Garagekeepers Insurance For Auto Repair Businesses

Garagekeepers insurance is a crucial protection for auto repair businesses that assume custody of customers’ vehicles. This specialized coverage safeguards shop owners against financial liability if a vehicle is damaged, stolen, or destroyed while in their care, custody, or control.

Unlike general liability insurance, garagekeepers insurance covers physical damage resulting from accidents, natural disasters, vandalism, or theft. For auto repair shops, this policy provides peace of mind and enhances customer trust. With rising vehicle values and potential repair costs, having the right coverage is essential to maintaining business continuity and protecting against unexpected claims.

Understanding Garagekeepers Insurance for Auto Repair Businesses

Garagekeepers insurance is a specialized type of coverage designed specifically for auto repair shops, mechanics, and other businesses that handle customers' vehicles as part of their service operations.

Auto Insurance Hurst

Auto Insurance HurstUnlike general liability insurance, which protects against injuries or property damage on your premises, garagekeepers insurance provides financial protection if a customer’s vehicle is damaged, stolen, or destroyed while in your care, custody, or control. This could include incidents such as fire, vandalism, flooding, or accidental damage during repairs or test drives.

Given the high value of vehicles and the potential legal and financial consequences of mishandling them, this insurance is essential for mitigating risk and maintaining customer trust. Most states require garages that hold customer vehicles overnight or perform repair work to carry some form of garagekeepers coverage, making it not only a smart business decision but often a legal necessity.

Types of Coverage in Garagekeepers Insurance

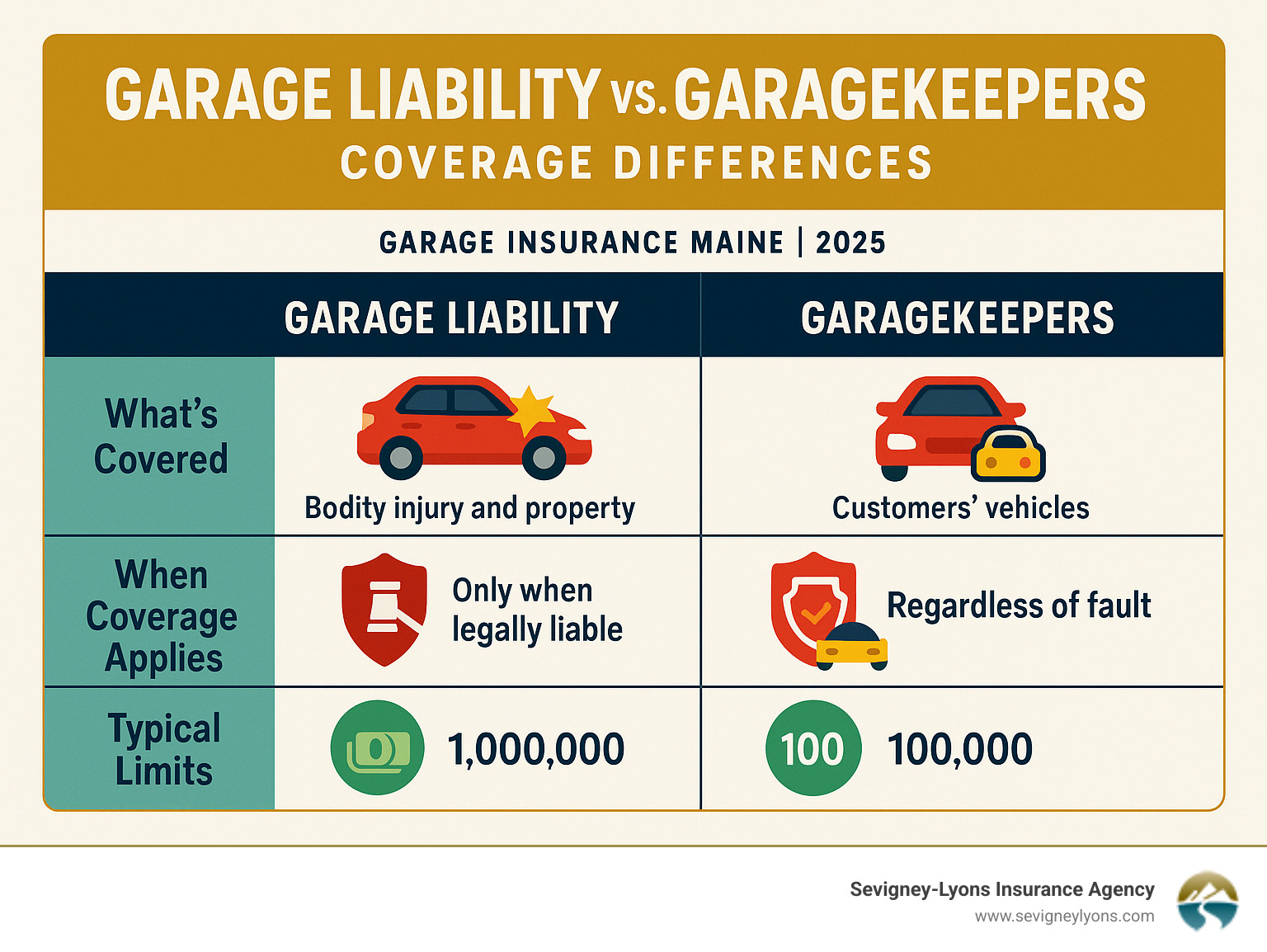

Garagekeepers insurance typically comes in three main forms: Broad Form, Continental (or Basic), and Limited coverage, each offering different levels of protection based on the garage’s needs and risk exposure.

The Broad Form provides the most comprehensive protection, covering nearly all causes of loss except those specifically excluded in the policy, such as wear and tear, mechanical breakdown, or vehicles used in racing. The Continental or Basic Form covers specific named perils like fire, lightning, explosion, theft, and vandalism, but excludes other risks unless explicitly added.

Auto Insurance In Miami

Auto Insurance In MiamiThe Limited Form offers minimal protection, usually excluding theft, making it less suitable for most repair shops. Choosing the right type depends on the scale of operations, types of services offered, and the value of vehicles typically held. Many reputable insurers recommend the Broad Form for full-service auto repair businesses due to its extensive coverage.

Who Needs Garagekeepers Liability Insurance?

Any business that regularly takes possession of customer-owned vehicles for service, repair, storage, or diagnostic work should carry garagekeepers insurance.

This includes independent auto repair shops, dealership service centers, body shops, tire and alignment centers, and even car wash facilities that may hold keys or move vehicles. Even if a shop does not perform major repairs, simply moving a vehicle for parking or detailing can expose the business to liability if damage occurs.

Without garagekeepers insurance, a single incident could result in significant out-of-pocket costs or legal action. Furthermore, many customers expect or require proof of such insurance before entrusting their vehicle to a repair facility, making it a critical component of a shop’s credibility and professional standards.

Auto Insurance In Mo

Auto Insurance In MoSeveral key factors influence the cost of garagekeepers insurance premiums, including the size and location of the facility, volume of vehicles serviced, claims history, and the security measures in place.

Facilities located in areas with high crime or severe weather risks may face higher premiums due to increased exposure to theft or natural disasters. Insurers also evaluate the value of the average vehicle stored or repaired—luxury or high-end vehicles generally result in higher premiums.

Implementing security features such as surveillance cameras, alarm systems, secure key storage, and employee background checks can help reduce risk and lower insurance costs. Additionally, a history of frequent claims can significantly drive up premiums, making risk management and employee training essential for maintaining affordable coverage.

| Coverage Feature | Broad Form | Continental (Basic) Form | Limited Form |

|---|---|---|---|

| Damage from Fire or Explosion | ✔ Covered | ✔ Covered | ✔ Covered |

| Theft or Vandalism | ✔ Covered | ✔ Covered | ✖ Not Covered |

| Accidental Damage (e.g., collision during test drive) | ✔ Covered | ✖ Not Covered | ✖ Not Covered |

| Natural Disasters (e.g., flood, hail) | ✔ Covered | ✖ Not Covered | ✖ Not Covered |

| Best For | Full-service repair shops | Small garages with low risk | Very low-risk operations (e.g., oil change only) |

Comprehensive Guide to Garagekeepers Insurance for Auto Repair Businesses

What does garage keepers insurance cover for auto repair businesses?

Auto Insurance In New York Ny

Auto Insurance In New York NyWhat Is Covered Under Garage Keepers Insurance for Stored Vehicles?

Garage keepers insurance provides essential protection for vehicles that are in the possession of an auto repair business. This includes any car, truck, or motorcycle that has been left with the shop for repairs, maintenance, storage, or detailing.

The coverage applies while the vehicle is physically on the business premises or, in some cases, during test drives or delivery to a customer. The policy typically covers damage resulting from perils such as fire, theft, vandalism, weather-related incidents, and collisions while the vehicle is being moved by shop personnel.

- Damage from fire or smoke while the vehicle is stored in the garage

- Theft of the entire vehicle or major components like wheels or audio systems

- Vandalism or malicious damage inflicted while the vehicle is in the shop’s care

How Does Garage Keepers Insurance Protect Against Accidents During Test Drives?

When mechanics need to test drive a customer’s vehicle to diagnose or verify repair work, accidents can happen.

Garage keepers insurance extends coverage to these situations, protecting the business from financial liability if the vehicle is damaged during a test drive conducted by an employee. This includes damage from collisions, single-vehicle rollovers, or hitting fixed objects. The insurance treats the repair shop as responsible for the vehicle at that time, and thus covers repair costs up to the policy limit.

Auto Insurance In Nh

Auto Insurance In Nh- Covers damage from collisions during authorized test drives by staff

- Includes accidents that occur off-site, such as on public roads near the garage

- Pays for repairs to the customer's vehicle, minus any applicable deductible

What Types of Damage Are Included in Physical Damage Coverage?

The core of garage keepers insurance is physical damage protection, which safeguards against various forms of tangible harm to vehicles in the shop’s custody.

This coverage is typically written as direct primary coverage, meaning the garage keeper’s policy responds first, even if the customer’s insurance might also apply. It covers a broad range of incidents that occur during the time the vehicle is under the shop’s control, offering financial protection that helps maintain customer trust and business reputation.

- Damage from falling objects, such as tools, equipment, or overhead storage

- Accidental scratches, dents, or paint damage caused during servicing

- Natural disaster damage, including floods, storms, or hail while the vehicle is parked at the facility

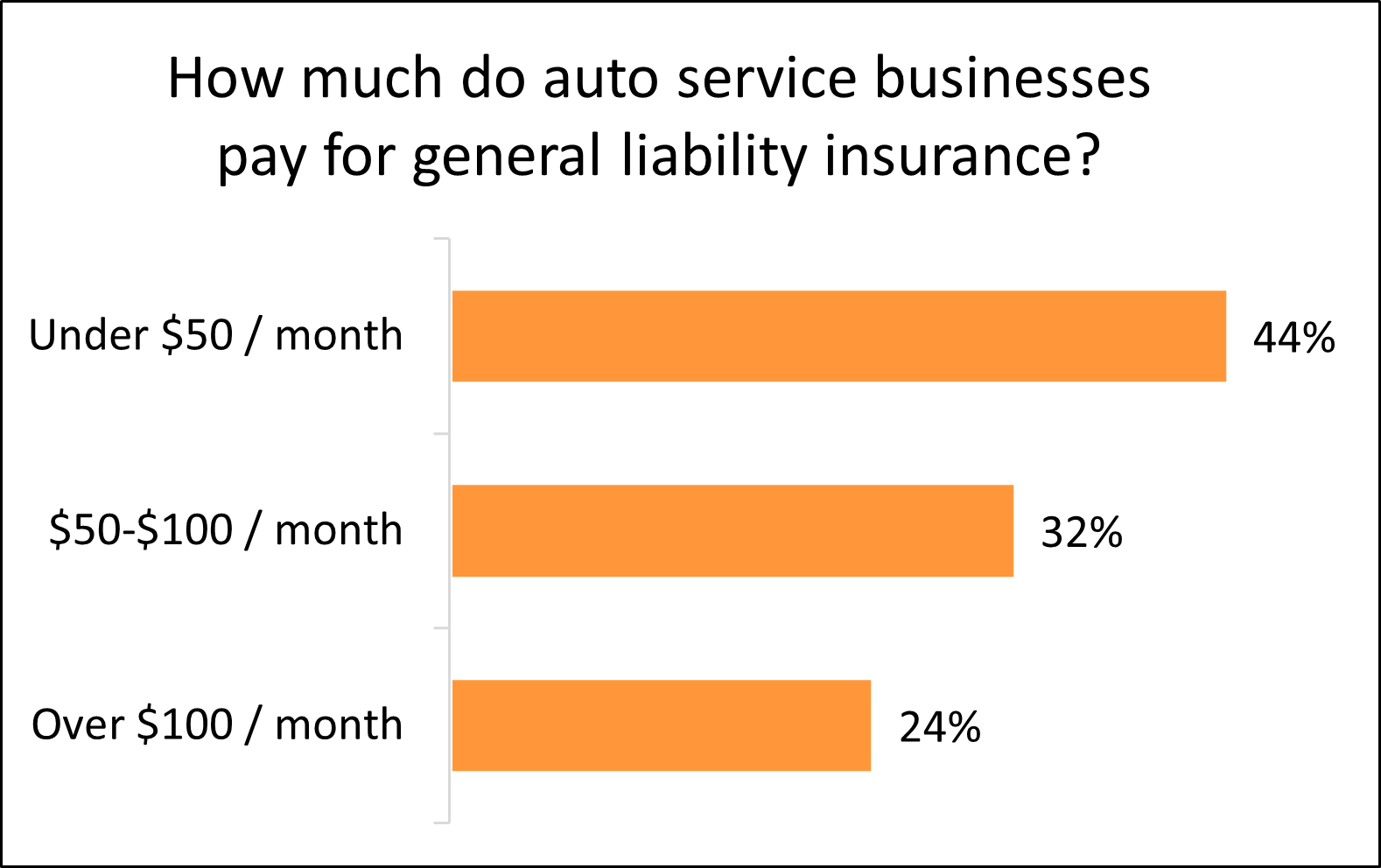

What Does a $1,000,000 Garagekeepers Liability Insurance Policy Cost for Auto Repair Shops?

Factors That Influence the Cost of a $1,000,000 Garagekeepers Liability Insurance Policy

- The size and location of the auto repair shop significantly impact the premium. Urban areas with higher crime rates or increased risk of theft may lead to higher insurance costs compared to rural locations. Insurers evaluate local statistics related to vehicle break-ins, vandalism, and claims history when setting rates.

- The type of services offered also affects pricing. Shops performing high-value repairs or handling luxury and exotic vehicles often face higher premiums because the cost of damages or loss can be more substantial. Additionally, businesses that store vehicles overnight are considered higher risk than those that do not.

- Claims history plays a critical role. A shop with a clean record and minimal past claims will generally receive lower rates, while a history of frequent or severe claims will result in increased premiums. Insurers use this data to assess the likelihood of future incidents and adjust pricing accordingly.

- Most auto repair shops can expect to pay between $500 and $2,500 annually for a $1,000,000 garagekeepers liability insurance policy. The exact amount depends on the shop's risk profile, including the volume of vehicles serviced, storage practices, and geographic region.

- Smaller operations that service fewer vehicles and do not store them overnight typically fall on the lower end of the price range. These businesses present less exposure to loss, which translates into more affordable premiums.

- Larger repair facilities, especially those in metropolitan areas or those working on high-end vehicles, often pay toward the upper end of the spectrum. The increased foot traffic, higher inventory value, and greater operational complexity justify the elevated cost.

Coverage Components Included in a Standard Garagekeepers Policy

- Physical damage to customers' vehicles while in the care, custody, or control of the repair shop is the core element of coverage. This includes damage caused by fire, flooding, theft, vandalism, or accidents that occur on the premises during repair or storage.

- Legal defense costs are covered if a customer sues the shop for alleged negligence or damage to their vehicle. Even if the claim is unfounded, the policy helps pay for attorney fees, court costs, and settlements up to the policy limit.

- Some policies may include optional endorsements or extensions, such as coverage for portable tools, key loss, or substitute transportation, though these are not standard and may increase the overall cost. It's important to review the policy details to understand what is included and what requires additional purchase.

What does commercial garage liability coverage include for auto repair businesses?

Commercial garage liability coverage is a specialized type of insurance designed to protect auto repair businesses from financial loss due to third-party claims of bodily injury, property damage, or personal injury that arise during garage operations.

This coverage is essential for businesses that service, store, or repair vehicles, as they face higher risks than standard commercial operations. It applies to accidents that occur on the premises or as a result of services provided, such as a customer slipping and falling in the waiting area or damage to a customer’s vehicle while in the shop for repairs.

Third-Party Bodily Injury Protection

- Covers medical expenses, legal fees, and compensation for pain and suffering if a customer, vendor, or passerby is injured on the business premises, such as from a slip, fall, or equipment accident.

- Applies to incidents that occur during operational hours as well as those related to repair activities, like a test drive that results in an accident involving another person.

- Includes defense costs even if the claim is groundless, provided it falls within the policy’s scope, helping the business manage litigation risks without significant out-of-pocket expenses.

Damage to Customers' Vehicles and Property

- Provides coverage for physical damage caused to a customer’s vehicle while it is in the care, custody, or control of the auto repair shop, such as accidental scratches, dents, or mechanical damage during repairs.

- Extends to personal belongings left inside a customer’s vehicle if those items are damaged or stolen while the car is at the facility.

- Does not typically cover damage arising from poor workmanship alone unless it directly results in physical harm to the vehicle, but some policies may include endorsements to broaden this protection.

- Covers liabilities that emerge from the repair process itself, such as a brake repair defect that later causes an accident involving the repaired vehicle and injures others on the road.

- Includes protection for off-premises incidents, like a mechanic causing a collision while road-testing a vehicle after service.

- May also address claims related to improper vehicle storage, such as fire or water damage to vehicles parked at the garage during adverse weather, depending on the policy terms and endorsements.

Do auto repair shops need garagekeepers insurance coverage?

What Is Garagekeepers Insurance and Why Is It Essential for Auto Repair Shops?

- Garagekeepers insurance is a specialized type of coverage designed to protect vehicles that are in the care, custody, or control of an auto repair shop. This policy covers damage to customer vehicles while they are being serviced, stored, or test-driven.

- Unlike general liability insurance, which covers third-party bodily injury or property damage, garagekeepers insurance specifically addresses property damage claims related to client vehicles. This makes it a crucial component of a comprehensive risk management strategy for repair facilities.

- Without garagekeepers insurance, a repair shop could be held financially responsible for theft, vandalism, fire, or accidental damage to a customer’s vehicle. The cost of repairs or replacement could be substantial and potentially devastating to a small business.

What Types of Damage Are Covered Under Garagekeepers Insurance?

- Garagekeepers insurance typically covers physical damage to customer vehicles caused by perils such as fire, theft, vandalism, flooding, and accidental damage during repairs or movement within the facility.

- Some policies also extend coverage to damage caused by employees while test-driving a vehicle or moving it within the shop premises. This protection includes issues arising from human error, like dropping a tool on the vehicle or scratching the paint during service.

- The extent of coverage may vary depending on the policy terms, with options for basic, broad, or superb forms of coverage. The broad form is most common and covers all risks except those explicitly excluded, such as wear and tear or mechanical breakdowns.

Are There Legal or Contractual Reasons Auto Repair Shops Need This Coverage?

- In many states, garagekeepers insurance is not legally mandated, but it is often required by commercial landlords, lenders, or major dealership partners as a condition for doing business.

- Customers may also expect proof of garagekeepers coverage before entrusting their vehicle to a repair shop, especially if it's a high-value or luxury car. Having this insurance can enhance a shop's credibility and attract more clients.

- Additionally, without garagekeepers insurance, a shop could face lawsuits or significant out-of-pocket expenses if a customer claims negligence after their vehicle is damaged. The policy helps mitigate legal risks and ensures financial protection against such claims.

Frequently Asked Questions

What is Garagekeepers Insurance for Auto Repair Businesses?

Garagekeepers Insurance protects auto repair shops, garages, and service centers when customers’ vehicles are damaged while in their care, custody, or control. It covers repair, replacement, or towing costs if a vehicle is damaged due to fire, theft, vandalism, or accidents on the premises. This coverage is essential because standard commercial property or liability policies typically don’t cover customer vehicles.

Why Do Auto Repair Shops Need Garagekeepers Insurance?

Auto repair businesses handle customers’ vehicles daily, making them legally responsible for any damage incurred during service. Without Garagekeepers Insurance, shops could face significant out-of-pocket expenses for repairs or legal claims. This insurance safeguards the business financially and builds customer trust by showing responsibility. It’s often required by law or by lease agreements, ensuring the business operates compliantly and securely.

What Types of Damage Are Covered by Garagekeepers Insurance?

Garagekeepers Insurance typically covers physical damage caused by fire, theft, vandalism, falling objects, and collisions with equipment on the premises. It may also include damage from storms or water leaks. However, coverage depends on the policy type—broad form covers all risks unless excluded, while limited form covers only specific perils. Always review your policy to understand exactly what incidents are included.

Does Garagekeepers Insurance Cover Employee Theft or negligence?

Yes, Garagekeepers Insurance generally covers damage caused by employee negligence, such as accidental scratches or improper repairs. However, employee theft of vehicle parts or components may not be covered under standard policies and might require additional crime insurance. It’s important to clarify coverage details with your insurer and implement strong internal controls to reduce risk and support claims in case of incidents involving staff.

Leave a Reply