Life Insurance After Dui

A DUI conviction can have far-reaching consequences beyond legal penalties and increased insurance premiums. One often overlooked area is its impact on life insurance. Insurers view DUIs as a significant red flag, indicating potential risk that can affect your ability to secure coverage or result in higher premiums.

Even after serving penalties, the record remains for years, influencing how underwriters assess your application. However, obtaining life insurance after a DUI is not impossible. With the right approach, understanding of the process, and transparency about your circumstances, you can still find a policy that meets your needs.

How a DUI Affects Your Life Insurance Options

Being convicted of a DUI (Driving Under the Influence) can significantly impact various aspects of your life, including your ability to secure affordable life insurance. Insurance providers view a DUI as a red flag indicating higher risk, especially when it comes to your judgment, health, and potential for future health complications.

Business Insurance Cost Estimate

Business Insurance Cost EstimateAs a result, many insurers will either deny coverage altogether or charge substantially higher premiums to offset the perceived risk. The extent of the impact depends on several factors, including the time elapsed since the offense, whether it was a first-time or repeat violation, your overall health, and the insurance company’s underwriting guidelines.

However, while obtaining life insurance after a DUI may be more challenging, it is not impossible—many people successfully secure coverage by understanding the process, being transparent during applications, and choosing the right provider.

Why Insurers Care About DUI Convictions

Life insurance companies assess your application based on risk, and a DUI conviction introduces concerns about your lifestyle, decision-making, and potential health risks such as liver disease or substance abuse.

Since insurers aim to anticipate mortality risk, behaviors indicating poor judgment or addiction raise red flags. A DUI suggests possible reckless behavior or alcohol dependency, which statistically correlates with a higher likelihood of premature death. As a result, underwriters typically classify applicants with DUIs as high-risk, requiring additional scrutiny during the application process.

Business Insurance For Dentists

Business Insurance For DentistsThis may involve requesting medical records, conducting a paramedical exam, or even requesting information from the Motor Vehicle Record (MVR) or the Medical Information Bureau (MIB). Full disclosure is crucial—failing to report a DUI can result in denied claims or policy cancellation.

Types of Life Insurance Available After a DUI

Despite a DUI on record, several life insurance options remain accessible, though eligibility and pricing vary widely. Term life insurance remains the most affordable and popular choice, but individuals with a DUI may face higher premiums or extended waiting periods.

Some insurers may offer guaranteed issue life insurance, which doesn’t require a medical exam or health questions, though these policies come with limited coverage and higher costs over time. Simplified issue policies are another alternative, bypassing the medical exam but asking health-related questions, including any DUIs in the past.

Whole life insurance is also available but often comes with steeper premiums for high-risk applicants. Working with an experienced agent who understands post-DUI underwriting guidelines can help identify insurers more lenient toward past offenses.

Business Insurance For Distributors

Business Insurance For DistributorsHow Long Does a DUI Affect Life Insurance Rates?

The impact of a DUI on your life insurance application typically lasts between 3 to 10 years, depending on the insurer and circumstances. Most companies will consider a DUI as part of your record for 5 to 7 years, aligning with most state traffic violation reporting periods.

However, some insurers may still find DUI information through MIB reports or comprehensive background checks beyond this window. The older the conviction, the less impact it generally has—especially if you’ve maintained a clean driving record and shown responsible behavior since.

Taking proactive steps such as completing a DUI program, maintaining good health, and demonstrating financial responsibility can help soften the negative effects over time. After a certain period, you may even qualify to reapply for better rates.

| Insurance Type | Impact of DUI | Typical Waiting Period | Best For |

|---|---|---|---|

| Term Life | High premiums or denial | 3–7 years | Those seeking affordable, temporary coverage |

| Whole Life | Moderate to high cost increase | 5+ years | Long-term financial planning |

| Guaranteed Issue | No medical questions, but high cost | Immediate availability | Individuals denied elsewhere |

| Simplified Issue | DUI question asked; possible surcharge | 1–3 years | Quick coverage with moderate health concerns |

Life Insurance Options After a DUI: What You Need to Know

How Does a DUI Impact Your Life Insurance Options?

Business Insurance For Independent Consultants

Business Insurance For Independent ConsultantsHow Does a DUI Affect Life Insurance Approval?

- Being convicted of a DUI (Driving Under the Influence) can significantly influence whether an individual is approved for life insurance. Insurers view DUIs as indicators of risky behavior, which raises concerns about the applicant’s long-term health and mortality risk.

- During the underwriting process, life insurance companies typically review an applicant’s driving record, medical history, and criminal background. A DUI often triggers a more thorough evaluation, during which the insurer may request additional documentation or impose stricter conditions.

- While a single DUI might not automatically disqualify someone from coverage, multiple offenses—or a recent conviction—can lead to outright denial, especially for preferred or non-medical underwriting policies that require cleaner records.

- Even if approved, individuals with a DUI on their record are typically placed in a higher risk category, which directly translates into increased premiums. Insurers use actuarial data that links substance-related driving offenses with a greater likelihood of premature death, thus justifying higher costs.

- The extent of the rate increase depends on several factors, including the number of DUIs, how recently the offense occurred, and whether it was accompanied by other infractions or accidents. For example, a DUI within the last three years will usually have a more severe impact than one that occurred a decade ago.

- Applicants may be assigned to a substandard risk class, such as Table D or Table E, where premiums can be 100% to 300% higher than standard rates. Over the course of a 20- or 30-year policy, this can result in tens of thousands of dollars in additional costs.

Strategies to Improve Life Insurance Options Post-DUI

- One effective way to mitigate the impact of a DUI is waiting before applying for life insurance. Most insurers only consider incidents within the past 5 to 10 years, so allowing time to pass demonstrates improved behavior and increases the chances of better rates.

- Completing court-mandated programs, such as alcohol education or treatment courses, can improve an applicant’s standing during underwriting. Providing proof of rehabilitation shows responsibility and may lead insurers to view the DUI as an isolated incident rather than a pattern.

- Shopping around is crucial, as different insurers have varying underwriting guidelines. Some companies are more lenient toward applicants with a history of DUIs and may offer more favorable terms, especially if other health and lifestyle factors are strong.

What disqualifies someone from getting life insurance after a DUI?

Severity and Recency of the DUI Offense

- The severity of the DUI incident plays a critical role in determining insurance eligibility. For example, a single DUI with a blood alcohol concentration (BAC) slightly over the legal limit may be viewed less harshly than a case involving extremely high BAC, accidents, injuries, or driving with a suspended license. Insurers assess the perceived risk based on how dangerous the episode was considered.

- The timing of the DUI is equally important. Most life insurance companies consider a DUI within the past five to seven years as a significant red flag. The closer the conviction is to the application date, the higher the risk in the eyes of underwriters. Individuals who had a DUI more than a decade ago, especially with no further infractions, may face fewer challenges.

- Some insurers maintain internal guidelines that automatically decline applicants with recent DUIs, particularly if multiple incidents occurred. Others may require a waiting period, such as two to three years post-conviction, before reconsidering an application. This reflects how insurers balance risk tolerance with customer eligibility.

Number of DUI Convictions on Record

- Having a single DUI may lead to higher premiums or special risk classifications, but it doesn’t always result in denial. Many insurers will still approve coverage, though often through a substandard or high-risk rating category which increases costs.

- Multiple DUIs significantly reduce the chances of approval. Two or more convictions drastically increase the perceived likelihood of premature death due to high-risk behavior, leading many insurers to decline applications outright.

- Life insurance underwriters look for patterns of recurring behavior. More than one DUI signals a lack of behavioral correction, which suggests ongoing exposure to risk. Such applicants may only qualify for specialized policies like guaranteed issue life insurance, which typically offers lower coverage amounts and higher premiums without a medical exam.

Additional Health and Lifestyle Risk Factors

- A DUI application is rarely evaluated in isolation. If the applicant has co-occurring health issues such as liver disease, cardiovascular conditions, or mental health disorders related to substance abuse, insurers may view the overall risk profile as too high for standard or even substandard coverage.

- Insurers often review driving records, medical history, and prescription drug history during underwriting. A DUI combined with traffic violations, substance abuse treatment, or prescriptions for alcohol dependency medications like naltrexone can compound eligibility concerns.

- Lifestyle choices such as tobacco use, excessive alcohol consumption, or participation in hazardous activities can interact with a DUI history to disqualify an applicant. Insurers use a holistic approach, and even if the DUI alone might not be disqualifying, its combination with other risk factors often results in denial or restrictive policy terms.

Can You Obtain a Life Insurance License with a DUI on Your Record?

Understanding the Impact of a DUI on Licensing Eligibility

- A DUI (Driving Under the Influence) conviction does not automatically disqualify an individual from obtaining a life insurance license, as licensing is primarily overseen at the state level and regulations vary. Most state insurance departments focus on an applicant’s overall character, honesty, and trustworthiness when reviewing licensing applications.

- While a DUI is generally considered a non-violent offense and not directly related to insurance fraud or financial misconduct, it may still raise concerns about an individual’s judgment and reliability. State regulators may scrutinize the timing, frequency, and circumstances surrounding the DUI to assess its relevance to professional conduct.

- Applicants are typically required to disclose any criminal convictions, including DUIs, on their licensing forms. Failing to report such information can result in denial of the license or future disciplinary action, even if the DUI itself might not have been a disqualifying factor.

State-by-State Licensing Requirements and Discretion

- Each U.S. state has its own rules regarding professional licensing for insurance agents, and some states are more lenient than others when evaluating criminal records. For example, states like Texas and Florida allow individuals with a DUI to obtain a license, provided they meet other requirements and disclose the offense truthfully.

- The decision often rests with the state insurance commissioner or licensing board, who may require additional documentation such as court records, personal statements, or proof of rehabilitation (e.g., completion of alcohol education programs).

- In certain cases, a recent DUI may be viewed more critically than one from several years ago. Many states consider the recency and pattern of offenses, meaning a single, isolated incident from the distant past is less likely to interfere with licensure than multiple or recent convictions.

Steps to Improve Chances of Approval with a DUI

- Be fully transparent when completing the insurance licensing application. Disclosing a DUI upfront demonstrates honesty and accountability, which licensing boards view favorably compared to discovering an omission during a background check.

- Gather supporting documentation that shows responsibility and rehabilitation, such as certificates of completion for DUI courses, letters of recommendation, or proof of stable employment. This evidence can help counterbalance concerns raised by the conviction.

- Consult with the state’s insurance department or a legal professional familiar with insurance licensing to understand specific requirements and determine if a waiver or additional review process is necessary. Proactively addressing potential issues improves the likelihood of a favorable outcome.

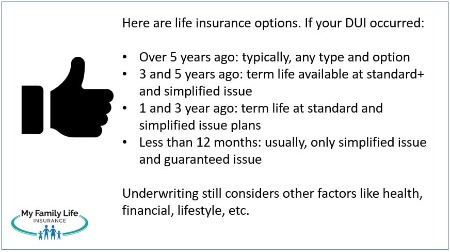

How Does the 3-Year Rule Affect Life Insurance Eligibility After a DUI?

Understanding the 3-Year Rule in Life Insurance After a DUI

- The 3-year rule refers to the general industry standard where life insurance companies consider the time elapsed since a DUI (Driving Under the Influence) conviction when evaluating an applicant's risk profile. Most insurers view the three-year mark as a significant period, suggesting that if no further incidents have occurred, the applicant may be seen as lower risk.

- During this period, insurers assess not only the conviction date but also the applicant’s behavior afterward, such as adherence to legal requirements, completion of rehabilitation programs, or continued clean driving records. Evidence of responsibility post-DUI strengthens the application.

- It's important to note that while the 3-year benchmark is common, it's not universal. Some insurers may require four or even five years without incidents, especially for preferred or non-smoker rate classes, depending on the severity of the DUI and the overall health profile of the applicant.

How Insurance Companies Evaluate DUI Convictions Within the First 3 Years

- In the immediate aftermath of a DUI, within the first 12 to 36 months, most life insurance providers categorize applicants as high-risk. As a result, they may either decline coverage or offer policies with significantly higher premiums.

- Underwriters typically request medical records, motor vehicle reports, and prescription histories to assess whether the DUI was an isolated incident or part of a broader pattern of risky behavior. Multiple offenses or elevated blood alcohol levels can extend the high-risk classification beyond three years.

- Some insurers may still approve coverage during this window, but applicants often face substandard underwriting classes, such as Table D through Table H, which reflect increased mortality risk and result in elevated premiums compared to standard rates.

Improving Eligibility and Rates After the 3-Year Period

- After the three-year period from the date of the DUI conviction, many applicants become eligible for better rate classes, provided they have maintained a clean driving record and demonstrated responsible behavior. This can include avoiding traffic violations and showing financial or personal stability.

- Transparency is key— insurers value applicants who disclose the DUI upfront rather than omitting it. Concealing a conviction can lead to policy denial or future cancellation, even if the offense occurred outside the three-year window.

- Shopping around is highly recommended, as underwriting guidelines vary across insurance carriers. Some companies specialize in high-risk cases and may offer more favorable terms post-DUI, especially after the three-year mark, compared to more conservative insurers.

Frequently Asked Questions

Can you get life insurance after a DUI?

Yes, you can still obtain life insurance after a DUI, though it may be more challenging and expensive. Insurers consider DUIs a significant risk factor, so they may increase your premiums or require a waiting period before offering coverage. Some companies specialize in high-risk applicants, making it possible to find a policy. Full disclosure of the incident is essential to avoid claim denial later.

How long does a DUI affect life insurance rates?

A DUI typically affects life insurance rates for 3 to 5 years, depending on the insurer. Most companies will view you as a higher risk during this period, resulting in higher premiums. After that, you may qualify for better rates, especially if you’ve maintained a clean driving record. Some insurers may still consider the DUI in underwriting if it's on your record during policy renewal.

Do I have to disclose a DUI on a life insurance application?

Yes, you must disclose a DUI on your life insurance application. Failing to report it can lead to policy denial or claim rejection later. Insurers often access driving records or medical reports and may discover undisclosed DUIs. Full transparency helps ensure your policy remains valid and benefits are paid to your beneficiaries without issues, even with a past conviction.

Can a life insurance company deny coverage for a DUI?

Yes, a life insurance company can deny coverage based on a DUI, especially if it’s recent or part of a pattern of risky behavior. Each insurer has different underwriting guidelines, and some may consider you too high-risk. However, denial by one company doesn’t mean all will refuse you. Shopping around increases your chances of finding a willing provider.

Leave a Reply