Life Insurance No Exam Policy

Life insurance no exam policies offer a simplified way to secure financial protection without the need for a medical examination.

These policies are designed for individuals seeking quick and convenient coverage, often with minimal health questions. While they may come with higher premiums compared to traditional life insurance, they provide accessibility for those who may not qualify due to medical history or time constraints.

No-exam policies can be issued rapidly, sometimes within days, making them ideal for urgent coverage needs. Understanding the benefits and limitations helps individuals make informed decisions when choosing the right life insurance option for their unique circumstances.

Business Insurance Statistics

Business Insurance StatisticsUnderstanding Life Insurance No Exam Policies: A Convenient Option for Immediate Coverage

Life insurance no exam policies offer a streamlined approach to obtaining life insurance without the need for a medical examination, making them an attractive option for individuals seeking quick and hassle-free coverage.

These policies are particularly beneficial for those who may have underlying health conditions, dislike medical exams, or simply want to avoid the time and effort typically associated with the traditional underwriting process. Instead of requiring lab tests or doctor visits, insurers evaluate applicants based on their medical history, prescription records, lifestyle factors, and sometimes a phone interview.

While no exam policies often come with higher premiums due to the increased risk for the insurer, they provide valuable access to coverage for people who might otherwise be declined or delayed in obtaining protection. The application process is generally faster, with some policies offering approval in just days, enabling individuals to secure financial protection for their loved ones promptly.

How No Exam Life Insurance Works: The Application and Approval Process

No exam life insurance simplifies the underwriting process by eliminating the need for physical medical exams, lab tests, or doctor visits. Instead, insurers rely on alternative methods to assess risk, such as reviewing medical records, prescription history, motor vehicle reports, and completing a detailed health questionnaire.

Business Insurance Westminster MD

Business Insurance Westminster MDSome companies may conduct a tele-interview with the applicant to clarify health or lifestyle details. Depending on the insurer and policy type, applicants may be required to sign a medical release form allowing the insurance company to access their health data from external databases like the Medical Information Bureau (MIB) or prescription drug monitoring systems.

Approval times are typically faster than traditional policies—often within 1 to 2 weeks—making no exam life insurance a practical solution for those in need of immediate coverage without medical delays.

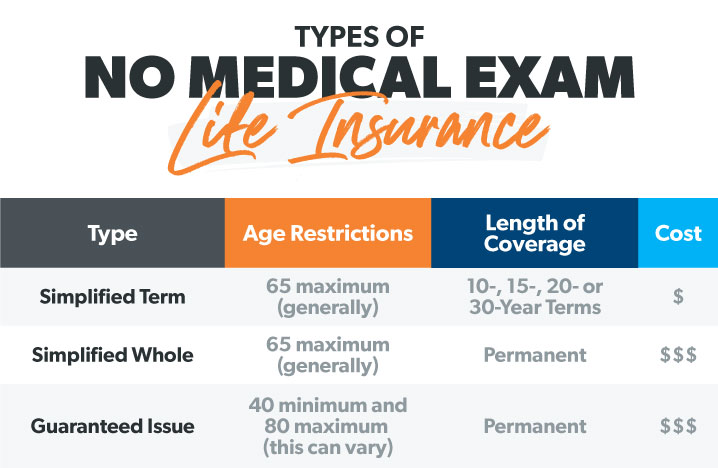

Types of No Exam Life Insurance Policies: Term vs. Permanent Options

There are primarily two types of no exam life insurance: term life and permanent life insurance. No-exam term life provides coverage for a specific period—commonly 10, 15, 20, or 30 years—and pays a death benefit if the insured passes away during the term.

These policies are generally more affordable, making them ideal for temporary needs like income replacement or mortgage protection. On the other hand, no-exam permanent life insurance, such as guaranteed issue whole life or simplified issue whole life, offers lifelong coverage and often includes a cash value component that grows over time.

Business Investment Insurance

Business Investment InsuranceWhile permanent no-exam policies are more expensive, they provide long-term security and are frequently used for final expense planning or estate purposes. Both options vary in eligibility requirements and coverage amounts, so it’s essential to compare offerings across multiple insurers.

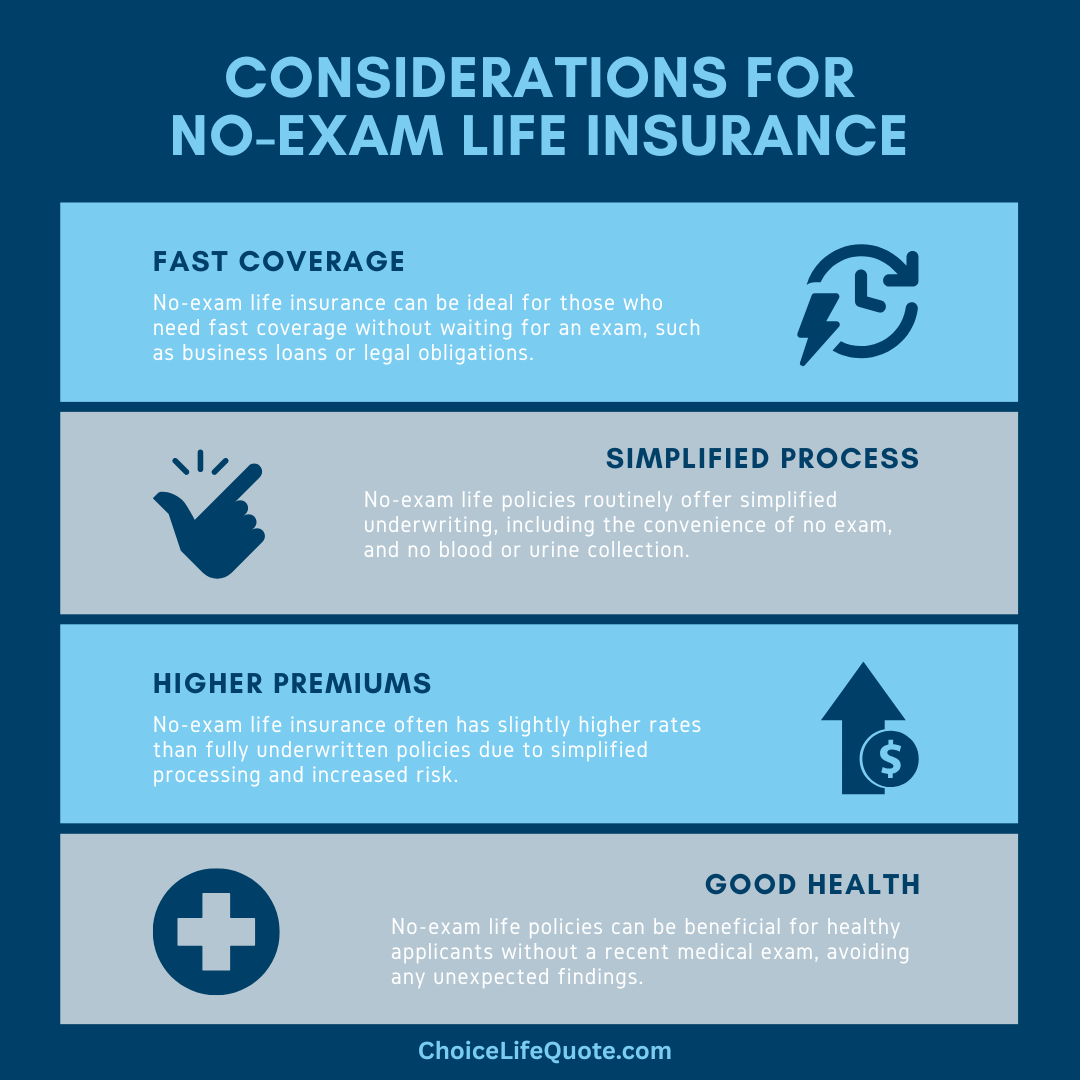

Pros and Cons of Skipping the Medical Exam: Weighing the Benefits and Limitations

Opting for a no exam life insurance policy comes with several notable advantages, including faster approval, minimal hassle, and accessibility for individuals with health concerns. Without the need for blood draws or EKGs, the application process is more convenient and private. However, there are trade-offs to consider.

Premiums are generally higher than those for medically underwritten policies because insurers assume more risk without direct medical data. Additionally, coverage amounts tend to be lower—often limited to $25,000 to $50,000 for guaranteed issue policies—making them less suitable for larger financial obligations.

Some policies also include a graded death benefit during the first two to three years, meaning beneficiaries receive limited or no payout if the insured dies of natural causes during that period. Therefore, while no exam policies offer essential protection for many, applicants should carefully assess their financial goals and health profile before choosing.

Business Liability Insurance Quotes Online

Business Liability Insurance Quotes Online| Feature | No Exam Term Life | No Exam Whole Life (Simplified Issue) | No Exam Whole Life (Guaranteed Issue) |

|---|---|---|---|

| Medical Exam Required? | No | No | No |

| Underwriting Process | Simplified (health questionnaire) | Simplified (health questions + records) | Guaranteed (no health questions) |

| Coverage Amount Range | $50,000 – $2 million | $5,000 – $100,000 | $5,000 – $25,000 |

| Policy Duration | 10–30 years | Lifetime | Lifetime |

| Death Benefit Payout | Full amount if death occurs during term | Full amount after waiting period | Graded benefits in first 2–3 years |

| Cash Value Accumulation | No | Yes | Yes (minimal) |

| Best For | Temporary needs, higher coverage needs | Lifelong coverage, moderate health issues | Seniors, serious health conditions |

Guide to No Exam Life Insurance Policies: Types, Benefits, and Considerations

Is it possible to obtain a life insurance policy without a medical exam?

Yes, it is possible to obtain a life insurance policy without a medical exam. These types of policies are commonly referred to as no medical exam life insurance and are designed to offer a faster, more convenient application process.

Instead of requiring lab tests or a physical examination, insurers typically rely on your medical history, prescription records, and sometimes a phone interview to assess your risk. While this option provides greater accessibility, it often comes with higher premiums or lower coverage amounts compared to traditional policies that include medical underwriting.

Types of No-Exam Life Insurance Policies

- Guaranteed Issue Life Insurance: This type of policy guarantees approval without a medical exam or health questions, making it accessible even for individuals with serious health conditions. However, coverage amounts are typically low, and premiums are relatively high. There is also usually a waiting period before the full death benefit is payable.

- simplified Issue Life Insurance: This policy does not require a medical exam but does involve answering a few health-related questions. The insurer may review your medical records or prescription history. Coverage amounts are higher than guaranteed issue policies, and premiums are based on your self-reported health and lifestyle factors.

- Accelerated Underwriting Policies: Some insurers offer traditional term life insurance with an expedited process that uses advanced data analytics to assess risk. While no in-person medical exam is needed, the company reviews your medical history, lab data from previous tests, and other personal information to make a decision quickly.

Pros and Cons of Skipping the Medical Exam

- Convenience and Speed: One of the biggest advantages is the streamlined application process. You can often get approved within days without visiting a doctor or giving blood samples, making it ideal for those who need coverage quickly or prefer to avoid medical exams.

- Potential for Higher Premiums: Since the insurer has less information to evaluate your health, they assume greater risk. As a result, premiums for no-exam policies are typically higher than for medically underwritten policies with the same death benefit.

- Limited Coverage Options: No-exam policies often have caps on the maximum death benefit available. This makes them less suitable for individuals who need substantial coverage to replace income or pay off large debts.

Who Should Consider No-Exam Life Insurance?

- Individuals with Health Concerns: People who may be declined for traditional insurance due to pre-existing conditions often find no-exam policies more accessible, especially guaranteed issue plans that do not require health disclosures.

- Those Seeking Quick Coverage: If you need life insurance promptly—perhaps for a loan, mortgage, or family planning—a no-exam policy can provide fast approval and peace of mind without delays.

- People Unwilling to Undergo Medical Tests: For applicants who are uncomfortable with medical exams or have difficulty scheduling appointments, skipping the exam offers a practical alternative, particularly with modern online application options.

Are no-exam life insurance policies legitimate and reliable?

Business Owners Insurance Charlotte

Business Owners Insurance CharlotteWhat Are No-Exam Life Insurance Policies?

- No-exam life insurance policies are a type of life insurance that allows applicants to obtain coverage without undergoing a traditional medical examination. Instead, insurers rely on alternative sources of information, such as medical records, prescription history, and health questionnaires, to evaluate an applicant’s risk profile.

- These policies are often faster to approve than fully underwritten policies, with some applicants receiving coverage in as little as a few days. This convenience appeals to individuals who want to avoid doctor visits or have scheduling limitations.

- Common types of no-exam life insurance include simplified issue and guaranteed issue policies. Simplified issue policies typically ask a few health-related questions, while guaranteed issue policies accept almost all applicants regardless of health, though they usually come with lower death benefits and higher premiums.

Are No-Exam Life Insurance Policies Legitimate?

- Yes, no-exam life insurance policies are legitimate and offered by well-known, licensed insurance companies. These policies are regulated by state insurance departments and must comply with the same legal and financial standards as traditional policies.

- Many reputable insurers, including major carriers like John Hancock, Mutual of Omaha, and Haven Life, offer no-exam options. Their legitimacy is further supported by policy validation through third-party data services like MIB or prescription databases.

- While the absence of a medical exam might raise concerns about transparency, the application process still requires honest disclosure. Providing false information can lead to claim denials, which underscores the importance of applying through trustworthy and experienced providers.

How Reliable Are No-Exam Life Insurance Policies?

- The reliability of no-exam life insurance depends on the insurer’s financial strength, policy terms, and the applicant’s eligibility. Policies from companies with high AM Best or Standard & Poor’s ratings are generally more reliable in terms of claim payout and long-term stability.

- While no-exam policies may have limitations—such as lower coverage amounts or higher premiums compared to fully underwritten plans—they are dependable for individuals seeking quick, accessible coverage, especially those with minor health issues that might complicate traditional applications.

- Some no-exam policies include a waiting period before the full death benefit is payable, particularly for deaths due to illness in the first two years. Understanding these terms ensures policyholders have accurate expectations about reliability under different circumstances.

What type of no-exam life insurance policy offers coverage without a medical exam?

A no-exam life insurance policy is designed to provide coverage without requiring the applicant to undergo a medical examination. These policies streamline the application process, making life insurance more accessible to individuals who may want faster approval or who are uncomfortable with or unable to attend a medical exam.

While underwriting standards still apply, insurers instead rely on alternative methods such as reviewing medical records, prescription history, and health questionnaires. The most common type of no-exam life insurance policy that offers coverage without a medical exam is simplified issue life insurance.

Another option includes guaranteed issue life insurance, which requires no medical questions at all, though it typically comes with lower coverage amounts and higher premiums. These policies are particularly suitable for older applicants or those with serious health conditions who might otherwise be denied traditional coverage.

Types of No-Exam Life Insurance Policies Available

- Simplified issue life insurance is one of the most widely available no-exam options. It does not require a medical exam but does involve answering a short series of health-related questions. Based on the answers, the insurer decides whether to approve the policy, often with coverage limits ranging from $50,000 to $500,000 depending on the provider and applicant profile.

- Guaranteed issue life insurance is another type that requires neither a medical exam nor health questions. Because the risk to the insurer is higher, these policies usually offer smaller death benefits, typically between $5,000 and $25,000, and include a graded death benefit period during which only a portion of the benefit is paid out if the policyholder passes away.

- Some insurers also offer accelerated underwriting life insurance, which uses algorithms and data from medical databases, prescription records, and driving history to assess risk without a physical exam. This process is more rigorous than simplified issue but provides faster approval for qualified applicants, often with higher coverage limits and better rates.

How Underwriting Works Without a Medical Exam

- Insurers use alternative sources of information to evaluate risk when no exam is conducted. This may include accessing your medical records through the Medical Information Bureau (MIB) or requesting permission to review your prescription history via pharmacy databases.

- Applicants are often required to complete a health questionnaire that covers topics such as current medical conditions, recent hospitalizations, tobacco use, and participation in high-risk activities. The answers significantly influence the final decision and premium rate.

- Some companies employ predictive analytics and artificial intelligence to assess an applicant’s longevity based on lifestyle data, credit history (where permitted), and public records. This digital underwriting process can result in a decision within days, sometimes even hours, after application submission.

Advantages and Limitations of Skipping the Medical Exam

- One major advantage of no-exam policies is speed and convenience. Applicants can often complete the entire process online and receive approval quickly, which is beneficial for those needing coverage promptly due to life events such as buying a home or planning for estate needs.

- These policies also provide an option for individuals with health issues who might be declined for traditional life insurance. Guaranteed issue policies, in particular, accept nearly all applicants regardless of health, offering a viable safety net for final expenses.

- However, the trade-offs include higher premiums relative to the death benefit, lower maximum coverage amounts, and potential restrictions like waiting periods before full benefits apply. Additionally, inaccurate answers on health questionnaires can lead to claim denials, so transparency remains essential.

Are no-exam life insurance policies typically more costly than traditional policies?

Yes, no-exam life insurance policies are typically more costly than traditional policies when comparing premiums on a like-for-like basis. This higher cost stems from the increased risk that insurance companies take by issuing coverage without requiring a medical exam or extensive health interviews.

Since insurers have less data to assess an applicant’s health, they often price policies higher to offset potential unknown risks. Additionally, no-exam policies may offer lower maximum coverage amounts and fewer underwriting categories, which can limit cost-saving opportunities for applicants in excellent health.

However, for certain individuals—particularly those who are healthy but time-constrained or averse to medical visits—the convenience and speed of approval can justify the higher premiums.

- Without access to comprehensive medical data such as blood work, blood pressure readings, or ECG results, insurers must rely on alternative risk assessment methods, such as prescription history, medical records, or actuarial tables. This lack of direct health verification leads to more conservative pricing to protect against adverse selection.

- Applicants who avoid medical exams might historically be perceived as higher risk, even if they are healthy. Insurers account for this perception by applying higher base rates across the board for no-exam applicants to maintain profitability.

- Traditional policies often place applicants into preferred risk classes (e.g., preferred plus, preferred, standard) based on their health, potentially lowering premiums for healthy individuals. In contrast, no-exam policies often offer fewer or no preferred classes, so even healthy applicants pay rates closer to standard or substandard categories.

Factors That Influence the Cost Difference

- Age and health status play a significant role; younger, healthier applicants may find that the cost difference between no-exam and traditional policies is more pronounced, as they would likely qualify for lower rates in a fully underwritten policy but are grouped into broader risk pools in no-exam options.

- The coverage amount also affects pricing disparities. Lower coverage limits (e.g., $50,000–$100,000) in no-exam policies may have relatively competitive rates, but as the death benefit increases, the lack of medical underwriting causes premiums to rise more steeply than in traditional policies.

- Insurance carriers use different underwriting models for no-exam policies—some rely entirely on automated algorithms using data from medical databases, while others combine limited questionnaires with medical records retrieval. These variations in underwriting rigor can lead to substantial differences in pricing across no-exam products.

When No-Exam Insurance May Be a Cost-Effective Choice

- For individuals with mild health issues or those who might not qualify for preferred ratings even with a medical exam, the price difference between no-exam and traditional policies may be negligible, making the faster approval process of no-exam policies more appealing.

- People who need immediate coverage—such as those purchasing life insurance after a life event like marriage or the birth of a child—may find that the expedited issuance (sometimes within days) outweighs the higher ongoing premiums.

- Some no-exam policies, especially guaranteed issue or simplified issue types, are designed for niche markets, such as seniors or individuals with serious health conditions. In these cases, no-exam insurance may be the only viable option, making it relatively cost-effective by comparison to no coverage at all.

Frequently Asked Questions

What is a life insurance no exam policy?

A life insurance no exam policy is a type of coverage that doesn’t require a medical examination to qualify. Instead, approval is based on your health history, lifestyle, and sometimes lab results from your records. These policies offer faster approval and are convenient for those seeking quick coverage. While premiums may be higher, they provide accessibility for individuals who want to avoid medical tests.

How do no exam life insurance policies work?

No exam life insurance policies work by using your medical records, prescription history, and health questionnaire to assess your risk. Insurers review this information instead of requiring a physical exam. Approval is typically faster, often within days or weeks. These policies usually have coverage limits and may cost more due to the higher risk for the insurer. They're ideal for people who need coverage quickly or prefer to skip medical testing.

Are no exam life insurance policies more expensive?

Yes, no exam life insurance policies tend to be more expensive than traditional policies with medical exams. Without a thorough health evaluation, insurers assume higher risk and may charge higher premiums. Rates vary by age, health condition, and coverage amount. However, they offer convenience and speed, making them worth the extra cost for individuals who need immediate coverage or have difficulty scheduling medical exams.

Who should consider a no exam life insurance policy?

A no exam life insurance policy is ideal for individuals seeking quick coverage without medical testing. It suits those with mild health concerns, busy schedules, or who dislike medical exams. It’s also useful for people needing immediate protection, like new parents or recent homeowners. While premiums are higher, the ease and speed of approval make it a practical option for those prioritizing convenience and fast results.

Leave a Reply