Do Uber Drivers Need Special Car Insurance

Rideshare drivers face unique risks that standard personal car insurance policies often don’t cover. When working for Uber, drivers transition between personal use and commercial activity, creating coverage gaps that can leave them financially exposed in the event of an accident.

While Uber provides some insurance during specific periods of a trip, the extent of protection varies depending on driver status—logged in, accepting rides, or transporting passengers.

Many drivers assume their personal policy is sufficient, but most exclude commercial use. Understanding Uber’s insurance policy structure and the need for additional rideshare coverage is essential for financial protection and peace of mind on the road.

Do I Need Special Insurance To Doordash

Do I Need Special Insurance To DoordashDo Uber Drivers Need Special Car Insurance?

Uber drivers operate in a unique space where personal vehicle use overlaps with commercial activity, which significantly affects their insurance needs. Standard personal auto insurance policies typically do not cover drivers when they are working for ride-sharing services like Uber.

This creates a coverage gap during different phases of a ride-share trip—such as when the driver is logged into the app but hasn't accepted a ride, during passenger pickup, or while transporting passengers. As a result, rideshare companies like Uber do provide insurance, but the extent and timing of coverage vary depending on the stage of the trip.

Drivers must understand these nuances to avoid being underinsured or facing out-of-pocket expenses in the event of an accident. Therefore, while not all states mandate additional policies, many drivers choose or are required to obtain rideshare-specific insurance to bridge the gaps left by both personal policies and the limited coverage provided by Uber.

When Does Personal Auto Insurance Not Cover Uber Drivers?

Most personal auto insurance policies explicitly exclude coverage when the vehicle is used for commercial purposes, and driving for Uber qualifies as such. When a driver logs into the Uber app, they are technically offering transportation services for compensation, which shifts the use of the vehicle from personal to commercial.

Do I Need Special Insurance To Drive For Lyft

Do I Need Special Insurance To Drive For LyftDuring this time—specifically Period 1 (app on, no ride accepted)—many personal insurers consider the driver uninsured for any accidents that occur. Even if the policy doesn't immediately cancel, a claim filed during ride-share activity could be denied, leaving the driver financially liable.

Some insurers may even see this as a breach of contract and terminate the policy altogether. Therefore, drivers must notify their insurance providers if they plan to drive for Uber, or risk losing coverage entirely during critical moments.

What Insurance Coverage Does Uber Provide to Drivers?

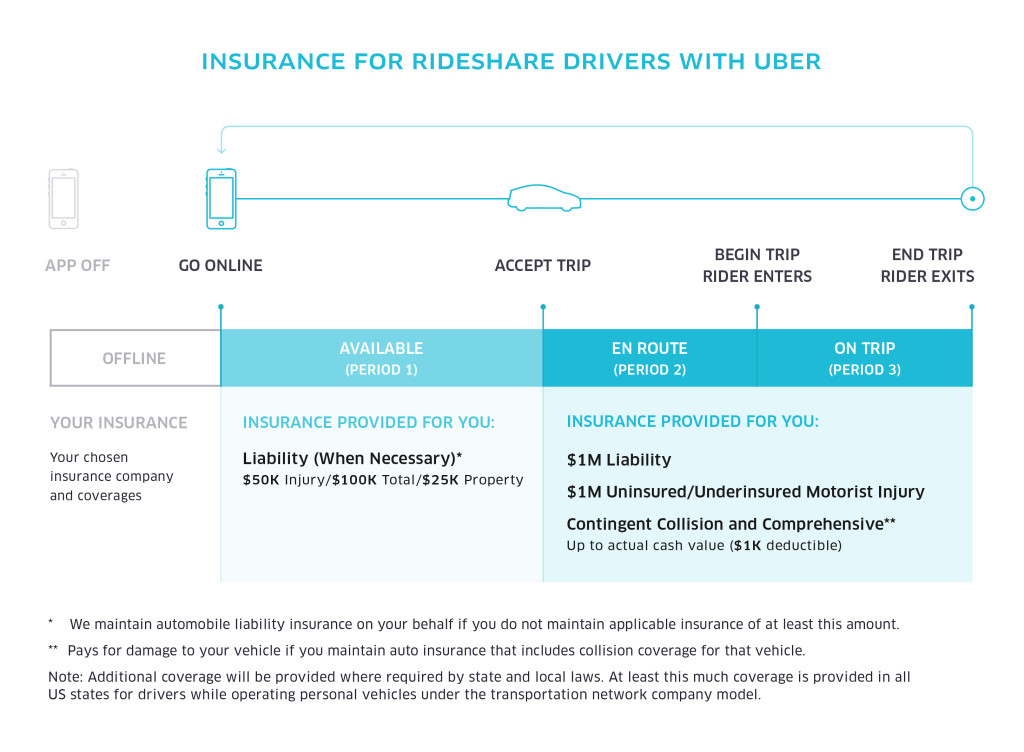

Uber provides contingent liability insurance that activates in stages depending on the driver's activity within the app.

During Period 1 (waiting for a ride request), Uber offers limited liability coverage—typically $50,000 per person, $100,000 per accident for bodily injury, and $25,000 for property damage, along with uninsured motorist coverage. Once a driver accepts a trip (Period 2) and during passenger transport (Period 3), coverage increases significantly to $1 million in liability protection.

Do I Need Special Insurance To Drive For Uber

Do I Need Special Insurance To Drive For UberAdditionally, Uber offers collision and comprehensive coverage options for damage to the driver’s vehicle if they use their own insurance as primary and file a claim through their insurer. However, this contingent coverage only applies when the driver is actively engaged in the ride-share process and does not replace the need for a proper insurance strategy that includes personal and possibly dedicated ride-share policies.

Rideshare insurance is a specialized policy or add-on endorsement offered by many major insurers designed to cover the gaps between personal auto policies and the coverage provided by companies like Uber.

It typically extends protection during all phases of ride-sharing, particularly in Period 1, when drivers are most vulnerable. This type of insurance can serve as secondary or primary coverage, depending on the provider and policy structure, and may include liability, collision, and comprehensive benefits tailored to commercial driving risks.

Drivers in states where personal policies automatically exclude ride-share use are strongly encouraged—or even required—to obtain this additional coverage. Given the potential financial risks of accidents during rideshare activity, any driver using their vehicle for Uber should evaluate their current policy and consider adding a rideshare endorsement to ensure continuous, reliable protection.

Do I Need Special Insurance To Drive For Uber Eats

Do I Need Special Insurance To Drive For Uber Eats| Insurance Phase | Uber Coverage | Personal Insurance Status |

|---|---|---|

| Period 1: App on, no ride accepted | $50,000/$100,000/$25,000 liability + uninsured motorist | Not covered by standard personal policy |

| Period 2: Ride accepted, en route to passenger | $1 million liability, contingent comprehensive/collision | Gaps exist; personal policy may deny claims |

| Period 3: Passenger in car | $1 million liability, damage coverage with deductible | Not applicable; commercial use voids personal coverage |

Do Uber Drivers Need Special Car Insurance? A Complete Guide

What Insurance Coverage Do Uber Drivers Need for Ridesharing?

Uber drivers require a combination of personal auto insurance and specialized rideshare coverage to remain protected throughout all stages of their work.

Standard personal auto insurance policies typically exclude coverage when a vehicle is used for commercial purposes, such as transporting passengers for money. However, ridesharing blurs the line between personal and commercial use, creating coverage gaps. To address this, many insurance companies now offer rideshare-endorsed policies or supplemental coverage designed specifically for gig economy drivers.

These policies usually provide protection during all three periods of rideshare activity: when the driver is waiting for a ride request, en route to pick up a passenger, and actively transporting a passenger. Uber also provides its own commercial insurance, but it only activates during certain periods, making it crucial for drivers to verify their personal policy's compatibility with ridesharing.

- Drivers must carry a valid personal auto insurance policy that meets their state's minimum liability requirements before driving for Uber.

- They should confirm whether their insurer offers a rideshare endorsement, which extends personal coverage to periods when the app is active but no passenger is in the vehicle.

- Drivers are responsible for maintaining continuous insurance coverage to remain eligible on the Uber platform and to avoid personal financial liability in case of an accident.

Understanding Uber’s Built-In Insurance Coverage

Uber provides a commercial insurance policy that supplements drivers’ personal coverage during specific phases of rideshare activity.

This built-in coverage includes liability insurance, uninsured/underinsured motorist protection, and contingent collision and comprehensive coverage, but its availability depends on the driver’s current status within the app. For example, when a driver logs into the Uber app and is waiting for a ride request (Period 1), Uber offers limited liability coverage, typically activating only if the driver’s personal insurance denies the claim.

Once a driver accepts a trip and is on the way to the passenger (Period 2), and during the trip itself (Period 3), Uber’s coverage expands significantly, including up to $1 million in liability protection. However, this policy is secondary during Period 1 and primary during Periods 2 and 3, making it essential for drivers to understand when Uber’s coverage applies and when their own policy must take over.

- During Period 1 (app on, no request accepted), Uber provides contingent liability coverage that only kicks in if the driver’s personal policy does not cover the incident.

- In Periods 2 and 3 (trip accepted and passenger in car), Uber’s $1 million liability policy becomes primary, offering broader protection for bodily injury and property damage.

- Collision and comprehensive coverage provided by Uber is contingent, meaning it applies only if the driver has these coverages on their personal policy and helps pay for damage to the driver’s vehicle after an accident.

Gaps in Coverage and How to Address Them

Despite Uber’s commercial insurance, significant gaps exist, especially during Period 1 when the driver is logged into the app but hasn’t accepted a ride. Many personal auto policies will not cover accidents that occur during this time because the vehicle is being used commercially. This creates a vulnerable window where a driver could be involved in an accident without adequate protection.

To bridge this gap, drivers should either obtain a rideshare-specific insurance policy or ensure their personal insurer offers a rideshare endorsement that covers this period. Additionally, some third-party insurers offer non-owner policies or commercial policies tailored to gig drivers. Drivers must also be aware of their state’s insurance regulations, as requirements and available products can vary by location.

- Unused personal insurance during the “app-on” period can result in denied claims, emphasizing the need for explicit rideshare coverage.

- Drivers should compare offerings from insurers like Progressive, State Farm, and Allstate, which offer rideshare endorsements in certain states.

- Regularly reviewing coverage limits and ensuring documents are updated with Uber helps maintain compliance and uninterrupted driving privileges.

Personal auto insurance policies are designed for private use, meaning driving for daily commutes, errands, or personal trips. When a driver starts using their vehicle for commercial purposes like Uber, the risk profile changes significantly.

Insurers assess risk based on how frequently and for what purpose a vehicle is driven, and ride-sharing increases both exposure to accidents and the likelihood of claims. Most standard auto policies explicitly exclude coverage for commercial activities, so failing to disclose ride-sharing can result in denied claims or policy cancellation. Understanding this distinction helps drivers realize why transparency with their insurer is critical.

- Personal auto policies typically exclude coverage for any form of hired transportation services.

- Increased mileage and driving during peak hours raise the statistical risk of accidents.

- Insurers rely on accurate usage information to assess premiums and coverage eligibility.

Legal and Financial Risks of Not Informing Your Insurer

Operating as an Uber driver without informing your insurance provider can lead to serious legal and financial consequences. If an accident occurs while you're logged into the Uber app or transporting passengers, your personal insurer may refuse to pay a claim upon discovering the commercial use of the vehicle.

This leaves the driver personally liable for damages, medical expenses, and legal fees. Additionally, misrepresenting the use of your vehicle could be considered insurance fraud, which carries civil and potentially criminal penalties. Awareness of these potential outcomes underscores the importance of proper disclosure.

- Claims may be denied if the insurer discovers unreported commercial use after an accident.

- Drivers could face out-of-pocket costs for vehicle repairs and third-party liabilities.

- Engaging in undisclosed ride-sharing may be classified as policy misrepresentation or fraud.

How to Properly Insure Your Vehicle for Ride-Sharing

To ensure adequate protection, Uber drivers should take proactive steps to update their insurance coverage. Many insurers offer ride-share endorsements or specific commercial policies that bridge the gap between personal and commercial use.

These endorsements typically activate coverage during the periods when the Uber app is on, including when waiting for a ride request or en route to pick up a passenger. Drivers should contact their current insurer to inquire about ride-share coverage options and compare policies from companies that specialize in gig economy insurance. Properly insuring your vehicle aligns with legal requirements and provides peace of mind.

- Contact your insurer to add a ride-share endorsement or switch to a commercial policy.

- Verify that coverage applies during all phases of ride-sharing, including app-on periods with no passenger.

- Compare quotes from multiple insurers to find comprehensive and affordable coverage tailored to gig driving.

What type of car insurance is required for Uber drivers?

Personal Auto Insurance and Its Limitations for Uber Drivers

- Most Uber drivers initially rely on their personal auto insurance, which typically covers accidents during personal use of the vehicle, such as commuting or running errands.

- However, standard personal policies often exclude coverage when the vehicle is used for ride-sharing activities, especially once the Uber app is turned on but before a passenger is picked up.

- Drivers may face claim denials or policy cancellations if they are involved in an accident during a ride-sharing period and only have personal insurance, making it essential to seek additional or specialized coverage.

Uber’s Provided Insurance Coverage by Trip Segment

- Uber supplies contingent insurance that activates in specific phases of a driver’s activity, divided into three main periods based on app status.

- Period 1 begins when the driver logs into the Uber app but has not accepted a ride request; during this time, Uber offers limited liability coverage, subject to the driver’s personal insurance.

- Periods 2 and 3—after accepting a trip and during passenger transport—include higher liability limits, uninsured/underinsured motorist protection, and contingent collision and comprehensive coverage, though deductibles may apply.

- To bridge gaps in coverage, especially during Period 1, drivers can purchase rideshare endorsement policies, which extend personal insurance to include periods when the app is active.

- Alternatively, full commercial auto insurance is available for drivers who use their vehicle exclusively for business, offering comprehensive protection but at a higher premium cost.

- Many insurance providers now offer specialized rideshare policies tailored to gig economy drivers, ensuring seamless coverage from the moment the app is turned on until the ride ends.

Frequently Asked Questions

Do Uber drivers need special car insurance?

Yes, Uber drivers need special insurance because personal auto policies don’t cover commercial activities like ridesharing. Uber provides commercial insurance during Periods 1, 2, and 3 of a trip, but it may not fully cover all damages or injuries. Drivers often purchase a rideshare-specific policy or endorsement to fill gaps, especially during Period 1 when they're logged in but haven't accepted a ride. This ensures full protection and compliance with both Uber’s requirements and state laws.

When does Uber's insurance coverage start?

Uber's insurance coverage starts in three periods. Period 1 begins when the driver logs into the app but hasn’t accepted a ride—limited liability coverage applies. Period 2 starts when a ride is accepted and continues until pickup; here, Uber provides increased liability and uninsured motorist coverage. Period 3 covers the time from passenger pickup to drop-off, offering the highest level of protection. While Uber's insurance applies during all periods, it's essential to understand coverage limits and possible gaps, especially in Period 1.

Can I use my personal car insurance for Uber driving?

No, standard personal car insurance won’t cover accidents that occur while driving for Uber. Most personal policies exclude commercial use, and filing a claim without disclosing rideshare activity could lead to denied claims or policy cancellation. While Uber offers its own insurance, it doesn’t replace personal coverage. Drivers should inform their insurer about ridesharing or get a rideshare endorsement, which modifies the personal policy to cover gaps, particularly during Period 1 when driving for Uber but not on an active trip.

Driving for Uber without proper rideshare insurance can lead to serious financial risks. If you’re in an accident during Period 1 and only have personal insurance, your claim could be denied due to commercial use exclusions. Without coverage, you may be responsible for vehicle repairs, medical bills, and legal fees. Uber’s insurance helps but has gaps, especially in Period 1. Not having appropriate coverage may also violate Uber’s requirements, potentially leading to deactivation from the platform.

Leave a Reply