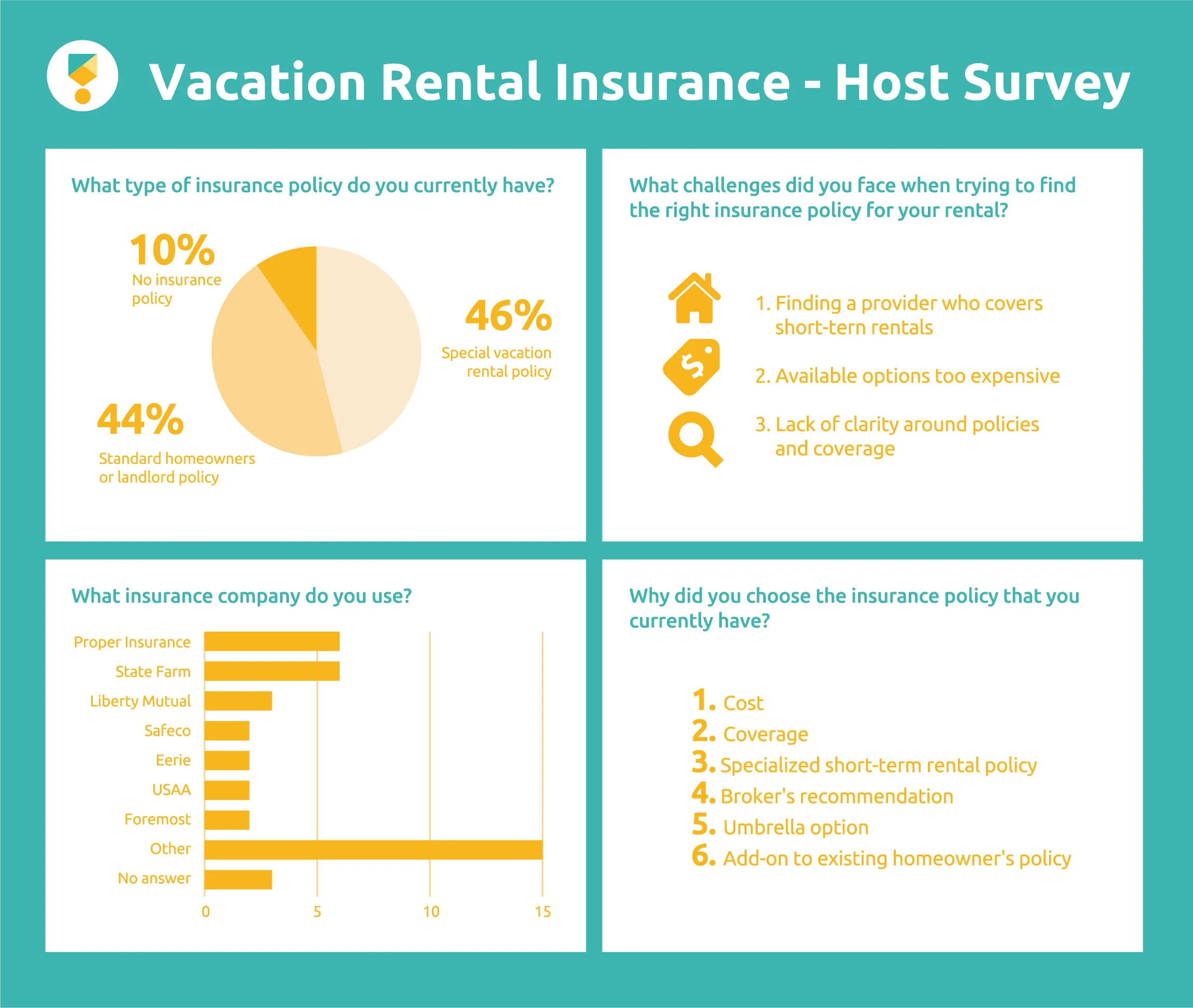

Do I Need Special Insurance For Airbnb

Running an Airbnb can be a rewarding way to earn extra income, but it also comes with risks that standard homeowners or renters insurance may not cover. Many property owners wonder whether they need special insurance for their short-term rentals.

The truth is, typical insurance policies often exclude coverage for guests or frequent rental activity, leaving hosts vulnerable to liability claims, property damage, or loss of income. Specialized Airbnb insurance or add-ons like host protection insurance can offer crucial protection. Understanding your policy options is essential to safeguarding your property, finances, and guests.

Do I Need Special Insurance For Airbnb?

If you're considering renting out your property on Airbnb, one of the most important questions to address is whether you need special insurance. Standard homeowners or renters insurance policies typically do not cover short-term rentals, especially if you’re regularly hosting guests for profit.

Does Special Event Insurance Cover Weather

Does Special Event Insurance Cover WeatherThis means that in the event of property damage, theft, or liability claims from guests, you could be left financially exposed. While Airbnb offers its own form of protection through the Airbnb Host Protection Insurance and the Airbnb Host Guarantee, these do not replace comprehensive coverage and may have limitations.

Therefore, it's often wise to explore dedicated short-term rental insurance or to amend your existing policy to include coverage for Airbnb hosting. Evaluating your needs based on frequency of rentals, property value, and local regulations can help determine the right level of protection.

Understanding Airbnb's Built-In Insurance Options

Airbnb provides two main layers of protection for hosts: the Host Guarantee and the Host Protection Insurance.

The Host Guarantee offers up to $1 million in coverage for damages to your property caused by guests, but it excludes high-value items like fine art or cash and is subject to certain terms and exclusions. On the other hand, Host Protection Insurance is liability coverage that also goes up to $1 million per occurrence, protecting you if a guest or third party sues you for bodily injury or property damage that happens during a stay.

How Much Is Special Event Liability Insurance

How Much Is Special Event Liability InsuranceWhile these programs offer a safety net, they are not substitutes for traditional insurance and do not cover damage you cause, intentional acts, or non-guest-related incidents. Therefore, relying solely on Airbnb’s protections may leave significant gaps in coverage.

When Standard Home Insurance Falls Short

Most standard homeowners insurance policies are designed for traditional residential use and often exclude coverage for short-term rentals, particularly if they’re conducted as a business.

If your property is rented frequently through Airbnb, insurers may consider it a commercial activity, which can void your policy or lead to denied claims. For example, if a guest is injured and files a liability claim, your standard policy might not respond because the incident occurred during a paid stay.

Some insurers offer endorsements or “riders” to extend existing coverage to include short-term rentals, but these vary widely by provider and location. It's crucial to contact your insurance agent to discuss your Airbnb activities and determine whether your current policy needs modification or replacement.

Do Off Grid Homes Require Special Insurance

Do Off Grid Homes Require Special InsuranceExploring Dedicated Short-Term Rental Insurance

A growing number of insurance companies now offer short-term rental insurance policies specifically designed for Airbnb hosts. These policies combine elements of home, business, and liability insurance, providing comprehensive coverage for both property damage and guest-related incidents.

They typically cover lost income due to property damage, theft of host belongings by guests, and legal expenses arising from liability claims. Pricing varies based on location, property value, and rental frequency, but for most hosts, the added cost is justified by the enhanced protection.

Unlike Airbnb’s built-in protections, these policies can offer broader coverage and greater peace of mind, especially in areas with strict regulations or higher risks. Shopping around and comparing quotes from insurers experienced in short-term rentals is a smart step before listing your property.

| Insurance Type | Coverage Highlights | Limitations |

|---|---|---|

| Standard Homeowners Insurance | Covers personal property and liability for personal use; may include limited guest coverage | Often excludes short-term rentals; may void policy if used commercially |

| Airbnb Host Guarantee | Up to $1 million in property damage protection from guests | Does not cover cash, pets, vehicles; exclusions for high-value items |

| Airbnb Host Protection Insurance | Liability coverage up to $1 million per occurrence | Does not cover host-caused incidents or non-guest claims |

| Short-Term Rental Insurance | Full coverage for property, liability, lost income, and guest incidents | Premiums can be higher; availability varies by location and insurer |

Do I Need Special Insurance for Airbnb? A Complete Guide

Do Airbnb Hosts Need Special Insurance Coverage?

UK Insurance Brokers Specializing In Risk Management

UK Insurance Brokers Specializing In Risk ManagementUnderstanding Standard Homeowners Insurance Limitations

- Standard homeowners insurance policies are typically designed for personal, non-commercial use of a property, meaning they may not cover damages or liabilities that occur when the home is used for short-term rentals like Airbnb.

- Most traditional policies explicitly exclude continuous or frequent rental activity, so filing a claim after an incident involving a guest might result in denial, leaving the host financially responsible.

- Insurance providers often consider short-term rentals a business activity, which requires different risk assessment and coverage scope than personal residence policies.

Types of Insurance Options for Airbnb Hosts

- Airbnb offers a Host Protection Insurance program that provides liability coverage in case a guest, third party, or even a neighbor files a claim for bodily injury or property damage caused by the host during a booking.

- Hosts can opt for a specialized short-term rental insurance policy which may include liability, property damage, loss of income, and coverage for guest injuries, tailored specifically for rental activities.

- Alternatively, adding a “dwelling fire” policy or an endorsement to an existing homeowners or renters insurance can extend protection to rental scenarios, though terms and availability vary by location and insurer.

Factors Influencing the Need for Specialized Coverage

- The frequency and nature of rentals play a significant role; hosts who rent out their property regularly or full-time face higher risks than those offering occasional rentals.

- The property’s location, value, and amenities such as pools or hot tubs increase potential liability, making additional insurance more critical.

- Local regulations may also require hosts to carry specific insurance amounts or types, especially in cities with strict short-term rental ordinances.

Do You Need Specific Insurance for Short-Term Rentals Like Airbnb?

Yes, you typically need specific insurance for short-term rentals like Airbnb, as standard homeowner’s or renter’s insurance policies often do not cover the unique risks associated with hosting guests for short durations.

While some homeowner’s insurance policies may offer limited liability coverage, they usually exclude commercial activities—such as renting out your property for profit—which is exactly what short-term rentals entail. Without proper insurance, property owners could face out-of-pocket expenses for damages, injuries, or loss of income due to unforeseen interruptions.

Several insurance options exist, including specialized short-term rental insurance policies, endorsements to existing policies, or coverage offered directly through platforms like Airbnb, but understanding which type suits your situation is essential.

What Is An Insurance Special Needs Plan

What Is An Insurance Special Needs Plan1. Limitations of Standard Homeowner’s Insurance for Short-Term Rentals

- Most standard homeowner’s insurance policies are designed for properties occupied by the owner or long-term tenants, not for transient guests. These policies commonly exclude coverage when a home is used for commercial purposes, and hosting short-term renters falls into this category.

- If a guest is injured on your property and you’re sued, your liability protection under a standard policy may be denied because the activity is considered business-related, not personal use.

- Additionally, damage caused by guests—such as vandalism or accidental fires—might not be covered, leaving you financially responsible for repairs and potential legal claims.

2. Types of Insurance Coverage Available for Short-Term Rentals

- Specialized short-term rental insurance policies are designed specifically for hosts and combine aspects of property, liability, and loss-of-use coverage, ensuring that both the structure and your income from rentals are protected.

- Some insurers offer endorsements or riders to existing homeowner’s policies that extend coverage to include short-term rental activities, but these vary by provider and location, and may require additional premiums.

- Airbnb and similar platforms often provide their own protection programs, such as Airbnb’s Host Protection Insurance, which offers liability coverage up to a certain amount. However, this does not replace property or income protection, and coverage limits and exclusions apply.

3. Factors Influencing the Need for and Type of Rental Insurance

- The location of your property plays a crucial role, as insurance regulations and risks vary by state or country. Areas prone to natural disasters or with high tourist traffic may require more comprehensive coverage.

- Whether you rent out an entire home or just a room can affect your insurance needs; whole-home rentals generally pose higher risks and may require broader policies.

- How often you host guests and whether you manage the property yourself or through a property management company also influence coverage requirements, as frequent rentals or third-party involvement may increase exposure to liability and property damage.

Frequently Asked Questions

Do I need special insurance for Airbnb as a host?

Yes, you should have proper insurance as an Airbnb host. Standard homeowner’s or renter’s insurance may not cover short-term rental activities. Airbnb offers Host Protection Insurance, which covers third-party claims of bodily injury or property damage. However, it doesn't replace home or liability insurance. Consider obtaining a specialized short-term rental insurance policy for comprehensive coverage tailored to hosting guests.

Does Airbnb provide insurance for property damage?

Yes, Airbnb offers a Host Guarantee that provides up to $3 million in protection for property damage caused by guests. This is not insurance but a damage protection program. It covers issues like broken electronics or ruined furniture but excludes theft, wear and tear, or damage by pets. Hosts should still consider additional insurance to fully protect their property against all potential risks.

Can my homeowner’s insurance cover Airbnb rentals?

Most standard homeowner’s insurance policies don’t cover short-term rentals like Airbnb. Regular policies assume long-term occupancy and may deny claims related to guest injuries or property damage. If you rent out your home, inform your insurer. They may offer an endorsement or require a specialized rental policy. Without proper coverage, you risk being financially responsible for damages or liability claims during guest stays.

Is guest insurance required when staying at an Airbnb?

Guests are not required to have special insurance to stay at an Airbnb. However, Airbnb provides a $1 million Host Liability Insurance for hosts, which indirectly benefits guests by ensuring hosts are covered in case of accidents. Guests should consider travel insurance for personal protection against trip cancellations, lost items, or medical emergencies. Always review the listing’s house rules and Airbnb’s terms for safety and coverage details.

Leave a Reply