Bga Insurance Life Insurance

BGA Insurance offers comprehensive life insurance solutions designed to provide financial security and peace of mind for individuals and families.

As a trusted name in the insurance industry, BGA specializes in tailoring policies that meet diverse needs, whether it’s term life, whole life, or universal life coverage. With a focus on affordability, flexibility, and customer service, BGA Insurance helps clients protect their loved ones from unforeseen circumstances.

Their experienced advisors work closely with policyholders to assess risks, determine appropriate coverage levels, and ensure long-term financial stability. BGA Insurance combines industry expertise with personalized attention, making life insurance accessible and straightforward for everyone.

How To Purchase Workers Compensation Insurance Online For Business

How To Purchase Workers Compensation Insurance Online For BusinessBGA Insurance Life Insurance: Comprehensive Coverage for Long-Term Financial Security

BGA Insurance offers a robust selection of life insurance products designed to meet the diverse needs of individuals and families seeking long-term financial protection.

As part of a trusted network of independent insurance agencies, BGA Insurance collaborates with top-rated carriers to provide customizable policies, including term life, whole life, and universal life insurance. These policies are structured to deliver essential benefits such as death benefits, cash value accumulation, and tax advantages, ensuring policyholders can safeguard their loved ones’ futures.

With a focus on personalized service, BGA Insurance helps clients assess their financial goals, evaluate coverage needs, and select plans offering optimal value and reliability in uncertain times.

Types of Life Insurance Policies Offered by BGA Insurance

BGA Insurance provides access to a broad spectrum of life insurance solutions tailored to various life stages and financial objectives.

Insurance Brokers Business

Insurance Brokers BusinessClients can choose from term life insurance, ideal for temporary coverage needs such as mortgage protection or income replacement during working years, typically offered in 10-, 20-, or 30-year durations. For those seeking permanent protection, whole life insurance offers fixed premiums, guaranteed cash value growth, and lifelong coverage.

Additionally, universal life insurance provides flexible premiums and adjustable death benefits, allowing policyholders to adapt their coverage as financial circumstances change. Each product is sourced from financially strong insurers, ensuring reliability and long-term security.

Benefits of Choosing BGA for Life Insurance Needs

Selecting BGA Insurance for life coverage offers multiple advantages, beginning with its role as an independent agency.

This independence enables BGA to shop multiple carriers on behalf of clients, ensuring the best possible rates and policy features without being tied to a single provider. Clients benefit from personalized consultations, where licensed agents assess individual needs, family structures, and future goals to recommend optimal coverage.

Insurance Business Architecture

Insurance Business ArchitectureAdditional benefits include fast underwriting processes, transparent policy terms, and ongoing support for policy management and claims. The emphasis on customer education ensures that clients make informed decisions, understanding the nuances of riders, exclusions, and premium structures.

How to Apply for Life Insurance Through BGA Insurance

The application process for life insurance through BGA Insurance is straightforward and client-focused. It begins with a free consultation, during which an agent gathers essential information about health history, lifestyle, financial obligations, and coverage goals. Based on this assessment, the agent presents tailored policy options from multiple insurers.

Applicants then complete a formal application, which may include a medical exam depending on the policy type and coverage amount. BGA facilitates the entire process, liaising with underwriters and expediting approvals to ensure a seamless experience. Once approved, clients receive their policy documents and can begin building financial protection immediately.

| Policy Type | Coverage Duration | Cash Value | Best For |

|---|---|---|---|

| Term Life | 10, 20, or 30 years | No | Temporary needs, budget-conscious buyers |

| Whole Life | Lifetime | Yes, guaranteed growth | Permanent protection, estate planning |

| Universal Life | Lifetime (flexible) | Yes, market-linked or fixed | Adaptable premiums, wealth accumulation |

BGA Insurance Life Insurance: A Comprehensive Guide to Coverage Options and Benefits

What is BGA Insurance and How Does It Relate to Life Insurance?

Insurance Business Strategy

Insurance Business StrategyWhat Is BGA Insurance?

BGA Insurance refers to services provided by Brokerage and General Agency organizations that act as intermediaries between insurance carriers and independent insurance agents or agencies. These entities do not underwrite policies themselves but instead support agents by offering access to multiple insurance products, administrative assistance, training, and marketing resources.

BGAs play a crucial role in the distribution chain of insurance, particularly in the life insurance sector, by enabling agents to represent multiple carriers without establishing individual contracts with each company.

- BGAs source and negotiate contracts with insurance carriers to provide competitive life insurance products to agents and brokers.

- They offer back-office support, compliance guidance, and technology platforms that help agents manage policies and client information efficiently.

- Many BGAs also provide product training, licensing assistance, and ongoing professional development to strengthen agent performance in selling life insurance.

How Does BGA Insurance Support Life Insurance Distribution?

BGAs enhance the distribution of life insurance by streamlining the process for agents to offer diverse and competitive policies.

By consolidating relationships with various life insurance carriers, BGAs allow agents to present clients with multiple options under one partnership, improving efficiency and customer choice. This model benefits both new and experienced agents who need tools and expertise to navigate complex underwriting guidelines, policy comparisons, and client education around term, whole, and universal life products.

Insurance For A Landscaping Business

Insurance For A Landscaping Business- Agents affiliated with a BGA can quickly compare life insurance quotes from several carriers, helping clients find the most suitable coverage at competitive rates.

- BGAs often provide marketing materials, lead generation tools, and client enrollment systems designed specifically for life insurance sales.

- They facilitate faster policy underwriting and issuance by ensuring agents adhere to carrier-specific requirements and submit complete applications.

What Is the Relationship Between BGAs and Independent Life Insurance Agents?

The relationship between BGAs and independent life insurance agents is built on partnership and mutual support. Independent agents rely on BGAs to access a broad portfolio of life insurance products while maintaining their business autonomy.

BGAs, in turn, benefit from the production and client reach of the agents they support. This symbiotic relationship allows independent agents to compete with larger agencies by offering comprehensive solutions and personalized service, backed by the infrastructure provided by the BGA.

- Agents receive access to multiple insurance carriers through a single BGA affiliation, increasing their ability to match clients with optimal life insurance plans.

- BGAs often provide commission structures, performance incentives, and revenue-sharing models that reward agent productivity in life insurance sales.

- Ongoing support from BGAs—including assistance with policy servicing and claims—helps independent agents maintain strong client relationships over the life of a policy.

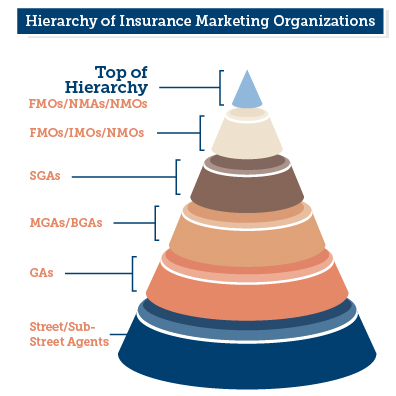

What distinguishes IMO from BGA in the context of BGA Insurance life insurance services?

Organizational Structure and Role in Distribution

- Independent Marketing Organizations (IMOs) function as third-party entities that recruit, train, and support independent insurance agents, particularly in the life insurance sector, acting as intermediaries between agents and insurance carriers. They typically provide logistical support, compliance oversight, and marketing resources.

- Brokerage General Agencies (BGAs), on the other hand, operate with a more formalized hierarchy and broader authority than IMOs. BGAs often have contractual agreements with insurers that allow them to underwrite policies, appoint agents, and manage commission structures directly, giving them greater control over distribution.

- While both IMOs and BGAs serve as channels for distributing BGA Insurance life insurance products, BGAs usually have a deeper integration with the insurer’s operational systems, allowing for more direct influence on policy issuance and agent performance.

- IMOs traditionally focus on agent recruitment and education, with limited contractual authority from insurance carriers. Their relationship with carriers like BGA Insurance is often indirect, with IMOs facilitating agent access but not managing policy contracts or binding coverage.

- BGAs, by contrast, frequently hold appointed power of attorney from insurers, enabling them to sign contracts on behalf of the carrier, manage blocks of business, and provide underwriting guidance. This grants BGAs a higher level of responsibility and influence.

- In the context of BGA Insurance, BGAs may be directly involved in designing compensation plans, setting sales goals, and overseeing compliance for life insurance policies, whereas IMOs generally support these activities without holding decision-making power.

Agent Support and Operational Services

- IMOs primarily offer training, licensing assistance, and lead generation tools to independent agents selling BGA Insurance life insurance products. Their support is often centered around increasing agent productivity through education and marketing materials.

- BGAs provide a more comprehensive suite of backend services, including case management, policy illustration software, compliance monitoring, and direct access to underwriting departments, which streamlines the life insurance application process.

- Agents aligned with a BGA may experience faster policy placements and enhanced servicing due to the BGA’s established infrastructure and direct carrier relationships, while those working through an IMO might rely more on external platforms and CRM tools for similar functions.

Frequently Asked Questions

What types of life insurance does BGA Insurance offer?

BGA Insurance offers term life, whole life, and universal life insurance policies. Term life provides coverage for a specific period, ideal for temporary needs. Whole life offers lifelong protection with fixed premiums and cash value accumulation. Universal life provides flexibility in premium payments and death benefits, along with potential cash growth. These options cater to diverse financial goals, ensuring clients can find a plan that suits their long-term protection and investment needs.

How can I apply for a life insurance policy with BGA Insurance?

You can apply for a BGA Insurance life policy online, by phone, or through a licensed agent. The process typically involves completing an application, answering health and lifestyle questions, and possibly undergoing a medical exam. Once submitted, BGA reviews your information and provides a decision, often within a few weeks. Approval leads to policy issuance, and coverage becomes effective once the first premium is paid.

Can I customize my BGA life insurance policy?

Yes, BGA Insurance allows policy customization to fit individual needs. You can adjust coverage amounts, select policy terms, and add riders such as accidental death, waiver of premium, or accelerated death benefit. These options enhance protection and flexibility. Working with a BGA agent helps ensure your policy aligns with your financial objectives and personal circumstances, making it easier to adapt coverage as life changes occur over time.

Premiums with BGA Insurance are influenced by age, health, lifestyle, occupation, and coverage amount. Younger, healthier individuals typically pay lower rates. Smoking, high-risk hobbies, and certain medical conditions can increase costs. The type of policy and selected riders also impact pricing. BGA evaluates these factors during underwriting to determine risk and set fair premiums, ensuring affordable and personalized coverage for each applicant.

Leave a Reply