Do I Need Special Insurance To Drive For Lyft

Driving for Lyft can be a flexible way to earn extra income, but it also raises important questions about insurance coverage. Personal auto insurance policies typically don’t cover accidents that occur while driving for a ridesharing service. This gap leaves drivers vulnerable to significant financial risk.

Lyft provides its own insurance, but coverage varies depending on the phase of the ride—waiting, en route, or transporting a passenger. Understanding these stages and the protection offered is crucial. Many drivers wonder if additional insurance is necessary to stay properly covered. The answer depends on individual policies, state regulations, and driving habits.

Do I Need Special Insurance To Drive For Lyft?

Yes, you do need special insurance considerations when driving for Lyft, as your personal auto insurance may not provide full coverage during all phases of rideshare driving.

Best UK Broker Offering Specialist Insurance

Best UK Broker Offering Specialist InsuranceWhile Lyft does offer its own insurance coverage for drivers, there are specific gaps and limitations depending on your activity within the app—such as being offline, waiting for a ride request, or actively transporting a passenger. Most personal auto insurance policies exclude coverage when the vehicle is used commercially, which includes driving for a rideshare service.

Therefore, relying solely on your personal policy can leave you at risk of denied claims or policy cancellation. To stay protected, it's essential to understand how Lyft’s insurance works in each period of operation and consider purchasing a rideshare-endorsed policy or additional commercial coverage that bridges any coverage gaps.

Understanding Lyft’s Three Periods of Insurance Coverage

Lyft provides insurance coverage that varies depending on which of the three operational periods a driver is in. Period 1 begins when the driver logs into the Lyft app but hasn’t accepted a ride request. During this time, Lyft offers limited liability coverage, typically $50,000 per person, $100,000 per accident for bodily injury, and $25,000 for property damage, but does not cover collision or comprehensive damage to the driver’s vehicle.

Period 2 starts when a driver accepts a ride request and ends when they pick up the passenger. Lyft provides increased liability coverage during this phase, along with uninsured motorist coverage and collision and comprehensive coverage if the driver has these coverages on their personal policy, often subject to a deductible.

What Are Special Damages In Insurance

What Are Special Damages In InsurancePeriod 3, when a passenger is in the vehicle, offers the most robust protection, including up to $1 million in liability coverage, plus full collision and comprehensive benefits. Drivers must understand these periods to ensure they’re adequately covered at every stage.

The Role of Personal Auto Insurance When Driving for Lyft

Your personal auto insurance is still necessary but has limitations when driving for Lyft. Most standard personal auto policies exclude coverage when the vehicle is used for commercial purposes, such as carrying passengers for pay.

This means that if you're involved in an accident while in Period 1 (logged into the app but not yet matched), your personal insurer might deny the claim since you're technically using the car for rideshare services. While some insurance companies offer rideshare endorsements that extend your personal policy to cover Period 1, others may require you to purchase a separate commercial policy. It's crucial to notify your insurance provider that you drive for Lyft so they can adjust your policy accordingly and avoid potential coverage lapses or claim denials.

A dedicated rideshare insurance policy is often the best way to ensure continuous protection throughout all phases of Lyft driving.

What Are Special Perils In Insurance

What Are Special Perils In InsuranceThese policies are designed specifically for rideshare drivers and can fill in the gaps left by both personal insurance and Lyft’s provided coverage. They typically cover periods when you're logged into the app but not yet on a trip (Period 1), which is when most personal policies stop offering protection.

Companies like Allstate, Progressive, and State Farm offer rideshare endorsements or full rideshare policies that integrate with both your personal use and commercial driving. Investing in this specialized coverage reduces the risk of out-of-pocket expenses after an accident and provides peace of mind, especially since being underinsured could result in legal and financial liability.

| Driving Period | Lyft Insurance Coverage | Personal Insurance Gaps |

|---|---|---|

| Period 1: App On, No Request Accepted | Limited liability only ($50k/$100k/$25k); no collision/comprehensive | Most personal policies exclude coverage here |

| Period 2: Ride Accepted, En Route to Passenger | Higher liability, collision and comprehensive (with deductible) | Only covered if you have rideshare endorsement |

| Period 3: Passenger in Vehicle | Up to $1 million liability, full collision/comprehensive | Generally well-covered by Lyft; personal policy may not apply |

Do I Need Special Insurance to Drive for Lyft? A Comprehensive Guide

What insurance coverage is required to drive for Lyft?

Personal Auto Insurance Requirements

Before driving for Lyft, drivers must have a valid personal auto insurance policy that meets their state’s minimum requirements. This includes liability coverage for bodily injury and property damage.

What Does Special Accident Insurance Cover

What Does Special Accident Insurance CoverWhile personal insurance is necessary to begin driving with Lyft, it does not cover the driver during all stages of a rideshare trip. Most personal insurance policies exclude coverage when the driver is using their vehicle commercially, which includes when the Lyft app is active but no ride has been accepted. Drivers are responsible for ensuring their current policy doesn't explicitly prohibit rideshare activity.

- Drivers must maintain a personal auto insurance policy in good standing.

- The policy must meet state-mandated minimum coverage levels for liability.

- Some personal insurance carriers may require additional rideshare endorsement or may cancel policies if commercial use is discovered.

Lyft’s Provided Insurance Coverage

Lyft provides supplemental insurance coverage that activates in specific stages of rideshare driving. This coverage includes liability, uninsured motorist protection, and contingent collision and comprehensive coverage, but only under certain conditions.

The supplemental insurance kicks in when the driver has the Lyft app turned on. Coverage limits vary depending on whether the driver is waiting for a ride request or actively transporting a passenger. Lyft's insurance is secondary during periods when no passenger is in the vehicle and primary once a ride is accepted.

- Period 1 (App On, No Request): Lyft provides $50,000/$100,000/$25,000 in liability coverage, but only after the driver’s personal insurance denies the claim.

- Period 2 (Request Accepted, En Route): Lyft’s coverage becomes primary with higher limits, typically $1 million in liability protection.

- Period 3 (Passenger in Car): The same $1 million liability coverage continues, plus additional protection for damage to the driver’s vehicle under certain circumstances.

Gap Coverage and Additional Options

There is a coverage gap during Period 1 when the app is on but no ride has been accepted. Most personal insurance policies do not cover this phase, and Lyft’s insurance acts as secondary only after the personal policy denies the claim.

To fill this gap, drivers may choose to purchase a personal rideshare insurance policy offered by certain insurance companies. These specialized policies extend personal coverage to include periods of commercial use and can prevent claim denials. Reviewing and possibly upgrading existing insurance is a proactive step for drivers to remain fully protected.

- Commercial rideshare endorsements from insurers like GEICO or State Farm can cover Period 1 when the app is active.

- These policies often blend personal and commercial coverage to ensure uninterrupted protection.

- Drivers should compare rates and coverage details before selecting a supplemental policy to avoid being underinsured during rideshare activity.

What Are the Lyft Driver Requirements That Could Disqualify You, Including Insurance?

Criminal History and Background Check Standards

Lyft conducts a comprehensive background check on all prospective drivers, and certain criminal convictions can result in disqualification. The company uses a third-party service to review both local and national criminal records, typically covering the past seven years.

While Lyft considers some factors like the nature and recency of offenses, specific convictions are almost always disqualifying. It's important to note that policies may vary slightly by city due to local regulations.

- Violent crimes such as assault, domestic violence, or homicide are automatic disqualifiers due to passenger safety concerns.

- Sex offenses, including any registered sex offender status, will result in immediate rejection regardless of when the offense occurred.

- Convictions related to drug trafficking, weapons possession, or driving under the influence (DUI) within the past seven years typically prevent approval.

Driving Record and Vehicle Safety Compliance

A driver’s motor vehicle record is scrutinized carefully during the application process, and poor driving history is a common reason for disqualification.

Lyft requires a valid driver’s license from the state of residence and typically mandates that applicants have at least one to three years of driving experience. Additionally, the vehicle used must meet Lyft’s safety and age requirements, which vary by location but generally include inspections and model year restrictions.

- Multiple moving violations, such as reckless driving, hit-and-run incidents, or excessive speeding tickets within the past three years, can lead to denial.

- Major infractions like driving without a license, driving with a suspended license, or accumulating too many points on a license are typically disqualifying.

- Vehicles that fail to meet Lyft’s model year minimums (usually 2000 or newer), lack required safety features, or show significant damage during inspection are not accepted.

Insurance Coverage and Liability Requirements

While drivers are not required to obtain special insurance at the time of applying, Lyft provides contingent insurance coverage that activates only when the driver is logged into the app and either waiting for a ride request or actively transporting a passenger.

However, applicants must have a personal auto insurance policy that meets their state’s minimum requirements. Gaps in coverage or using commercial insurance not compliant with Lyft’s partner programs may raise red flags during the application review.

- Drivers must maintain active personal auto insurance; lapses in coverage can delay or prevent approval until valid proof is provided.

- Using a vehicle insured under a commercial policy not affiliated with Lyft’s insurance partners may result in disqualification unless properly registered.

- Insurance claims history involving repeated at-fault accidents or fraudulent behavior could impact eligibility during Lyft’s risk assessment.

Can You Use Standard Auto Insurance for Uber Rides?

Does Personal Auto Insurance Cover Uber Driving?

Personal auto insurance policies are designed for private, non-commercial use of a vehicle. When it comes to driving for Uber, standard personal coverage typically does not extend to periods when you're actively working as a rideshare driver. Most personal auto insurance providers consider ridesharing a commercial activity, which changes the risk profile of the driver.

As a result, engaging in Uber rides without proper rideshare-specific coverage could leave you financially exposed in the event of an accident. Insurance companies often deny claims if they discover the vehicle was being used for commercial purposes at the time of the incident, even if the driver believed they were covered.

- Personal auto insurance usually excludes coverage during ridesharing, especially when the app is active or you have passengers.

- Insurance providers classify Uber driving as commercial use, which is not included under standard policy terms.

- Claims made during rideshare activity may be rejected if the insurer determines the vehicle was being used for business purposes.

When Does Uber’s Insurance Apply?

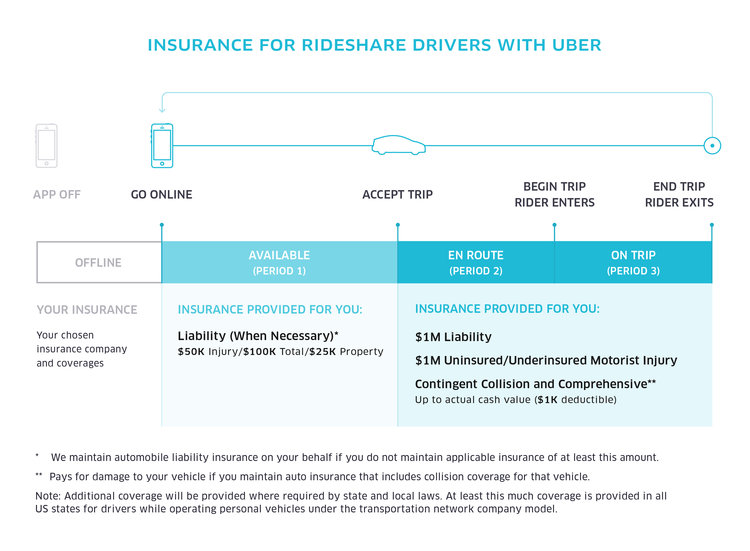

Uber provides its own insurance coverage, but it only activates during specific periods of your rideshare activity. Understanding these segments is critical to knowing when you’re protected and when you may need supplementary coverage.

Uber’s insurance kicks in during three main periods: when the app is on and you’re waiting for a ride request (Period 1), when you’re en route to pick up a passenger (Period 2), and when you have a passenger in the vehicle (Period 3). However, during gaps such as when the app is off, your personal or a rideshare-specific insurance policy is responsible for coverage.

- Period 1 (app on, no ride accepted) includes liability coverage, but with limitations compared to personal policies.

- Periods 2 and 3 offer higher liability limits and include collision and comprehensive coverage, subject to deductibles.

- There may be coverage gaps between personal insurance and Uber’s policy, particularly during low-activity times or vehicle downtime.

To bridge the gaps left by both personal auto insurance and Uber’s coverage, several insurance providers offer rideshare-specific insurance policies. These policies are designed to extend protection during all phases of ridesharing, including when the app is active but no ride has been accepted.

Rideshare insurance can be added as an endorsement to an existing policy or obtained as a standalone policy, depending on the insurer and state regulations. Drivers are encouraged to review their current coverage and discuss options with their insurance agent to ensure continuous protection.

- Some major insurers offer rideshare endorsements that activate when the Uber app is in use.

- Standalone rideshare insurance policies provide comprehensive coverage tailored to gig economy drivers.

- Availability and cost of rideshare insurance vary by state and insurance provider, requiring individual assessment.

Frequently Asked Questions

Do I need special insurance to drive for Lyft?

Yes, you need special insurance to drive for Lyft. Personal auto policies typically don’t cover you when driving for ride-sharing. Lyft provides commercial insurance during periods when you’re logged in and carrying passengers, but you need a rideshare-endorsed policy for full coverage. This ensures protection when you’re online without a ride or during passenger pickups, bridging the gap between personal and commercial coverage.

Does Lyft provide insurance for its drivers?

Yes, Lyft provides insurance for its drivers, but coverage varies by activity period. When you’re offline, your personal insurance applies. Once you log in to the app, Lyft offers contingent liability coverage. During trips with passengers, Lyft provides comprehensive insurance, including liability, collision, and uninsured motorist protection. However, for complete protection, especially during gaps in Lyft’s coverage, a rideshare-specific insurance policy is recommended.

If you don’t have rideshare insurance and get into an accident while driving for Lyft, your personal auto insurer may deny the claim. Many standard policies exclude commercial activities like ridesharing. This could leave you financially liable for damages, medical costs, or repairs. Without proper coverage during gaps in Lyft’s insurance—like when waiting for a ride request—you risk being underinsured or uninsured, resulting in significant out-of-pocket costs.

Can I use my personal car insurance for Lyft driving?

No, you cannot fully rely on personal car insurance when driving for Lyft. Most personal policies exclude commercial use, so they may not cover accidents that occur while you’re logged into the app. If you’re in an accident during gaps in Lyft’s coverage—such as when waiting for a ride request—your personal insurer might deny the claim, leaving you exposed. It’s safer to get a rideshare-endorsed policy for complete protection.

Leave a Reply