20 Year Term Life Insurance Quote

A 20-year term life insurance policy offers a balanced solution for individuals seeking affordable, long-term financial protection.

This type of coverage provides a fixed death benefit for a period of two decades, making it ideal for those with medium-term obligations such as a mortgage, children’s education, or income replacement. Premiums remain level throughout the term, ensuring predictability in budgeting.

When shopping for a 20-year term life insurance quote, factors like age, health, lifestyle, and coverage amount play a crucial role in determining costs. Comparing quotes from multiple insurers helps ensure competitive pricing and optimal coverage tailored to individual needs.

Health Insurance For Large Businesses

Health Insurance For Large BusinessesUnderstanding a 20 Year Term Life Insurance Quote

A 20 year term life insurance policy is one of the most popular forms of life insurance due to its balance of affordable premiums and long-term coverage.

When you request a 20 year term life insurance quote, insurers evaluate factors such as your age, health history, lifestyle habits (like smoking), occupation, and the death benefit amount you're seeking to determine your monthly or annual premium. Unlike permanent life insurance, this type of policy provides coverage for a specific 20-year period, after which the policy expires unless renewed, often at a significantly higher cost.

A key advantage of a 20-year term is it can align well with financial obligations such as a mortgage, college tuition for children, or income replacement during your prime earning years. Quotes are typically fixed for the entire term, meaning your premium remains unchanged, offering predictability and financial planning ease. It’s important to compare quotes from multiple insurers to ensure you're getting the most competitive rate based on your profile.

Several key factors influence the cost of your 20 year term life insurance quote. Insurers assess your age first—premiums increase with age due to higher mortality risk.

Health Insurance Small Business Arizona

Health Insurance Small Business ArizonaYour health condition, including blood pressure, cholesterol levels, BMI, and pre-existing medical conditions like diabetes or heart disease, heavily impacts pricing. Lifestyle choices such as tobacco use, alcohol consumption, and hazardous hobbies (e.g., skydiving or scuba diving) can also increase your rates. Additionally, a family medical history of chronic illnesses may lead to higher premiums.

The death benefit amount, or the sum paid to beneficiaries upon your death, directly correlates with cost—higher coverage equals higher premiums. Finally, optional riders such as a waiver of premium or convertible term feature can adjust your quote upward but add valuable flexibility. Shopping around and improving health markers before applying can help secure a more favorable rate.

How to Compare 20 Year Term Life Insurance Quotes Accurately

To effectively compare 20 year term life insurance quotes, ensure you're evaluating policies with identical death benefits, term lengths, and medical underwriting categories.

Small variations in coverage amount—such as $400,000 versus $500,000—can skew comparisons. Also, check whether quotes are based on fully underwritten, simplified issue, or no-medical-exam policies, as less stringent underwriting may result in higher premiums or exclusions. Pay attention to the insurer’s financial strength ratings from agencies like AM Best or Standard & Poor’s, which indicate reliability in paying claims.

How Much Business Insurance Do You Need

How Much Business Insurance Do You NeedLook into customer service reputation and policy conversion options, allowing you to switch to permanent coverage without medical underwriting. Using independent online comparison tools or consulting a licensed insurance broker can streamline the process and uncover the best value without sacrificing service quality.

Typical Costs of a 20-Year Term Life Insurance Policy by Profile

Premiums for a 20-year term life insurance policy can vary significantly based on individual profiles. For example, a healthy 35-year-old non-smoker may pay as little as $25 to $40 per month for a $500,000 death benefit, while a 50-year-old with high blood pressure might pay $80 to $150 for the same coverage.

Gender and location also contribute to pricing differences due to statistical life expectancy variations. The table below outlines average monthly premium estimates based on common applicant profiles. These figures are approximate and based on fully underwritten, non-tobacco rates from top-rated insurers in 2024.

| Applicant Profile | Death Benefit | Average Monthly Premium |

|---|---|---|

| 35-year-old male, non-smoker, excellent health | $500,000 | $28 |

| 35-year-old female, non-smoker, excellent health | $500,000 | $24 |

| 45-year-old male, non-smoker, standard health | $750,000 | $62 |

| 45-year-old male, smoker, standard health | $750,000 | $185 |

| 55-year-old female, non-smoker, standard health | $250,000 | $68 |

20-Year Term Life Insurance Quotes: A Comprehensive Guide to Coverage and Costs

What is the monthly cost of a $1,000,000 20-year term life insurance policy?

%20(1).png)

How To Bundle Business Insurance For Savings

How To Bundle Business Insurance For SavingsThe monthly cost of a $1,000,000 20-year term life insurance policy depends on several key factors that insurers evaluate during the underwriting process. These elements help determine the level of risk each applicant poses, which directly affects the premium.

- Age at application: Younger applicants typically pay lower premiums because they are statistically less likely to pass away during the policy term. For example, a 30-year-old may pay significantly less per month than a 50-year-old for the same coverage amount and term length.

- Health and medical history: Insurers assess health through medical exams, personal questionnaires, and sometimes lab tests. Individuals with excellent health, no chronic conditions, and healthy lifestyles (such as non-smokers) are offered lower rates.

- Lifestyle and occupation: High-risk hobbies (like skydiving), dangerous occupations (such as commercial fishing or firefighting), or tobacco use can increase premiums significantly due to the higher likelihood of claims.

Typical Monthly Cost Range for a $1,000,000 20-Year Term Policy

The actual monthly cost can vary widely, but healthy, non-smoking applicants often fall within a predictable range. It's important to note these are average estimates based on current market data and may fluctuate with different insurers and underwriting guidelines.

- For a 30-year-old male in excellent health, the monthly premium can range from $45 to $70 depending on the insurance provider and specific qualifications. Women typically pay slightly less due to longer average life expectancies, with rates between $35 and $60 per month under the same conditions.

- Applicants at age 40 can expect to pay between $60 and $95 monthly for equivalent coverage, again depending on gender, health, and lifestyle. Premiums rise with age because the probability of health-related claims increases over time.

- At age 50, premiums jump more noticeably—often ranging from $130 to $200 per month for non-smokers in good health. Smokers or those with medical issues may see rates exceed $300 monthly due to the heightened risk profile.

How to Get the Best Rate on a $1,000,000 20-Year Term Life Insurance Policy

Securing an affordable rate on a $1,000,000 20-year term life insurance policy requires careful planning and comparison. Several actionable steps can help applicants qualify for lower premiums and reduce the long-term financial burden.

- Compare multiple insurance providers: Different companies use varying underwriting criteria and pricing models. Using online quoting tools or working with an independent broker can help identify the most competitive rates available.

- Improve your health before applying: Losing weight, quitting smoking, managing blood pressure, and reducing cholesterol can improve your health classification. Even waiting a few months for better lab results may lead to significant savings.

- Choose the right coverage duration and amount: While $1,000,000 provides strong financial security, analyzing your actual needs—such as debts, income replacement, and children’s education—may reveal that slightly lower coverage is sufficient, thereby reducing monthly costs.

What is the average cost of a $500,000 20-year term life insurance quote for a healthy individual?

How To Pay For Business Insurance

How To Pay For Business InsuranceThe average cost of a $500,000 20-year term life insurance policy for a healthy individual typically ranges between $20 and $40 per month.

This range depends heavily on key factors such as age, gender, health profile, and lifestyle habits like smoking. For example, a healthy 35-year-old non-smoking male might pay around $27 per month, while a non-smoking female of the same age could pay closer to $22 due to longer average life expectancy.

These rates are based on policies issued by highly rated insurers and assume the applicant qualifies for a preferred or preferred plus health class. It's important to note that rates increase significantly with age, so a 45-year-old might pay roughly double what a 35-year-old pays for the same coverage.

- Age is one of the most significant determinants—premiums increase approximately 8% to 10% per year as you age, so securing a policy earlier can lead to substantial long-term savings.

- Health status plays a crucial role; applicants who are non-smokers, maintain a healthy weight, and have no history of chronic conditions like diabetes or high blood pressure usually qualify for the lowest rates.

- Gender also affects pricing, with women typically receiving lower premiums due to statistical longevity, though the gap has narrowed in recent years due to regulatory changes in some regions.

How Underwriting Class Impacts Your Rate

- Insurers categorize applicants into underwriting classes such as Standard, Preferred, Preferred Plus, and in some cases, Super Preferred, with each tier offering progressively lower premiums based on health and lifestyle.

- Qualifying for a Preferred Plus class could reduce your $500,000 20-year term policy by 20% to 30% compared to a Standard rate, making medical underwriting a critical part of the application process.

- Providing recent lab results, maintaining a clean driving record, and demonstrating stable finances can improve your chances of securing a higher risk classification and, consequently, lower costs.

Typical Costs by Age and Gender

- A 30-year-old non-smoking male might pay between $18 and $24 per month, while a female of the same age could expect to pay $15 to $20 for the same $500,000 20-year term policy.

- By age 40, premiums rise to approximately $28 to $38 for men and $23 to $30 for women, reflecting increased mortality risk over time.

- At age 50, rates can range from $50 to $70 monthly for men and $40 to $55 for women, showing how age accelerates premium growth even within a healthy applicant pool.

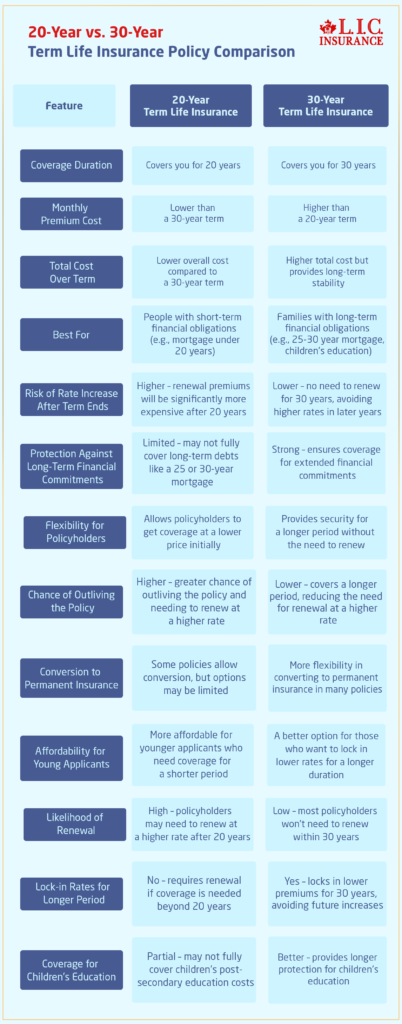

Is a 30-year term life insurance policy available compared to a 20-year term?

Yes, a 30-year term life insurance policy is available from many insurance providers, though it is less common than a 20-year term policy. The availability of a 30-year term depends on several factors, including the applicant’s age, health, and the specific underwriting guidelines of the insurer.

Generally, individuals seeking a 30-year term must apply at a younger age—typically in their 20s or early 30s—because insurers limit the maximum age at the end of the term (often capping it around age 70 to 80). In contrast, a 20-year term is more widely accessible to a broader age range and is offered by nearly all insurance companies.

While both policies provide level premiums and a death benefit for the duration of the term, the 30-year option ensures longer coverage, which can be beneficial for those with extended financial responsibilities such as long-term mortgages, special needs dependents, or late-life income replacement planning. However, premiums for a 30-year term are higher than those for a 20-year term due to the increased risk exposure over time.

Key Differences in Availability and Eligibility

- Insurance companies typically require applicants for a 30-year term policy to be younger, often under age 40, because the policy would extend coverage into the applicant’s 70s or beyond, increasing mortality risk for the insurer. In contrast, a 20-year term policy is available to applicants up to their early 60s in many cases, making it accessible to a wider demographic.

- Health underwriting is generally more stringent for 30-year terms because of the longer commitment. Individuals must demonstrate strong long-term health prospects to qualify, whereas 20-year policies may accommodate moderately higher health risks due to the shorter coverage period.

- Not all insurers offer 30-year term policies. Major providers like Haven Life, Policygenius-affiliated carriers, and some mutual life companies may offer them, but the selection is more limited compared to the nearly universal availability of 20-year policies.

- Premiums for a 30-year term life insurance policy are significantly higher than those for a 20-year term because the insurer assumes financial risk for an additional decade. This cost difference can range from 30% to 50% more depending on age and health classification.

- While the 30-year term offers extended protection, it may not be cost-effective for individuals whose major financial obligations—such as mortgage payments or children’s education—conclude within 20 years. In such cases, the added premium expense over ten extra years may not provide proportional value.

- Conversely, a 30-year term can offer better long-term value for younger couples purchasing a home with a 30-year mortgage or for those who anticipate ongoing dependents, such as caring for aging parents or a child with lifelong medical needs, where continued coverage is crucial beyond two decades.

Coverage Needs and Financial Planning Considerations

- Individuals with long-duration financial liabilities are more likely to benefit from a 30-year term. For example, someone starting a business with long-term debt, planning to co-sign a lengthy education loan, or supporting future generational needs may find the extended term more aligned with their risk exposure.

- Life stage plays a critical role in selecting the appropriate term. A 25-year-old with a newborn and a new home may prefer a 30-year policy to cover until the child is financially independent and the mortgage is paid. In comparison, a 45-year-old may only need coverage until retirement, making a 20-year term more suitable.

- It’s also important to consider future insurability. Locking in a 30-year term at a young age with favorable health can prevent the need to requalify later in life when health conditions may make coverage more expensive or unattainable, especially when compared to renewing or extending a 20-year policy after it expires.

What does a 20-year level term life insurance policy include in a quote?

A 20-year level term life insurance policy quote typically includes specific details that help applicants understand the costs and coverage offered for a two-decade period. These quotes are designed to provide clarity on premiums, death benefits, and any附加 conditions tied to the policy.

Insurers calculate the quote based on factors such as age, health, gender, lifestyle, and the desired death benefit amount. The term level refers to the stability of both the premium and the death benefit throughout the 20-year period, meaning neither will increase or decrease as long as premiums are paid on time. The quote will also outline any riders, exclusions, and requirements like medical exams.

Key Components Included in the Quote

- The death benefit amount, which is the sum paid to beneficiaries upon the insured's death during the policy term, is clearly stated. This is typically a fixed dollar amount chosen by the applicant, such as $250,000 or $500,000.

- The level premium, or the monthly or annual payment, is detailed in the quote. This amount remains constant for all 20 years, allowing for predictable budgeting regardless of aging or health changes during the term.

- Information about the insured person’s profile, including age, gender, tobacco usage, and health classification (e.g., preferred, standard, or substandard), is used to calculate and justify the quoted rate.

Underwriting Requirements and Health Disclosures

- The quote often comes with a requirement for medical underwriting, which may involve answering detailed health questions, authorizing medical records, or completing a paramedical exam including blood tests and blood pressure checks.

- Lifestyle factors such as occupation, travel habits, alcohol consumption, and participation in high-risk activities are assessed and factored into the quote to determine insurability and pricing.

- Pre-existing medical conditions like diabetes, heart disease, or a history of cancer can influence the quote, potentially resulting in higher premiums or exclusions if coverage is approved.

Policy Riders and Optional Add-Ons

- Some quotes include optional riders such as a waiver of premium for disability, which allows the policyholder to stop paying premiums if they become totally disabled during the term.

- An additional option might be a conversion rider, enabling the policyholder to convert the term policy into a permanent life insurance policy without a new medical exam before the term ends.

- Accidental death benefit riders may be offered, providing extra payout if the cause of death is due to an accident, although this increases the overall premium cost.

Frequently Asked Questions

What is a 20 year term life insurance quote?

A 20 year term life insurance quote is an estimate of how much you'll pay for a life insurance policy that provides coverage for exactly 20 years. It includes your monthly or annual premium based on factors like age, health, lifestyle, and coverage amount. The quote helps you compare policies and choose affordable protection for your family’s financial security during the two-decade term.

How is a 20 year term life insurance quote calculated?

Insurance providers calculate a 20 year term life insurance quote using factors such as your age, gender, health history, smoking status, occupation, and desired death benefit. Younger, healthier individuals typically receive lower rates. The insurer evaluates your risk profile to determine how likely you are to make a claim during the term, ensuring premiums reflect the level of risk over the 20-year period.

Can I lock in my 20 year term life insurance rate after getting a quote?

Yes, once you apply and are approved for a policy based on your quote, your premium is locked in for the full 20-year term. This means it won’t increase over time, as long as you pay on time. The quote reflects the rate you’ll pay throughout the policy, offering predictable and stable coverage costs for two decades, even if your health changes later.

Does a 20 year term life insurance quote include medical exams?

Most 20 year term life insurance quotes involve a medical exam, but some insurers offer no-exam policies. The exam typically includes basic health checks like blood pressure, height, weight, and blood or urine tests. Results impact your final rate. The quote you receive initially might be preliminary; your actual premium could change slightly based on exam findings and underwriting approval.

Leave a Reply