Indexed Universal Life Insurance Lawyers Columbia

Indexed Universal Life (IUL) insurance offers policyholders the potential for cash value growth tied to market indexes, along with a death benefit.

However, the complexity of IUL policies can lead to misunderstandings, mismanagement, and even financial loss. In Columbia, South Carolina, individuals facing disputes or legal challenges related to IUL policies often turn to experienced legal professionals for assistance.

Lawyers specializing in indexed universal life insurance help clients navigate issues such as misrepresentation, inadequate disclosures, or improper sales practices. These attorneys advocate for policyholders' rights, ensuring transparency and accountability from insurers and financial advisors.

Empower Retirement Permanent Life Insurance Offerings

Empower Retirement Permanent Life Insurance OfferingsUnderstanding Indexed Universal Life Insurance Legal Support in Columbia

Indexed Universal Life (IUL) insurance policies offer a unique combination of lifelong coverage and the potential for cash value growth tied to a market index, such as the S&P 500.

However, these policies can be complex and often lead to disputes involving misrepresentation, inadequate disclosures, or unsuitable sales practices. In Columbia, individuals facing challenges with their IUL policies may benefit from consulting experienced Indexed Universal Life Insurance lawyers who specialize in policyholder rights and insurance bad faith claims.

These legal professionals help clients navigate disputes with insurers, seek compensation for damages, and ensure that insurance companies adhere to state regulations and ethical standards. Whether you were misled during the sales process or are experiencing unexpected premium hikes or policy lapses, legal representation in Columbia can be critical in protecting your financial interests.

Common Legal Issues with Indexed Universal Life Insurance Policies

Policyholders in Columbia often encounter legal complications related to Indexed Universal Life Insurance, including misrepresentation, fraudulent sales tactics, and failure to disclose risks.

Evaluate The Financial Services Company Progressive On Life Insurance

Evaluate The Financial Services Company Progressive On Life InsuranceInsurance agents may overstate the benefits of IUL policies while downplaying the risks of premium increases, caps on returns, or policy lapses due to poor index performance. When policyholders are sold IUL products without a clear understanding of long-term financial obligations, it may constitute unsuitable recommendations under South Carolina insurance laws.

Lawyers with expertise in IUL cases can analyze the original sales documentation, recorded meetings, and agent credentials to build a case for financial recovery or policy reinstatement. These legal issues are particularly prevalent when retirees or conservative investors are steered toward complex, high-cost policies that do not align with their risk tolerance or financial goals.

How Columbia Lawyers Protect IUL Policyholders’ Rights

Indexed Universal Life Insurance lawyers in Columbia focus on holding insurance companies and agents accountable for unethical practices.

They provide services such as policy reviews, claim dispute representation, and bad faith litigation when insurers fail to act in good faith. These attorneys often work on a contingency fee basis, meaning they only collect a fee if they win the case, making legal recourse more accessible.

Evaluate The Insurance Company Guardian Life On Accident Insurance

Evaluate The Insurance Company Guardian Life On Accident InsuranceBy leveraging state insurance regulations and financial industry standards, Columbia-based legal professionals advocate for clients who have suffered financial harm due to misleading IUL sales. Their goal is to secure compensatory damages, rescission of the policy, or restitution for out-of-pocket losses, including excessive premiums or lost investment opportunities.

Choosing the Right Legal Representation in Columbia

Selecting the best Indexed Universal Life Insurance lawyer in Columbia requires evaluating their experience with insurance litigation, track record in settling or winning IUL disputes, and familiarity with South Carolina insurance statutes.

Look for attorneys or law firms that specialize specifically in life insurance claims and have a history of confronting major insurance carriers. Client testimonials, peer reviews, and case results can help determine a lawyer’s effectiveness.

Additionally, initial consultations are typically free and provide an opportunity to discuss your situation, understand your legal options, and determine whether the attorney is the right fit for your case. The expertise and responsiveness of your legal representative can significantly influence the outcome of your IUL insurance dispute.

Evaluate The Insurance Company Nationwide On Life Insurance

Evaluate The Insurance Company Nationwide On Life Insurance| Legal Issue | Description | Legal Remedy |

|---|---|---|

| Misrepresentation | Agents falsely claim IUL policies have guaranteed high returns or low premiums. | Rescission of policy or monetary damages |

| Unsuitable Sale | Policies sold to individuals with low risk tolerance or fixed incomes. | Recovery of premiums and lost interest |

| Bad Faith Denial | Insurers refuse to honor claims or communication without valid reason. | Bad faith lawsuit with potential for punitive damages |

Guidance on Indexed Universal Life Insurance Lawyers in Columbia

What are the potential drawbacks of indexed universal life insurance policies?

:max_bytes(150000):strip_icc()/Pros-and-cons-indexed-universal-life-insurance_final-1b83c0fd52154eb69edd47f99ab8927a.png)

Complexity and Lack of Transparency

- Indexed universal life (IUL) insurance policies are often difficult for consumers to fully understand due to their complex structure, which combines life insurance with a cash value component tied to stock market indices like the S&P 500. This complexity can make it challenging for policyholders to grasp how their cash value grows and what fees or caps are applied.

- Insurance companies use intricate formulas involving participation rates, caps, and spreads to determine how much of the index’s return is credited to the policy, and these terms are not always clearly explained. As a result, policyholders may have unrealistic expectations about potential returns.

- The lack of standardized terminology and variations in policy design across insurers further contribute to confusion, making it difficult to compare policies objectively and increasing the risk of misunderstandings about long-term performance.

High Fees and Costs

- IUL policies typically come with multiple layers of fees, including cost of insurance charges, administrative fees, and expenses related to the index crediting mechanism. These costs can significantly reduce the amount of money that actually goes into the cash value component of the policy.

- Commissions for agents selling IUL policies are often high, and these costs are ultimately borne by the policyholder, which may incentivize the sale of these policies even when they are not the best fit for the customer’s financial goals.

- Some policies also include surrender charges if the policy is canceled or modified within the first several years, which can make it expensive to exit the policy if it underperforms or if the policyholder's financial situation changes.

Vulnerability to Poor Performance Under Certain Market Conditions

- Although IUL policies offer downside protection by guaranteeing no loss of cash value in negative market years, they also limit upside potential through caps on index gains. If the linked index performs strongly, the policyholder may receive only a fraction of the actual return due to these caps.

- Periods of low index volatility or sideways market movement can result in minimal or zero interest credits to the cash value, especially if the policy’s participation rate or cap is restrictive. This can lead to cash value growth that fails to keep pace with premium payments or inflation.

- Because the long-term performance of IUL policies heavily depends on assumptions about future index performance and interest rates, actual outcomes may fall short of projections, particularly if premiums are not sustained at the projected levels or if loan amounts reduce the policy’s value over time.

What Should You Consider About Indexed Universal Life Insurance in Columbia?

Understanding the Basics of Indexed Universal Life Insurance in Columbia

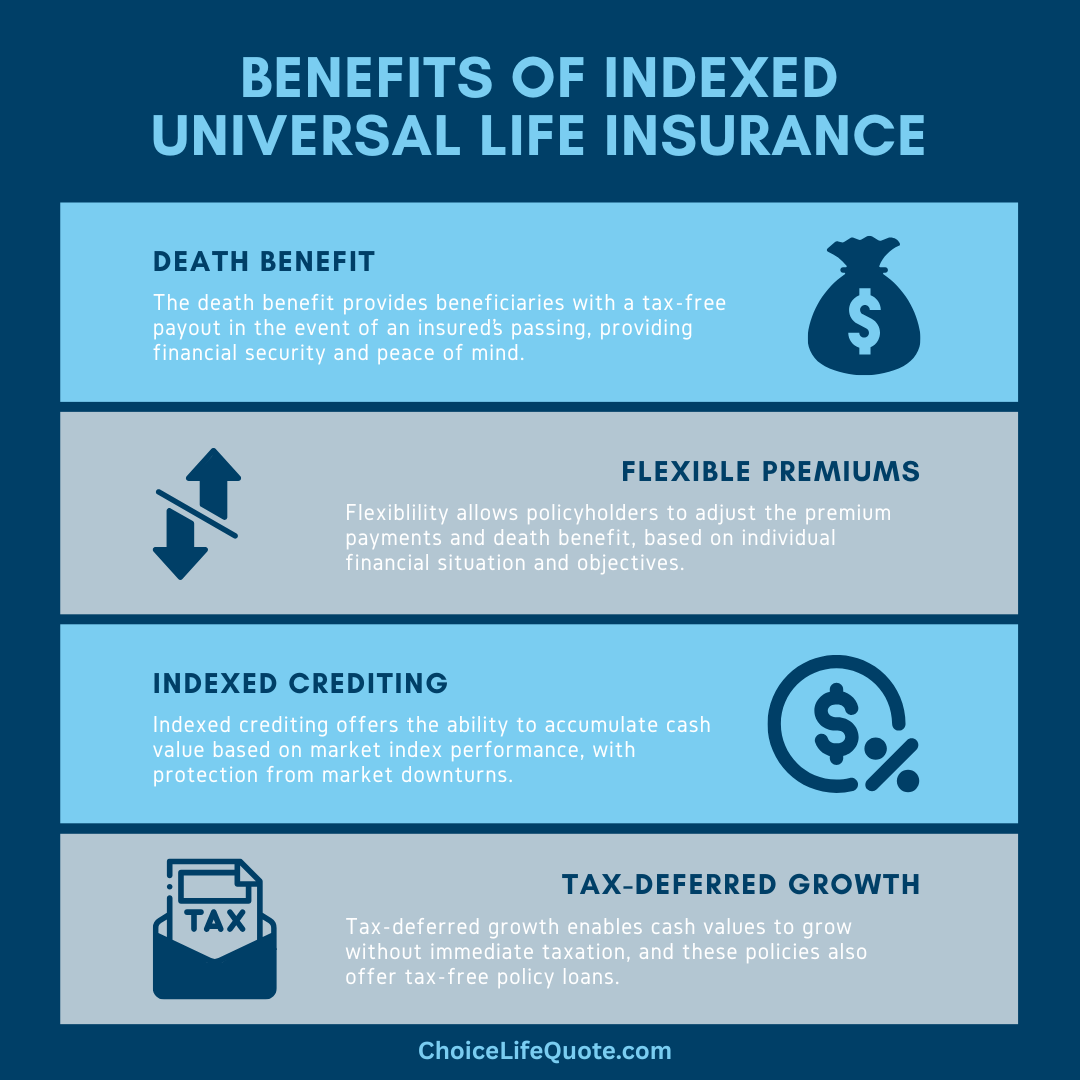

- Indexed Universal Life (IUL) insurance is a type of permanent life insurance that offers both a death benefit and a cash value component, which grows based on the performance of a market index, such as the S&P 500. In Columbia, as in other regions, it’s essential to understand how this mechanism separates IUL from traditional whole life policies, which offer fixed interest rates on cash value growth.

- Unlike variable universal life policies, IUL does not directly invest in the stock market. Instead, it uses a crediting formula tied to the chosen index, allowing policyholders to benefit from market gains while protecting against losses during downturns. This feature is often referred to as a “floor” and is typically set at zero, meaning the cash value will not decrease if the index performs negatively.

- Local regulatory standards in Columbia may impose specific requirements on how these policies are sold and administered. Prospective policyholders should verify that the IUL product complies with regional insurance regulations and that the issuing company is licensed to operate in the area.

Evaluating Fees, Caps, and Participation Rates

- One of the most critical aspects to analyze in an IUL policy is the fee structure. These policies often come with a variety of charges, including administrative fees, cost of insurance charges, and rider fees. In Columbia, insurance providers may display these fees differently, so it's vital to request a detailed illustration that breaks down each component.

- Another key consideration is the cap rate—the maximum percentage of index growth that can be credited to the policy. For example, if the cap is set at 8% and the index gains 11%, the policy’s cash value will only grow by 8%. Additionally, some insurers apply participation rates, which determine the percentage of the index’s return passed on to the policyholder.

- These limits—caps, participation rates, and spreads—can significantly impact long-term cash value accumulation. Comparing multiple IUL proposals from different insurers in Columbia can help identify which policies offer more favorable terms and transparency in crediting methods.

Assessing Long-Term Financial Goals and Flexibility

- Indexed Universal Life insurance can be a strategic tool for individuals in Columbia seeking lifelong coverage combined with potential cash accumulation. However, its suitability depends on personal financial objectives, such as estate planning, supplemental retirement income, or legacy building. A clear understanding of these goals is necessary before committing to a long-term policy.

- IUL policies offer flexible premium payments and adjustable death benefits, providing a level of customization not found in term life insurance. This flexibility allows policyholders to modify their coverage as financial circumstances change, such as increasing coverage after a major life event like marriage or the birth of a child.

- It’s also important to consider funding consistency. IUL policies require sufficient premium payments to remain in force, especially in the early years when expenses are higher. Failure to maintain funding levels may result in lapses or the need to draw from cash value, which could reduce the death benefit or trigger tax consequences.

Frequently Asked Questions

What is Indexed Universal Life Insurance, and how does it work?

Indexed Universal Life (IUL) insurance is a type of permanent life insurance that offers a death benefit and a cash value component linked to a market index, like the S&P 500. The cash value grows based on the index’s performance, with a guaranteed minimum interest rate and protection from market losses. Policyholders can adjust premiums and death benefits, making IUL flexible for long-term financial planning.

Why might I need a lawyer for Indexed Universal Life Insurance issues?

You may need a lawyer if you suspect misrepresentation, improper sales practices, or disputes with your insurance provider regarding your IUL policy. Lawyers in Columbia specializing in IUL insurance can help review policy terms, uncover contractual violations, and assist with claims or litigation. Their expertise ensures your rights are protected and can be crucial in resolving complex insurance disputes effectively and efficiently.

How can an Indexed Universal Life Insurance lawyer in Columbia help me?

An IUL lawyer in Columbia can provide legal guidance on policy interpretation, help resolve claim denials, and represent you in negotiations or litigation. They assist in identifying agent misconduct, such as misleading commission structures or unrealistic performance projections. With their knowledge of insurance laws, they protect your financial interests and seek compensation when policies don’t perform as promised due to improper sales practices.

What should I look for when hiring an IUL insurance lawyer in Columbia?

When hiring an IUL insurance lawyer in Columbia, look for experience handling insurance disputes, knowledge of South Carolina insurance laws, and a history of successful client outcomes. Choose someone with strong communication skills who offers transparent fee structures. Reading client reviews and scheduling consultations can help assess their professionalism and expertise in dealing with complex Indexed Universal Life Insurance cases.

Leave a Reply