Home premium insurance

Home premium insurance offers comprehensive protection for homeowners seeking enhanced coverage beyond standard policies.

Designed for high-value properties and discerning clients, it combines robust structural coverage with personalized amenities such as extended liability protection, luxury item valuation, and concierge services. This type of insurance addresses unique risks associated with upscale homes, including custom finishes, advanced security systems, and location-specific threats.

With tailored premiums and faster claims processing, home premium insurance ensures peace of mind while safeguarding significant investments. As property values rise and homeowner expectations evolve, this elite coverage continues gaining traction among those prioritizing security, exclusivity, and seamless service in their insurance solutions.

High value home insurance massachusetts

High value home insurance massachusettsHome premium insurance refers to an elevated level of home protection that goes beyond the standard coverage typically included in basic homeowners insurance policies.

Designed for higher-value properties or individuals seeking more comprehensive protection, home premium insurance often includes extended dwelling coverage, increased liability limits, and specialized endorsements for high-value personal property such as fine art, jewelry, and collectibles. These policies are typically customizable and may cover unique risks like natural disasters specific to a region, service line damage, or even identity theft protection.

Insurers offering home premium insurance usually provide additional concierge services, like assistance with home repairs, travel arrangements during displacement, or quick claims response, enhancing the overall value for policyholders who prioritize service and extensive protection.

Home premium insurance policies offer significantly broader protection compared to standard plans, often featuring higher coverage limits for the dwelling, personal property, and liability.

Home and auto insurance in anaheim

Home and auto insurance in anaheimFor example, while a standard policy might cap personal property coverage at $250,000, a premium plan could offer $1 million or more, which is essential for homeowners with valuable possessions. These policies may also include extended replacement cost, meaning your home can be rebuilt even if the cost exceeds the policy limit due to inflation or construction spikes.

Additional features frequently include scheduled personal property coverage for items like rare collectibles or heirloom jewelry, ordinance or law coverage to meet updated building codes, and water backup from sewers, which is typically excluded in basic policies. The customization of these coverages ensures that high-net-worth individuals and owners of luxury homes receive tailored, robust protection.

Benefits of Concierge and White-Glove Claims Service

One of the defining characteristics of home premium insurance is the inclusion of superior customer service, often referred to as concierge-level support or white-glove claims handling.

Unlike standard insurance experiences, premium policyholders benefit from dedicated claims representatives, direct phone lines, and expedited claims processing that reduce stress during emergencies. These services may also include assistance with temporary housing arrangements, coordination of contractors, and continuous updates throughout the repair process.

Home building insurance calculator

Home building insurance calculatorSome insurers even offer global travel assistance or support for securing emergency home entry services. The goal is to deliver a seamless and dignified experience that reflects the value of the insured property and the client’s lifestyle, ensuring that service quality matches the level of coverage provided.

Home premium insurance is ideally suited for owners of high-value homes, typically those valued above the standard policy limits or located in costly real estate markets.

It’s also recommended for individuals with significant personal assets, expensive renovations, or unique architectural features that require specific coverage. Homeowners in areas prone to natural catastrophes like hurricanes, wildfires, or earthquakes may benefit from the enhanced peril protection included in premium policies.

Additionally, those who travel frequently or maintain second homes can appreciate the added services such as remote monitoring integration, vacancy coverage, and concierge coordination during emergencies. Unlike one-size-fits-all policies, premium insurance adapts to the homeowner’s specific risks and lifestyle, making it a strategic choice for those seeking both comprehensive protection and superior service.

Home improvement insurance quote

Home improvement insurance quote| Feature | Standard Home Insurance | Home Premium Insurance |

|---|---|---|

| Dwelling Coverage Limits | Typically up to $500,000–$750,000 | Often exceeds $1M+, customizable |

| Personal Property Protection | Basic limits; few scheduled items | High-value item endorsements; broader coverage |

| Claims Service | Standard claims process | White-glove service, direct representative |

| Additional Living Expenses | Limited reimbursement periods | Extended coverage with premium accommodations |

| Niche Add-Ons | Minimal or not available | Identity theft protection, service line, cyber liability |

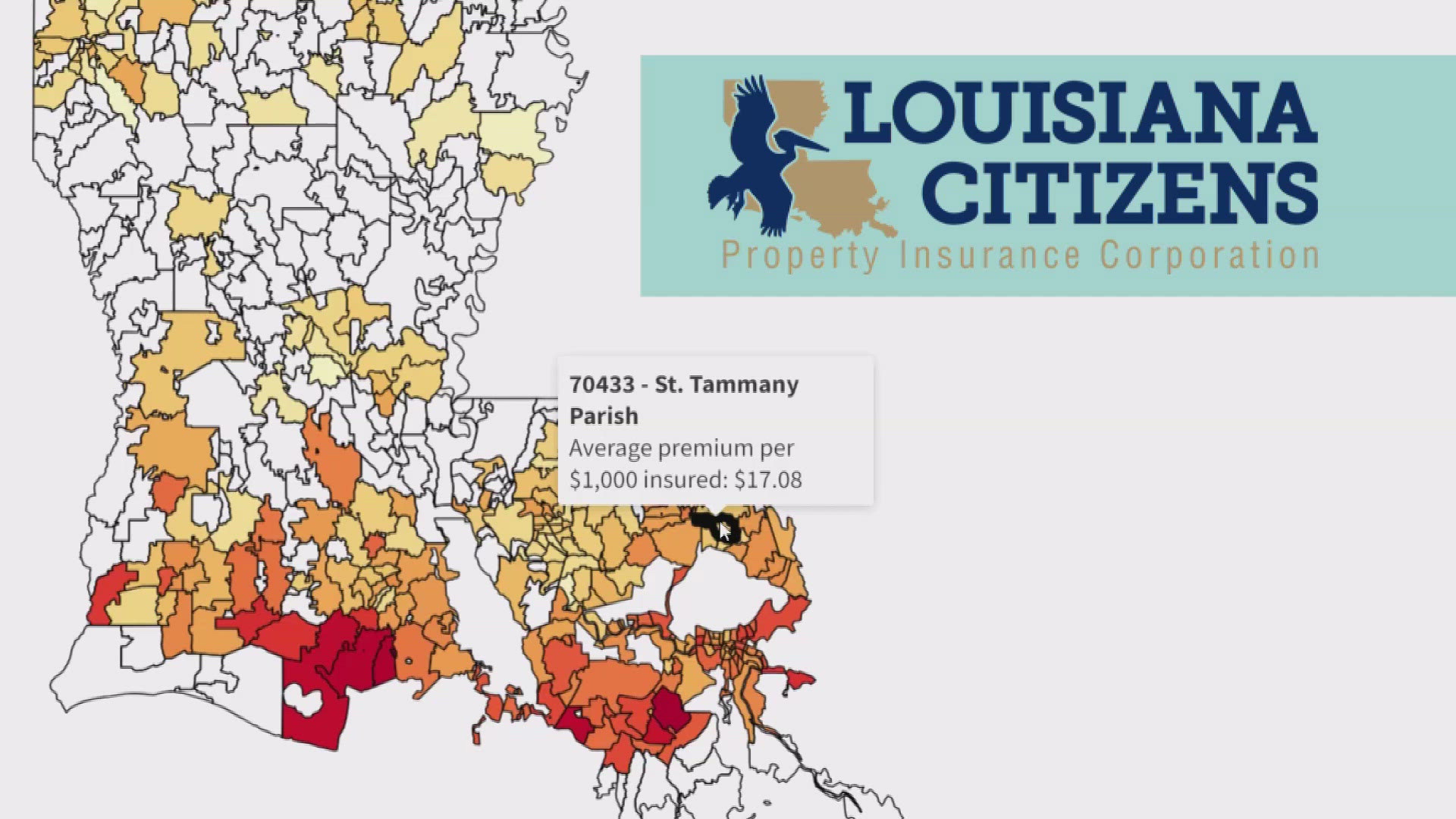

The lowest home insurance premium rate in Louisiana varies significantly depending on the insurance provider, location within the state, home characteristics, and the coverage selected.

However, as of recent data, some homeowners in lower-risk areas (such as central or northern parishes away from the Gulf Coast) may secure annual premiums starting as low as $1,200 to $1,500 with certain insurers. These rates typically apply to modestly valued homes with strong construction features and enhanced risk mitigation (e.g., storm shutters, updated electrical systems).

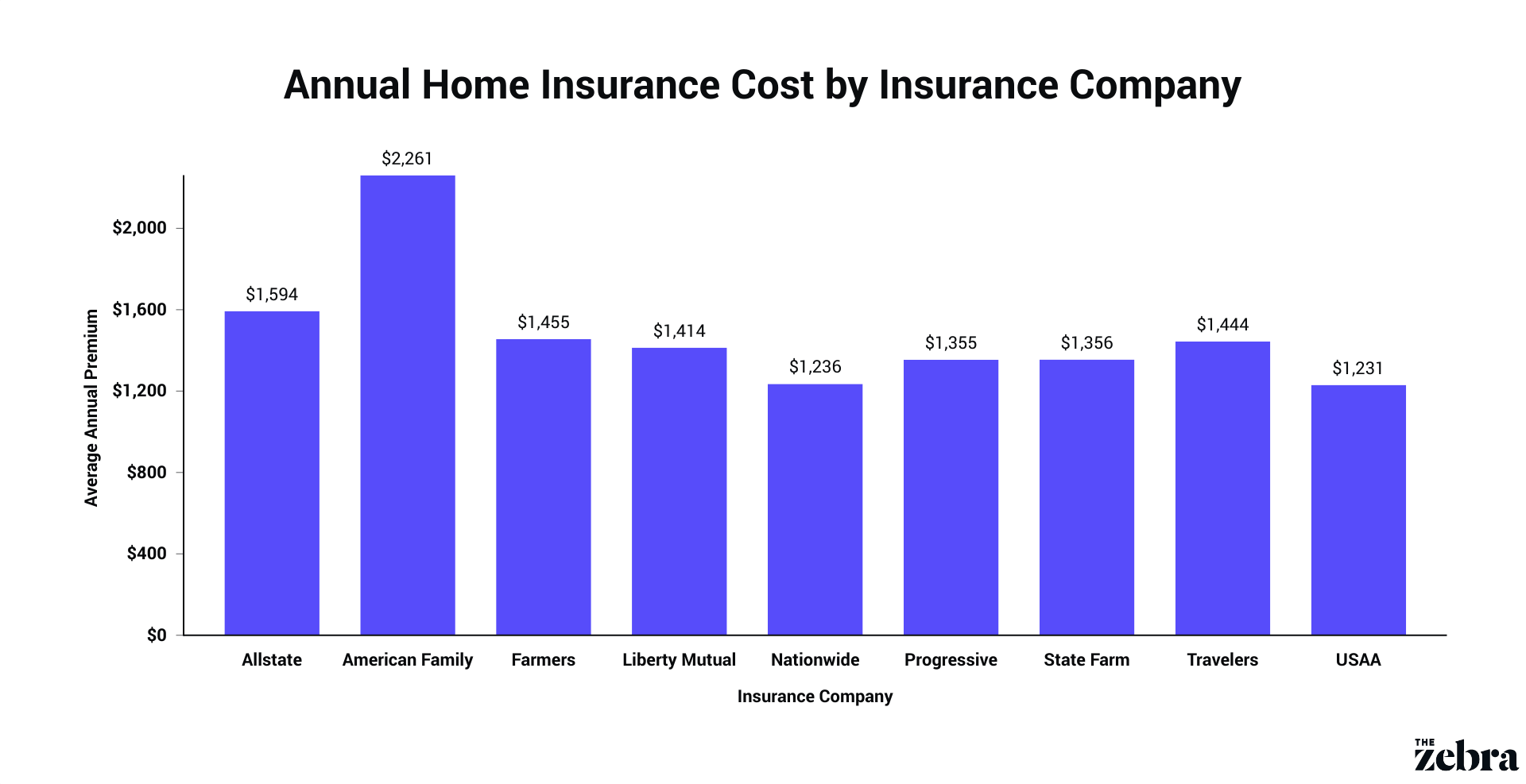

Insurers like State Farm, Allstate, and USAA often offer competitive base rates, but the actual lowest rate for an individual will depend on personalized risk factors. It's crucial to compare quotes from multiple companies and consider available discounts.

Factors That Influence Low Home Insurance Rates in Louisiana

- Geographic location plays a primary role. Homes in inland parishes such as Rapides or Ouachita face lower hurricane and flood risks, leading to reduced premiums compared to coastal areas like Jefferson or Plaquemines.

- Home construction materials and age affect rates. Properties built with reinforced concrete, metal roofing, or impact-resistant windows are often eligible for lower rates due to increased resilience against storms.

- Insurance score and claims history also impact pricing. Policyholders with strong credit-based insurance scores and no prior claims typically qualify for the most competitive rates offered by insurers.

Top Insurance Providers Offering Competitive Rates

- State Farm frequently ranks among the most affordable options in Louisiana, particularly for homeowners in medium-risk zones, offering robust coverage with added discount opportunities for bundling or safety features.

- USAA provides low premium options for military members and their families, often reporting among the lowest average rates in the state, assuming eligibility and favorable property conditions.

- Travelers and Allstate also offer competitively priced policies in specific regions, especially when homeowners take advantage of claims-free discounts, home security systems, or early renewal savings.

- Shop around and obtain at least three personalized quotes from both national insurers and regional companies familiar with Louisiana's risk landscape to identify the most affordable option for your specific home.

- Improve your home’s risk profile by installing storm shutters, reinforcing the roof deck, or upgrading plumbing and electrical systems, which may qualify you for mitigation discounts.

- Ask about available discounts such as loyalty rewards, automatic payment enrollment, paperless billing, or bundling home and auto policies, all of which can significantly reduce your annual premium.

The average home insurance premium for a house valued at $100,000 can vary significantly depending on location, construction type, age of the home, claims history, and other risk factors. While the replacement cost of the home is a major factor in determining premiums, a $100,000 home does not necessarily mean the insurance cost will be minimal.

According to data from the National Association of Insurance Commissioners (NAIC) and various insurance providers, the national average for homeowners insurance in the United States ranges from $1,200 to $1,800 per year. However, for a lower-valued home such as one at $100,000, premiums often fall on the lower end of that spectrum—typically between $800 and $1,300 annually.

Factors such as choosing a higher deductible, bundling policies, or qualifying for discounts can further reduce this amount. It’s important to note that the dwelling coverage portion of a policy for a $100,000 house might only be around $50,000 to $80,000, as it reflects replacement cost rather than market value, which also affects the final premium.

- Geographic location plays a crucial role—homes in areas prone to natural disasters such as hurricanes, wildfires, or tornadoes generally face higher premiums due to increased risk of claims. A $100,000 house in Florida, for example, may cost more to insure than an identical home in Iowa.

- The age and condition of the home also impact the rate. Older homes with outdated electrical systems, plumbing, or roofing may be considered higher risk, leading to increased premiums even if the market value is low. Upgrades like a new roof or storm shutters can reduce the cost.

- Insurance companies evaluate the home’s construction materials, square footage, and local crime rates. For instance, a brick house in a low-crime area with a security system may qualify for lower rates compared to a wood-frame home in a higher-risk neighborhood.

- Home insurance premiums are primarily based on the cost to rebuild the home, not its market value. For a $100,000 house, the dwelling coverage (reconstruction cost) might only be $60,000–$80,000 depending on local construction costs, which directly influences the premium amount.

- Materials and labor costs vary by region—rebuilding a modest house in a high-cost area like California may cost far more than in a rural part of Mississippi, even if both homes are valued at $100,000 on the market.

- Insurers also consider features like foundation type, roofing, and heating systems when estimating replacement costs. Accurate assessment ensures policyholders are neither underinsured nor overpaying for unnecessary coverage.

Ways to Save on Home Insurance for a $100,000 Property

- Shop around and compare quotes from multiple insurers. Rates for the same $100,000 home can differ by hundreds of dollars depending on the provider, so obtaining at least three quotes is advisable to secure the best rate.

- Bundle home and auto insurance with the same company. Many insurers offer multi-policy discounts that can reduce home insurance costs by 10% to 25%, which is especially beneficial for lower-valued homes where savings might seem modest but add up over time.

- Maintain a good credit score and claims-free history. Insurers often use credit-based insurance scores to assess risk, and policyholders with strong financial histories typically qualify for lower premiums, even on less expensive homes.

The typical cost of home insurance premiums in the United States varies significantly depending on location, coverage type, home value, and other risk factors. On average, homeowners pay approximately $1,750 to $2,000 per year for a standard home insurance policy. This cost primarily covers dwelling protection, personal property, liability, and additional living expenses.

However, premiums can range from as low as $1,000 annually in states with low risk and construction costs to over $3,500 in areas prone to natural disasters such as hurricanes, wildfires, or tornadoes. Insurance companies use extensive data modeling to determine risk levels, meaning two similar homes in different regions can have vastly different premiums.

- Geographic location plays a critical role; homes in regions exposed to natural disasters like floods, earthquakes, or hurricanes typically face higher premiums due to increased risk of claims.

- The age and condition of the home affect pricing, with older homes often costing more to insure because of outdated electrical systems, plumbing, or roofing materials that may not meet current building codes.

- Local crime rates, proximity to fire stations and hydrants, and the cost of construction materials in the area directly influence the overall cost of coverage, as insurers assess the likelihood and potential cost of repairs or rebuilds.

Different Types of Home Insurance Policies and Their Cost Impact

- HO-3 policies, the most common type, offer broad coverage for the dwelling and named perils for personal property, with average annual premiums falling within the national range of $1,750 to $2,000.

- HO-5 policies provide more comprehensive coverage, especially for personal property, and are typically 10% to 20% more expensive than HO-3 policies due to their broader protection scope.

- Specialized policies, such as HO-8 for older homes or those in historic districts, are tailored to specific needs and can vary widely in price, often influenced by replacement cost challenges and limited market availability of materials.

- Choosing a higher deductible—such as $2,500 instead of $500—can significantly reduce the annual premium, as the homeowner assumes more financial responsibility before the insurance kicks in, lowering the insurer’s risk exposure.

- Increasing coverage limits, especially for high-value items like jewelry, art, or electronics, raises the cost of premiums because the insurer is liable for larger potential payouts.

- Optional endorsements like water backup, sewer damage, or increased liability coverage add to the base premium but can be essential for comprehensive protection depending on the home’s location and structure.

Frequently Asked Questions

Home premium insurance offers comprehensive protection beyond standard policies, covering your dwelling, personal property, and liability. It often includes higher coverage limits, additional perils like earthquakes or floods, and enhanced features such as increased replacement cost coverage. Premium policies may also cover detached structures, landscaping, and valuable items like jewelry or art, providing broader financial protection in case of damage, theft, or lawsuits.

Home premium insurance provides broader and higher-value coverage than standard home insurance. It includes elevated coverage limits, protection for high-value items, and often covers more perils. Premium policies may offer additional services like faster claims processing, higher liability limits, and extended replacement cost benefits. They are tailored for homeowners with more valuable properties or possessions, ensuring more comprehensive protection and peace of mind compared to basic home insurance plans.

For homeowners with high-value properties, expensive belongings, or unique needs, home premium insurance can be worth the extra cost. It offers stronger financial protection, higher coverage limits, and broader perils inclusion. Many premium policies also provide personalized services and additional benefits like increased rebuilding costs or worldwide personal property coverage. If your home or possessions exceed standard policy limits, a premium plan can offer essential, cost-effective protection against major losses.

Yes, most home premium insurance policies can be customized to suit your specific needs. Insurers often allow you to add endorsements or riders for valuable items like jewelry, fine art, or collectibles. You can also adjust coverage limits, include protection for home-based businesses, or add features like service line coverage or identity recovery. Customization ensures your policy fully aligns with your assets, lifestyle, and risk exposure, offering truly tailored protection.

Leave a Reply