Gap Insurance For Auto Loans

Gap insurance for auto loans is a crucial financial safeguard often overlooked by car buyers. When financing a vehicle, standard auto insurance may not cover the full remaining loan balance if the car is totaled or stolen. This is where gap insurance steps in, covering the “gap” between the car’s actual cash value and the amount still owed.

Given that new vehicles can depreciate rapidly—sometimes up to 20% in the first year—borrowers can quickly find themselves underwater on their loan. Gap insurance offers peace of mind, ensuring that unexpected events don’t result in significant out-of-pocket expenses.

Understanding Gap Insurance for Auto Loans

Gap insurance, or Guaranteed Asset Protection insurance, is a specialized type of coverage designed to protect auto loan borrowers in the event their vehicle is totaled or stolen and the insurance payout falls short of the outstanding loan balance.

Auto Insurance In Mo

Auto Insurance In MoWhen you finance a vehicle, its value typically depreciates rapidly—often faster than the loan is paid down—creating a financial gap between what you owe and what your primary insurance company will pay based on the car’s current market value. This shortfall can leave borrowers responsible for thousands of dollars out of pocket if not covered.

Gap insurance bridges this difference, paying the remaining balance on the auto loan after the primary insurer's settlement is applied, thus shielding borrowers from unexpected financial burdens. It is especially valuable for those who make low down payments, lease vehicles, or purchase cars that depreciate quickly.

What Does Gap Insurance Cover?

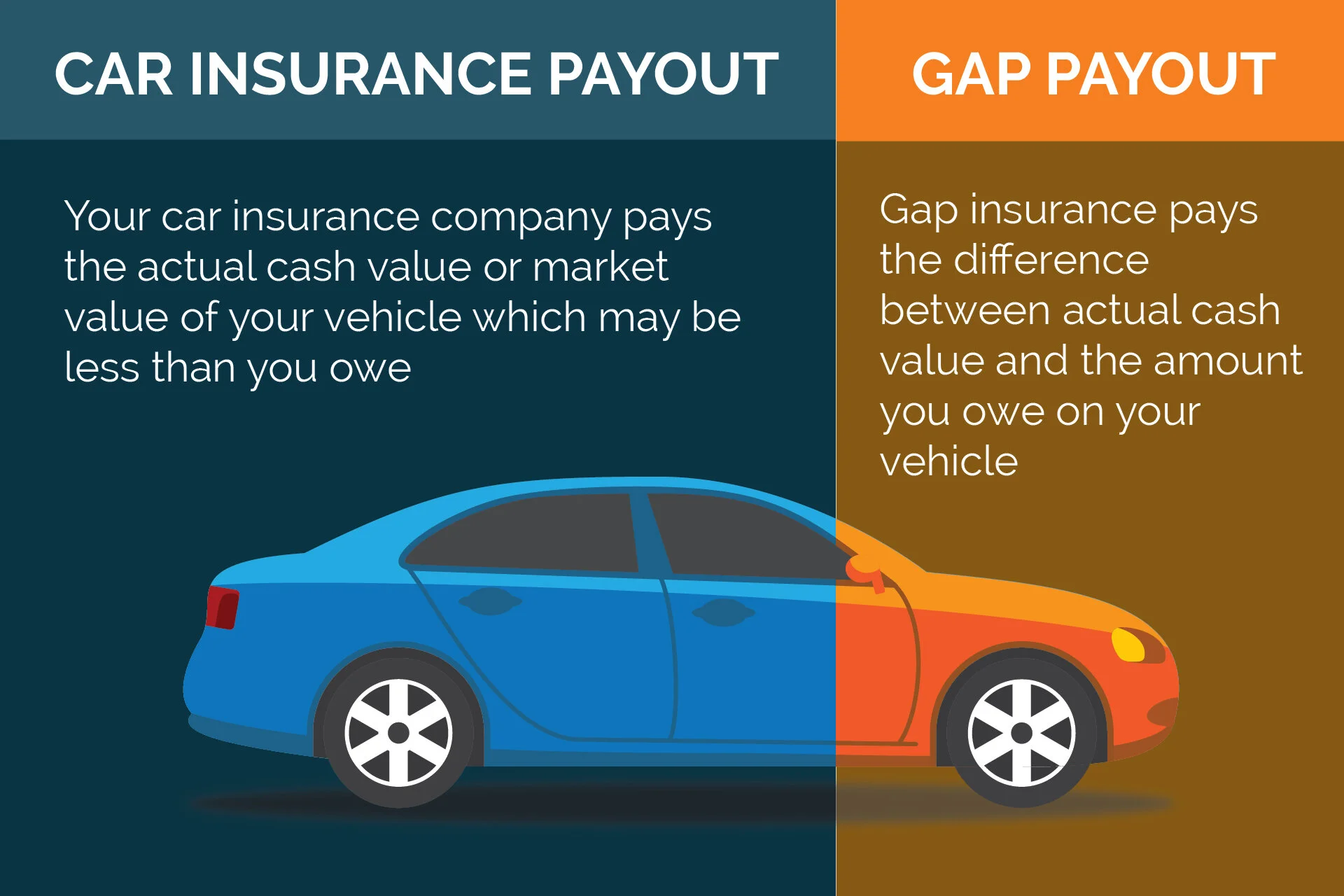

Gap insurance specifically covers the difference between the actual cash value (ACV) of a totaled or stolen vehicle and the remaining balance on the auto loan or lease.

For example, if your car is worth $18,000 at the time of an accident but you still owe $22,000 on the loan, your primary insurance will only reimburse you $18,000. Without gap insurance, you would be responsible for the remaining $4,000. However, with gap coverage, this financial gap is paid by the insurer, often up to certain policy limits.

Auto Insurance In New York Ny

Auto Insurance In New York NyIt's important to note that gap insurance does not cover deductibles, late payment fees, extended warranties, mechanical repairs, or personal injuries. It is purely designed to address loan or lease shortfall in the case of a total loss, making it a crucial safety net for financed or leased vehicles.

Who Should Consider Gap Insurance?

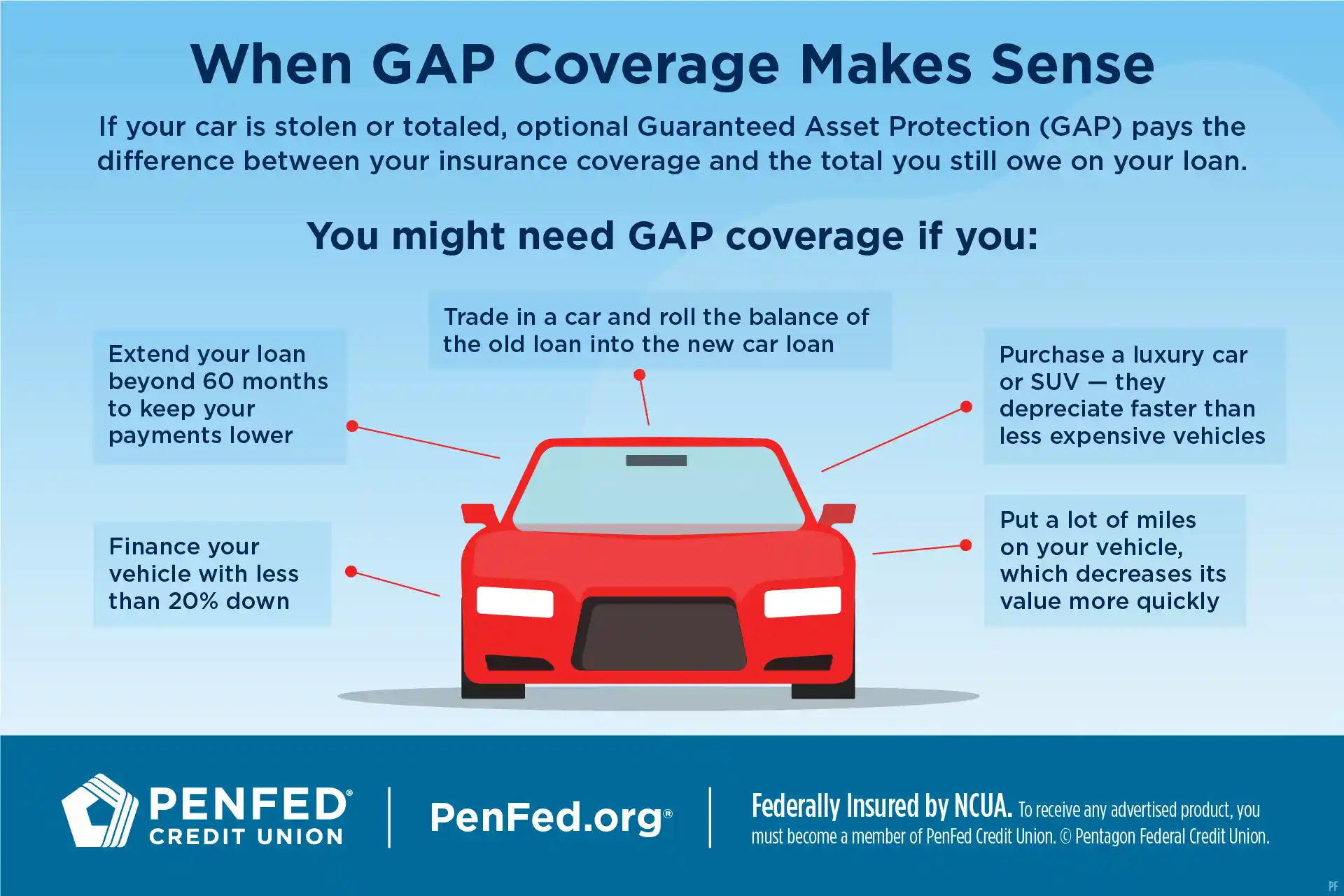

Gap insurance is particularly beneficial for specific groups of borrowers who are at higher risk of owing more on their auto loan than the car’s depreciated value.

Those who make a small down payment (less than 20%), finance for long terms (60 months or more), or purchase vehicles with high depreciation rates—such as many new cars and certain luxury models—should strongly consider gap coverage. It's also commonly recommended for individuals who roll over negative equity from a previous auto loan into a new one, as this increases the initial loan balance.

Additionally, lessees are often required by leasing companies to carry gap insurance, sometimes referred to as lease gap coverage. While not mandatory in most states, it provides essential protection for drivers who could otherwise face significant financial liability after a total loss.

Auto Insurance In Nh

Auto Insurance In NhHow to Obtain and Compare Gap Insurance Options

Consumers have several avenues to purchase gap insurance, including through auto insurers, car dealerships, and financing institutions. It's crucial to compare prices and terms, as costs and coverage details can vary significantly. Purchasing gap insurance directly through your auto insurance provider is often the most cost-effective option, typically adding only a few dollars per month to your premium.

In contrast, buying through a dealership may result in higher prices, often rolled into your loan, leading to added interest over time. Be sure to read the policy carefully to confirm what is included—some policies cap the coverage amount or exclude certain fees. The table below outlines a comparison of common gap insurance sources:

| Provider Type | Average Cost | Payment Method | Key Benefits |

|---|---|---|---|

| Auto Insurance Company | $20–$40 per year | Added to monthly premium | Lowest cost option, easy integration with existing policy |

| Car Dealership | $400–$700 (one-time) | Rolled into loan | Convenient at purchase, but higher cost and interest accrues |

| Financing Institution / Lender | $300–$600 (one-time) | Included in loan amount | May be required for some loans, but less flexible than insurance provider |

Understanding Gap Insurance for Auto Loans: A Comprehensive Guide

Can gap insurance be financed as part of an auto loan?

Yes, gap insurance can typically be financed as part of an auto loan. This type of insurance, also known as Guaranteed Asset Protection insurance, is designed to cover the difference between the amount you still owe on your car loan and the actual cash value of the vehicle if it’s totaled or stolen and declared a total loss.

Auto Insurance In Tucson Arizona

Auto Insurance In Tucson ArizonaMany lenders and auto financing institutions allow borrowers to roll the cost of gap insurance directly into the overall auto loan amount. This means instead of paying the premium upfront in a lump sum, you pay it gradually with your monthly car payments over the life of the loan. While convenient, including gap insurance in the loan increases both the total amount financed and the total interest paid over time.

How Financing Gap Insurance with Your Auto Loan Works

- When you purchase a vehicle, especially a new one, the lender may offer gap insurance as an optional add-on during the loan application or financing process.

- The premium for the gap insurance is calculated upfront and then added to the principal balance of your auto loan, meaning you don’t pay it separately.

- Once included, the cost of gap insurance is paid off incrementally through your regular monthly loan payments, just like the cost of the car itself.

Pros and Cons of Including Gap Insurance in Your Loan

- One advantage is convenience—adding gap insurance to your loan eliminates the need for an out-of-pocket payment, making it easier to manage your finances at the time of purchase.

- A potential downside is that financing the insurance increases the total loan amount, which can lead to higher interest charges over the life of the loan.

- Additionally, if the car depreciates quickly or you owe more than the car is worth, you might still be at risk of being upside-down on your loan even with gap coverage, especially if you make a low down payment.

Alternatives to Financing Gap Insurance through Your Lender

- You can often purchase gap insurance directly from your auto insurance provider, which may offer lower premiums compared to dealer-sold policies.

- Some automakers offer their own gap coverage through affiliated finance arms, such as GM Financial or Ford Credit, sometimes including it in lease agreements by default.

- Another option is paying for gap insurance upfront out of pocket, which avoids adding to your loan balance and accumulating interest over time.

What does gap insurance cover for auto loans?

What Is Gap Insurance and How Does It Work?

- Gap insurance, also known as guaranteed asset protection insurance, is a specialized type of coverage designed to protect auto loan borrowers in the event of a total loss due to theft or an accident. When a vehicle is declared a total loss, the primary auto insurance policy typically reimburses the current market value of the car, not the outstanding balance on the loan or lease.

- Because vehicles depreciate rapidly—often losing 20% or more of their value in the first year—there can be a significant difference between what the car is worth and what the borrower still owes. This difference is referred to as the gap, and gap insurance covers that shortfall so the borrower isn’t left paying for a car they can no longer use.

- For example, if a car is totaled and the insurance payout is $18,000 but the remaining loan balance is $22,000, gap insurance would cover the $4,000 difference. This helps avoid personal financial liability in a difficult situation and allows the borrower to settle the loan without using savings or incurring additional debt.

What Specific Costs Does Gap Insurance Cover?

- Gap insurance specifically covers the difference between the actual cash value (ACV) of the vehicle at the time of total loss and the remaining balance on the auto loan or lease. This includes any unpaid principal, accrued interest, and certain other finance charges that may be part of the loan agreement.

- It does not cover late fees, extended warranties, service contracts, credit life insurance, or any mechanical repairs not related to the loss. Additionally, gap insurance typically won't cover down payments, security deposits, or future insurance premiums, even if those were included in the financed amount.

- Some gap insurance policies offered through dealerships or lenders may include additional benefits such as covering the deductible required by the primary insurance policy. However, this varies by provider, so it’s important to read the terms carefully to understand what costs are included in the specific policy.

When Should You Consider Purchasing Gap Insurance?

- Gap insurance is most beneficial when the down payment on a vehicle is less than 20% of the purchase price. Since low down payments result in higher loan balances relative to the car’s value, the risk of being upside-down on the loan increases significantly during the early years.

- It’s also advisable for individuals who have financed a vehicle for a long term (60 months or more), as longer loan terms slow down equity buildup, making it more likely that the loan balance will exceed the vehicle’s market value if it’s totaled early in the term.

- Additionally, gap insurance is a smart option for drivers who purchase vehicles known for rapid depreciation, such as luxury cars or certain brands that lose value quickly. Lessees are often required by leasing companies to carry gap insurance, also known as lease gap coverage, to protect the leasing entity’s financial interest.

Frequently Asked Questions

What is gap insurance for auto loans?

Gap insurance for auto loans covers the difference between what you owe on your car loan and the vehicle’s actual cash value if it’s stolen or totaled. If your car depreciates quickly, you may owe more than it’s worth. This coverage helps avoid out-of-pocket expenses for the remaining loan balance after an accident, providing financial protection during the early years of ownership when depreciation is highest.

Do I need gap insurance on my auto loan?

You may need gap insurance if you owe more on your auto loan than your car’s current market value. This often happens with long loan terms, low down payments, or vehicles that depreciate quickly. If your car is totaled or stolen, gap insurance prevents you from paying the remaining loan balance out of pocket. It’s especially useful during the first few years of ownership and can provide valuable peace of mind.

How does gap insurance work with my auto loan?

Gap insurance works by covering the “gap” between your car’s actual cash value and the outstanding balance on your auto loan if the vehicle is totaled or stolen. Your primary insurance pays the car’s market value, and gap insurance pays the remaining loan amount, up to policy limits. This helps prevent financial loss when depreciation exceeds loan payoff, ensuring you’re not stuck paying for a vehicle you can no longer use.

Where can I buy gap insurance for my auto loan?

You can buy gap insurance from auto insurers, car dealerships, or some loan lenders. Auto insurance companies often offer it as an add-on to your policy, usually at a lower cost. Dealerships may include it in your financing agreement, but prices can be higher. Compare options to find affordable coverage. Make sure the provider is reputable and the policy clearly covers your loan balance in case of a total loss.

Leave a Reply