Do I Need Special Insurance To Doordash

Driving for DoorDash can be a flexible way to earn extra income, but it raises an important question: do you need special insurance? Standard auto insurance policies are designed for personal use and may not cover accidents that occur while delivering food.

Most insurers consider delivery driving a commercial activity, which could lead to denied claims or canceled coverage. While DoorDash provides some liability protection when you’re actively delivering, there are gaps, especially during the time between accepting a delivery and picking up the order. Understanding your coverage options and potential risks is crucial for anyone considering or already working with delivery platforms.

Do I Need Special Insurance To Doordash?

As a DoorDash driver, you might wonder whether you need special insurance to deliver food safely and legally.

Best UK Broker Offering Specialist Insurance

Best UK Broker Offering Specialist InsuranceThe short answer is that you don't need to purchase a separate commercial insurance policy specifically for DoorDashing, but your existing personal auto insurance may not fully cover you while delivering. DoorDash does provide some insurance coverage during specific periods of your delivery activity, such as when you’ve accepted a delivery and are en route to the restaurant or customer.

However, there are gaps in coverage, especially during the waiting for a dash phase. This raises concerns for drivers who rely on their personal vehicles for gig work. Understanding how personal, commercial, and platform-provided insurance interact is essential to protect yourself financially in the event of an accident.

Understanding DoorDash’s Built-in Insurance Coverage

DoorDash offers third-party liability insurance that activates during certain phases of the delivery process—specifically, once you accept a delivery request and are traveling to the restaurant or customer.

This coverage typically includes bodily injury and property damage liability, but it does not cover damage to your own vehicle or personal medical expenses. The policy limits vary by state and country, but generally fall within standard liability ranges (e.g., $1 million per incident).

What Are Special Damages In Insurance

What Are Special Damages In InsuranceIt’s crucial to note that this protection does not apply when you’re logged into the app but haven’t accepted a delivery yet. During this Period 0 phase, only your personal auto insurance would provide coverage, assuming it allows for delivery driving. Always verify the exact terms of DoorDash’s insurance through the app or their official resources.

How Personal Auto Insurance Applies While Doordashing

Most standard personal auto insurance policies are designed for non-commercial use, meaning they assume you're driving for personal reasons—not delivering food for pay.

Engaging in commercial activity like DoorDashing could, in theory, violate the terms of your personal policy, potentially leading to a denial of claims if the insurer discovers you were working during an accident. Some insurers offer rideshare or delivery endorsements that extend coverage to include gig economy activities, bridging the gap between personal use and commercial driving.

Companies like GEICO, Progressive, and State Farm have specific add-ons for rideshare and delivery drivers. If you plan to Dash regularly, it’s wise to notify your insurer and consider upgrading your policy to ensure continuous protection without risking claim denials.

What Are Special Perils In Insurance

What Are Special Perils In InsuranceWhile not required by DoorDash, obtaining rideshare or commercial insurance can provide added peace of mind.

These policies are tailored for gig economy drivers and fill the gaps left by both personal insurance and the limited coverage provided by DoorDash. A rideshare endorsement or commercial policy typically covers all periods of app usage, including when you’re waiting for a delivery request—a critical time when your personal insurance might fall short.

The cost varies depending on location and driving history, but it’s usually more affordable than a full commercial policy. For frequent Dashers or those who spend many hours online, investing in this type of coverage is a smart financial safeguard against potential out-of-pocket expenses in case of an accident.

| Insurance Type | Coverage During App Login (No Delivery Accepted) | Coverage After Accepting Delivery | Best For |

|---|---|---|---|

| Personal Auto Insurance | Limited to no coverage (depends on insurer and state) | May be void or limited during deliveries | Inactive or very occasional Dashers |

| DoorDash Insurance | No coverage | Yes (liability only) | Part-time Dashers during active deliveries |

| Rideshare/Commercial Insurance | Yes (full coverage) | Yes (comprehensive coverage) | Frequent or full-time gig drivers |

Do You Need Special Insurance for DoorDash Delivery? A Complete Guide

Can I use personal auto insurance for DoorDash deliveries?

What Does Special Accident Insurance Cover

What Does Special Accident Insurance CoverDoes Personal Auto Insurance Cover DoorDash Deliveries?

- Standard personal auto insurance policies are designed for personal use, such as commuting, running errands, or leisure travel. These policies typically exclude coverage when the vehicle is used for commercial purposes.

- When you use your vehicle for DoorDash deliveries, you are engaging in a commercial activity. This means that in the event of an accident while actively delivering for DoorDash, your personal auto insurance may not cover damages or injuries.

- Most personal auto insurance providers explicitly state in their policies that using a vehicle for delivery services invalidates coverage during those periods. As a result, relying on personal insurance while working for DoorDash could leave you financially exposed.

What Happens If I Get Into an Accident While Dashing?

- If an accident occurs while you are logged into the DoorDash app and on your way to pick up a delivery, DoorDash's commercial insurance may provide liability coverage, but only after your personal insurance is billed first, if applicable.

- During periods when you are en route to a restaurant or delivering food to a customer, DoorDash provides contingent liability insurance, but this coverage depends on the accident occurring during active delivery status in the app.

- However, before accepting a delivery or after completing one—when you are merely online but not actively delivering—your personal auto insurance would typically be expected to respond. But because this is considered commercial use, your personal insurer may deny the claim, potentially leading to out-of-pocket expenses or policy cancellation.

How Can I Get Proper Insurance for Delivery Work?

- One option is to obtain a commercial auto insurance policy tailored for delivery drivers. These policies are designed to cover vehicles used for business purposes, including food delivery.

- Alternatively, some insurance companies offer drive-for-hire endorsements or ride-share add-ons that extend personal policies to include certain commercial activities, though availability varies by state and insurer.

- Additionally, DoorDash partners with insurance providers to offer protection during specific periods of active delivery, but drivers must understand the gaps in coverage. It’s essential to review both DoorDash's insurance policy and your personal policy to ensure you have adequate protection at all times while driving for pay.

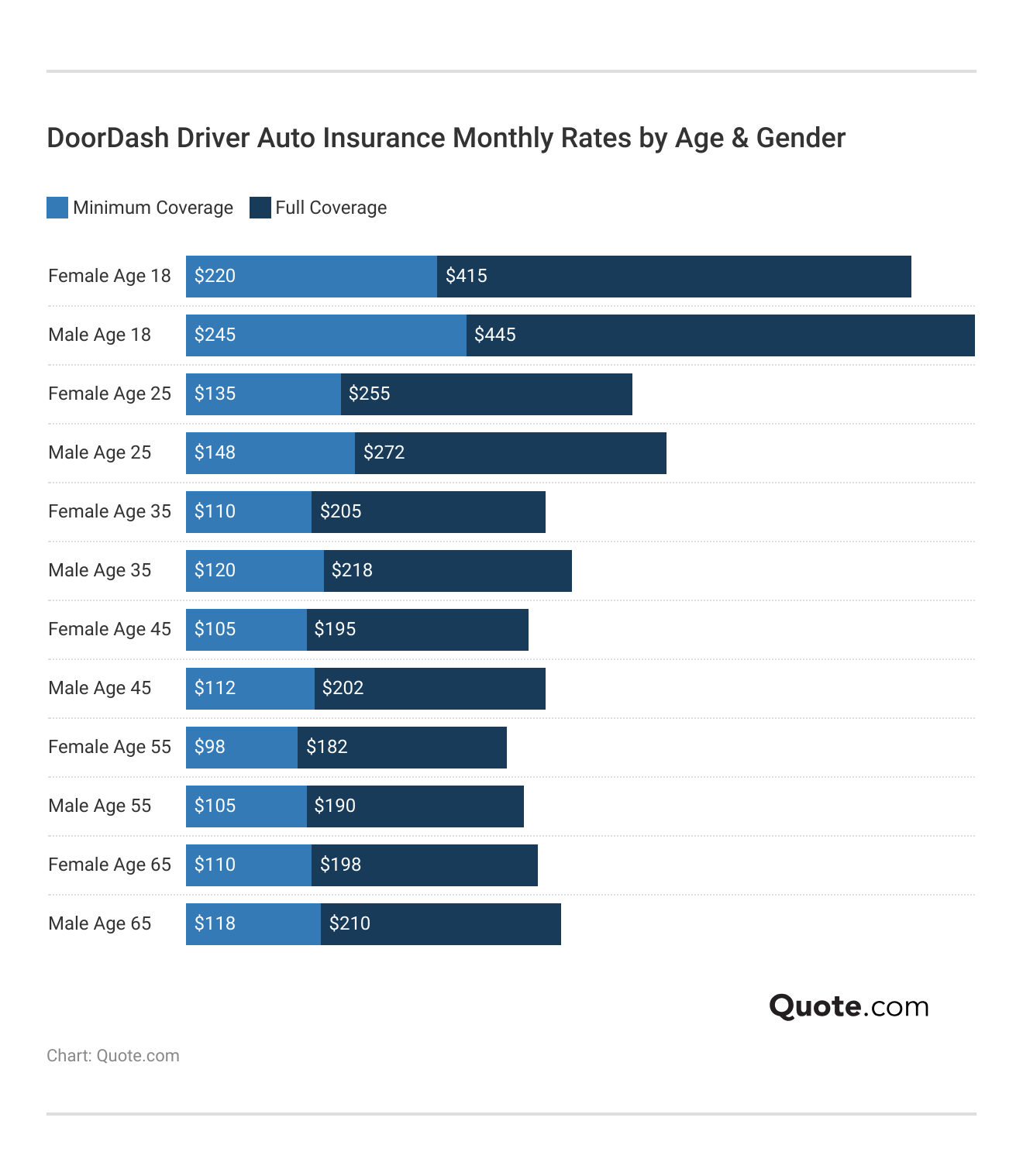

What Is the Average Cost of Insurance for DoorDash Drivers?

Factors That Influence Insurance Costs for DoorDash Drivers

- One of the primary factors affecting insurance costs for DoorDash drivers is the driver’s personal driving record. Drivers with clean records, meaning no accidents, traffic violations, or claims history, typically qualify for lower premiums. Conversely, drivers with recent infractions may face significantly higher rates due to being considered higher risk by insurers.

- The type of vehicle being used for deliveries also plays an important role. Newer, more expensive cars or vehicles with higher repair costs tend to result in higher insurance premiums. Additionally, vehicles equipped with advanced safety features may qualify for discounts, helping reduce overall costs.

- Geographic location has a major impact on insurance pricing. Urban areas with heavy traffic, higher accident rates, and increased theft risk generally see higher insurance costs. Drivers in rural areas may benefit from lower premiums due to reduced exposure to these risks.

- Standard personal auto insurance policies do not cover commercial driving activities such as food delivery. This creates a coverage gap when drivers are actively using their vehicle for DoorDash, especially between accepting a delivery and dropping off the order, when personal policies often exclude liability.

- Many insurance companies now offer rideshare or delivery-specific endorsements that bridge this gap. These add-ons extend coverage during periods when the driver is logged into the DoorDash app but hasn’t yet accepted a delivery, or during active deliveries. This added layer of protection ensures continuous coverage throughout the delivery process.

- Without proper rideshare coverage, drivers risk denied claims in the event of an accident during delivery hours. This could lead to out-of-pocket expenses for vehicle repairs, medical bills, and legal costs, making specialized insurance a necessary investment for regular DoorDash drivers.

Estimated Monthly and Annual Insurance Expenses

- On average, DoorDash drivers with standard personal auto insurance might pay between $100 and $250 per month, depending on individual circumstances. However, adding a rideshare endorsement can increase this cost by $10 to $50 per month, bringing the total to roughly $120–$300 monthly.

- Several insurers, including Allstate, Progressive, and State Farm, offer specific rideshare coverage options that integrate with existing policies. Rates vary widely based on location, age, driving history, and vehicle usage levels, making it essential for drivers to obtain personalized quotes.

- For drivers who log a high number of delivery hours, a commercial auto insurance policy might be more appropriate, though it typically costs significantly more—often exceeding $500 per month. Most DoorDash drivers find that a personal policy with a rideshare endorsement offers a more affordable and legally sound balance between protection and cost.

Does DoorDash Delivery Impact Your Personal Car Insurance Coverage?

Most standard personal car insurance policies are designed for personal use, which includes commuting, running errands, and other non-commercial activities. When a driver begins using their vehicle for commercial purposes—such as delivering food through DoorDash—they may exceed the scope of what their policy covers.

Many personal auto insurers explicitly exclude coverage when the vehicle is used to transport goods for compensation, which applies to delivery services. This means that if an accident occurs while accepting or delivering a DoorDash order, the driver's personal insurer might deny the claim due to the vehicle being used for commercial activity.

- Personal insurance policies generally assume the vehicle is not being used to generate income, so any use that contradicts this can invalidate coverage.

- Insurers categorize driving into tiers: personal, business, and commercial. DoorDash delivery typically falls into the commercial tier, which requires appropriate coverage.

- Policyholders may unknowingly breach their contract by engaging in food delivery without notifying their insurer, potentially leading to claim denials or policy cancellations.

When DoorDash Insurance Provides Coverage (And When It Doesn't)

DoorDash provides some level of insurance coverage for its delivery drivers, but it's important to understand that this coverage is conditional and only activates during specific phases of the delivery process.

DoorDash’s insurance typically applies once a driver has accepted a delivery request and is actively en route to the restaurant or delivering the order. However, there are critical gaps in coverage—such as when the driver is logged into the app but waiting for a delivery assignment (known as Period 1), or when they are driving to a restaurant without an active order.

- Coverage begins during Period 2 (driving to pick up food) and Period 3 (delivering to the customer), where DoorDash offers liability, collision, and comprehensive protection.

- In Period 1, when logged in but not assigned a delivery, DoorDash offers limited liability coverage in some regions, but this may not meet state minimums or cover all damages.

- If an incident occurs outside active delivery periods, the driver’s personal or commercial insurance must step in, which may not be available if the insurer wasn't informed of delivery activity.

Steps to Maintain Proper Insurance Coverage While DoorDashing

To avoid financial risk and ensure continuous protection, DoorDash drivers should take proactive steps regarding their insurance. The key is transparency with insurance providers and understanding how policy terms interact with gig economy work.

Some insurers offer ride-share or delivery endorsements that extend personal policies to cover commercial driving periods. Failing to obtain proper coverage could result in out-of-pocket costs for accidents, vehicle repairs, or liability claims.

- Inform your auto insurance company that you perform delivery work, as many allow policy upgrades or add-ons for gig drivers.

- Consider purchasing a commercial auto policy or a hybrid ride-share endorsement if your insurer offers one, especially if you deliver frequently.

- Review DoorDash’s insurance details regularly, as coverage terms, limits, and availability might vary by state or country and can change over time.

Frequently Asked Questions

Do I need special insurance to drive for DoorDash?

You do not need special insurance to start driving for DoorDash, but your personal auto insurance may not cover you during deliveries. DoorDash provides liability, uninsured motorist, and collision coverage during active delivery periods. Check with your insurance provider about how gig work affects your policy and consider a commercial or rideshare endorsement if needed.

Does DoorDash provide insurance while I’m delivering?

Yes, DoorDash provides insurance coverage when you’re actively delivering. This includes liability, uninsured motorist, and damage to your vehicle once you’ve accepted a delivery. Coverage starts when you accept a dash and ends when you mark the delivery as complete. It does not cover the period when you’re logged in but haven’t accepted an order.

Will my personal car insurance cover me while DoorDashing?

Most personal auto insurance policies do not cover you while making deliveries for DoorDash, as it’s considered commercial use. Engaging in gig work with only personal insurance could risk cancellation or denial of claims. It’s important to notify your insurer and consider adding a rideshare or commercial-use endorsement to remain protected.

What happens if I get in an accident while DoorDashing?

If you’re in an accident while actively delivering for DoorDash, their insurance policy provides coverage for liability, property damage, and injuries, depending on the situation. Coverage applies once you’ve accepted a delivery. You should report the accident to DoorDash and your insurance provider immediately and document the incident properly for claims processing.

Leave a Reply