Best Child Life Insurance Plans

A child’s future is every parent’s greatest concern, and securing it financially is a crucial responsibility. Child life insurance plans offer not only protection but also a structured way to build savings for milestones like education and marriage.

These policies combine life coverage with investment components, ensuring financial stability even in unforeseen circumstances. With various options available, choosing the best child life insurance plan requires understanding benefits, payout structures, and long-term returns.

This article explores top-performing plans, highlighting features such as premium flexibility, bonuses, and early payout options to help parents make informed decisions for their child's secure and prosperous future.

Health Insurance Small Business Arizona

Health Insurance Small Business ArizonaTop-Rated Child Life Insurance Plans: Secure Your Child’s Future Today

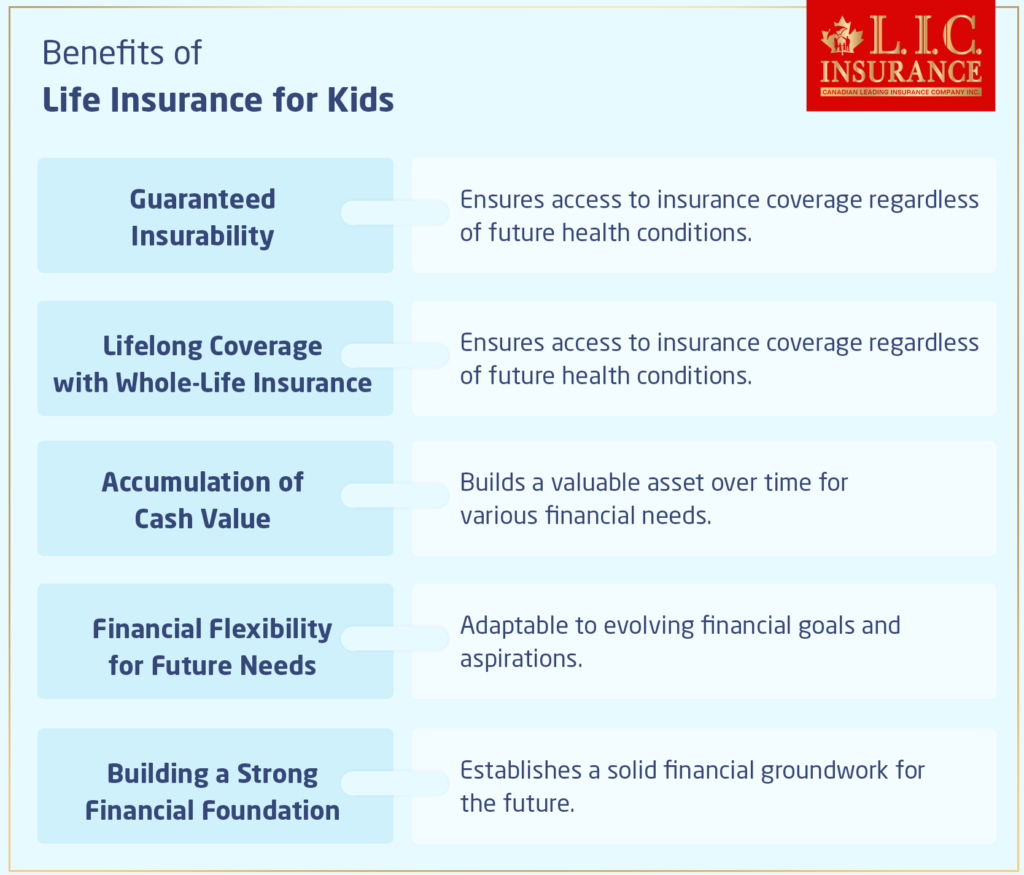

Investing in the best child life insurance plans is a proactive way for parents to ensure long-term financial protection and future stability. These policies are specifically designed to lock in coverage at an early age when health risks are minimal, guaranteeing insurability later in life regardless of medical changes.

Unlike traditional life insurance focused on income replacement, child life insurance often emphasizes permanent coverage with a cash value component that grows over time. This can be used for important life milestones such as education, a first home, or emergencies.

Leading insurance providers offer customizable plans with affordable premiums, making it easier for families to find coverage that fits their budget while securing critical benefits. When evaluating options, it’s essential to consider policy duration, cash value accumulation, and rider availability to maximize value and future utility.

Types of Child Life Insurance Policies Available

There are primarily two types of child life insurance plans: whole life and term life. Whole life insurance is the most common choice for children because it offers lifelong coverage, a guaranteed death benefit, and a cash value component that accumulates over time.

How Much Business Insurance Do You Need

How Much Business Insurance Do You NeedThis cash value can be borrowed against or withdrawn in the future, providing flexibility for major expenses. Whole life policies for children typically come with level premiums that remain the same throughout the life of the policy, making long-term planning easier. On the other hand, term life insurance provides coverage for a set period—usually 10, 20, or 30 years—and is often more affordable.

However, it doesn't build cash value and expires at the end of the term, offering no financial return if not claimed. Most financial advisors recommend whole life plans for children due to their dual benefit of protection and growth potential.

Key Benefits of Enrolling Your Child Early

Purchasing life insurance for a child at a young age comes with several compelling advantages. First, premiums are significantly lower when the policy is issued during infancy or early childhood because the risk of health complications is minimal.

This allows families to lock in affordable rates that won’t increase over time. Second, enrolling early ensures guaranteed insurability, meaning the child will remain covered for life even if they develop health issues in adulthood that would otherwise make them uninsurable.

How To Bundle Business Insurance For Savings

How To Bundle Business Insurance For SavingsThird, the cash value growth in permanent policies benefits from compounding over decades, potentially resulting in a substantial financial reserve by adulthood. Additionally, some policies offer riders like accelerated death benefits or waiver of premium, which enhance flexibility and protection, making early enrollment a smart financial move.

Top Providers Offering the Best Child Life Insurance Plans

Several reputable insurance companies stand out for their comprehensive child life insurance offerings. Companies like Northwestern Mutual, New York Life, and Mutual of Omaha are frequently ranked among the best due to their financial strength, customer service, and policy customization options.

These providers offer no medical exam policies for young children, simplifying the application process. They also allow policies to be converted or expanded as the child ages, sometimes even enabling the policyholder to attach a payor rider, which waives premiums if the parent or guardian becomes disabled.

Customer reviews often highlight transparent pricing, straightforward claims processing, and reliable performance. Evaluating features such as cash value interest rates, dividend payouts (in participating policies), and available riders is critical when selecting the right provider.

How To Pay For Business Insurance

How To Pay For Business Insurance| Insurance Provider | Policy Type | Minimum Coverage | Premium Starting At | Notable Features |

|---|---|---|---|---|

| Northwestern Mutual | Whole Life | $10,000 | $50/month | High cash value growth, dividend-paying policies |

| New York Life | Whole Life | $5,000 | $40/month | Flexible payment options, strong financial ratings |

| Mutual of Omaha | Whole Life | $5,000 | $35/month | No medical exam required, payor rider available |

| Transamerica | Whole Life | $5,000 | $30/month | Affordable entry-level plans, conversion options |

| State Farm | Whole Life | $10,000 | $55/month | Local agent support, strong customer service |

Best Child Life Insurance Plans: A Comprehensive Guide to Secure Your Child's Future

What are the top-rated life insurance plans for children in 2024?

Top-Rated Life Insurance Providers Offering Children's Policies in 2024

- Northwestern Mutual is widely recognized for its strong financial stability and customizable life insurance options for children. Their child riders can be added to a parent’s permanent life insurance policy, allowing the child to inherit coverage that can be converted into an individual policy later in life without requiring a medical exam.

- New York Life offers guaranteed issue child riders on their whole life policies, making it a popular choice among parents seeking long-term coverage. These riders typically provide up to $50,000 in coverage and lock in insurability from an early age, regardless of future health issues.

- Guardian Life provides competitive child term and whole life insurance options with a strong track record for customer service. Their child policies often include living benefits and can be tailored to grow with the child into adulthood, offering conversion options and cash value accumulation.

Types of Life Insurance Plans Available for Children

- Child riders attached to a parent’s permanent life policy are the most common form of children’s life insurance. These are typically low-cost, offer fixed coverage amounts (usually $5,000 to $50,000), and are guaranteed issue—meaning no medical underwriting is required.

- Standalone whole life policies for children are also available, allowing parents to purchase a small policy directly in the child’s name. These policies build cash value over time and can be used in the future for expenses like education, though their primary purpose is lifelong protection.

- Term life insurance for children is rare, as there is minimal demand for temporary coverage on a young child. However, some insurers provide level-term options as part of a family plan, usually lasting until the child reaches early adulthood (e.g., age 25).

Key Benefits and Considerations When Choosing a Child Life Insurance Plan

- Locking in insurability at a young age ensures that the child will have access to life insurance in adulthood, even if they develop medical conditions later. This is one of the most compelling reasons to purchase coverage early, especially with convertible riders.

- Cash value accumulation in whole life policies can offer a financial resource later in life, which can be accessed via loans or withdrawals. While returns are generally modest, the savings component adds long-term value beyond just the death benefit.

- Cost-effectiveness is notable, as insuring a healthy child is generally very affordable. However, families should evaluate whether the long-term financial commitment aligns with broader financial goals, such as college savings or retirement planning.

What are the benefits of choosing the best child life insurance plans for your family’s financial security?

Long-Term Financial Protection for Your Child’s Future

- One of the primary benefits of selecting the best child life insurance plan is securing long-term financial protection for your child. Even at a young age, having a policy in place ensures that they will have a financial foundation as they grow into adulthood. This foundation can support future goals such as higher education, buying a first home, or starting a business.

- These policies often accumulate cash value over time, especially permanent life insurance plans, which build savings that can be accessed later in life. This cash value grows tax-deferred and can serve as a financial safety net during emergencies or major life events.

- By locking in coverage early, you also ensure insurability. Health conditions that may arise later in life won’t affect the child’s eligibility, allowing them to maintain coverage regardless of future medical changes, providing peace of mind for the entire family.

Protection Against Unexpected Financial Burdens

- Although the loss of a child is unimaginable, a life insurance policy can help cover unexpected expenses such as funeral costs, medical bills, or outstanding debts. These costs can place a significant financial strain on families during an already emotionally difficult time, and having a plan helps mitigate that stress.

- Some policies offer riders or additional benefits that can provide financial support for counseling services or family therapy, helping loved ones cope with grief in a healthy and sustainable way.

- Choosing a comprehensive plan ensures that funds are readily available when needed most, allowing families to focus on healing rather than financial logistics during a crisis.

Building a Foundation for Lifelong Financial Responsibility

- Child life insurance plans can serve as an educational tool, teaching children about financial responsibility, savings, and the importance of planning for the future. As they grow, parents can involve them in understanding the policy's growth and how financial decisions impact long-term outcomes.

- Many policies allow children to take ownership of the policy when they reach adulthood, transitioning the responsibility and encouraging them to manage their own financial affairs. This early exposure fosters independence and informed decision-making.

- By instilling these values early, families lay the groundwork for stronger financial habits, helping the child avoid debt, budget effectively, and appreciate the long-term benefits of consistent saving and investment.

Frequently Asked Questions

What are the best child life insurance plans available?

Some of the best child life insurance plans include whole life policies from providers like Northwestern Mutual, New York Life, and Mutual of Omaha. These plans offer lifelong coverage, build cash value, and often allow conversion to adult policies. They are designed to secure low premiums early and provide financial protection for future needs, such as funeral costs or estate planning.

Why should I consider life insurance for my child?

Life insurance for a child offers financial protection in the rare event of a child’s passing, covering funeral and medical expenses. It also locks in insurability, ensuring coverage even if the child develops health issues later. Many policies accumulate cash value, which can be used for future needs like education, and may be converted to adult coverage without a medical exam.

Are child life insurance plans worth the investment?

Child life insurance plans can be worth it for families seeking long-term financial planning and guaranteed insurability. While the immediate need is low, these policies often build cash value over time and lock in affordable premiums. They provide peace of mind and future flexibility, especially if the child develops health conditions that could make obtaining insurance later more difficult or expensive.

What types of coverage are included in child life insurance policies?

Child life insurance policies typically offer whole life coverage with level premiums and a death benefit. Many include cash value accumulation that grows over time and can be borrowed against. Some policies allow riders for additional benefits and offer conversion options to adult life insurance. Coverage amounts usually range from $10,000 to $50,000, designed to meet future financial needs.

Leave a Reply