Life Insurance Application Declined

Being denied life insurance can be both surprising and discouraging, especially when seeking financial protection for loved ones.

A declined application does not necessarily mean coverage is out of reach, but it does signal that the insurer identified risks that exceeded their underwriting guidelines. Common reasons for denial include pre-existing health conditions, high-risk lifestyles, or inaccurate application information. Understanding the specific cause is crucial for next steps.

Some applicants may qualify with a different provider or policy type, while others might need to improve their health before reapplying. This article explores why applications get declined and how to move forward effectively.

Business Insurance Cost Estimate

Business Insurance Cost EstimateWhat to Do If Your Life Insurance Application Is Declined

Being denied life insurance can be a stressful and unexpected setback, especially if you're counting on coverage for financial security or estate planning.

While a decline doesn't mean you'll never qualify for life insurance, it's important to understand the reasons behind the decision and explore your options moving forward. Insurers evaluate applications based on a variety of factors, including medical history, lifestyle choices, and financial background.

Knowing why your application was declined allows you to address underlying issues, consider alternative products, or reapply with a different provider. The good news is that there are still pathways to obtain coverage—even after a denial.

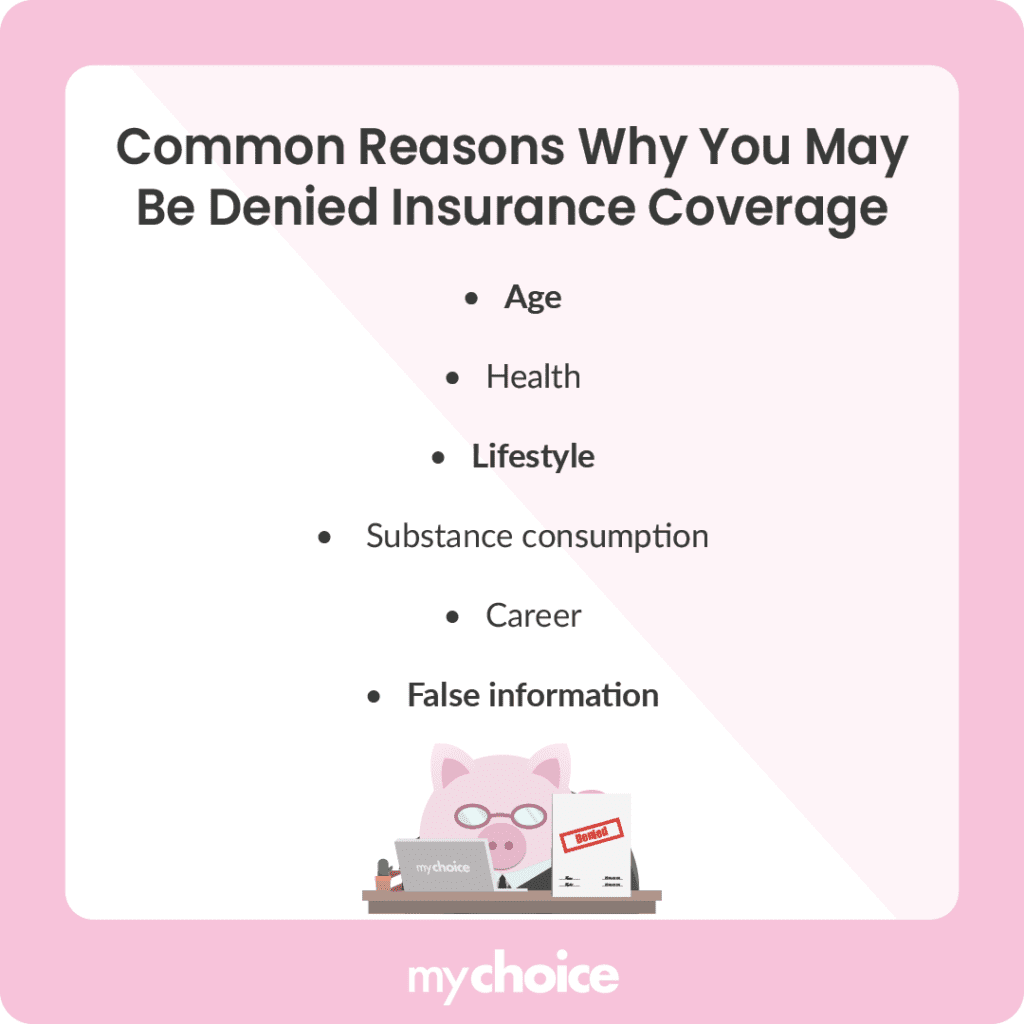

Common Reasons for Life Insurance Application Denial

Insurance companies assess risk carefully when reviewing applications, and several factors can lead to a denial. Pre-existing medical conditions such as cancer, heart disease, or diabetes are among the most frequent causes, especially if they are uncontrolled or recently diagnosed.

Business Insurance For Dentists

Business Insurance For DentistsOther medical concerns, like poor results from a paramedical exam or undisclosed health issues, can also result in rejection. Lifestyle factors play a significant role too—smoking, excessive alcohol consumption, participation in high-risk hobbies (e.g., skydiving), or a history of drug use may raise red flags.

In some cases, financial instability or a poor credit history can influence underwriting decisions, particularly for larger policy amounts. Additionally, providing incomplete or inaccurate information on the application can lead to an automatic decline.

Steps to Take After a Denial

After learning your application has been declined, the first step is to request a detailed explanation from the insurer or your agent. Insurers are required to provide a reason for denial under regulations like the Fair Credit Reporting Act (FCRA). Once you understand the cause, consider reviewing your medical records for inaccuracies and, if necessary, work with your doctor to clarify or improve your health profile.

If the denial was based on a specific health issue, you might wait several months or years, address the condition, and reapply later. It’s also wise to shop around with different insurers, as underwriting guidelines vary significantly between companies. Some insurers specialize in high-risk or guaranteed issue policies, which may offer alternatives despite prior denials.

Business Insurance For Distributors

Business Insurance For DistributorsAlternative Life Insurance Options After a Decline

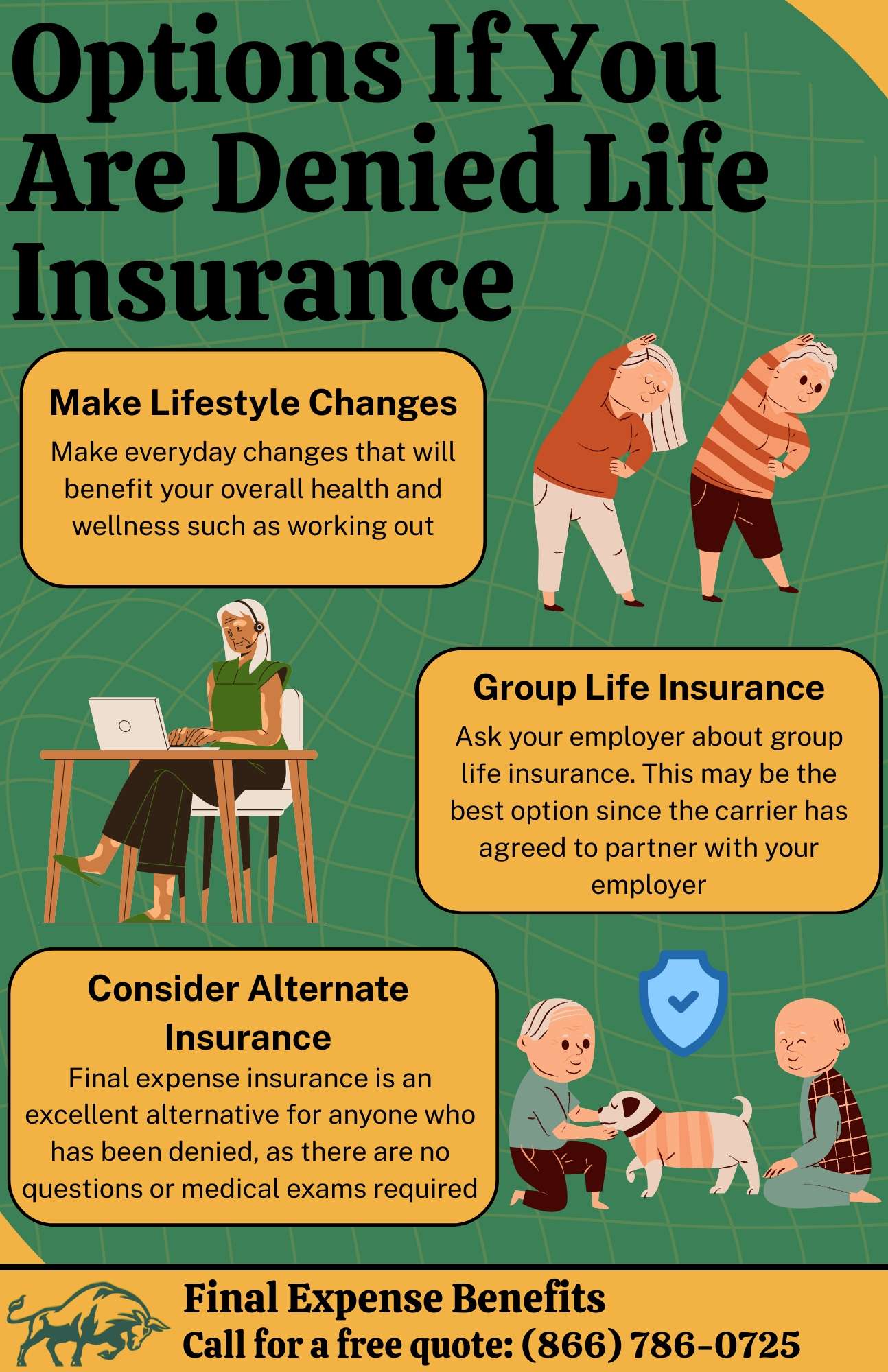

Even if you’ve been declined for traditional term or whole life insurance, several alternative options may still be available. Guaranteed issue life insurance is one such option; these policies typically don’t require a medical exam and cannot deny coverage based on health, although they often come with higher premiums and lower death benefits. Another possibility is group life insurance through an employer, which may not require individual underwriting. Accidental death and dismemberment (AD&D) policies are another consideration, though they offer limited coverage. Some individuals also turn to final expense insurance, which is designed to cover funeral and burial costs and is easier to qualify for, even with serious health issues.

| Insurance Type | Medical Exam Required? | Approval Likelihood After Denial | Typical Coverage Limit |

|---|---|---|---|

| Term Life Insurance | Yes | Low to Moderate | $50,000 – $2M+ |

| Whole Life Insurance | Yes | Moderate | $10,000 – $500,000 |

| Guaranteed Issue Life Insurance | No | Very High | $5,000 – $25,000 |

| Group Life Insurance | No (usually) | High (if employer-sponsored) | $10,000 – $100,000 |

| Final Expense Insurance | No | High | $5,000 – $50,000 |

What to Do If Your Life Insurance Application Is Declined

What are common reasons for a life insurance application to be declined?

Certain medical conditions significantly increase the risk profile of an applicant, leading insurers to decline life insurance applications. Insurers evaluate an individual's current and past health to determine life expectancy and the probability of a claim. Chronic or severe illnesses may indicate a higher likelihood of early death, making the applicant too high-risk to insure.

- Pre-existing conditions such as advanced heart disease, cancer, kidney failure, or severe diabetes can result in denial because they directly impact longevity and require costly treatment.

- Recent hospitalizations or major surgeries raise red flags for insurers, as recovery complications or recurring health issues may affect survival rates.

- Poor results on medical exams, including abnormal blood pressure, high cholesterol levels, or signs of liver disease, can lead to a rejection even if the applicant feels healthy.

Lifestyle and Behavioral Risk Factors

Insurance companies assess how a person's daily habits and choices may influence their mortality risk. Engaging in dangerous or unhealthy behaviors can lead to higher premiums or outright denial of coverage, as they suggest a shorter life expectancy.

Business Insurance For Independent Consultants

Business Insurance For Independent Consultants- Tobacco use, especially smoking or vaping, is a major contributor to policy denial. Insurers often charge higher rates for smokers, and heavy usage combined with related health issues can result in rejection.

- Excessive alcohol consumption or a history of substance abuse significantly increases the risk of life-threatening conditions, leading insurers to decline applications.

- Participation in high-risk activities such as skydiving, scuba diving, or racing may lead to denial due to the heightened chance of accidental death.

Incomplete or Inaccurate Application Information

Providing false or incomplete information on a life insurance application can result in immediate denial. Insurance contracts are based on full disclosure, and any misrepresentation—intentional or not—can invalidate the application process.

- Omitting a past medical diagnosis or treatment history can lead to rejection when discovered during underwriting or medical record reviews.

- Incorrect details about height, weight, tobacco use, or occupation can skew risk assessment, prompting insurers to decline the application after verification.

- Discrepancies between application data and third-party sources such as prescription drug databases (e.g., MIB reports) may trigger denial due to concerns about trustworthiness.

What are the odds of being denied life insurance during the application process?

Factors That Influence Life Insurance Application Approval

Several key factors can significantly affect the likelihood of being denied life insurance during the application process. Insurance companies assess applicant risk based on various personal and medical criteria to determine insurability.

These include age, overall health, pre-existing medical conditions, family medical history, lifestyle habits, and occupation. For example, individuals with serious health conditions such as cancer, heart disease, or uncontrolled diabetes are more likely to face denial or require further underwriting.

Similarly, those who participate in high-risk hobbies like skydiving or who have a history of substance abuse may be considered higher risk. Each insurer has its own underwriting guidelines, which can lead to variability in outcomes across different providers.

- Pre-existing health conditions like heart disease, diabetes, or cancer significantly increase the chance of denial due to elevated risk.

- Lifestyle factors such as tobacco use, excessive alcohol consumption, or engaging in extreme sports can lead to application rejection.

- Occupational hazards, including jobs in construction, aviation, or military service, may result in denial or the need for specialized policies.

Common Reasons for Denial During Underwriting

Life insurance applications are closely evaluated during the underwriting process, where insurers analyze medical records, prescription histories, and sometimes results from paramedical exams.

A denial can occur when the risk to the insurer is deemed too high based on this information. Frequently cited reasons include a history of serious medical issues, such as stroke or chronic obstructive pulmonary disease (COPD), a poor driving record involving DUIs, or a criminal history.

Additionally, incomplete applications or misrepresentation of facts can result in immediate denial. Some applicants may also be denied due to recent bankruptcy or lack of stable income, as insurers may view financial instability as a red flag.

- Medical red flags such as untreated hypertension or liver disease can lead to automatic or conditional denial.

- Legal and behavioral issues, including DUI convictions or drug-related offenses, are common grounds for rejection.

- Inaccurate or omitted information on the application may result in denial, even if the oversight was unintentional.

How Different Types of Policies Affect Approval Odds

The type of life insurance policy applied for can influence the probability of approval. Traditional underwritten term or whole life policies require detailed health assessments and are more likely to result in denial for high-risk applicants.

In contrast, no-medical-exam policies, such as guaranteed issue or simplified issue life insurance, have higher acceptance rates but come with significant limitations, including lower coverage amounts and higher premiums.

Guaranteed issue policies, often marketed to seniors, accept nearly all applicants regardless of health but typically include a graded death benefit during the first two to three years. Therefore, while the odds of being denied a fully underwritten policy might be higher for certain individuals, alternative products exist to accommodate those who may not qualify.

- Traditional underwritten policies have stricter criteria, increasing denial odds for applicants with health complications.

- No-exam policies improve access but often limit coverage and include waiting periods for full benefits.

- Guaranteed issue plans accept most applicants but are more costly and offer reduced death benefits initially.

What factors can lead to a life insurance application denial?

Life insurance applications are often denied due to health-related issues that indicate a higher risk of premature death.

Insurance underwriters evaluate your current health status, medical history, and any pre-existing conditions to determine your eligibility and premium rate. Individuals with serious or chronic illnesses such as cancer, heart disease, diabetes, or severe respiratory conditions may be seen as high-risk applicants.

Additionally, untreated mental health conditions like severe depression or a history of suicide attempts can significantly impact approval. Poor results from required medical exams, including high blood pressure, elevated cholesterol, or abnormal liver function, can also lead to denial.

- Pre-existing medical conditions such as cancer, diabetes, or cardiovascular disease increase risk assessment and may result in denial.

- Poor performance on medical tests, including blood work or EKGs, can signal underlying health issues that insurers are unwilling to cover.

- Obesity, depending on BMI and related complications, may disqualify applicants due to associated health risks like hypertension and stroke.

Lifestyle and Behavioral Risks

Applicants’ lifestyle choices play a critical role in the underwriting process. Engaging in risky behaviors or maintaining habits deemed dangerous by insurers can lead to application denial. Smoking, excessive alcohol consumption, and use of recreational drugs are major red flags.

Insurers also consider participation in hazardous activities such as skydiving, scuba diving, or motor racing, as these increase the probability of accidental death. A history of driving under the influence or multiple traffic violations can signal reckless behavior, which insurers may interpret as reduced life expectancy.

Overall, patterns of behavior that suggest a disregard for personal safety may negatively influence underwriting decisions.

- Smoking and tobacco use, including vaping, typically result in higher premiums or denial, especially if combined with other health concerns.

- Heavy alcohol use or documented alcoholism can lead to denial due to the long-term health effects and increased mortality risk.

- Involvement in extreme sports or dangerous hobbies may result in denial or require special high-risk policies not offered by standard insurers.

Application and Background Issues

Denials can also stem from problems unrelated to health or lifestyle, including inaccuracies or omissions on the application itself. Providing false or incomplete information about medical history, income, or past insurance applications is a common reason for rejection.

Insurers often cross-reference your application with databases like the Medical Information Bureau (MIB) to verify details. A criminal record, particularly involving fraud, violence, or drug offenses, may lead to denial. Additionally, applicants with a history of multiple life insurance applications or previous denials may face more scrutiny, as insurers may perceive this as an attempt to conceal risky information.

- Incomplete or falsified application details, even unintentional ones, can lead to immediate denial and affect future insurability.

- Adverse financial history, such as bankruptcy or lack of verifiable income, may raise concerns about the legitimacy of the application intent.

- Previous denials or extensive searches for coverage may prompt insurers to investigate further and potentially reject the application.

Frequently Asked Questions

Why was my life insurance application declined?

Life insurance applications may be declined due to health issues, high-risk occupations, lifestyle choices (like smoking or extreme hobbies), or previous medical history. Insurers assess your risk level, and if it's too high, they may deny coverage. Results from medical exams or inaccurate information on the application can also lead to a decline. Each insurer has specific criteria, so one denial doesn't mean all companies will reject you.

Can I reapply for life insurance after a denial?

Yes, you can reapply for life insurance after being declined, but timing matters. Wait until your health improves or circumstances change, like quitting smoking or managing a medical condition. Consider applying with a different insurer, as underwriting guidelines vary. Working with an experienced agent can help you find a better fit. Be honest on your new application to increase chances of approval and avoid future issues.

Will a life insurance decline affect other insurance applications?

A life insurance decline may be shared between insurers if they access your application history through the MIB (Medical Information Bureau). This could influence other applications, such as disability or long-term care insurance. However, not all companies use MIB reports. Being transparent and improving your health before reapplying can reduce negative impacts. Always disclose past declines when required to maintain credibility.

What are my alternatives if life insurance is denied?

If traditional life insurance is denied, consider alternatives like guaranteed issue life insurance, which doesn’t require a medical exam but has higher premiums and lower coverage. Group life insurance through an employer may also be an option. Accidental death policies or final expense insurance can provide some protection. Additionally, improving your health could make you eligible for standard policies in the future. Consult a financial advisor for personalized guidance.

Leave a Reply