Do Uber Drivers Need Special Insurance

Ridesharing has transformed urban transportation, with millions relying on services like Uber daily. However, a critical question arises for drivers: do they need special insurance? Standard personal auto policies often exclude coverage when a vehicle is used for commercial purposes, leaving drivers vulnerable during trips.

Uber provides some insurance, but gaps exist depending on the driver’s activity—whether waiting for a ride request or en route to pick up a passenger. Without proper coverage, drivers could face significant financial risks in the event of an accident. Understanding the intricacies of rideshare insurance is essential for protection, compliance, and peace of mind on the road.

Do Uber Drivers Need Special Insurance?

Uber drivers operate in a unique space between personal and commercial vehicle use, which raises critical questions about insurance coverage.

Do I Need Special Insurance To Doordash

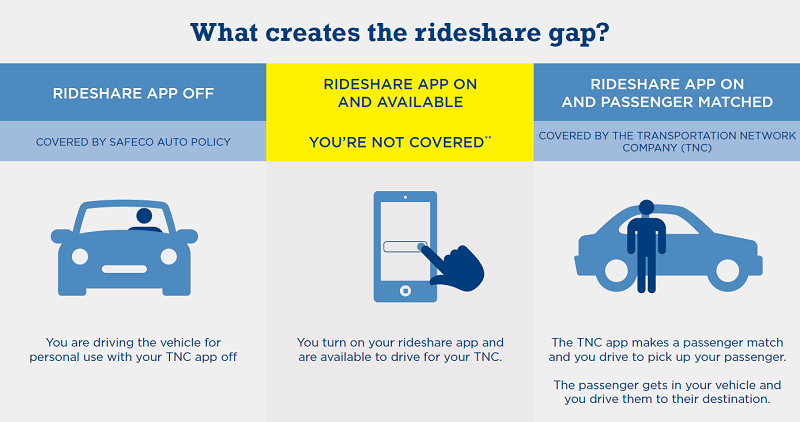

Do I Need Special Insurance To DoordashStandard personal auto insurance policies are typically not designed to cover drivers when they are using their vehicles for ride-sharing services like Uber. When an individual becomes an Uber driver, their vehicle transitions from purely personal use to a form of commercial activity, particularly during specific periods such as when the app is on and they are either waiting for a ride request, en route to pick up a passenger, or actively transporting a rider.

Without proper coverage during these phases, drivers could face significant financial liability in the event of an accident. Therefore, understanding whether and when special insurance is required is essential for protecting both the driver and others on the road.

When Does Personal Insurance Fall Short for Uber Drivers?

Most standard personal auto insurance policies explicitly exclude coverage when a vehicle is used for commercial purposes, which includes ride-sharing services. While personal insurance may still apply when the Uber app is completely off, it often does not cover the times when the app is active—specifically during periods when the driver is logged into the app and available for rides, even if no passenger has been picked up yet.

This gap in coverage is significant because accidents can occur during these transitional phases, and without proper protection, drivers could be held personally responsible for damages, medical expenses, or legal fees. As a result, relying solely on personal insurance is not sufficient for those driving for Uber.

Do I Need Special Insurance To Drive For Lyft

Do I Need Special Insurance To Drive For LyftWhat Insurance Coverage Does Uber Provide?

Uber does offer its own commercial insurance coverage, but it’s important to understand that this coverage activates only at specific times during a driver’s trip.

When the driver logs into the app, Uber’s liability insurance typically begins, providing coverage if the driver causes injury or damage to others while waiting for a ride request. Once a trip is accepted and the driver is en route to pick up the passenger or has the passenger in the car, Uber's coverage increases significantly, including higher liability limits, collision coverage, and comprehensive protection.

However, this Uber-provided insurance acts as a secondary or primary layer depending on the period, and it may not cover everything such as personal medical expenses or damage to personal property, which is why supplemental insurance may still be necessary.

Rideshare insurance is a specialized policy designed to fill the gaps left by both personal auto insurance and the coverage provided by Uber.

Do I Need Special Insurance To Drive For Uber

Do I Need Special Insurance To Drive For UberOffered by many major insurance companies, this type of policy extends protection during all phases of driving for Uber—from when the app is on and you’re waiting for a ride request to when you're actively giving a ride. It typically supplements your personal policy during commercial use without leading to cancellation of your existing plan.

For drivers, obtaining rideshare insurance can be a cost-effective way to ensure continuous protection and avoid potential denial of claims due to commercial use exclusions. Given the risks involved and the limitations of both personal and Uber-provided insurance, having this additional layer is strongly recommended.

| Insurance Period | Personal Insurance | Uber’s Insurance | Recommended Rideshare Insurance |

|---|---|---|---|

| App is Off | Full coverage | No coverage | Not needed |

| App is On, No Ride Accepted | Gaps in coverage | Liability only (varies by state) | Highly recommended |

| En Route to Passenger | No coverage | Primary coverage: Liability, collision, comprehensive | Supports continuity |

| Passenger in Car | No coverage | Full commercial coverage | Supplemental benefit |

Do Uber Drivers Need Special Insurance? A Comprehensive Guide

What Insurance Coverage Do Uber Drivers Need While Driving?

Personal Auto Insurance and Its Limitations for Uber Drivers

- Most Uber drivers start with a personal auto insurance policy, which typically covers daily commuting and personal use of the vehicle.

- However, standard personal policies often exclude coverage when the vehicle is used for commercial purposes, such as transporting passengers for payment.

- Drivers may face denied claims or policy cancellation if they're involved in an accident while logged into the Uber app, even if no passenger is in the car, because insurers view app activation as engaging in rideshare activity.

Uber’s Provided Insurance Coverage During Different Trip Phases

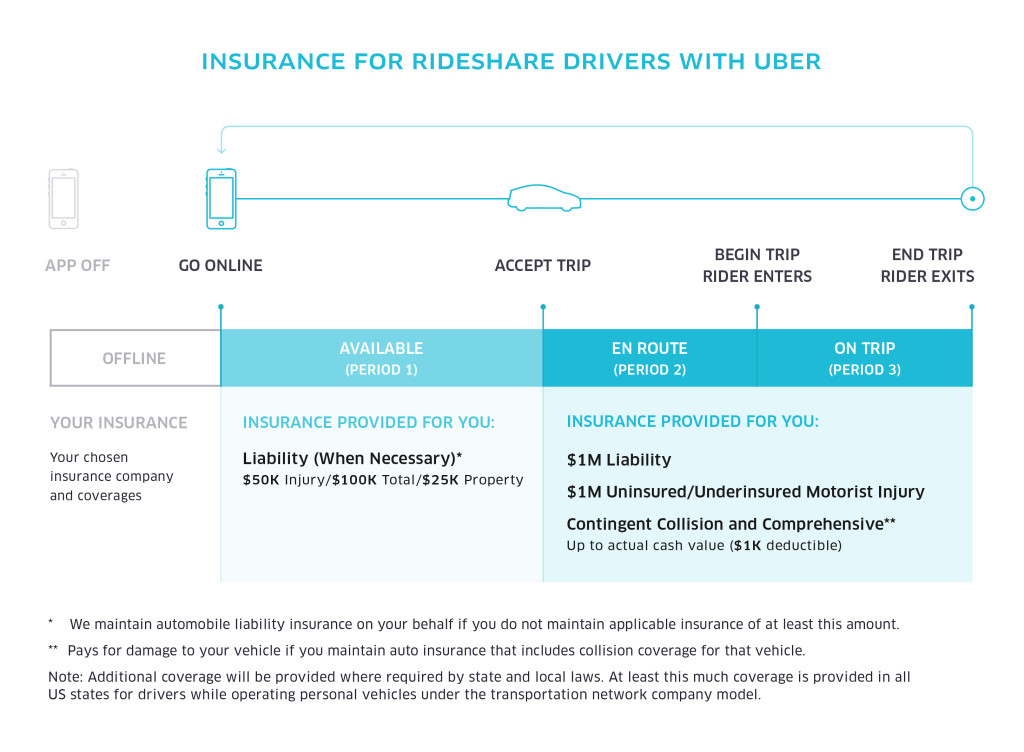

- Uber supplies contingent insurance that activates only when the driver is logged into the app and remains in effect across three distinct periods defined by Uber.

- Period 1 begins when a driver logs into the app and is waiting for a ride request. During this phase, Uber offers limited liability coverage, usually up to $50,000 per person, $100,000 per accident for bodily injury, and $25,000 for property damage, but only if a personal insurance denial occurs.

- Periods 2 and 3—once a ride is accepted and while transporting a passenger—include higher liability limits, often up to $1 million, along with collision and comprehensive coverage subject to a deductible, provided the driver's personal insurance does not cover the incident.

- To close coverage gaps, especially when personal policies decline claims during Period 1, drivers are advised to purchase a commercial rideshare insurance policy or an endorsement from their insurer.

- These specialized policies are designed explicitly for rideshare use, providing continuous protection regardless of app status and eliminating disputes between personal insurers and rideshare companies.

- Many major insurance companies now offer rideshare endorsements that extend personal policies to include commercial driving periods, offering more affordable and seamless coverage than standalone commercial policies while meeting Uber’s insurance expectations.

What Type of Insurance Is Required for Uber Drivers?

Do I Need Special Insurance To Drive For Uber Eats

Do I Need Special Insurance To Drive For Uber EatsPersonal Auto Insurance Coverage During Offline Periods

When Uber drivers are not actively using the app—meaning they are logged out or the app is turned off—only their personal auto insurance policy applies. During this time, if an accident occurs, the driver’s personal insurance is solely responsible for covering damages or injuries.

However, many personal auto insurance policies explicitly exclude coverage for commercial activities, which ride-sharing can be considered. This creates a potential coverage gap that drivers may overlook.

- Drivers should review their personal auto insurance policy to confirm whether ride-sharing activities are covered at any stage.

- Many insurers now offer ride-sharing endorsements or add-ons that extend coverage to periods when the driver is logged into the Uber app but hasn’t accepted a ride.

- Without proper endorsement, a claim could be denied if the insurer determines the vehicle was being used for commercial purposes at the time of the accident.

Uber’s Commercial Insurance During Ride Acceptance

Once an Uber driver accepts a trip request, the company’s commercial insurance policy becomes active and provides primary coverage. This is the highest level of protection offered by Uber and applies from the moment the driver is en route to pick up the passenger until the end of the trip. This coverage includes liability, collision, and uninsured motorist protection, which safeguards both the driver and passengers.

- Uber’s liability coverage typically includes up to $1 million in third-party liability per incident during active trip periods.

- The company also provides collision and comprehensive coverage, but drivers may be responsible for a deductible if they file a claim.

- This commercial policy fully supersedes the driver’s personal insurance during active trips, ensuring continuous protection throughout the ride.

Interim Coverage When the App Is On But No Ride Is Accepted

There is a middle phase when an Uber driver has the app open and is available to receive ride requests but hasn’t yet accepted a trip. During this period, Uber provides contingent liability coverage, which comes into effect only if the driver’s personal insurance denies the claim. This coverage helps bridge a critical gap but is secondary rather than primary.

- Uber offers contingent liability coverage of up to $1 million during this available phase, but it activates only after personal insurance declines the claim.

- Drivers must carry at least the state-minimum auto insurance to qualify for Uber’s interim coverage.

- Because this coverage is secondary, any delays or disputes with the personal insurer can affect claim processing, making it essential for drivers to maintain valid personal coverage at all times.

Frequently Asked Questions

Do Uber Drivers Need Special Insurance?

Yes, Uber drivers need special insurance because personal auto policies typically don’t cover commercial driving activities. While Uber provides some insurance coverage during specific periods of the trip—such as when a driver has accepted a ride—there may be gaps. Drivers need additional coverage, often called rideshare insurance, to ensure they're protected during all phases of driving for Uber, including when the app is on but no ride is active.

When Does Uber’s Insurance Coverage Start?

Uber's insurance coverage begins when the driver turns on the app and is available to accept rides, but full protection starts only after a ride is accepted. From that point—period 2 (en route to pick up) and period 3 (during the trip)—Uber provides liability, collision, and comprehensive coverage. However, during period 1 (app is on but no ride accepted), only liability coverage with high deductibles applies, so personal or rideshare insurance is recommended.

Can I Use My Personal Car Insurance for Uber Driving?

No, you cannot rely solely on personal car insurance when driving for Uber. Most personal auto policies exclude coverage for commercial use, and filing a claim while engaged in rideshare activities may lead to denial or policy cancellation. Using your car for Uber requires rideshare-endorsed insurance or a rideshare add-on to ensure continuous protection during all driving periods related to the service.

If you're in an accident while driving for Uber without proper rideshare insurance, you could face significant out-of-pocket expenses. Personal insurance may deny the claim due to commercial use, and Uber’s coverage might not apply depending on the phase of the trip. This leaves drivers vulnerable to liability, repair costs, and legal fees. Having dedicated rideshare insurance ensures comprehensive protection and peace of mind.

Leave a Reply