Rossmoor Irrevocable Life Insurance Trust Lawyer

An Irrevocable Life Insurance Trust (ILIT) can be a powerful estate planning tool, particularly for high-net-worth individuals seeking to minimize estate taxes and ensure a smooth transfer of wealth. In Rossmoor, navigating the complexities of ILITs requires experienced legal guidance. A knowledgeable Rossmoor irrevocable life insurance trust lawyer provides essential support in structuring, funding, and administering these trusts in compliance with state and federal laws. From selecting trustees to coordinating with insurance providers, proper legal oversight ensures the trust fulfills its intended purpose. This article explores the critical role of a skilled attorney in establishing an ILIT tailored to your unique financial goals and family needs.

Why You Need a Rossmoor Irrevocable Life Insurance Trust Lawyer

An Irrevocable Life Insurance Trust (ILIT) can be a powerful estate planning tool, especially for high-net-worth individuals in communities like Rossmoor who seek to minimize estate taxes, protect life insurance proceeds, and ensure efficient wealth transfer to beneficiaries. However, establishing and managing an ILIT requires precise legal guidance to comply with complex IRS regulations and avoid unintended tax consequences. A knowledgeable Rossmoor Irrevocable Life Insurance Trust Lawyer provides essential support in drafting the trust, transferring life insurance policies, appointing trustees, and structuring the trust to meet your specific goals. Without proper legal oversight, the trust may fail to achieve its intended tax and asset protection benefits, leaving your estate vulnerable to probate and taxation. Engaging a qualified attorney ensures that your ILIT is set up correctly from the start and maintained in accordance with fiduciary and legal standards.

Understanding the Role of an Irrevocable Life Insurance Trust

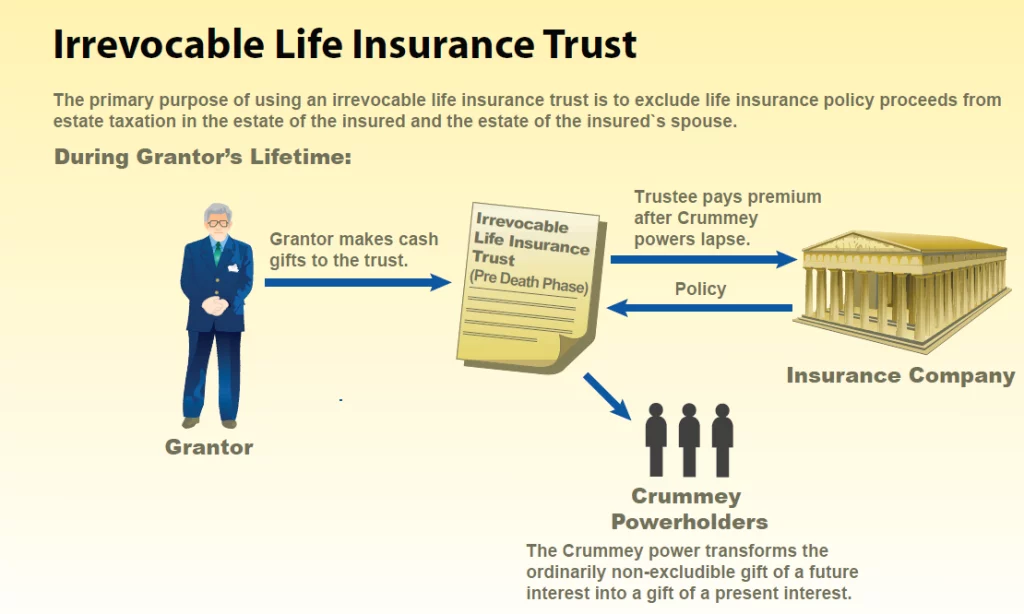

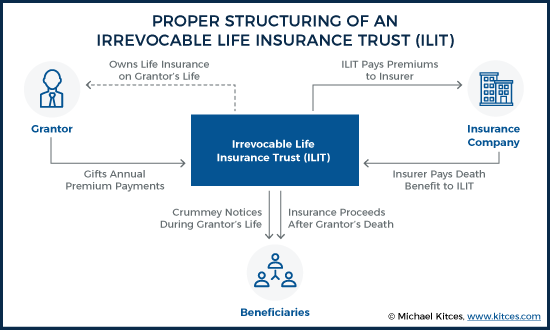

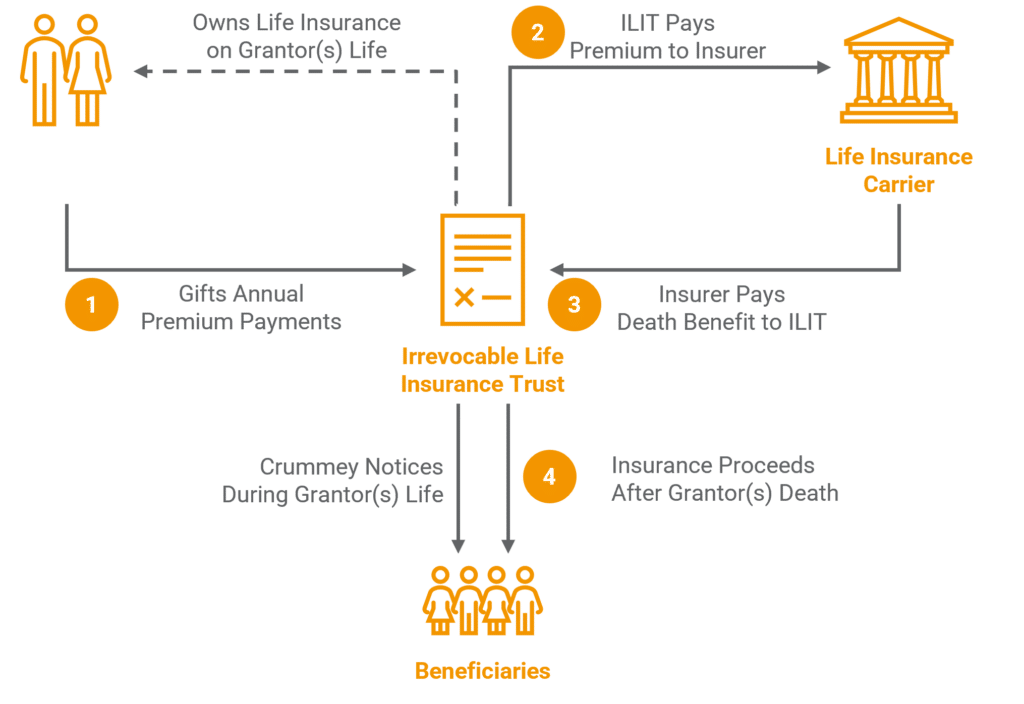

An Irrevocable Life Insurance Trust (ILIT) is designed to remove life insurance proceeds from your taxable estate, potentially saving thousands or even millions in federal and state estate taxes. Once established, the ILIT becomes the owner and beneficiary of your life insurance policy, meaning the death benefit does not count as part of your estate for tax purposes. This structure is particularly beneficial for individuals in affluent areas like Rossmoor, where estate values may exceed federal or state exemptions. Because the trust is irrevocable, you generally cannot change its terms once it is created, which underscores the importance of careful planning. A skilled Rossmoor attorney ensures that the trust is structured with appropriate provisions for trustee powers, beneficiary distributions, and compliance with IRS requirements, including the Crummey powers, which allow beneficiaries to withdraw contributions temporarily to qualify for annual gift tax exclusions.

Digital Life Insurance Platforms

Digital Life Insurance PlatformsKey Benefits of Hiring a Local Rossmoor ILIT Attorney

Working with a Rossmoor-based Irrevocable Life Insurance Trust Lawyer offers distinct advantages, including familiarity with California estate laws, local tax considerations, and regional financial planning trends. These attorneys understand the unique estate planning needs of Rossmoor residents, many of whom are retirees or have significant home equity and investment portfolios. A local lawyer can coordinate with your financial advisor, insurance agent, and accountant to ensure seamless integration of the ILIT into your broader financial strategy. Additionally, in-person consultations allow for more personalized service and quicker resolution of concerns. Most importantly, a Rossmoor attorney will help you avoid procedural missteps—such as improper funding or failure to follow gift tax rules—that could invalidate the trust’s tax benefits. Their localized expertise makes them an invaluable partner in securing your family’s financial future.

Common Mistakes to Avoid When Setting Up an ILIT

Establishing an Irrevocable Life Insurance Trust involves numerous technical requirements, and even minor errors can jeopardize its effectiveness. One common mistake is failing to properly retitle the life insurance policy in the name of the trust, which can result in the proceeds being pulled back into your estate. Another critical error is not adhering to Crummey notice requirements, which mandate that beneficiaries receive formal notification of their right to withdraw gifts into the trust; skipping this step risks losing annual gift tax exclusions. Some individuals also neglect ongoing compliance, such as filing Form 706 (estate tax return) when necessary or maintaining accurate trust records. A qualified Rossmoor ILIT lawyer helps you avoid these pitfalls by ensuring strict adherence to legal timelines, documentation, and administrative procedures, preserving the trust’s integrity and maximizing its financial advantages.

| Aspect | Key Consideration | Role of a Rossmoor ILIT Lawyer |

|---|---|---|

| Trust Funding | Life insurance policy must be transferred or purchased directly by the trust | Ensures correct titling and avoids inclusion in the estate |

| Crummey Powers | Beneficiaries must receive withdrawal rights for gifts to qualify for exclusions | Drafts proper notices and timelines for compliance |

| Trustee Selection | Trustee manages distributions and trust administration | Recommends suitable individuals or institutions and outlines duties |

| State & Federal Laws | ILITs must comply with IRS and California regulations | Provides up-to-date legal guidance and avoids tax penalties |

| Ongoing Maintenance | Trust requires annual contributions and recordkeeping | Advises on compliance and helps coordinate with financial institutions |

Comprehensive Guide to Choosing a Rossmoor Irrevocable Life Insurance Trust Lawyer

What Is the 5-Year Rule for Irrevocable Life Insurance Trusts in Rossmoor?

Understanding the 5-Year Rule for Irrevocable Life Insurance Trusts

- The 5-year rule in the context of Irrevocable Life Insurance Trusts (ILITs) refers to a provision in the U.S. federal estate tax code that affects when life insurance proceeds are considered part of a deceased individual’s taxable estate. Specifically, if the grantor (the person who creates the trust) transfers a life insurance policy into an ILIT and dies within five years of that transfer, the death benefit may still be included in their estate for estate tax purposes.

- This rule is derived from Internal Revenue Code Section 2035, which governs gifts made within three years of death but extends to five years in the case of life insurance policy transfers. The purpose is to prevent individuals from avoiding estate taxes by transferring valuable assets, like life insurance, shortly before death.

- In Rossmoor, a community in California known for its large population of retirees, understanding this rule is particularly important due to the high value of real estate and personal assets. Residents often utilize ILITs as part of estate planning to protect wealth, making the 5-year timing rule a critical consideration when restructuring ownership of life insurance policies.

How the 5-Year Rule Impacts Estate Tax Planning in Rossmoor

- For residents of Rossmoor seeking to minimize estate tax liability, transferring a life insurance policy to an ILIT well in advance of the five-year window is essential. If the grantor survives for at least five years after the transfer, the policy’s death benefit is excluded from the taxable estate, potentially saving beneficiaries significant sums in estate taxes, especially given California's high property values and net worth of many retirees.

- Estate planners in Rossmoor often recommend establishing the ILIT and purchasing the life insurance policy directly through the trust, rather than transferring an existing policy. This approach avoids the 5-year rule altogether, as there is no prior ownership by the grantor that triggers the lookback period.

- However, if the grantor retains any incidents of ownership over the policy—such as the right to change beneficiaries or cancel the policy—during the five years, the IRS may still include the proceeds in the estate. Thus, strict compliance with trust terms is necessary to ensure the rule functions as intended.

Strategic Timing and Compliance for ILITs in Rossmoor Estates

- Proper timing is crucial when funding an ILIT with a life insurance policy in Rossmoor. Residents are advised to set up the trust and complete the transfer of ownership at least five years before any anticipated health decline or potential passing. This buffer ensures full compliance with the 5-year rule and maximizes tax benefits.

- Professional guidance from estate attorneys familiar with both federal tax law and local financial trends in Rossmoor is recommended. These experts help structure the ILIT to include proper Crummey powers, allowing beneficiaries to withdraw annual contributions for a limited period, which satisfies the IRS requirement for a completed gift and supports the trust’s validity.

- Additionally, ongoing maintenance of the ILIT is necessary, including consistent payment of premiums by the trust using funds from annual exclusion gifts. Failure to adhere to these protocols can jeopardize the trust’s integrity and may result in the life insurance payout being re-included in the estate, regardless of the 5-year holding period.

What Are the Costs to Modify an Irrevocable Life Insurance Trust in Rossmoor?

Empower Retirement Permanent Life Insurance Offerings

Empower Retirement Permanent Life Insurance OfferingsUnderstanding Legal Fees for Modifying an ILIT in Rossmoor

- Modifying an irrevocable life insurance trust (ILIT) typically involves hiring an experienced estate planning attorney, which is one of the primary costs. In Rossmoor, California, legal fees can vary based on the complexity of the modifications and the attorney’s hourly rate, which generally ranges from $250 to $450 per hour.

- Simple amendments, such as changing a successor trustee, may require only a few hours of legal work, costing approximately $750 to $1,500. However, more complex modifications—like removing or adding beneficiaries, restructuring trust terms, or decanting the trust into a new one—can take 10 or more hours, pushing legal fees to $3,000 or higher.

- Attorneys may also charge flat fees for certain ILIT modifications. Clients should request a fee agreement upfront to understand whether they will be billed hourly or through a fixed-fee structure to avoid unexpected expenses.

Trust Decanting and Associated Administrative Costs

- In some cases, rather than amend the original ILIT, trustees may choose to decant the trust—transferring assets from the existing trust into a new one with updated terms. This process allows for greater flexibility, especially if the original trust prohibits direct amendments. In Rossmoor, decanting typically requires legal documentation, notice to beneficiaries, and adherence to California Probate Code Section 19500 et seq., all contributing to higher costs.

- Administrative costs include preparing the new trust document, filing notices, and possibly obtaining court approval if beneficiaries do not consent. These steps can add $1,000 to $2,500 in additional legal and administrative expenses beyond standard modification fees.

- There may also be costs related to updating the life insurance policy itself—for example, reassigning ownership or changing beneficiaries on the policy to align with the new trust structure, which may involve coordination with the insurance carrier and additional documentation.

Cost Implications of Beneficiary or Trustee Changes

- Changing beneficiaries or trustees in an ILIT, while seemingly straightforward, still requires formal legal procedures to maintain the trust's integrity and tax advantages. In Rossmoor, even minor changes often involve drafting and executing a trust amendment, which can cost between $500 and $1,200 depending on the attorney.

- If the change involves closely held business interests or substantial assets within the ILIT, additional reviews of tax implications may be necessary. This can trigger consultations with tax professionals, adding $300 to $800 in advisory fees to the overall cost.

- It is also important to account for record-keeping and filing costs. Copies of amended documents may need to be distributed to financial institutions, insurance providers, and successor trustees, and maintaining proper records could result in small but recurring administrative fees over time.

Can an irrevocable life insurance trust beneficiary be changed in Rossmoor, and what role does a trust lawyer play?

Yes, an irrevocable life insurance trust (ILIT) beneficiary generally cannot be changed once the trust is established, including in Rossmoor, California. This is because the defining feature of an irrevocable trust is its permanence—the grantor relinquishes control over the trust assets, including the life insurance policy, to prevent those assets from being included in their taxable estate. However, there may be limited exceptions depending on the trust’s specific terms, state laws, or through legal mechanisms such as trust decanting or court approval. Given the complexity and strict regulations surrounding irrevocable trusts, it is vital to consult with an experienced trust lawyer who understands California estate laws and can navigate potential options for modification if circumstances change.

Understanding the Irrevocability of Life Insurance Trusts in Rossmoor

- An irrevocable life insurance trust is structured to remove the life insurance policy from the grantor’s estate for tax purposes, which requires that the grantor give up control, including the power to change beneficiaries freely. Once the trust is funded and activated, the terms become fixed unless specific provisions were included at the time of creation.

- In Rossmoor, as in the rest of California, state trust laws govern how these trusts operate. While the general rule is that beneficiaries of an ILIT cannot be changed, some trusts may include limited powers of appointment or provisions allowing a trustee or trust protector to modify beneficiaries under narrowly defined circumstances.

- Changes to beneficiaries are only possible if the original trust document anticipates such flexibility. Without such language, attempting to modify a beneficiary could violate the trust's terms and have unintended tax or legal consequences, making it essential to review the trust document carefully with a qualified attorney.

Exceptions and Legal Mechanisms for Modifying Beneficiaries

- One potential method for changing beneficiaries is trust decanting, a legal process recognized in California that allows a trustee to transfer assets from an existing irrevocable trust into a new trust with modified terms. Decanting is subject to specific statutory requirements and is typically allowed only when it serves the trust’s purposes and does not violate the original intent.

- In certain cases, a court may permit a modification through reformation if there is a mistake in the trust document or if unanticipated circumstances render the original terms impractical. This requires a formal petition and judicial approval, and the process can be time-consuming and costly.

- California’s Uniform Trust Code allows for nonjudicial modifications if all beneficiaries and the trustee agree, provided the grantor is deceased and the changes align with the overall trust purpose. This route still demands careful legal oversight to ensure compliance with state law and tax regulations.

The Role of a Trust Lawyer in Managing ILIT Beneficiary Changes

- A trust lawyer provides critical guidance in interpreting the language of the ILIT, assessing whether any flexibility exists for beneficiary changes, and determining the most appropriate legal strategy based on California law and federal tax rules. Their expertise helps avoid actions that could trigger estate tax inclusion or invalidate the trust.

- They assist in preparing and filing the necessary legal documents, whether for trust decanting, court reformation, or nonjudicial modification, ensuring that all procedural requirements are met and that the interests of all parties are protected throughout the process.

- Additionally, a trust lawyer can advise on the tax implications, coordinate with financial institutions holding the policy, and represent the trustee or beneficiaries in legal proceedings if court intervention is required, making their involvement essential for navigating the complexities of irrevocable trust modifications in Rossmoor.

Frequently Asked Questions

What is an Irrevocable Life Insurance Trust (ILIT), and how can a Rossmoor ILIT lawyer help?

An Irrevocable Life Insurance Trust (ILIT) holds life insurance policies outside your estate to reduce estate taxes and control benefit distribution. A Rossmoor ILIT lawyer helps structure and manage the trust properly, ensuring compliance with tax laws. They guide you through funding the trust, changing beneficiaries, and navigating complex legal requirements to protect your family’s financial future and maximize insurance benefits.

Why should I hire a Rossmoor life insurance trust attorney instead of using online forms?

Hiring a Rossmoor life insurance trust attorney ensures your ILIT is correctly established and legally valid. Online forms often lack customization and may not comply with California or federal regulations. An experienced attorney provides personalized advice, prevents costly errors, and ensures your wishes are enforceable. They also assist with ongoing trust administration and address changes in tax laws, offering long-term peace of mind and asset protection.

Evaluate The Financial Services Company Progressive On Life Insurance

Evaluate The Financial Services Company Progressive On Life InsuranceCan an Irrevocable Life Insurance Trust be modified once it's created?

Generally, an Irrevocable Life Insurance Trust cannot be easily modified after creation, which is why precise drafting is crucial. However, under certain circumstances—such as changes in tax law or family dynamics—modifications may be possible through legal remedies like decanting or court approval. A Rossmoor ILIT lawyer can assess options and guide trustees through permissible changes while preserving the trust’s tax advantages and legal integrity.

How does an ILIT help reduce estate taxes for Rossmoor residents?

An ILIT removes the life insurance death benefit from your taxable estate, potentially saving thousands in estate taxes. For Rossmoor residents with sizable assets, this trust ensures proceeds are not counted toward the estate’s value. By keeping the policy outside the estate, heirs receive more of the benefit tax-free. A qualified Rossmoor ILIT attorney ensures proper setup and ongoing compliance to maximize these tax savings.

Leave a Reply