surrogate agency offers the highest compensation with comprehensive life insurance coverage?

Top Surrogate Agencies with High Compensation and Life Insurance Benefits

- ConceiveAbilities is consistently recognized for offering competitive compensation packages, with base payments ranging from $60,000 to $100,000 depending on experience and location. They also provide comprehensive life insurance policies, typically valued at $500,000, which are fully covered by the intended parents and managed through reputable providers. Their structured program ensures surrogates are financially protected throughout the journey.

- Family Inceptions is another leading agency known for transparency in compensation and robust insurance offerings. Surrogates with this agency can earn between $55,000 and $90,000, with additional benefits including a $500,000 life insurance policy, long-term disability coverage, and legal support. The agency partners with A-rated insurers to guarantee reliable and accessible coverage.

- Extraordinary Conceptions stands out for its personalized compensation plans and enhanced insurance options. They offer base compensation starting at $60,000 and increasing with each successful surrogacy, along with an optional upgrade to $1 million in life insurance coverage. This flexibility makes them a preferred choice for surrogates seeking maximum financial and medical protection.

Factors Influencing Compensation and Insurance in Surrogacy Agencies

- Geographic location significantly affects compensation rates, with surrogates in states like California often receiving higher base payments due to lower legal risks and established surrogacy laws. Agencies adjust their offers based on state-specific regulations, which can also influence the type and extent of life insurance provided.

- Surrogate experience plays a crucial role—first-time surrogates generally receive lower compensation compared to repeat surrogates, who may earn 10–15% more. Agencies reward proven track records by increasing both base pay and insurance benefits as a way to encourage experienced surrogates to return.

- Medical and psychological screening requirements also impact the overall package. Agencies that conduct more rigorous health evaluations often pair this with stronger life insurance plans to mitigate risks. Comprehensive policies are seen as an investment in surrogate well-being and are standard among top-tier programs.

How Life Insurance Coverage Enhances Surrogate Protection

- Life insurance is a critical component in surrogacy agreements, ensuring that a surrogate's family receives financial support in the rare event of a pregnancy-related fatality. Agencies like Growing Generations and Surrogate First include this as a standard part of their contracts, with policies typically underwritten before the embryo transfer.

- The value of the policy often reflects the level of risk associated with surrogacy, and most reputable agencies offer minimum coverage of $250,000 to $500,000. Some programs allow surrogates to name beneficiaries, giving them control over who receives the payout, which adds an essential layer of personal security.

- These policies are fully funded by the intended parents, with premiums paid in advance. This removes financial burden from the surrogate and ensures uninterrupted coverage throughout gestation and postpartum recovery, reinforcing ethical standards in the surrogacy industry.

Which life insurance providers offer coverage for surrogate pregnancies?

Top Life Insurance Providers Offering Coverage for Surrogate Pregnancies

- Principal Financial Group is one of the few insurers that may consider life insurance for intended parents involved in surrogacy, particularly if the intended mother is not carrying the pregnancy. They evaluate applications based on medical history, age, and the specifics of the surrogacy arrangement, including legal contracts and medical screenings of the surrogate.

- Guardian Life has been known to provide coverage for intended parents undergoing surrogacy, especially when the embryo is genetically related to one or both parents. Guardian typically requires detailed medical records, a surrogacy agreement, and proof of embryo origin to assess risk and determine eligibility.

- John Hancock evaluates surrogacy cases on an individual basis and may offer policies to intended parents if comprehensive documentation is provided. This includes legal gestational carrier agreements, medical evaluations of the surrogate, and genetic links between the child and the applicants, ensuring alignment with the insurer's underwriting standards.

Key Requirements Insurers Evaluate for Surrogacy Coverage

- Legal documentation, including a fully executed gestational surrogacy agreement, is often required to verify that the intended parents are legally recognized as the child’s parents. Insurers use this to minimize legal and financial risk in the event of a claim.

- Medical records from the surrogate, including fertility treatments, pregnancy history, and current health status, are critical in assessing risk. Insurers analyze these to evaluate potential complications during the pregnancy that could impact the intended parents’ life insurance application.

- Genetic linkage between the intended parent(s) and the child is frequently a deciding factor. Policies are more likely to be approved when one or both parents contribute genetically, as insurers view this as a more stable family arrangement with stronger emotional and biological ties.

Challenges and Considerations in Obtaining Coverage

- Many insurers automatically classify surrogacy arrangements as high-risk, leading to declined applications or significantly higher premiums. This is due to perceived legal uncertainties and the complex medical and emotional factors involved in third-party reproduction.

- Some providers exclude coverage during active surrogacy pregnancies, offering policies only after the child is born and the intended parents have established guardianship. This delay can leave families vulnerable during a critical period.

- International surrogacy arrangements often face greater scrutiny, as legal frameworks vary across countries. Insurers may hesitate to approve applications involving cross-border surrogacy due to inconsistencies in parental rights and documentation standards.

What is the top-rated life insurance provider in the U.S. for surrogate policies across agencies?

Top Life Insurance Providers Offering Surrogate Policies in the U.S.

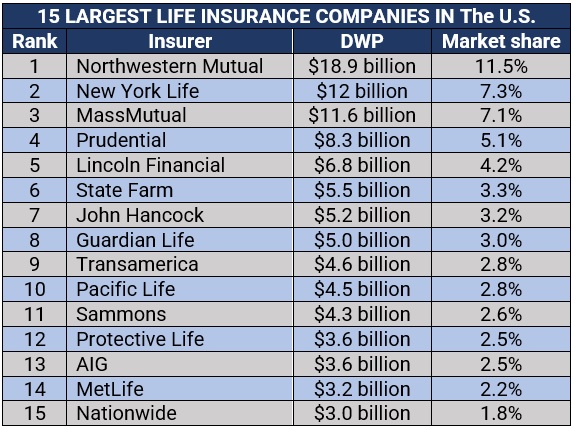

- Several top-rated life insurance companies in the United States offer coverage options tailored specifically for surrogates, though availability and underwriting criteria can vary significantly. Among the most frequently cited providers are New York Life, Northwestern Mutual, and Guardian Life. These insurers are recognized for their strong financial strength ratings, customer service, and comprehensive underwriting processes that accommodate the unique medical and ethical considerations associated with surrogacy. While no single provider is officially ranked as the definitive leader in surrogate-specific policies, these companies are often recommended by fertility specialists and reproductive law experts due to their experience handling complex cases involving third-party reproduction.

- New York Life is known for its flexibility in underwriting high-risk pregnancies, including surrogacy arrangements, and offers competitive premium rates backed by an AM Best A++ rating.

- Northwestern Mutual provides customizable term and permanent life insurance plans, with underwriters trained to evaluate surrogacy risks using individualized health assessments.

- Guardian Life regularly collaborates with fertility clinics and intended parent legal teams to structure policies that protect both the surrogate and the commissioning parties during pregnancy.

Underwriting Criteria for Surrogate Life Insurance Policies

- Insurers offering life insurance to surrogates typically apply specialized underwriting standards due to the elevated health risks associated with pregnancy, particularly in gestational carrier arrangements. These criteria often involve detailed medical evaluations, including pre-surrogacy health screenings, psychological assessments, and verification of prior successful pregnancies. Underwriters also consider factors such as the surrogate’s age, BMI, gestational history, and whether the pregnancy involves multiples. Because surrogacy is considered a higher-risk scenario, some insurers may impose coverage limitations or exclusions during the pregnancy term unless specific contractual agreements are in place with the agency or intended parents.

- Medical documentation is required, including obstetrical history, fertility treatment protocols, and a letter of explanation from the fertility clinic overseeing the surrogacy.

- Policies often include temporary restrictions or higher premiums during the gestational period, with rates normalized post-delivery if no complications occur.

- Insurers may require that surrogates are enrolled through accredited agencies with established medical and legal safeguards, reducing overall risk exposure for the provider.

Role of Insurance Agencies and Fertility Programs in Surrogate Coverage

- Independent insurance agencies and fertility benefit programs play a critical role in securing appropriate life insurance for surrogates by acting as intermediaries between insurers, intended parents, and reproductive legal teams. Specialized agencies such as Alternative Risk Solutions, Surrogate First, and Fertility & Life Insurance Advisors focus exclusively on third-party reproduction coverage and maintain relationships with multiple carriers to find the most favorable terms.

- These agencies assist in navigating complex applications, advocating for policy approvals, and ensuring that both the surrogate and intended parents are adequately protected. Their expertise increases the likelihood of obtaining comprehensive coverage, even for high-risk cases or previous claim histories.

- Agencies like Surrogate First offer bundled insurance solutions that include life, disability, and medical gap coverage tailored to surrogacy contracts and state-specific legal requirements.

- Collaboration with fertility programs enables real-time verification of medical protocols, improving underwriting transparency and speeding up the approval process.

- These agencies often provide educational resources to surrogates, helping them understand policy terms, beneficiary designations, and their rights during the insurance application process.

Frequently Asked Questions

What factors should I consider when comparing surrogate life insurance policies?

When comparing surrogate life insurance policies, consider coverage amounts, premium costs, waiting periods, and exclusions. Evaluate the financial strength of the insurance company and policy flexibility. Ensure the policy aligns with the surrogacy agreement and intended parents' needs. Review application requirements, such as medical exams and consent forms. Choose a policy that offers clear beneficiary designations and sufficient support throughout the surrogacy journey.

Insurance Options For Landscaping Business

Insurance Options For Landscaping BusinessWhy is it important to compare policies from multiple insurance agencies?

Comparing policies from multiple agencies helps identify the most comprehensive and affordable coverage. Different agencies offer varying terms, benefits, and limitations. Reviewing multiple options ensures you select a plan that meets specific surrogacy needs, such as maternity coverage and complications protection. It also helps avoid gaps in coverage and provides leverage in negotiations. A thorough comparison leads to better-informed decisions and financial security for all parties involved.

Can surrogate mothers get life insurance directly through surrogacy agencies?

Surrogacy agencies typically don’t provide life insurance directly but help surrogates obtain policies through partner insurers. The intended parents usually pay for the policy, which names them as beneficiaries. Agencies assist with the application process and ensure all legal and medical requirements are met. It's essential to work with reputable agencies that guide surrogates in selecting appropriate, licensed insurance providers for adequate coverage during the surrogacy process.

How does a surrogate's health history affect life insurance approval?

A surrogate's health history significantly impacts life insurance approval and premium rates. Insurers review medical records for conditions like hypertension, gestational diabetes, or prior complications. Healthy candidates with low-risk profiles are more likely to qualify for favorable terms. Full disclosure is essential, as misrepresentation can lead to denial or lapses in coverage. A thorough health evaluation ensures accurate risk assessment and appropriate policy selection for all parties.

Leave a Reply